|

市場調查報告書

商品編碼

1693849

歐洲聚醯胺:市場佔有率分析、產業趨勢與成長預測(2024-2029年)Europe Polyamide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

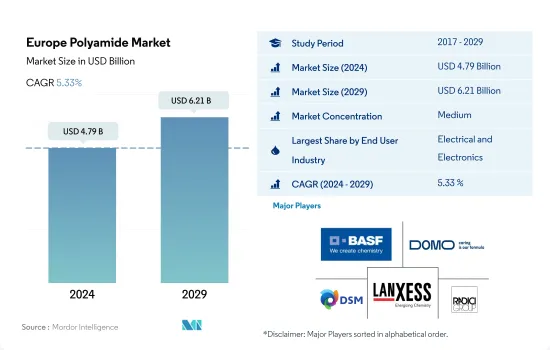

預計 2024 年歐洲聚醯胺市場規模將達到 47.9 億美元,預計到 2029 年將達到 62.1 億美元,預測期內(2024-2029 年)的複合年成長率為 5.33%。

汽車和電氣/電子行業日益成長的需求正在推動市場成長

- 聚醯胺具有多種物理特性,使其成為製造和工業應用的理想選擇,包括耐磨性、耐腐蝕性、耐化學性、阻燃性、柔韌性和強度。 2019年歐洲聚醯胺消費量與2017年相比成長了3.3%,主要原因是汽車和電氣電子產業的需求增加。

- 隨著企業實施在家工作模式、個人設立家庭辦公室,對電子設備的需求激增,歐洲電氣和電子產業的消費量最高。技術進步每年都會對電子設備產生穩定的需求。 2022年該產業將佔聚醯胺總消費量的26.9%,與2017年相比消費量成長1.5%。

- 汽車產業因汽車產量激增,消費量則位居第二。到2022年,該產業將佔聚醯胺總消費量的約26.6%。政府對內燃機製造和生產的監管正在推動消費者選擇電動車。由於電動車和需要輕型和省油的現代汽車產量不斷增加,該地區的聚醯胺銷量預計將成長。

- 預計航太業將成為支出成長第二快的產業,預測期內(2023-2029 年)的複合年成長率為 7.97%。這是因為生產飛機零件是為了滿足對更輕的飛機和更高的燃油效率日益成長的需求。

德國將在整個預測期內保持主導地位

- 2022年,歐洲將佔全球聚醯胺(PA)消費量的25%。由於其多功能的特性,聚醯胺被用於各種行業,包括汽車、包裝和電氣/電子行業。

- 德國是最大的市場,2022 年以金額為準與前一年同期比較3.67%。這主要得益於電氣電子和汽車行業,按數量計算,這兩個行業分別佔了 26% 和 28% 的市場佔有率。電子設備需求的激增是由於企業採用在家工作模式以及人們設立家庭辦公室。經過數月的談判,歐盟達成協議,將從2035年起有效禁止電動車以外的所有新車。該協議可能會增加電動車的銷量,並促進該地區聚醯胺的消費。

- 法國是成長最快的市場,2022 年的以金額為準與 2021 年相比成長了 6.39%。電氣電子和航太工業是該國聚醯胺使用率最高的產業。法國航太和國防工業以出口主導,是世界第二大工業國。

- 預計預測期內 [2023-2029] 的複合年成長率為 5.52%,其中包裝行業的以金額為準年成長率最高,為 8.08%。預計包裝產量將從2022年的3,000萬噸達到2029年的3,980萬噸,導致未來聚醯胺消費量增加。

歐洲聚醯胺市場趨勢

科技創新推動家用電子電器市場

- 2017年至2021年,歐洲電氣和電子設備產量的複合年成長率將超過3.8%。電子創新的快速步伐推動著對更新、更快的電氣和電子產品的持續需求。因此,該地區對電氣和電子設備生產的需求也在增加。

- 儘管遠距工作和學習導致對電腦和筆記型電腦的需求增加,但歐洲消費性電子產品領域的每用戶平均收入仍下降了 6.3%。 2020年銷售額約2,521億美元。因此,該地區2020年電氣及電子設備產量較去年與前一年同期比較2.8%。

- 2021年,歐洲電氣和電子設備出口額約2,283.7億美元,比2020年成長12.4%。因此,該地區電氣和電子設備產量有所成長,2021與前一年同期比較成長11.6%。

- 預計機器人、虛擬和擴增實境實境、物聯網 (IoT) 和 5G 連線將在預測期內成長。由於技術進步,預計預測期內家用電子電器的需求將會上升。該地區消費電子領域的銷售額預計將從 2023 年的 1,211 億美元增至約 2027 年的 1,572 億美元。到 2027 年,歐洲預計將成為第二大電氣和電子設備生產國,佔全球市場的 12.7% 左右。因此,預計未來幾年家用電子電器的興起將推動對電氣和電子設備生產的需求。

歐洲聚醯胺產業概況

歐洲聚醯胺市場適度整合,前五大公司佔58.73%。該市場的主要企業包括BASF SE、Domo Chemicals、DSM、LANXESS、Radici Partecipazioni SpA等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 電氣和電子

- 包裝

- 進出口趨勢

- 聚醯胺(PA)貿易

- 價格趨勢

- 回收概述

- 聚醯胺(PA)回收趨勢

- 法律規範

- EU

- 法國

- 德國

- 義大利

- 俄羅斯

- 英國

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 電氣和電子

- 工業/機械

- 包裝

- 其他

- 子樹脂類型

- 芳香聚醯胺

- 聚醯胺(PA)6

- 聚醯胺(PA)66

- 聚鄰苯二甲醯胺

- 原產地

- 法國

- 德國

- 義大利

- 俄羅斯

- 英國

- 其他歐洲國家

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- BASF SE

- Celanese Corporation

- Domo Chemicals

- DSM

- Grodno Azot

- Grupa Azoty SA

- Koch Industries, Inc.

- KuibyshevAzot

- LANXESS

- Radici Partecipazioni SpA

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 5000188

The Europe Polyamide Market size is estimated at 4.79 billion USD in 2024, and is expected to reach 6.21 billion USD by 2029, growing at a CAGR of 5.33% during the forecast period (2024-2029).

Growing demand from automotive and electrical & electronics industries will drive market growth

- Polyamide has several physical properties that make it ideal for manufacturing and industrial use, including abrasion, corrosion, chemical resistance, flame resistance, flexibility, and strength. The volume of European polyamide consumption increased by 3.3% in 2019 compared to 2017 due to increased demand, primarily from the automotive and electrical and electronics industries.

- The European electrical and electronics industry has the highest consumption volume due to the surge in demand for electronic devices as a result of companies implementing work-from-home models and individuals establishing home offices. Technological advancements generate consistent demand for electronic devices year after year. The industry accounted for 26.9% of the total polyamide volume consumed in 2022, and the consumption volume increased by 1.5% in 2022 compared to 2017.

- The automotive industry has the second-largest consumption rate due to the surge in vehicle production. The industry accounted for around 26.6% of the total polyamide volume consumed in 2022. Consumers are opting for electric vehicles due to government regulations on the manufacturing and production of internal combustion engines. Polyamide sales in the region are expected to increase due to the growing production of EVs and vehicles with the latest lightweight and higher fuel efficiency requirements.

- The aerospace industry is expected to be the second fastest growing in terms of consumption value during the forecast period (2023-2029), with a CAGR of 7.97%, owing to the production of aircraft components in response to the growing demand for lighter and more fuel-efficient aircraft.

Germany to remain dominant during the forecast period

- In 2022, Europe accounted for 25% of the global polyamide (PA) consumption by volume. Polyamide's versatile properties make it applicable in various industries such as automotive, packaging, and electrical and electronics.

- Germany was the largest market, recording a growth of 3.67% by value in 2022 compared to the previous year, attributed to the electrical and electronics and automotive industries, which held 26% and 28% of the market share, respectively, by volume. The surge in demand for electronic devices is a consequence of companies adopting work-from-home models and people setting up home offices. After months of negotiations, the EU reached an agreement to effectively ban new non-electric cars from 2035. This agreement has increased the sales of electric vehicles, which may boost the consumption of polyamides in the region.

- France was the fastest-growing market, witnessing a growth of 6.39% in terms of value in 2022 compared to 2021. The electrical and electronics and aerospace industries are at the forefront of polyamide utilization in the country. France's aerospace and defense industry is export-driven and ranks second globally.

- The market is projected to record a CAGR of 5.52% during the forecast period [2023-2029], with the packaging industry reporting the highest CAGR of 8.08% by value. The packaging production volume is expected to reach 39.8 million tons in 2029, up from 30 million tons in 2022, thereby increasing the consumption of polyamides in the future.

Europe Polyamide Market Trends

Technological innovations to boost the consumer electronics market

- Europe's electrical and electronics production registered a CAGR of over 3.8% between 2017 and 2021. The rapid pace of electronic technological innovation is driving consistent demand for newer and faster electrical and electronic products. As a result, it has also increased the demand for electrical and electronics production in the region.

- Despite the increased demand for computers and laptops due to remote working and distance learning, the average revenue per user in the European consumer electronics segment dropped by 6.3%. It generated a revenue of around USD 252.1 billion in 2020. As a result, in 2020, the electrical and electronic production in the region decreased by 2.8% by revenue compared to the previous year.

- In 2021, Europe's electrical and electronic equipment exports were around USD 228.37 billion, 12.4% higher compared to 2020. As a result, electrical and electronic production in the region increased and registered 11.6% in 2021 compared to the previous year.

- Robotics, virtual reality and augmented reality, IoT (Internet of Things), and 5G connectivity are expected to grow during the forecast period. As a result of technological advancements, demand for consumer electronics is expected to rise during the forecast period. The consumer electronics segment in the region is projected to reach a revenue of around USD 157.2 billion in 2027 from USD 121.1 billion in 2023. By 2027, Europe is projected to be the second-largest electrical and electronics production accounting for around 12.7% of the global market. As a result, the rise in consumer electronics is projected to increase the demand for electrical and electronics production in the coming years.

Europe Polyamide Industry Overview

The Europe Polyamide Market is moderately consolidated, with the top five companies occupying 58.73%. The major players in this market are BASF SE, Domo Chemicals, DSM, LANXESS and Radici Partecipazioni SpA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Polyamide (PA) Trade

- 4.3 Price Trends

- 4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.5 Regulatory Framework

- 4.5.1 EU

- 4.5.2 France

- 4.5.3 Germany

- 4.5.4 Italy

- 4.5.5 Russia

- 4.5.6 United Kingdom

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Sub Resin Type

- 5.2.1 Aramid

- 5.2.2 Polyamide (PA) 6

- 5.2.3 Polyamide (PA) 66

- 5.2.4 Polyphthalamide

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 United Kingdom

- 5.3.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 BASF SE

- 6.4.2 Celanese Corporation

- 6.4.3 Domo Chemicals

- 6.4.4 DSM

- 6.4.5 Grodno Azot

- 6.4.6 Grupa Azoty S.A.

- 6.4.7 Koch Industries, Inc.

- 6.4.8 KuibyshevAzot

- 6.4.9 LANXESS

- 6.4.10 Radici Partecipazioni SpA

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

聚醯胺市場-全球產業規模、佔有率、趨勢、機會與預測,按產品、應用、地區和競爭細分,2020-2030 年

聚醯胺市場-全球產業規模、佔有率、趨勢、機會與預測,按產品、應用、地區和競爭細分,2020-2030 年 全球聚醯胺市場(按類型、應用和地區)- 預測至 2030 年

全球聚醯胺市場(按類型、應用和地區)- 預測至 2030 年 生物聚醯胺(Bio-PA)全球市場、市場規模、平均價格和預測(2018-2034)透明聚醯胺市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、等級、最終用戶、地區和競爭細分,2020-2030 年)

生物聚醯胺(Bio-PA)全球市場、市場規模、平均價格和預測(2018-2034)透明聚醯胺市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、等級、最終用戶、地區和競爭細分,2020-2030 年) 全球長鏈聚醯胺市場特種聚醯胺產能、產量、供應、需求、價格及市場預測分析(2034年)

全球長鏈聚醯胺市場特種聚醯胺產能、產量、供應、需求、價格及市場預測分析(2034年) 2025-2033年聚醯胺市場報告(按類型、應用、最終用途產業和地區)

2025-2033年聚醯胺市場報告(按類型、應用、最終用途產業和地區) 生物聚醯胺市場規模、佔有率、成長分析(按產品類型、材料、應用、最終用戶、地區)- 2025-2032 年產業預測

生物聚醯胺市場規模、佔有率、成長分析(按產品類型、材料、應用、最終用戶、地區)- 2025-2032 年產業預測 長鏈聚醯胺市場報告:趨勢、預測和競爭分析(至 2031 年)

長鏈聚醯胺市場報告:趨勢、預測和競爭分析(至 2031 年) 中東聚醯胺:市場佔有率分析、產業趨勢和成長預測(2024-2029)

中東聚醯胺:市場佔有率分析、產業趨勢和成長預測(2024-2029)

▼