|

市場調查報告書

商品編碼

1842468

電致變色材料:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Electrochromic Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

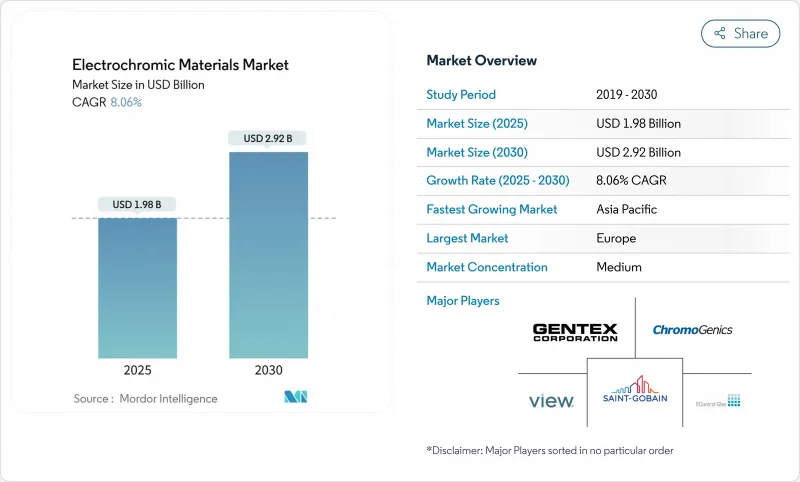

預計2025年電致變色材料市場規模將達19.8億美元,2030年將成長至29.2億美元,複合年成長率為8.06%。

這一成長反映了強制性能源效率法規的訂定、設備成本的下降以及在建築、汽車和飛機領域的快速商業化。動態嵌裝玻璃可將建築的冷卻負載降低高達39.5%,這使得電致變色材料市場成為淨零能耗建築的理想解決方案。成本方面的突破已將智慧窗戶的價格從每平方公尺180-250美元降至每平方公尺80美元,從而刺激了更廣泛的改裝應用。歐洲憑藉嚴格的碳排放法規引領產業發展,而亞太地區則在都市化和基礎設施項目的推動下經歷快速成長。產品創新著重於氧化鎢的耐久性和聚合物的柔韌性,而競爭對手則專注於擴大低成本生產規模並提高循環穩定性。

全球電致變色材料市場趨勢與洞察

能源效率法規加速智慧窗戶的普及

加州2025年能源法規要求窗牆比超過一定標準的建築必須使用有色嵌裝玻璃,為美國其他州的評估提供了合規模板。 2024年國際節能規範收緊了U係數限值和空氣洩漏閾值,指導建築師採用動態嵌裝玻璃。上海2024年光反射率評級指南使亞太地區法規與歐洲標準一致。亞洲開發銀行強調,建築效率對於快速發展的城市脫碳至關重要,並支持電致變色材料市場的持續需求。 ASHRAE標準90.1-2022明確了一條更傾向於電致變色玻璃而非靜態玻璃的圍護結構合規路徑。

汽車對自動防眩後視鏡和全景天窗的需求

鏡泰公司計劃在2024年出貨超過5,000萬台調光設備,並在2025年國際消費性電子展(CES 2025)上推出了一款以薄膜為基礎的天窗。安比萊特(Ambilight)的第二代全車黑色智慧薄膜可實現40倍調光,並具有高紅外線阻隔性,可滿足電動車的散熱需求。現代的奈米冷卻薄膜可將車內溫度降低10°C,且不會影響視野,與高階電動車的電致變色嵌裝玻璃相得益彰。汽車溫度控管要求和感測器整合趨勢正在將電致變色材料市場拓展到後視鏡以外的領域。

單價高於傳統鍍膜玻璃

傳統電致變色窗戶的成本為每平方公尺180-250美元,阻礙了其大規模應用。預計2024年推出的無電極設備將使成本降至每平方公尺80美元,與Low-E低輻射鍍膜玻璃相當。規模化生產仍然受限於利基市場的產量,但汽車產業的產量顯示其經濟效益正在改善。

細分分析

金屬氧化物將佔2024年營收的49.42%,憑藉氧化鎢久經考驗的穩定性,支撐電致變色材料市場。此細分市場的循環耐久性在60°C下超過10萬次循環,鈦插層WO3可達到85%的光調製深度和95.61%的可逆性。受PEDOT和聚苯胺柔韌性驅動的導電聚合物非常適合可捲曲顯示器,複合年成長率為10.69%。摻雜MoS2的PEDOT可達到70.28%的色深,縮小了效能差距。儘管面臨環保審查,紫羅蘭鹼和普魯士藍仍繼續滿足利基色彩切換需求。

金屬氧化物製造商正轉向與聚合物薄膜相容的薄塗層,而聚合物創新者則正在探索混合有機金屬疊層,以提高抗紫外線性能。氧化銦錫靶材的供應鏈集中在亞洲,而高純度三氧化鎢的供應鏈集中在歐洲,凸顯了材料安全在電致變色材料市場的優先地位。

到2024年,智慧窗戶將維持46.04%的市場佔有率,並將繼續成為電致變色材料市場的支柱,因為成本下降推動了計劃,以平衡日照和太陽能發電。得益於適用於物流標籤、零售貨架和曲面汽車儀錶板的印刷雙穩態薄膜,小型顯示器的複合年成長率達到11.02%。

後視鏡業務保持穩定收益,尤其是在北美輕型汽車領域。薄膜作為汽車改裝件,其市場佔有率正在不斷擴大,而鍍膜技術則能夠實現平板玻璃無法實現的客製化形狀。設備的多功能性使供應商免受單一細分市場週期性波動的影響,並有助於生產計畫。

區域分析

由於2030年碳減排目標的約束性以及綠色改造計劃補貼,歐洲在2024年維持了33.15%的銷售額。瑞典能源署向Chromogenics公司提供了450萬美元的貸款,顯示了對該國電致變色生產能力的政策信心。在德國復興信貸銀行(KfW)的能源效率激勵措施下,德國在智慧窗戶安裝方面處於主導,而英國正在擴大公共建築智慧窗戶的補貼。南歐地區對用於文物維修中眩光控制的高遮光需求日益成長。

亞太地區是成長最快的地區,複合年成長率達11.07%,這得益於中國積極的都市化和光污染監管。上海2024年的反光法規凸顯了監管的收緊。日本充分利用其汽車天窗模組供應鏈,而韓國顯示器巨頭則共同開發軟性電致變色儀錶板。政府的淨零排放藍圖和高電費加速了投資回報的計算,鞏固了電致變色材料市場的發展軌跡。

在北美,加州法規和航太需求推動了電致變色技術的普及。波音和空中巴士的生產線採用了Gentex調光窗,推動了材料銷售的穩定成長。聯邦商業建築節能維修稅額扣抵正在獲得大力支持。南美、中東和非洲地區仍在發展中,但海灣地區的機場和飯店計劃正在試驗能夠管理沙漠太陽能增益的動態建築幕牆,這預示著中期商機。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 能源效率法規加速智慧窗戶的普及

- 汽車對自動防眩後視鏡和全景天窗的需求

- 航太航太窗戶升級,減輕重量並減少眩光

- 用於改裝現有建築的電致變色建築幕牆膜

- 增加政府國防費用

- 市場限制

- 與傳統鍍膜玻璃相比,單價更高

- 關於循環穩定性和耐久性的問題

- 暫停執行紫精廢棄物。

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場規模及成長預測

- 依產品類型

- 紫羅蘭鹼

- 導電聚合物

- 金屬氧化物

- 普魯士藍

- 其他產品類型

- 依設備類型

- 智慧窗戶

- 鏡子

- 展示

- 薄膜和塗層

- 其他設備

- 按外形規格

- 玻璃基板

- 聚合物薄膜

- 墨水和顏料

- 按最終用戶產業

- 車

- 電氣和電子

- 建築/施工

- 航太/國防

- 其他最終用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率(%)/排名分析

- 公司簡介

- Changzhou YAPU new material Co., Ltd.

- ChromoGenics

- Crown Electrokinetics Corp.

- EControl-Glas GmbH & Co. KG

- GENTEX CORPORATION

- KIBING GROUP

- Kinestral Technologies(Halio)

- Ningbo Miruo Electronic Technology Co., Ltd.

- Polytronix, Inc.

- Ricoh

- Saint-Gobain

- View Inc.

- Zhuhai Kaivo Optoelectronic Technology Co., Ltd.

第7章 市場機會與未來展望

The electrochromic materials market stands at USD 1.98 billion in 2025 and is projected to grow to USD 2.92 billion by 2030, advancing at an 8.06% CAGR.

The growth reflects mandatory energy-efficiency codes, falling device costs, and rapid product commercialization across buildings, vehicles, and aircraft. Dynamic glazing lowers building cooling loads by up to 39.5%, positioning the electrochromic materials market as a preferred solution for net-zero construction. Cost breakthroughs have cut smart-window prices to USD 80 per m2 from USD 180-250 per m2, stimulating wider retrofit adoption. Europe leads due to stringent carbon mandates, while Asia-Pacific grows fastest on urbanization and infrastructure programs. Product innovation pivots on tungsten-oxide durability and polymer flexibility, and competitive focus centers on scaling low-cost manufacturing and improving cycling stability.

Global Electrochromic Materials Market Trends and Insights

Energy-efficiency regulations accelerating smart-window adoption

California's 2025 Energy Code requires chromogenic glazing for buildings surpassing specific window-to-wall ratios, creating a compliance template that other U.S. states are evaluating. The 2024 International Energy Conservation Code tightens U-factor limits and air-leakage thresholds, steering architects toward dynamic glazing. Shanghai's 2024 guidelines on light-reflection assessments align Asia-Pacific rules with European norms sthj.sh.gov.cn. The Asian Development Bank underscores building efficiency as vital for decarbonizing rapidly growing cities, supporting sustained demand for the electrochromic materials market. ASHRAE Standard 90.1-2022 clarifies envelope compliance paths that favor electrochromic over static glass.

Automotive demand for auto-dimming mirrors and panoramic sunroofs

Gentex shipped more than 50 million dimmable devices in 2024 and introduced film-based sunroofs at CES 2025, reducing system weight and enabling larger panoramic apertures. Ambilight's second-generation whole-vehicle black smart film delivers 40X dimming with high infrared rejection, addressing electric-vehicle cooling requirements. Hyundai's nano-cooling film cuts cabin temperature by 10 °C without darkening the view, complementing electrochromic glazing in premium EVs. Automotive thermal management mandates and sensor-integration trends are expanding the electrochromic materials market far beyond rearview mirrors.

High unit cost versus conventional coated glass

Traditional electrochromic windows cost USD 180-250 per m2, deterring mass adoption. Electrode-free devices published in 2024 slash cost to USD 80 per m2, signaling a path to parity with low-E glass. Scaling remains limited by niche production volumes, but automotive volumes hint at improving economies.

Other drivers and restraints analyzed in the detailed report include:

- Aerospace window upgrades for weight and glare reduction

- Retro-fit electrochromic facade films for existing buildings

- Cycling-stability and durability challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal oxides accounted for 49.42% of 2024 revenue, anchoring the electrochromic materials market with proven tungsten-oxide stability. The segment's cycling durability surpasses 100,000 cycles at 60 °C, and titanium-intercalated WO3 reaches 85% optical modulation and 95.61% reversibility. Conducting polymers trail yet post a 10.69% CAGR, propelled by PEDOT and polyaniline flexibility that suits rollable displays. MoS2-doped PEDOT achieves 70.28% coloration depth, narrowing performance gaps. Viologens and Prussian Blue serve niche color-switching needs despite environmental scrutiny.

Metal-oxide makers pivot toward thinner coatings compatible with polymer films, while polymer innovators explore hybrid metal-organic stacks to improve UV tolerance. Supply chains remain concentrated in Asia for indium-tin-oxide targets and in Europe for high-purity tungsten trioxide, underscoring material security priorities for the electrochromic materials market

Smart windows retained a 46.04% stake in 2024 and will stay the backbone of the electrochromic materials market as cost drops expand project pipelines. Building-integrated photovoltaics increasingly pair with electrochromic layers to balance daylight and solar power. Displays, though smaller, log an 11.02% CAGR thanks to printed, bi-stable films suited to logistics tags, retail shelving, and curved automotive clusters.

Mirrors remain a stable revenue stream, especially in North American light vehicles. Films gain share in retrofits, while coatings enable custom shapes that flat glass cannot address. Device diversity protects suppliers from single-segment cyclicality and smooths production planning.

The Electrochromic Materials Market Report Segments the Industry by Product Type (Viologens, Conducting Polymers, and More), Device Type (Smart Windows, Mirrors, and More), Form Factor (Glass Substrates, Polymer Films, and More), End-User Industry (Automotive, Electrical and Electronics, and More) and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe retained 33.15% of 2024 revenue, propelled by binding 2030 carbon targets and subsidies for green-renovation projects. Sweden's energy agency converted a USD 4.5 million loan to ChromoGenics, signaling policy trust in domestic electrochromic capacity. Germany leads installations under KfW efficiency incentives, while the United Kingdom extends smart-window grants in public buildings. Southern Europe adds high-insolation demand for glare control in heritage retrofits.

Asia-Pacific is the fastest-growing region at an 11.07% CAGR, underpinned by China's aggressive urbanization and light-pollution rules that favor adaptive facades. Shanghai's 2024 reflection code underscores regulatory tightening. Japan leverages automotive supply chains for sunroof modules, while South Korea's display majors co-develop flexible electrochromic dashboards. Government net-zero roadmaps and high electricity tariffs accelerate payback calculations, cementing the electrochromic materials market trajectory.

North America adopts through leading California codes and aerospace demand. Boeing and Airbus lines integrate Gentex dimmable windows, driving steady material off-take. Federal tax credits for commercial-building energy retrofits add momentum. South America and Middle East & Africa remain nascent; however, Gulf airports and hospitality projects trial dynamic facades to manage desert solar gain, signaling medium-term opportunities.

List of Companies Covered in this Report:

- Changzhou YAPU new material Co., Ltd.

- ChromoGenics

- Crown Electrokinetics Corp.

- EControl-Glas GmbH & Co. KG

- GENTEX CORPORATION

- KIBING GROUP

- Kinestral Technologies (Halio)

- Ningbo Miruo Electronic Technology Co., Ltd.

- Polytronix, Inc.

- Ricoh

- Saint-Gobain

- View Inc.

- Zhuhai Kaivo Optoelectronic Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy-efficiency regulations accelerating smart-window adoption

- 4.2.2 Automotive demand for auto-dimming mirrors and panoramic sunroofs

- 4.2.3 Aerospace window upgrades for weight and glare reduction

- 4.2.4 Retro-fit electrochromic facade films for existing buildings

- 4.2.5 Increase in defense spending by the government

- 4.3 Market Restraints

- 4.3.1 High unit cost versus conventional coated glass

- 4.3.2 Cycling-stability & durability challenges

- 4.3.3 Pending ecotoxicity norms on viologen waste streams

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products & Services

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Viologens

- 5.1.2 Conducting Polymers

- 5.1.3 Metal Oxides

- 5.1.4 Prussian Blue

- 5.1.5 Other Product Types

- 5.2 By Device Type

- 5.2.1 Smart Windows

- 5.2.2 Mirrors

- 5.2.3 Displays

- 5.2.4 Films & Coatings

- 5.2.5 Other Devices

- 5.3 By Form Factor

- 5.3.1 Glass Substrates

- 5.3.2 Polymer Films

- 5.3.3 Inks & Paints

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Electrical and Electronics

- 5.4.3 Building and Construction

- 5.4.4 Aerospace and Defense

- 5.4.5 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Changzhou YAPU new material Co., Ltd.

- 6.4.2 ChromoGenics

- 6.4.3 Crown Electrokinetics Corp.

- 6.4.4 EControl-Glas GmbH & Co. KG

- 6.4.5 GENTEX CORPORATION

- 6.4.6 KIBING GROUP

- 6.4.7 Kinestral Technologies (Halio)

- 6.4.8 Ningbo Miruo Electronic Technology Co., Ltd.

- 6.4.9 Polytronix, Inc.

- 6.4.10 Ricoh

- 6.4.11 Saint-Gobain

- 6.4.12 View Inc.

- 6.4.13 Zhuhai Kaivo Optoelectronic Technology Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026年全球電動變色智慧玻璃市場報告

2026年全球電動變色智慧玻璃市場報告 電致變色玻璃市場報告:按應用、終端用戶產業和地區分類(2026-2034 年)

電致變色玻璃市場報告:按應用、終端用戶產業和地區分類(2026-2034 年) 電致變色材料市場:按材料、應用、最終用戶和產品分類-2026-2032年全球市場預測電致變色玻璃及裝置市場:按產品類型、技術、安裝方式、控制模式和最終用途分類的全球預測,2026年至2032年

電致變色材料市場:按材料、應用、最終用戶和產品分類-2026-2032年全球市場預測電致變色玻璃及裝置市場:按產品類型、技術、安裝方式、控制模式和最終用途分類的全球預測,2026年至2032年 電致變色材料市場規模、佔有率及成長分析(按產品、應用、最終用戶及地區分類)-產業預測,2026-2033年

電致變色材料市場規模、佔有率及成長分析(按產品、應用、最終用戶及地區分類)-產業預測,2026-2033年 電致變色玻璃市場規模、佔有率及成長分析(依材料、產品、終端用戶產業及地區分類)-2026-2033年產業預測

電致變色玻璃市場規模、佔有率及成長分析(依材料、產品、終端用戶產業及地區分類)-2026-2033年產業預測 電致變色玻璃市場 - 預測 2025-2030

電致變色玻璃市場 - 預測 2025-2030 全球電致變色材料市場

全球電致變色材料市場 電致變色材料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

電致變色材料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 電致變色玻璃市場:按應用、最終用途和地區分類

電致變色玻璃市場:按應用、最終用途和地區分類