|

市場調查報告書

商品編碼

1693924

綜合設施管理:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

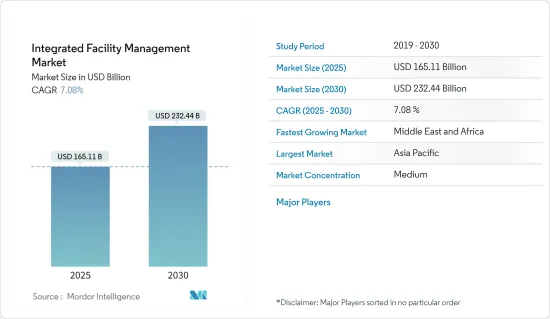

綜合設施管理 (FM) 市場規模預計在 2025 年為 1,651.1 億美元,預計到 2030 年將達到 2,324.4 億美元,預測期內(2025-2030 年)的複合年成長率為 7.08%。

綜合設施管理 (IFM) 主要是指將所有設施管理合約整合到單一服務中。 IFM 將複雜的設施管理與安全、清潔和廢棄物管理等軟設施管理相結合。將這些不同的服務整合在一起將改善客戶服務,增強 FM 服務之間的協作,並整合成本以保持在預算之內。

關鍵亮點

- 對環保永續建築實踐的日益重視以及建設活動的復甦被分析為推動綜合設施管理市場成長的因素。

- 過去幾年,由於各種政府措施推動的建設活動擴大、都市化加快以及已開發經濟體和新興經濟體商業建築計劃的增加,對綜合設施管理服務的需求不斷增加。

- 由於業務擴張導致入住需求增加、技術進步導致設施需求不斷變化以及對成本效率的關注,各行業的商業活動正在回暖,綜合設施管理 (IFM) 正在經歷上升趨勢。

- 日益增強的環境意識和相關商業實踐已經推動綜合設施管理 (IFM) 超越其作為計劃業務促進因素的傳統維護角色。 IFM 不再局限於其作為成本中心的角色,而是成為了產業的策略驅動力。

- 對專業人才的需求是發展全球綜合設施管理市場的一大挑戰。 IFM 涵蓋的服務範圍很廣,從複雜 FM 到軟 FM,而尋找擁有多個類別專業知識的專家非常困難,這意味著人才缺口阻礙了 IFM服務供應商發揮其服務的潛力。

綜合設施管理市場趨勢

商業領域成為最大的終端使用者領域

- 商業房地產涵蓋由商業服務機構建造或占用的辦公大樓,例如企業 IT 和通訊辦公室、製造企業和其他服務供應商。提供必要的設備、室內設計和商業建築裝飾和管理已變得越來越重要,並正在推動商業領域市場的發展。商業區需要物業會計、租賃、合約管理、採購管理等多項服務,需要聘請專業人員。由於這些因素,商業類別在市場上有進一步的成長機會,預計這一趨勢將在整個預測期內持續下去。

- 隨著美國各零售商開設分店並擴大業務範圍,對軟 FM 服務的需求也隨之增加。例如,2023年4月,宜家商店所有者英格卡集團宣布計劃在未來三年內投資20億歐元(22億美元)在美國擴張。根據該計劃,該公司已完成在美國開設 8 家新的大型宜家商場和 9 家小型宜家商場以及對現有商場進行升級,美國是宜家繼德國之後的第二大銷售額市場。

- 此外,世邦魏理仕預計,印度等國家的零售業將在 2023 年顯著成長,該國主要城市的零售面積將創歷史新高,達到 710 萬平方英尺(比 2022 年成長 47%)。零售空間的需求主要受到最近竣工的購物中心的建設所推動。隨著國內外品牌的湧入,時尚服飾佔據了商業區最大的租賃面積。隨著商場零售空間的擴大,消費者流量增加,需要增加維護、清潔、安全和能源管理服務。

- 根據高力國際的一項調查,預計到2023年,辦公大樓和工業/物流房地產將成為房地產投資者最需要的資產類別,全球近60%的投資者打算投資這些類型的房地產。 48% 的受訪者表示多用戶住宅位居第二,其次是飯店。

- 總體而言,商業活動的復甦預計將推動綜合設施管理的需求,以管理不斷增加的運轉率,並採用先進的技術,使企業能夠開展核心活動,同時確保業務順利運作。

亞太地區佔主要市場佔有率

- 亞太地區商業發展日益壯大,醫院、機場、製造工廠、資料中心和教育機構等基礎建設計劃的投資也日益增加。人們對綜合 FM 外包和服務整合優勢的認知不斷提高有望推動市場發展。

- 在中國,許多設施管理者正在採用永續的建築管理實踐來提高職場效率、改善基礎設施並延長資產的使用壽命。綜合設施管理影響組織的各個方面。預計設施經理和戰略管理規劃在該國的地位將變得越來越重要。

- 中國經濟擁有巨大的市場潛力,尤其是上海、北京等商業中心。政府對房地產行業的投資增加預計將為市場帶來成長機會。例如,中國的五年計畫(2021-2025)針對關鍵領域制定了平衡國家經濟的目標。

- 2023年12月,中國汽車製造商比亞迪表示將向韓國汽車製造商KG Mobility投資4.12億美元,以確保電動車電池的穩定供應。該廠計劃於2025年開始量產。韓國是汽車市場主要參與者的所在地,包括 LG Energy Solutions、三星 SDI、SK On 和比亞迪。他們對該工廠的投資對於該國電動車生態系統的發展至關重要。

- 按類型分類,MEP(機械、電氣、管道)和 HVAC(維護服務、企業資產管理等)等硬體維修在亞太地區迅速普及。在設施管理的各個領域,對制定和實施計劃維護計劃以及確保減少設施熱量損失的需求不斷成長,從而提高建築物的能源效率並延長設施的使用壽命,正在推動市場上硬體維修領域的成長。

- 在日本,FM 業者必須應對現場勞動力短缺和老化設施的維護,包括建築物和空調、照明系統等設備。日本生活水準的提高推動了對具有先進安全功能且管理更有效率的建築的需求。這一趨勢在城市地區尤為明顯,預計在預測期內將獲得發展動力。

綜合設施管理產業概況

綜合設施管理市場高度細分,主要企業包括仲量聯行 IP 公司、索迪斯公司、ISS 設施服務公司、世邦魏理仕集團公司和康帕斯Group Limited。該市場的參與企業正在採取合作和收購等策略來加強其產品供應並獲得永續的競爭優勢。

- 2023年12月-仲量聯行宣布將繼續為德州達拉斯、埃爾帕索和聖安東尼德克薩斯州的35家小型醫院和急診部提供綜合設施管理、奧克拉荷馬市管理和能源永續性服務,總面積達100萬平方英尺;內華達州拉斯維加斯;俄克拉荷馬城和匹茲堡;以及威斯康辛州密爾瓦基。

- 2023 年 7 月-EMCOR Group, Inc. 收購位於威斯康辛州的能源效率改善服務供應商 ECM Holding Group, Inc.。該集團相信,ECM的加入將進一步加強其在專業能源效率服務領域的地位,並拓寬其捆綁節能和永續性解決方案的全國組合範圍。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

- 評估影響市場的宏觀經濟因素

第5章市場動態

- 市場促進因素

- 商業活動復甦可望推動經濟成長

- 強調綠色和永續的建築實踐

- 市場限制

- 缺乏專業人員

第6章市場區隔

- 按類型

- 硬體維修

- 軟調頻

- 按最終用戶

- 公共/基礎設施

- 商業的

- 工業的

- 設施

- 其他

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 拉丁美洲

- 澳洲和紐西蘭

第7章競爭格局

- 公司簡介

- Jones Lang LaSalle IP Inc.

- Sodexo Inc.

- ISS Facility Service

- CBRE Group Inc

- Compass Group PLC

- Cushman & Wakefield

- AHI Facility Services Inc

- EMCOR Facility Services

- Facilicom

- CBM Qatar LLC.

第8章投資分析

第9章 市場機會與未來趨勢

The Integrated Facility Management Market size is estimated at USD 165.11 billion in 2025, and is expected to reach USD 232.44 billion by 2030, at a CAGR of 7.08% during the forecast period (2025-2030).

An integrated facilities management (IFM) primarily brings all the facility management contracts under a single service. IFM combines complex facilities management and soft FM, such as security, cleaning, and waste management. Bringing all these different services together under a single umbrella can result in better customer service, better coordination between FM services, and consolidated costs to bring everything in under budget.

Key Highlights

- Growing emphasis on green and sustainable building practices coupled with rebounding construction activity are analyzed as drivers for the growth of the integrated facility management market.

- The growing construction activities due to various government initiatives, rising urbanization, and growing commercial construction projects in developed and developing economies have necessitated the need for integrated facility management services in the past few years.

- Integrated facility management (IFM) is experiencing an upswing due to rebounding commercial activity across various sectors due to the increased need for occupancy due to business expansion; evolving facility needs with technology advancements, and a focus on cost-efficiency.

- Augmented environmental awareness and concerned business practices have pushed integrated facility management (IFM) to exceed its conventional maintenance role as planned business drivers. IFM has appeared as a strategic driver within industries, no longer limited to being a cost center.

- The need for specialized talents poses significant challenges to advancing the integrated facility management market worldwide. The talent gap hinders IFM service providers from delivering the potential of their services as IFM involves a broad range of services from complex FM to soft FM, and finding professionals with expertise in these multiple categories is challenging.

Integrated Facility Management Market Trends

Commercial Segment to be the Largest End-user Segment

- Commercial entities cover office buildings constructed or occupied by business services, such as corporate IT and communication offices, manufacturers, and other service providers. Due to the provision of necessary fitments, interiors, and commercial buildings, decoration and management have gained significant importance, driving the commercial sector market. Commercial spaces require property accounting, renting, contract management, procurement management, and several other services, so hiring professionals becomes necessary. Due to such factors, the commercial category has further growth opportunities in the market, and the trend is likely to continue throughout the forecast period.

- Various retail businesses are expanding their presence by opening new stores in the United States, creating demand for soft FM services. For instance, in April 2023, IKEA store owner Ingka Group announced a plan to spend EUR 2 billion (USD 2.2 billion) expanding in the United States over the next three years. With this plan, the company finalized the opening of eight new big IKEA stores and nine smaller stores and upgraded existing stores in the United States, which is IKEA's second-biggest market by sales after Germany.

- Furthermore, the retail sector in countries like India has shown significant growth during 2023, with the highest record of 7.1 million square feet across key cities in the country, which is 47% more than in 2022, according to CBRE. Recently completed mall constructions primarily led to the demand for retail spaces. Fashion and apparel accounted for the largest leasing of commercial spaces with the expansion of domestic and international brands. Retail space growth in malls is witnessing higher consumer traffic, necessitating robust maintenance, cleaning, security, and energy management services.

- According to a survey by Colliers International, among real estate investors, offices and industrial and logistic properties are expected to be the most demanding asset classes in 2023, with nearly 60% of global investors intending to invest in these types of properties. Multifamily real estate came second with 48% of respondents, followed by hotels.

- Overall, rebounding commercial activities are expected to drive the need for integrated facility management to manage increased occupancy and adopt evolving technologies that allow businesses to address core activities while ensuring smooth business operations.

Asia Pacific to Hold Major Market Share

- The Asia-Pacific region is witnessing an increased development of commercial facilities, with significant investments in infrastructure projects such as hospitals, airports, manufacturing facilities, data centers, and educational institutions, which are expected to drive the Integrated FM market growth. Increasing awareness of Integrated FM outsourcing and service integration benefits is expected to fuel the market's development.

- In China, many facilities managers are incorporating sustainable building management techniques to encourage workplace efficiency and improve the infrastructure to increase asset longevity. Integrated Facility Management impacts every aspect of the organization; a facilities manager's position and the plans for strategic business management will become increasingly strategic in the country.

- China's economy offers an enormous market potential, especially in commercial hubs such as Shanghai and Beijing. Increasing government investments in the country's real estate sector would provide growth opportunities to the market. For instance, China's Five-Year Plan (2021- 2025) targets key areas to balance the country's economy.

- In December 2023, China's automotive company, BYD, announced it would invest USD 412 million to supply South Korea's automaker KG Mobility Co. Ltd with a stable supply of EV batteries. The factory is expected to start mass production in 2025. The country is home to big automotive market players, including LG Energy Solutions, Samsung SDI, SK On, and BYD. Their investment in the factory is crucial to advancing the EV ecosystem in the country.

- By type, hard FM such as MEP (Mechanical, Electrical, Plumbing) and HVAC (Maintenance Services, Enterprise Asset Management, and others) is gaining rapid popularity in Asia-Pacific. Growing demands for creating and operating a planned maintenance schedule across all areas of facility management and enhancing the energy efficiency of buildings by ensuring a reduction in heat loss from premises and lengthening a premise's operational lifespans are propelling the growth of the Hard FM segment in the market.

- In Japan, FM businesses must deal with frontline labor shortages and the upkeep of aging facilities, including buildings and equipment like air-conditioning and lighting systems. Improvements in living standards in the country have escalated demand for buildings equipped with sophisticated security features that can be managed more efficiently. This trend has been particularly evident in urban centers and is expected to gain even more momentum in the forecast period.

Integrated Facility Management Industry Overview

The integrated facility management market is highly fragmented, with significant players like Jones Lang LaSalle IP Inc., Sodexo Inc., ISS Facility Service, CBRE Group Inc., and Compass Group PLC. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2023 - JLL declared that it would continue to provide Integrated Facilities Management, Lease Administration, Property Management, and Energy and Sustainability Services for 35 small-format hospitals and emergency departments totaling 1 million square feet in Dallas, El Paso, and San Antonio, Texas; Las Vegas, Nev.; Oklahoma City, Okla.; Pittsburgh, Pa.; and Milwaukee, Wis.; in addition to starting to provide Project and Development Services (PDS) for select markets.

- July 2023 - ECM Holding Group, Inc., a Wisconsin-based provider of energy efficiency retrofit services, was acquired by EMCOR Group, Inc. The group believes that adding ECM will further strengthen its position in energy efficiency specialty services and broaden the scope of its nationwide portfolio of bundled energy conservation and sustainability solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rebounding Commercial Activity Expected to Drive Growth

- 5.1.2 Emphasis on Green and Sustainable Building Practices

- 5.2 Market Restrains

- 5.2.1 Lack of Specialized Talents

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Hard FM

- 6.1.2 Soft FM

- 6.2 By End -User

- 6.2.1 Public/Infrastructure

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.2.4 Institutional

- 6.2.5 Other End-Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Latin America

- 6.3.5 Australia and new Zealand

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Jones Lang LaSalle IP Inc.

- 7.1.2 Sodexo Inc.

- 7.1.3 ISS Facility Service

- 7.1.4 CBRE Group Inc

- 7.1.5 Compass Group PLC

- 7.1.6 Cushman & Wakefield

- 7.1.7 AHI Facility Services Inc

- 7.1.8 EMCOR Facility Services

- 7.1.9 Facilicom

- 7.1.10 CBM Qatar LLC.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

設施管理市場:2026-2032年全球市場預測(依產品、產品模式、部署類型、公司規模及最終用途分類)

設施管理市場:2026-2032年全球市場預測(依產品、產品模式、部署類型、公司規模及最終用途分類) 設施管理市場規模、佔有率、趨勢和預測:按解決方案、服務、部署類型、組織規模、行業和地區分類,2026-2034 年設施管理服務市場:2026-2032年全球市場預測(依服務類型、合約類型、服務交付方式、最終用戶和組織規模分類)

設施管理市場規模、佔有率、趨勢和預測:按解決方案、服務、部署類型、組織規模、行業和地區分類,2026-2034 年設施管理服務市場:2026-2032年全球市場預測(依服務類型、合約類型、服務交付方式、最終用戶和組織規模分類) 2026年全球地下設施維護與管理市場報告2026年全球硬性服務設施管理市場報告2026年全球設施支援服務市場報告2026年全球設施管理服務市場報告2026年全球軟性服務設施管理市場報告

2026年全球地下設施維護與管理市場報告2026年全球硬性服務設施管理市場報告2026年全球設施支援服務市場報告2026年全球設施管理服務市場報告2026年全球軟性服務設施管理市場報告 設施管理市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測硬設施管理市場:依服務類型、合約類型、所有權類型和最終用戶產業分類-2026-2032年全球市場預測

設施管理市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測硬設施管理市場:依服務類型、合約類型、所有權類型和最終用戶產業分類-2026-2032年全球市場預測