|

市場調查報告書

商品編碼

1693851

非洲聚醯胺:市場佔有率分析、產業趨勢和成長預測(2024-2029)Africa Polyamide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

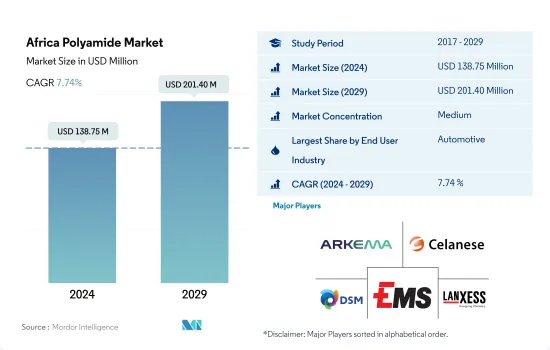

預計 2024 年非洲聚醯胺市場規模為 1.3875 億美元,到 2029 年將達到 2.014 億美元,預測期內(2024-2029 年)的複合年成長率為 7.74%。

汽車產業是規模最大、成長最快的終端用戶產業

- 汽車業是非洲聚醯胺市場最大的終端用戶產業。預計該地區汽車產量到 2022 年將達到 136 萬輛,以收入計算,從 2020 年起的複合年成長率為 3.51%。肯亞在汽車製造領域提供了各種投資機會。憑藉優惠的經濟政策,肯亞已成為汽車製造商進入東非和中非發展業務的理想樞紐。透過增加外國直接投資和貿易,非洲汽車工業的成長策略專注於與全球汽車格局高度融合。這些因素正在推動非洲聚醯胺市場的成長。

- 電子業是該地區第二大終端用戶產業。預計未來幾年該地區電子元件產量的成長將推動對聚醯胺樹脂的需求。預計到 2027 年,非洲家用電子電器需求將達到 177.9 億美元,複合年成長率為 13.85%。因此,該地區電氣和電子終端用戶產業的產量預計將增加,預計預測期內該部門的收益複合年成長率將達到 7.72%。

- 汽車產業是該地區市場中聚醯胺樹脂成長最快的終端用戶產業,預計在預測期內(2023-2029 年)的以金額為準年成長率為 9.28%。預計該地區的汽車產量將從 2023 年的 123 萬輛增加到 2029 年的 174 萬輛。預計該地區汽車產量的成長將在預測期內推動非洲對聚醯胺樹脂的需求。

南非是最大、發展最快的國家

- 2022 年,非洲將佔全球聚醯胺樹脂消費量的約 0.89%。這些樹脂具有高度多功能的特性,可應用於汽車、包裝和電氣/電子等各個行業。

- 南非是該地區最大的聚醯胺樹脂消費國,由於包裝和汽車產業的不斷發展,2022 年的銷售佔有率分別為 38.76% 和 33.4%。 2022年全國塑膠包裝製品年增率為2.20%,達到約94萬噸。此外,該國汽車產量將從2021年的51萬輛增加到2022年的53萬輛。預計未來幾年塑膠包裝和汽車產量的成長將推動該國對PET樹脂的需求。

- 奈及利亞是非洲聚醯胺樹脂市場第二大國家,預計預測期內以金額為準年成長率為 5.65%。由於汽車產量增加和建設活動活性化等因素,該國對聚醯胺樹脂的需求正在大幅增加。預計到2022年,該國汽車產量將達39萬輛,高於2021年的37萬輛。隨著奈及利亞人口持續以每年2.5%以上的速度成長,預計到2050年將達到4億,該國現有的基礎設施在未來幾年面臨不堪負荷的風險。因此,預計在 2021 年至 2025 年間,奈及利亞建築市場將以每年 3.2% 的速度成長。預計這將推動未來對聚醯胺樹脂的需求。

非洲聚醯胺市場趨勢

製造業活性化,滿足不斷成長的需求

- 南非是非洲領先的製造地。其製造能力、高效的物流網路和優惠的區域市場進入使南非成為尋求供應非洲的電子公司的理想之地。南非電子產業多元化,涵蓋電子機械、家用電子電器產品、通訊設備、消費性電子產品等。 2022年,非洲地區進口滿足其本土電氣和電子設備需求的約70%。

- 家用電子電器產業仍高度依賴進口。據估計,2018年南非進口了非洲60%的消費性電子產品。 2020年,由於政府採取大規模封鎖措施以及封鎖導致的供應鏈中斷,該國電氣和電子設備產量銷售年增率下降與前一年同期比較3.2%。在功能手機領域,由於廠商持續從功能手機轉型為入門級智慧型手機,出貨量較去年與前一年同期比較下降 26.6% 至 2,190 萬台。所有這些因素導致該地區電氣和電子元件產量下降,2020-2022 年期間的複合年成長率為 -9.41%。

- 政府致力於促進和支持國內製造、研發以及製定電氣和電子製造的安全標準。預計預測期內(2023-2029 年),電氣和電子元件產量的複合年成長率將達到 6.28%,以滿足非洲新興中產階級的需求。

非洲聚醯胺產業概況

非洲聚醯胺市場適度整合,前五大公司佔59.74%。市場的主要企業包括阿科瑪、塞拉尼斯公司、帝斯曼、EMS-Chemie Holding AG、朗盛等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 電氣和電子

- 包裝

- 進出口趨勢

- 聚醯胺(PA)貿易

- 價格趨勢

- 回收概述

- 聚醯胺(PA)回收趨勢

- 法律規範

- 奈及利亞

- 南非

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 電氣和電子

- 工業/機械

- 包裝

- 其他

- 子樹脂類型

- 芳香聚醯胺

- 聚醯胺(PA)6

- 聚醯胺(PA)66

- 聚鄰苯二甲醯胺

- 原產地

- 奈及利亞

- 南非

- 其他非洲國家

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Arkema

- Celanese Corporation

- DSM

- EMS-Chemie Holding AG

- LANXESS

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 5000190

The Africa Polyamide Market size is estimated at 138.75 million USD in 2024, and is expected to reach 201.40 million USD by 2029, growing at a CAGR of 7.74% during the forecast period (2024-2029).

The automotive segment is the largest and fastest-growing end-user industry

- The automotive segment is the largest end-user industry in the African polyamide market. Vehicle production in the region reached 1.36 million units in 2022, recording a CAGR of 3.51% by revenue from 2020. Kenya has various opportunities for investments in the field of automobile production. In line with favorable economic policies, Kenya has become the ideal hub for automotive manufacturers to gain entry into the eastern and central parts of Africa in order to grow their businesses. Through increased foreign direct investments and trade, the African automotive industry's growth strategies are focused on becoming highly integrated with the global automotive environment. Such factors are, in turn, fueling the growth of the African polyamide market.

- Electronics is the region's second-largest end-user industry. Over the coming years, rising production of electronics components in the region is expected to drive demand for polyamide resins. The demand for consumer electronics in Africa is expected to register a CAGR of 13.85% and reach a value of USD 17.79 billion by 2027. As a result, the region's increased production in the electrical and electronics end-user industry is expected to result in the segment recording a CAGR of 7.72% by revenue over the forecast period.

- Automotive is the fastest-growing end-user industry for polyamide resin in the regional market, expected to register a CAGR of 9.28% by value during the forecast period (2023-2029). Vehicle production in the region is projected to reach 1.74 million units in 2029 from 1.23 million units in 2023. This increase in vehicle production in the region is projected to drive demand for polyamide resins in Africa over the forecast period.

South Africa is the largest and the fastest-growing country

- Africa accounted for nearly 0.89% of the global consumption of polyamide resin in 2022. These resins exhibit versatile properties, which they find applications in various industries, such as automotive, packaging, and electrical and electronics.

- South Africa is the region's largest consumer country of polyamide resin due to its rising packaging and automotive industries, which held a revenue share of 38.76% and 33.4% in 2022. Plastic packaging products in the country increased at an annual rate of 2.20% in 2022 and reached around 0.94 million tons. Moreover, automotive production in the country reached 0.53 million units in 2022 from 0.51 million units in 2021. The rising plastic packaging and automotive production are projected to drive the demand for PET resin in the country in the coming years.

- Nigeria is the second-largest country in the African polyamide resin market which is expected to register a CAGR of 5.65% in terms of value during the forecast period. The country's demand for polyamide resin is increasing significantly due to rising vehicle production, increasing building and construction activities, etc. Automotive production in the country reached 0.39 million units in 2022 from 0.37 million units in 2021. As Nigeria's population continues to rate of more than 2.5% per year and is projected to reach 400 million by 2050, the country's existing infrastructure is at risk of becoming overburdened in the coming years. Therefore, between 2021 and 2025, the construction market in Nigeria is projected to experience an annual growth rate of 3.2%. Thereby, it is projected to drive the demand for polyamide resin in the future.

Africa Polyamide Market Trends

Manufacturing on the rise to tackle the rapidly growing demand

- South Africa is the leading manufacturing hub in Africa. Its manufacturing capabilities, efficient logistics network, and preferential regional market access position the country as an ideal location for electronics companies seeking to supply their products to Africa. South Africa has a diverse electronics industry that ranges from electrical machinery, household appliances, and telecommunication equipment to consumer electronics. In 2022, the African region imported around 70% of its local electrical and electronics demand.

- The consumer electronics industry still relies heavily on imports. According to estimates, South Africa brought 60% of all consumer electronics into Africa in 2018. In 2020, the electrical and electronic production in the country decreased at a growth rate of around 3.2%, by revenue, compared to the previous year, owing to the widespread lockdown adopted by the government and the supply chain disruption faced due to the lockdown. In the feature phone space, shipments were down by 26.6% to 21.9 million units as vendors were transitioning away from these devices toward entry-level smartphones. All such factors led to a decrease in the production of electrical and electronic components in the region at a CAGR of -9.41% from 2020 to 2022.

- The government is focused on promoting and supporting domestic manufacturing, R&D, and developing safety standards for the electrical and electronics manufacturing industry. The output of electrical and electronic industrial components is anticipated to record a CAGR of 6.28% during the forecast period (2023-2029) to supply the emerging African middle-class population.

Africa Polyamide Industry Overview

The Africa Polyamide Market is moderately consolidated, with the top five companies occupying 59.74%. The major players in this market are Arkema, Celanese Corporation, DSM, EMS-Chemie Holding AG and LANXESS (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Polyamide (PA) Trade

- 4.3 Price Trends

- 4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.5 Regulatory Framework

- 4.5.1 Nigeria

- 4.5.2 South Africa

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Sub Resin Type

- 5.2.1 Aramid

- 5.2.2 Polyamide (PA) 6

- 5.2.3 Polyamide (PA) 66

- 5.2.4 Polyphthalamide

- 5.3 Country

- 5.3.1 Nigeria

- 5.3.2 South Africa

- 5.3.3 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Arkema

- 6.4.2 Celanese Corporation

- 6.4.3 DSM

- 6.4.4 EMS-Chemie Holding AG

- 6.4.5 LANXESS

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

聚醯胺市場報告:按類型、應用、終端用戶產業和地區分類(2026-2034 年)電子保護裝置(EPD)用聚醯胺市場:按產品、應用和地區分類(2026-2034 年)

聚醯胺市場報告:按類型、應用、終端用戶產業和地區分類(2026-2034 年)電子保護裝置(EPD)用聚醯胺市場:按產品、應用和地區分類(2026-2034 年) 聚醯胺市場:2026-2032年全球市場預測(依產品、形態、製造流程、產品形態、等級、應用及分銷通路分類)

聚醯胺市場:2026-2032年全球市場預測(依產品、形態、製造流程、產品形態、等級、應用及分銷通路分類) 2026年全球長鏈聚醯胺市場報告

2026年全球長鏈聚醯胺市場報告 聚醯胺腳輪市場規模、佔有率和成長分析:按腳輪類型、承載能力、材質、終端用戶產業、地區和產業預測分類,2026-2033年

聚醯胺腳輪市場規模、佔有率和成長分析:按腳輪類型、承載能力、材質、終端用戶產業、地區和產業預測分類,2026-2033年 3D 聚醯胺(PA)市場規模、佔有率和成長分析:按聚醯胺類型、3D 列印方法、配方、應用和地區分類-2026-2033 年產業預測

3D 聚醯胺(PA)市場規模、佔有率和成長分析:按聚醯胺類型、3D 列印方法、配方、應用和地區分類-2026-2033 年產業預測 聚醯胺12市場:依最終用途產業和地區分類

聚醯胺12市場:依最終用途產業和地區分類 聚醯胺市場分析及預測(至2035年):類型、產品、應用、技術、終端用戶、形式、材料類型、製程及功能全球再生聚醯胺纖維市場依形態、來源、技術、聚醯胺類型和最終用途分類,預測至2026-2032年尼龍12市場按形態、等級、應用和最終用戶產業分類-2026年至2032年全球預測

聚醯胺市場分析及預測(至2035年):類型、產品、應用、技術、終端用戶、形式、材料類型、製程及功能全球再生聚醯胺纖維市場依形態、來源、技術、聚醯胺類型和最終用途分類,預測至2026-2032年尼龍12市場按形態、等級、應用和最終用戶產業分類-2026年至2032年全球預測

▼