|

市場調查報告書

商品編碼

1836528

東南亞建築化學品:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Southeast Asia Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

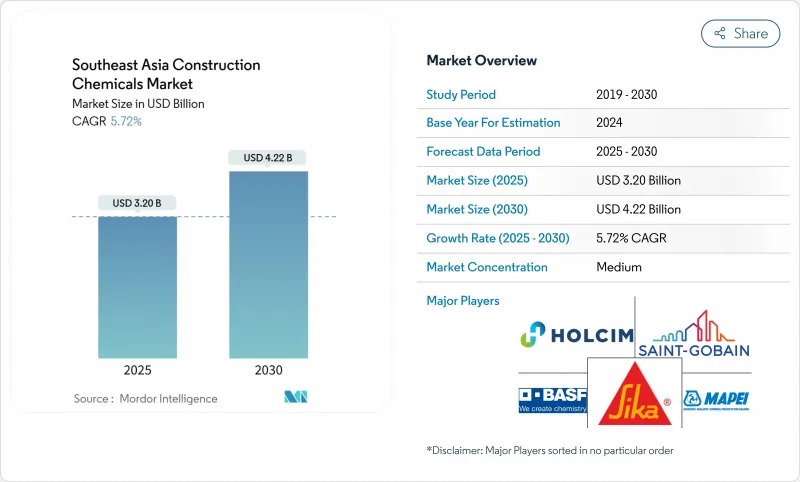

東南亞建築化學品市場預計到2025年將達到32億美元,到2030年將達到42.2億美元,複合年成長率為5.72%。

大型公共基礎設施管道、快速的都市化和更嚴格的性能標準正在推動全部區域對高級外加劑、防水劑和防護塗料的需求。交通走廊、住房和工業園區的公共支出不斷增加,導致每年混凝土澆築量增加,而老化橋樑、港口和建築的維修需求不斷成長,也擴大了高性能修復產品的機會。以新加坡 2025 年持久性化學品法規為首的平行監管壓力正在加速向低 VOC 和生物基配方的轉變。以聖戈班收購 FOSROC 為例,全球供應商之間的整合日益加強,正在加劇東南亞建築化學品市場在創新和服務能力上的競爭。

東南亞建築化學品市場趨勢與洞察

公共基礎設施投資快速成長

各國政府正在加大建設預算,以解決產能瓶頸並刺激經濟成長。印尼已累計423.3 兆印尼幣用於 2024 年的基礎設施建設,其耗資 350 億美元的新首都建設預計將消耗 200 萬噸水泥,這將刺激對混凝土外加劑和防護被覆劑的需求。越南將於 2024 年啟動 13 個交通計劃,總價值 12 億美元,將增加對耐腐蝕塗料和高早強水泥漿的需求。泰國的東部經濟走廊大型企劃和菲律賓彌補 1000 萬套住房供不應求的努力正在加強對防水和密封劑的穩定需求。馬來西亞的建築業在 2024 年上半年成長了 14.6%,這表明財政支出可以轉化為外加劑和修補劑消費的增加。

預製和模組化建築的採用正在蓬勃發展

工業化建築系統縮短了工期,減少了工時,並重建了化學規範。金務大工業建築系統(Gamuda IBS)在馬來西亞建造了一座50層的塔樓,耗時僅為原先的三分之二,這推動了速水泥漿灌漿料和連接膠的廣泛應用。印尼的預製混凝土可節省5-10%的成本,並提高抗震性能,激發了人們對軟性連接材料的興趣。新加坡建屋發展局已在超過70萬套住宅中嵌入了聚合物混凝土,引領了東南亞建築化學品市場的性能標準。在越南,製造業外商投資的增加正推動模組化建築的發展,使用專用密封膠進行異地組裝。

嚴格的VOC和甲醛排放法規

新加坡《環境保護和管理法》修正案要求處理持久性有機污染物必須獲得許可證,這增加了溶劑型產品的合規成本。越南QCVN 01:2025/BYT法規對工作場所70種物質進行了限制,強制要求對傳統黏合劑進行再生產。泰國廣泛的環境框架收緊了工廠排放,導致中小型供應商難以籌集資金研發環保配方。印尼塗料製造商預測其建築業務將繼續成長,但他們警告稱,消費者對高階環保產品的接受度有限,這可能會限制其應用。

報告中分析的其他促進因素和限制因素

- 對水性、低VOC建築解決方案的需求不斷成長

- 基礎設施老化導致維修需求增加

- 技術純熟勞工短缺

細分分析

到2024年,混凝土外加劑將佔東南亞建設化學品市場的33.48%,這將增強其在大型交通和住房項目中的作用。 2024年,印尼的水泥出貨量將達到6,488.7萬噸,再加上越南2025年第一季20%的消費量成長,這為減水劑和凝固劑創造了肥沃的土壤,有助於促進現澆結構的周轉。防護塗料是成長最快的細分市場,複合年成長率為6.75%,用於修復橋樑、橋墩和管道,需要能夠抵抗氯化物侵蝕的高強度環氧樹脂。黏合劑和阻燃劑解決了模組化建築的擴展問題,而防水膜則可以保護暴露於季風循環和高地下水位的計劃。

東南亞建築化學品市場的技術發展軌跡專注於多功能外加劑,旨在縮短週期並減少水泥消費量。西卡對MBCC的整合預計將在2026年產生每年1.8億至2億瑞士法郎的協同效應,從而支持廣泛的產品組合,同時滿足混凝土、地板材料和密封劑的需求。漢高收購了Seal For Life,擴大了其適用於沿海基礎設施的長效防腐蝕包裝產品組合。區域配方師也在局部化添加劑,以應對熱帶濕度和地震應力,從而搶佔不熟悉當地情況的進口市場佔有率。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 公共基礎設施投資快速成長

- 預製和模組化建築的採用激增

- 越來越多採用創新施工程序

- 對水性、低VOC建築解決方案的需求不斷增加

- 基礎設施老化導致維修需求增加

- 市場限制

- 嚴格的VOC和甲醛排放法規

- 原物料價格上漲

- 技術純熟勞工短缺

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模及成長預測(金額)

- 依產品類型

- 膠水

- 混凝土和水泥外加劑

- 阻燃劑

- 保護漆

- 防水劑

- 其他建築化學品(水泥漿、密封劑等)

- 按用途

- 商業

- 工業

- 基礎設施

- 住房

- 按功能

- 提高強度

- 耐用且耐腐蝕

- 防火/防熱

- 美觀和表面光潔度

- 按地區

- 印尼

- 越南

- 菲律賓

- 泰國

- 馬來西亞

- 新加坡

- 其他東南亞地區

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- Akzo Nobel NV

- Arkema

- Ashland

- BASF SE

- Dow

- HB Fuller

- Henkel AG & Co. KGaA

- Holcim

- MAPEI SpA

- Nippon Paint Holdings Co., Ltd.

- Pidilite Industries Ltd.

- RPM International Inc.

- Saint Gobain

- Sika AG

- The Euclid Chemical Company

- Wacker Chemie AG

第7章 市場機會與未來展望

The Southeast Asia construction chemicals market is valued at USD 3.20 billion in 2025 and is forecast to reach USD 4.22 billion by 2030, registering a 5.72% CAGR.

A sizable public-sector infrastructure pipeline, rapid urbanization, and stricter performance standards are increasing demand for advanced admixtures, waterproofing agents, and protective coatings throughout the region. Elevated public spending on transport corridors, housing, and industrial estates is amplifying the volume of concrete placed each year, while swelling renovation needs for aging bridges, ports, and buildings expand opportunities for high-performance repair products. Parallel regulatory pressure, led by Singapore's 2025 restrictions on persistent chemicals, is accelerating the switch toward low-VOC and bio-based formulations. Intensifying consolidation among global suppliers, exemplified by Saint-Gobain's purchase of FOSROC, is raising the competitive bar on both innovation and service capability across the Southeast Asia construction chemicals market.

Southeast Asia Construction Chemicals Market Trends and Insights

Surging Public-sector Infrastructure Investments

Governments are boosting construction budgets to relieve capacity bottlenecks and spur economic growth. Indonesia has earmarked IDR 423.3 trillion for 2024 infrastructure work, while its USD 35 billion New Capital City is expected to consume 2 million tons of cement, stimulating demand for concrete admixtures and protective coatings. Vietnam began 13 transport projects worth USD 1.2 billion in 2024, raising requirements for corrosion-resistant coatings and high-early-strength grouts. Thailand's Eastern Economic Corridor megaprojects and the Philippines' drive to narrow a 10 million-unit housing backlog reinforce a steady call for waterproofing and sealants. Malaysia's 14.6% construction growth in H1 2024 further illustrates how fiscal outlays translate into higher consumption of admixture and repair compounds.

Booming Prefabricated and Modular Building Adoption

Industrialized Building Systems shorten schedules and cut labor hours, reshaping chemical specifications. Gamuda IBS has erected 50-story towers in two-thirds of the traditional timelines in Malaysia, spurring the uptake of fast-setting grouts and connection adhesives. Indonesian precast concrete delivers 5-10% cost savings and enhanced seismic resilience, driving interest in flexible jointing compounds. Singapore's Housing Development Board has embedded polymer concrete in more than 700,000 units, guiding performance benchmarks across the Southeast Asia construction chemicals market. Vietnam's rising foreign investment inflows into manufacturing fuel modular construction that depends on specialty sealants for off-site assembly.

Stringent VOC and Formaldehyde Emission Caps

The Environmental Protection and Management Act amendments in Singapore require handling licences for persistent organic pollutants, adding compliance costs for solvent-borne products. Vietnam's QCVN 01:2025/BYT regulation sets workplace limits on 70 substances, forcing reformulation of legacy adhesives. Thailand's broad environmental framework tightens factory emissions, with smaller suppliers struggling to finance R&D for greener recipes. Indonesian coatings makers project continued construction growth, yet warn that limited consumer acceptance of premium eco-products could restrain uptake.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Water-based, Low-VOC Construction Solutions

- Growing Renovation Requirements Due to Aging Infrastructure

- Lack of Skilled Labour

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Concrete admixtures held a 33.48% slice of the Southeast Asia construction chemicals market in 2024, cementing their role in large-scale transport and housing programs. Indonesia's cement dispatches of 64.887 million tons in 2024, paired with Vietnam's 20% consumption surge in Q1 2025, created fertile territory for water reducers and set-controllers that accelerate turnaround of cast-in-place structures. Protective coatings, the fastest-growing sub-segment at 6.75% CAGR, ride on rehabilitating bridges, wharves and pipelines that need high-build epoxies to resist chloride ingress. Adhesives and flame retardants cater to the expanding modular-building scene, while waterproofing membranes protect projects exposed to monsoon cycles and high groundwater tables.

Technological trajectories within the Southeast Asia construction chemicals market emphasize multi-functional admixtures that shorten cycle times and shrink cement consumption. Sika's integration of MBCC is slated to deliver CHF 180-200 million in annual synergies by 2026, underpinning broader portfolios that address concrete, flooring and sealant demands simultaneously. Henkel's acquisition of Seal For Life enlarges its offering in long-life anticorrosion wraps tailored to coastal infrastructure. Regional formulators also localize additives to match tropical humidity and seismic stresses, winning share from imports less attuned to local job-site realities.

The Southeast Asia Construction Chemicals Market Report Segments the Industry by Product Type (Adhesives, Concrete and Cement Admixtures, Flame Retardants, and More), Application (Commercial, Industrial, Infrastructure, and Residential), Function (Strength Enhancement, Durability and Corrosion Protection, and More), and Geography (Indonesia, Vietnam, Philippines, Thailand, Malaysia, Singapore, and Rest of Southeast Asia).

List of Companies Covered in this Report:

- 3M

- Akzo Nobel N.V.

- Arkema

- Ashland

- BASF SE

- Dow

- H.B. Fuller

- Henkel AG & Co. KGaA

- Holcim

- MAPEI S.p.A.

- Nippon Paint Holdings Co., Ltd.

- Pidilite Industries Ltd.

- RPM International Inc.

- Saint Gobain

- Sika AG

- The Euclid Chemical Company

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Public-sector Infrastructure Investments

- 4.2.2 Booming Prefabricated and Modular Building Adoption

- 4.2.3 Increased Adoption of Innovative Construction Procedures

- 4.2.4 Rising Demand for Water-based, Low-VOC Construction Solutions

- 4.2.5 Growing Renovation Requirements Due to Aging Infrastructure

- 4.3 Market Restraints

- 4.3.1 Stringent VOC and Formaldehyde Emission Caps

- 4.3.2 High Raw-material Price Volatility

- 4.3.3 Lack of Skilled Labour

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Adhesives

- 5.1.2 Concrete and Cement Admixtures

- 5.1.3 Flame Retardants

- 5.1.4 Protective Coatings

- 5.1.5 Water-proofing Chemicals

- 5.1.6 Other Construction Chemicals (Grouts, Sealants, etc.)

- 5.2 By Application

- 5.2.1 Commercial

- 5.2.2 Industrial

- 5.2.3 Infrastructure

- 5.2.4 Residential

- 5.3 By Function

- 5.3.1 Strength Enhancement

- 5.3.2 Durability and Corrosion Protection

- 5.3.3 Fire and Thermal Protection

- 5.3.4 Aesthetic and Surface Finishing

- 5.4 By Geography

- 5.4.1 Indonesia

- 5.4.2 Vietnam

- 5.4.3 Philippines

- 5.4.4 Thailand

- 5.4.5 Malaysia

- 5.4.6 Singapore

- 5.4.7 Rest of Southeast Asia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Arkema

- 6.4.4 Ashland

- 6.4.5 BASF SE

- 6.4.6 Dow

- 6.4.7 H.B. Fuller

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Holcim

- 6.4.10 MAPEI S.p.A.

- 6.4.11 Nippon Paint Holdings Co., Ltd.

- 6.4.12 Pidilite Industries Ltd.

- 6.4.13 RPM International Inc.

- 6.4.14 Saint Gobain

- 6.4.15 Sika AG

- 6.4.16 The Euclid Chemical Company

- 6.4.17 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

建築化學品市場:2026-2032年全球市場預測(依產品類型、技術、劑型、建築類型、應用、最終用戶和通路分類)固定式機械錨栓市場:依產品類型、材料、應用、終端用戶產業及通路分類,全球預測,2026-2032年

建築化學品市場:2026-2032年全球市場預測(依產品類型、技術、劑型、建築類型、應用、最終用戶和通路分類)固定式機械錨栓市場:依產品類型、材料、應用、終端用戶產業及通路分類,全球預測,2026-2032年 建築化學品市場分析及預測(至2035年):類型、產品、應用、形態、材質類型、技術、最終用戶、功能、安裝類型、解決方案

建築化學品市場分析及預測(至2035年):類型、產品、應用、形態、材質類型、技術、最終用戶、功能、安裝類型、解決方案 建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球建築化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球建築化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 建築化學品市場規模、佔有率、趨勢及預測(按類型、應用和地區分類)(2026-2034 年)

建築化學品市場規模、佔有率、趨勢及預測(按類型、應用和地區分類)(2026-2034 年) 2026年全球建築化學品市場報告

2026年全球建築化學品市場報告