|

市場調查報告書

商品編碼

1842542

光學陶瓷:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030)Optical Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

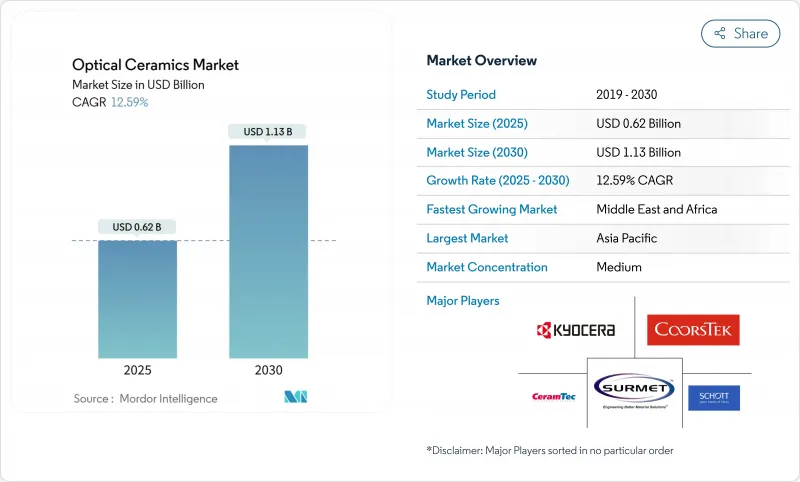

預計2025年光學陶瓷市場規模將達6.2億美元,2030年將成長至11.3億美元,複合年成長率為12.59%。

這一勢頭的推動因素包括:積極的國防採購,尋求輕量化、紅外線滲透性裝甲;多晶YAG在手術雷射中的日益普及;以及對極端溫度能源系統的嚴格性能要求。 「清潔熱等靜壓」(Clean HIP)和真空燒結等生產創新提高了光學透明度,同時降低了缺陷率,促進了其在大面積組件中的廣泛應用。同時,智慧財產權整合以及直徑超過120毫米的組件持續的高產量比率損失限制了新進入者,並使該領域保持中等集中度。國防、醫療和能源需求的交叉加速了跨部門的材料轉移,並壓縮了典型的創新週期。

全球光學陶瓷市場趨勢與洞察

下一代戰鬥車輛將迅速採用紅外線滲透性裝甲

一項國防項目整合了鋁合金和尖晶石窗玻璃,與夾層玻璃相比,其重量減輕高達60%,同時保持了防彈保護性能,並提高了燃油效率和乘員機動性。組件尺寸擴大到8平方英尺的面板,使整車嵌裝玻璃安裝實用化。機器學習引導的層壓方案將厚度減少了22.2%,透射率提高了42.3%,證明了該概念的擴充性。與美國簽訂的供應合約加快了大型組件的認證,並縮短了測試週期。因此,採購機構下達了多年期固定數量和穩定價格的訂單。

需要多晶YAG 光學元件的 UV-LED 和雷射醫療設備的普及

微創手術擴大使用雷射,因為Ho:YAG和Nd:YAG雷射的波長可被水強烈吸收,從而能夠精確切除組織,同時最大限度地減少伴隨加熱。多晶YAG雷射的熱導率優於玻璃,從而能夠實現更高的脈衝能量和更長的組件壽命。製程創新使1064奈米波長的透射率達到83.7%,提高了光轉換效率,並促進了適用於門診的可攜式手術平台的開發。亞洲的合約設備製造商已擴大生產,加速了該地區雷射應用的成長曲線。

熱熱等靜壓線的高資本支出限制了其進入新興市場

商業熱靜壓(HIP)安裝成本通常超過1500萬美元,這給新參與企業設定了較高的財務門檻。壓力容器設計和受控大氣操作方面的專業知識仍然集中在成熟的工業領域,這擴大了能力差距。諸如「清潔熱靜壓」和「轉向冷卻」等升級雖然提高了性能,但也增加了資本密集度,從而強化了現有企業的優勢。

細分分析

YAG 憑藉其在工業雷射、閃爍體和感測光學領域的多功能性,在 2024 年光學陶瓷市場中保持 30.2% 的主導地位。多項燒結改進提高了 1064 nm 的透射率,改善了 10kW 級雷射切割機的光束品質。 ALON 的複合年成長率為 12.3%,滿足了國防和航太領域對輕型彈道級窗口的嚴格要求。藍寶石憑藉其無與倫比的硬度(Moci 9)和高達 2,000 度C 的熱穩定性,在能源領域保持了忠誠度。尖晶石的立方晶格消除了屈光並支援航空成像。氧化釔在半導體工廠等電漿蝕刻室襯裡的用途穩步擴大。新興的鎦石榴石顯示出下一代閃爍體的前景。

YAG 系統中光學陶瓷的市場規模預計將以每年 11.6% 的速度成長,而 ALON 的不斷成長的佔有率預計將在 YAG 產量不顯著下降的情況下提升整個行業的價值。目前,YAG 和 ALON 的雙重採購在供應鏈中已很常見,混合材料組件體現的是設計最佳化,而非嚴格的替代方案。

熱等靜壓透過生產接近理論密度且孔隙率低的零件,確保了2024年41.3%的收入成長,這對於防彈裝甲和高功率光學元件至關重要。氣體純化室等製程改進提高了更大尺寸面板的產量比率,增強了熱等靜壓技術在高級產品領域的經濟優勢。然而,真空燒結技術實現了11.2%的最高複合年成長率,因為它在較低的單位能量下實現了透明氧化鋁70%的透射率,對成本敏感的行業具有吸引力。固體燒結仍然適用於較簡單的幾何形狀,而隨著研究人員列印漸變折射率元件,積層製造加入了「其他」類別。

到2030年,隨著真空燒結規模的擴大,HIP在光學陶瓷市場的佔有率可能會略有下降,但隨著更大型的裝甲組件推動產量成長,HIP爐的整體產量預計將上升。目前正在評估將真空預燒結與最終HIP緻密化相結合的混合流程,以平衡透明度和成本。

光學陶瓷行業材料類型(釔鋁石榴石等)、製造方法(固體燒結等)、產品類型(多晶、單晶)、應用(透明裝甲、防彈窗等)、最終用途行業(航太、國防、醫療保健等)和地區(北美、南美、歐洲、亞太、中東和非洲)細分。

區域分析

受中國電池組雷射的快速擴張以及日本對輕型衛星光學元件的關注推動,亞太地區將在2024年引領光學陶瓷市場,佔38.3%的收入佔有率。韓國和台灣地區則新增了專門生產陶瓷閃光燈和感測器窗口的工廠。日本的《精細陶瓷藍圖2050》等政府舉措已規劃出長期的技術需求。

北美憑藉著雄厚的國防費用,尤其是美國升級透明裝甲和雷射系統的項目,保持了巨大的市場佔有率。桑迪亞國家實驗室和私人企業組成的合作叢集,透過以基於物理的建模取代反覆試驗,縮短了開發週期。加拿大和墨西哥貢獻了專業的製造和研發能力,確保了北美供應鏈的韌性。

中東和非洲的複合年成長率最快,為 11.2%,其中沙烏地阿拉伯和阿拉伯聯合大公國資助了 ALON 生產的機載紅外線感測器圓頂,以色列陶瓷和矽酸鹽研究所實現了區域技術轉讓,促進了國內彈道飛彈裝甲的發展。

歐洲在渦輪機高溫藍寶石窗口和科學研究精密光學領域擁有豐富的專業知識。德國和英國推動了產品創新,北歐叢集率先使用氫燃窯爐,以減少陶瓷加工的碳排放。南美洲從小規模發展起來,巴西和阿根廷利用當地礦產資源,將藍寶石檢測口引入精煉和醫療保健領域。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 下一代戰鬥車輛將迅速採用紅外線透明裝甲

- 需要多晶YAG 光學元件的 UV-LED 和雷射醫療設備的普及

- 高溫燃氣渦輪機檢測的成長需要藍寶石窗口

- 太空船重量減輕增強了低地球軌道衛星的 ALON/尖晶石視口

- 大面積鋰離子電池組雷射器,附陶瓷閃光燈

- 分配給陶瓷圓頂機載紅外線感測器的軍事現代化預算

- 市場限制

- 熱等靜壓線的高資本投入限制了其進入新興市場

- 如果直徑超過120毫米,就會出現產量比率損失(15%以上),而且單價與玻璃失去競爭力。

- 5-7µm 波段的透射率有限,限制了較長波長紅外線的採用。

- 超過 120 項美國專利阻礙新配方

- 價值鏈分析

- 技術展望

- 監理展望

- 五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 投資及資本趨勢分析

- 宏觀經濟因素的影響

第5章市場規模及成長預測

- 依材料類型

- 釔鋁石榴石(YAG)

- 氮氧化鋁(ALON)

- 尖晶石

- 藍寶石

- 氧化釔

- 其他

- 依製造方法

- 固體燒結

- 熱等靜壓(HIP)

- 真空燒結

- 其他

- 依產品類型

- 多晶

- 單晶

- 按用途

- 透明裝甲和防彈窗

- 感測器和成像光學元件

- 雷射和照明組件

- 醫學影像和診斷

- LED 和磷光體

- 用於能源和發電的光學元件

- 其他

- 按行業

- 航太/國防

- 衛生保健

- 能源

- 消費性電子產品

- 工業和製造業

- 研究和測量設備

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家(瑞典、芬蘭、挪威、丹麥)

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 台灣

- 其他亞太地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Surmet Corporation

- CoorsTek Inc.

- CeramTec GmbH

- CeraNova Corporation

- Schott AG

- Saint-Gobain SA

- Kyocera Corporation

- Murata Manufacturing Co., Ltd.

- Konoshima Chemical Co., Ltd.

- Ceradyne Inc.(3M)

- II-VI Incorporated/Coherent Corp.

- Rubicon Technology Inc.

- Adamant Namiki Precision Jewel Co., Ltd.

- Crystalwise Technology Inc.

- Advanced Ceramics Manufacturing LLC

- AGC Inc.

- Baikowski SA

- Zhongke Jingcheng New Material Co., Ltd.

- Sinoma Advanced Nitride Ceramics Co., Ltd.

- SICCAS High-Tech Materials Co., Ltd.

- American Elements

- Toshima Manufacturing Co., Ltd.

- Ceratec Technical Ceramics BV

- Tera YAG Co., Ltd.

- Precision Ceramics International Ltd.

- Blasch Precision Ceramics Inc.

第7章 市場機會與未來展望

The optical ceramics market size stood at USD 0.62 billion in 2025 and is forecast to grow to USD 1.13 billion by 2030, registering a 12.59% CAGR.

Strong defense procurement for lighter, infrared-transparent armor, rising use of polycrystalline YAG in surgical lasers, and stricter performance demands in extreme-temperature energy systems supported this momentum. Production innovations such as 'Clean HIP' and vacuum sintering lifted optical clarity while lowering defect rates, encouraging wider use in large-area components. Meanwhile, intellectual-property consolidation and persistently high yield losses for parts above 120 mm diameters limited new entrants, keeping the field moderately concentrated. The intersection of defense, medical, and energy requirements accelerated material transfer across sectors, compressing typical innovation cycles.

Global Optical Ceramics Market Trends and Insights

Rapid Adoption of IR-Transparent Armor in Next-Gen Combat Vehicles

Defense programs integrated ALON and spinel windows that cut weight up to 60% versus laminated glass while maintaining ballistic stop levels, enhancing fuel efficiency, and crew mobility. Components grew to panel sizes of eight square feet, making full-vehicle glazing practical. Machine-learning-guided stacking schemes lowered thickness 22.2% yet raised transmission 42.3%, proving the concept's scalability. Supply contracts from the U.S. Army accelerated the qualification of larger parts and shortened testing cycles. As a result, procurement agencies issued multi-year orders that locked in volume and stabilized pricing.

Surge in UV-LED and Laser-Based Medical Devices Demanding Polycrystalline YAG Optics

Minimally invasive therapies increasingly relied on Ho:YAG and Nd:YAG lasers whose wavelengths are strongly absorbed by water, ensuring precise tissue removal with limited collateral heating. Polycrystalline YAG offered improved thermal conductivity over glass, enabling higher pulse-energy operation and longer component lifetimes. Process innovations delivered 83.7% transmittance at 1064 nm, lifting wall-plug efficiency and facilitating portable surgical platforms well suited to outpatient clinics. Asian contract-device makers expanded production, accelerating regional adoption curves.

Capex-Intensive Hot-Isostatic-Pressing Lines Limiting Emerging-Market Entry

Commercial HIP installations often exceeded USD 15 million, creating high financial thresholds for newcomers. Expertise in pressure-vessel design and controlled-atmosphere operations remained concentrated in mature industrial regions, widening the capability gap. Upgrades such as 'Clean HIP' and 'Steered Cooling' improved performance but also raised capital intensity, reinforcing incumbent advantages.

Other drivers and restraints analyzed in the detailed report include:

- Growth of High-Temperature Gas-Turbine Inspections That Require Sapphire Windows

- Spacecraft Light-Weighting Drives ALON/Spinel Viewports in LEO Satellites

- Yield Losses Above 15% for 120 mm-Diameter Components Keep Unit Costs Uncompetitive vs. Glass

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

YAG retained 30.2% dominance within the optical ceramics market in 2024 through versatility across industrial lasers, scintillators, and sensing optics. Multiple sintering refinements elevated its 1064 nm transmittance, improving beam quality in 10 kW-class laser cutters. ALON posted a 12.3% CAGR by fulfilling aggressive defense and space specifications for lightweight yet ballistic-grade windows. Sapphire maintained energy-sector loyalty thanks to unmatched hardness (Mohs 9) and 2,000 °C thermal stability. Spinel's cubic lattice removed birefringence, supporting airborne imaging. Yttria expanded steadily for plasma-etch chamber liners in semiconductor fabs. Emerging lutetium-based garnets showed promise in next-generation scintillators.

The optical ceramics market size for YAG systems is projected to rise at 11.6% annually, while ALON share gains are forecast to elevate total industry value without materially eroding YAG volumes. Supply chains now routinely dual-source YAG and ALON to tailor mixed-material assemblies, reflecting design optimization rather than strict substitution.

Hot isostatic pressing secured 41.3% revenue in 2024 by producing near-theoretical-density parts with low porosity, essential for ballistic armor and high-power optics. Process refinements like gas-purified chambers raised yield in large panels, reinforcing HIP's economic edge in premium products. Vacuum sintering, however, posted the highest 11.2% CAGR outlook by delivering 70% transmittance in transparent alumina at lower unit energy, appealing to cost-sensitive sectors. Solid-state sintering kept relevance for simpler geometries, while additive manufacturing joined the "Others" category as researchers printed gradient-index elements.

Through 2030, the optical ceramics market share for HIP may slip modestly as vacuum sintering scales, yet overall output from HIP furnaces will climb because larger armor sets drive volume. Hybrid flows that combine vacuum pre-sintering with final HIP densification are under evaluation to balance clarity and cost.

Optical Ceramics Industry is Segmented by Material Type (Yttrium Aluminum Garnet, and More), Fabrication Method (Solid-State Sintering, and More), Product Type (Polycrystalline and Monocrystalline), Application (Transparent Armor and Bullet-Resistant Windows, and More), End-Use Industry (Aerospace and Defense, Healthcare, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific led the optical ceramics market with 38.3% 2024 revenue thanks to China's rapid battery-pack laser expansion and Japan's focus on light-weighted satellite optics. South Korea and Taiwan added fabs specializing in ceramic flash lamps and sensor windows. Government initiatives such as Japan's Fine Ceramics Roadmap 2050 mapped long-range technology needs.

North America leveraged strong defense spending, particularly U.S. programs upgrading transparent armor and laser systems, maintaining a sizeable share. Collaborative clusters involving Sandia National Laboratories and private industry shortened development cycles by replacing trial-and-error with physics-based modeling. Canada and Mexico contributed specialized production and R&D, securing resiliency in North American supply chains.

The Middle East and Africa recorded the fastest 11.2% CAGR, with Saudi Arabia and the United Arab Emirates funding airborne IR sensor domes built from ALON. Israel's Ceramic and Silicate Institute enabled regional know-how transfer, fostering domestic ballistic-grade armor developments.

Europe retained critical expertise in high-temperature sapphire windows for turbines and precision optics for scientific research. Germany and the United Kingdom drove product innovation, while the Nordic cluster pioneered hydrogen-fired kilns to cut carbon footprints in ceramic processing. South America grew from a small base as Brazil and Argentina introduced sapphire inspection ports in refining and healthcare sectors, leveraging local mineral resources.

- Surmet Corporation

- CoorsTek Inc.

- CeramTec GmbH

- CeraNova Corporation

- Schott AG

- Saint-Gobain S.A.

- Kyocera Corporation

- Murata Manufacturing Co., Ltd.

- Konoshima Chemical Co., Ltd.

- Ceradyne Inc. (3M)

- II-VI Incorporated / Coherent Corp.

- Rubicon Technology Inc.

- Adamant Namiki Precision Jewel Co., Ltd.

- Crystalwise Technology Inc.

- Advanced Ceramics Manufacturing LLC

- AGC Inc.

- Baikowski SA

- Zhongke Jingcheng New Material Co., Ltd.

- Sinoma Advanced Nitride Ceramics Co., Ltd.

- SICCAS High-Tech Materials Co., Ltd.

- American Elements

- Toshima Manufacturing Co., Ltd.

- Ceratec Technical Ceramics BV

- Tera YAG Co., Ltd.

- Precision Ceramics International Ltd.

- Blasch Precision Ceramics Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of infra-red transparent armor in next-gen combat vehicles

- 4.2.2 Surge in UV-LED and laser-based medical devices demanding polycrystalline YAG optics

- 4.2.3 Growth of high-temperature gas-turbine inspections that require sapphire windows

- 4.2.4 Spacecraft light-weighting drives ALON/spinel viewports in LEO satellites

- 4.2.5 Large-area Li-ion battery pack lasers using ceramic flash lamps

- 4.2.6 Military modernization budgets earmarked for airborne IR sensors with ceramic domes

- 4.3 Market Restraints

- 4.3.1 Capex-intensive hot-isostatic-pressing lines limiting emerging-market entry

- 4.3.2 Yield-losses (>15 %) above 120 mm diameter keep unit costs uncompetitive vs. glass

- 4.3.3 Limited transmittance in the 5-7 µm band constrains long-wave IR adoption

- 4.3.4 IP consolidation-over 120 active U.S. patents block new formulations

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment and Funding Trends Analysis

- 4.9 Impact of Macroeconomic factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Yttrium Aluminum Garnet (YAG)

- 5.1.2 Aluminum Oxynitride (ALON)

- 5.1.3 Spinel

- 5.1.4 Sapphire

- 5.1.5 Yttria

- 5.1.6 Others

- 5.2 By Fabrication Method

- 5.2.1 Solid-state Sintering

- 5.2.2 Hot Isostatic Pressing (HIP)

- 5.2.3 Vacuum Sintering

- 5.2.4 Others

- 5.3 By Product Type

- 5.3.1 Polycrystalline

- 5.3.2 Monocrystalline

- 5.4 By Application

- 5.4.1 Transparent Armor and Bullet-resistant Windows

- 5.4.2 Sensor and Imaging Optics

- 5.4.3 Laser and Lighting Components

- 5.4.4 Medical Imaging and Diagnostics

- 5.4.5 LEDs and Phosphors

- 5.4.6 Energy and Power Generation Optics

- 5.4.7 Others

- 5.5 By End-Use Industry

- 5.5.1 Aerospace and Defense

- 5.5.2 Healthcare

- 5.5.3 Energy

- 5.5.4 Consumer Electronics

- 5.5.5 Industrial and Manufacturing

- 5.5.6 Research and Instrumentation

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Nordics (Sweden, Finland, Norway, Denmark)

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 Taiwan

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Surmet Corporation

- 6.4.2 CoorsTek Inc.

- 6.4.3 CeramTec GmbH

- 6.4.4 CeraNova Corporation

- 6.4.5 Schott AG

- 6.4.6 Saint-Gobain S.A.

- 6.4.7 Kyocera Corporation

- 6.4.8 Murata Manufacturing Co., Ltd.

- 6.4.9 Konoshima Chemical Co., Ltd.

- 6.4.10 Ceradyne Inc. (3M)

- 6.4.11 II-VI Incorporated / Coherent Corp.

- 6.4.12 Rubicon Technology Inc.

- 6.4.13 Adamant Namiki Precision Jewel Co., Ltd.

- 6.4.14 Crystalwise Technology Inc.

- 6.4.15 Advanced Ceramics Manufacturing LLC

- 6.4.16 AGC Inc.

- 6.4.17 Baikowski SA

- 6.4.18 Zhongke Jingcheng New Material Co., Ltd.

- 6.4.19 Sinoma Advanced Nitride Ceramics Co., Ltd.

- 6.4.20 SICCAS High-Tech Materials Co., Ltd.

- 6.4.21 American Elements

- 6.4.22 Toshima Manufacturing Co., Ltd.

- 6.4.23 Ceratec Technical Ceramics BV

- 6.4.24 Tera YAG Co., Ltd.

- 6.4.25 Precision Ceramics International Ltd.

- 6.4.26 Blasch Precision Ceramics Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

光學陶瓷市場:依產品類型、形狀、塗層類型及最終用途產業分類-2026-2032年全球市場預測

光學陶瓷市場:依產品類型、形狀、塗層類型及最終用途產業分類-2026-2032年全球市場預測 2026年全球透明陶瓷市場研究報告

2026年全球透明陶瓷市場研究報告 2026-2034年全球透明陶瓷市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球透明陶瓷市場規模、佔有率、趨勢和成長分析報告 透明陶瓷市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、材料、最終用途產業、地區及競爭格局分類,2021-2031年)

透明陶瓷市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、材料、最終用途產業、地區及競爭格局分類,2021-2031年) 2026-2030年全球透明陶瓷市場

2026-2030年全球透明陶瓷市場 光學陶瓷市場規模、佔有率和成長分析(按材料、最終用途和地區分類)—產業預測(2026-2033 年)透明陶瓷市場(按材料、形式和最終用戶分類)—2025-2032 年全球預測光學陶瓷市場-全球產業規模、佔有率、趨勢、機會及預測(按材料類型、應用、最終用戶、地區和競爭細分,2020-2030 年)

光學陶瓷市場規模、佔有率和成長分析(按材料、最終用途和地區分類)—產業預測(2026-2033 年)透明陶瓷市場(按材料、形式和最終用戶分類)—2025-2032 年全球預測光學陶瓷市場-全球產業規模、佔有率、趨勢、機會及預測(按材料類型、應用、最終用戶、地區和競爭細分,2020-2030 年) 全球光學陶瓷市場

全球光學陶瓷市場 2032年透明陶瓷市場預測:按類型、材料、製造流程、最終用戶和地區進行的全球分析

2032年透明陶瓷市場預測:按類型、材料、製造流程、最終用戶和地區進行的全球分析