|

市場調查報告書

商品編碼

1693651

歐洲電動車:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Europe Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

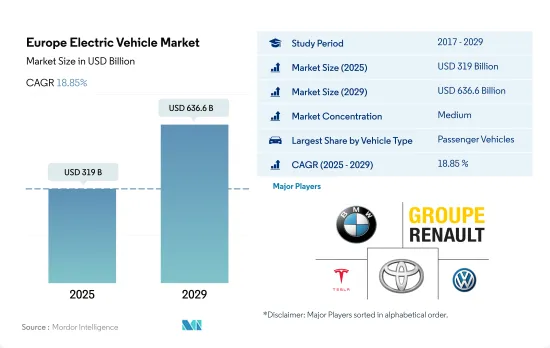

預計 2025 年歐洲電動車市場規模為 3,190 億美元,到 2029 年將達到 6,366 億美元,預測期內(2025-2029 年)的複合年成長率為 18.85%。

物流、供應鏈、基礎設施和建築行業的成長以及公共運輸服務的增加將增強歐洲電動車市場

- 未來幾年商用車的需求將大幅成長。這一成長的主要驅動力是物流、供應鏈、基礎設施和建築業。公共交通的增加也推動了對公車的需求。然而,受疫情影響,2020年商用車銷量大幅下滑。 2021年市場迅速復甦,歐洲氣候計畫發揮了關鍵作用。隨著歐洲計劃在 2030 年前禁止柴油引擎汽車,我們預計商用消費者將明顯轉向電動商用汽車。

- 在整個歐洲,新產品的推出和戰略合作夥伴關係(例如現代與 H2 Energy 的合作)有望推動電動卡車的銷售。基於這項合作,現代氫能移動出行公司 (HHM) 於 2019 年 9 月成立,其願景是在瑞士和歐洲培育綠色氫能生態系統。 HHM 有一個雄心勃勃的目標,即到 2025 年在其車隊中擁有 1,600 輛燃料電池電動重型卡車。預計這些努力將在 2024 年至 2030 年期間促進歐洲重型電動卡車的銷售。

- 2021年,德國公共運輸領域的電動公車數量幾乎加倍,新註冊車輛數量從前一年的689輛躍升60%至1269輛。其中,586輛為電池式電動車,只有少數使用燃料電池或其他技術。此外,德國當地交通運輸業者和政府機構都計劃在 2025 年之前在其車隊中增加 3,000 多輛電動公車。其他歐洲國家的類似趨勢可能會在 2024 年至 2030 年期間推動整個歐洲商用車市場的發展。

歐洲電動車市場的特點是各國之間存在差異,反映了獎勵、基礎設施和消費者偏好的差異。

- 歐洲是世界上最大的電動車生產地之一。從全球來看,它是採用電動車速度最快的國家之一。就電動車而言,到 2023 年,純電動車將佔全部區域所有新乘用車註冊量的最大佔有率,達到 8.3%。預計到2030年和2035年,大多數國家將禁止使用汽油動力汽車,這將推動電動車的銷售。

- 新產品的推出和新品牌的進入預計將推動歐洲乘用車市場的發展。 2022年2月,中國汽車製造商小鵬汽車推出電動轎車P7和P5,進入瑞典電動乘用車市場。 2022年6月,美國汽車製造商福特宣布,2030年將在歐洲只生產和銷售電動車。該公司計劃投資114億美元在其位於西班牙瓦倫西亞的製造工廠生產電動車。

- 由於政府的退稅和補貼等舉措,電動車在歐洲國家越來越受歡迎。例如,到2023年,新電動車將獲得2,950歐元的補貼,二手電動車將獲得約2,000歐元的補貼。但車輛價格必須至少為12,000歐元,最多為45,000歐元。這些優勢正在吸引客戶對電動車的興趣,預計2024年至2030年間歐洲國家對各種類型電動車的需求將會增加。

歐洲電動車市場趨勢

環境問題、政府支持和脫碳目標刺激了歐洲電動車的需求和銷售

- 近年來,歐洲國家對電動車的需求和銷售量大幅成長。德國 2022 年電動車銷量與 2021 年相比成長了 22%,其次是英國,2022 年電動車銷量與 2021 年相比成長了 18.40%。日益成長的環境問題、嚴格的政府規範、電動車的優勢(例如更好的燃油經濟性、更低的服務成本、更少的碳排放)以及政府補貼是推動歐洲國家電動車成長的一些因素。

- 歐洲國家對電動商用車,特別是輕型卡車的需求逐漸增加。此外,世界各國政府也支持電動車的普及。 2021年11月,英國政府宣布承諾在2040年實現所有重型車輛零排放。這些因素將使2022年英國電動商用車銷量較2021年成長23.17%,不同國家的類似做法將推動整個歐洲對電動商用車的需求。

- 預計未來幾年歐洲國家的汽車電氣化將呈指數級成長。預計政府在脫碳方面的努力將推動歐洲電動商用車市場的發展。例如,2022年1月,德國交通部長宣布了2030年道路上電動車保有量達到1,500萬輛的目標。受這些因素影響,預計2024年至2030年間歐洲國家的電動車銷量將會成長。

歐洲電動車產業概況

歐洲電動車市場適度整合,前五大企業佔43.69%。市場的主要企業有:Bayerische Motoren Werke AG、雷諾集團、特斯拉公司、豐田汽車公司和大眾汽車公司(按字母順序排列)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 人口

- 人均GDP

- 消費者汽車支出(cvp)

- 通貨膨脹率

- 汽車貸款利率

- 共乘

- 電氣化的影響

- 電動車充電站

- 電池組價格

- 新款 Xev 車型發布

- 二手車銷售

- 燃油價格

- OEM生產統計

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 車輛類型

- 商用車

- 搭乘用車

- 掀背車

- 多用途車輛

- 轎車

- SUV

- 摩托車

- 燃料類別

- BEV

- FCEV

- HEV

- PHEV

- 國家

- 奧地利

- 比利時

- 捷克共和國

- 丹麥

- 愛沙尼亞

- 法國

- 德國

- 愛爾蘭

- 義大利

- 拉脫維亞

- 立陶宛

- 挪威

- 波蘭

- 俄羅斯

- 西班牙

- 瑞典

- 英國

- 其他歐洲國家

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Audi AG

- Bayerische Motoren Werke AG

- Groupe Renault

- Hyundai Motor Company

- Kia Corporation

- Mercedes-Benz

- Tesla Inc.

- Toyota Motor Corporation

- Volkswagen AG

- Volvo Car AB

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 93039

The Europe Electric Vehicle Market size is estimated at 319 billion USD in 2025, and is expected to reach 636.6 billion USD by 2029, growing at a CAGR of 18.85% during the forecast period (2025-2029).

The growing logistics, supply chain, infrastructure, and construction sectors and the rise in public transportation services are bolstering the European EV market

- The demand for commercial vehicles is set to witness a significant uptick in the coming years. Key drivers of this growth include the logistics, supply chain, infrastructure, and construction sectors. Additionally, a rise in public transportation services is bolstering the demand for buses. However, the sales of commercial vehicles experienced a downturn in 2020, largely due to the impact of the pandemic. The market swiftly rebounded in 2021, with Europe's Climate Plan playing a pivotal role. As Europe aims to ban diesel-powered vehicles by 2030, a notable shift is expected to be witnessed among business consumers toward electric commercial vehicles.

- Across Europe, the introduction of new products and strategic collaborations, such as the partnership between Hyundai Motor Company and H2 Energy, are poised to drive sales of electric trucks. This collaboration produced Hyundai Hydrogen Mobility (HHM) in September 2019 with a vision to foster a green hydrogen ecosystem in Switzerland and Europe. HHM has set an ambitious target of introducing 1,600 fuel-cell electric heavy-duty trucks by 2025. Such initiatives are expected to fuel the sales of heavy electric trucks in Europe from 2024 to 2030.

- In 2021, the number of electric buses in Germany's public transport sector nearly doubled, with new registrations surging by 60% to reach 1,269, up from 689 in the previous year. Of these, 586 were battery electric vehicles, while only a handful was fuel cell-powered or utilized other technologies. Furthermore, both local transport companies and government bodies in Germany have plans to add over 3,000 e-buses by 2025. Similar trends in other European nations are poised to propel the overall commercial vehicle market in Europe from 2024 to 2030.

The European electric vehicles market is characterized by country-level variations, reflecting differing incentives, infrastructure, and consumer preferences

- Europe is one of the largest electric vehicle manufacturers globally. Globally, it has one of the fastest adoptions of electric mobility. In terms of electric vehicles, sales of electric passenger cars accounted for the largest share of 8.3% of all newly registered cars across the region in 2023, which were fully electric. Gasoline-powered vehicles are expected to be banned by 2030 and 2035 in most countries, providing a boost to the sales of electric vehicles.

- The launch of new products and the entry of new brands are expected to drive the market for passenger cars in Europe. In February 2022, the Chinese automaker Xpeng entered Sweden's electric passenger cars with its debut electric cars, P7 and P5 sedans. In June 2022, the American automaker Ford announced that it would produce and sell only electric cars in Europe by 2030. The company plans to invest USD 11.4 billion in producing an electric car at a manufacturing plant in Valencia, Spain.

- Several government efforts in terms of rebates and subsidies are increasing the adoption of electric vehicles in various European countries. For instance, in 2023, a subsidy of EUR 2,950 was made eligible for new battery electric cars and a subsidy of around EUR 2,000 for used battery electric cars. However, the price of the vehicles should be a minimum of EUR 12,000 and a maximum of EUR 45,000. Such advantages attract customer attention to these vehicles, which is expected to enhance the demand for various types of electric vehicles in European countries from 2024 to 2030.

Europe Electric Vehicle Market Trends

Environmental concerns, government support, and decarbonization goals fuel European electric vehicle demand and sales

- The demand and sales of electric vehicles in European countries have grown significantly over the past few years. Germany witnessed a growth in the sales of electric cars by 22% in 2022 over 2021, followed by the United Kingdom with an 18.40% increase in 2022 over 2021. Growing environmental concerns, stringent governmental norms, advantages of electric vehicles such as fuel efficiency, low service cost, no carbon emissions, and subsidies by the government are some of the factors contributing to the growth of electric vehicles in European countries.

- The demand for electric commercial vehicles, especially light trucks, is growing gradually in European countries. Moreover, the governments of various countries are also supporting the adoption of electric vehicles. In November 2021, the government of the United Kingdom announced a pledge that all heavy-duty vehicles would be zero-emission by the year 2040. Such factors have increased the sales of electric commercial vehicles in the United Kingdom by 23.17% in 2022 over 2021, and similar practices in various countries are enhancing the demand for electric commercial vehicles across Europe.

- It is projected that the electrification of vehicles in European countries is expected to grow tremendously in the next few years. The efforts of the governments in the regions for decarbonization are expected to drive the electric commercial vehicle market in Europe. For instance, in January 2022, the transport minister of Germany announced a goal to put 15 million electric vehicles on the road by 2030. Such factors are expected to increase the sales of electric vehicles during the 2024-2030 period in European countries.

Europe Electric Vehicle Industry Overview

The Europe Electric Vehicle Market is moderately consolidated, with the top five companies occupying 43.69%. The major players in this market are Bayerische Motoren Werke AG, Groupe Renault, Tesla Inc., Toyota Motor Corporation and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Impact Of Electrification

- 4.8 EV Charging Station

- 4.9 Battery Pack Price

- 4.10 New Xev Models Announced

- 4.11 Used Car Sales

- 4.12 Fuel Price

- 4.13 Oem-wise Production Statistics

- 4.14 Regulatory Framework

- 4.15 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.2 Passenger Vehicles

- 5.1.2.1 Hatchback

- 5.1.2.2 Multi-purpose Vehicle

- 5.1.2.3 Sedan

- 5.1.2.4 Sports Utility Vehicle

- 5.1.3 Two-Wheelers

- 5.2 Fuel Category

- 5.2.1 BEV

- 5.2.2 FCEV

- 5.2.3 HEV

- 5.2.4 PHEV

- 5.3 Country

- 5.3.1 Austria

- 5.3.2 Belgium

- 5.3.3 Czech Republic

- 5.3.4 Denmark

- 5.3.5 Estonia

- 5.3.6 France

- 5.3.7 Germany

- 5.3.8 Ireland

- 5.3.9 Italy

- 5.3.10 Latvia

- 5.3.11 Lithuania

- 5.3.12 Norway

- 5.3.13 Poland

- 5.3.14 Russia

- 5.3.15 Spain

- 5.3.16 Sweden

- 5.3.17 UK

- 5.3.18 Rest-of-Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Audi AG

- 6.4.2 Bayerische Motoren Werke AG

- 6.4.3 Groupe Renault

- 6.4.4 Hyundai Motor Company

- 6.4.5 Kia Corporation

- 6.4.6 Mercedes-Benz

- 6.4.7 Tesla Inc.

- 6.4.8 Toyota Motor Corporation

- 6.4.9 Volkswagen AG

- 6.4.10 Volvo Car AB

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

電動車虛擬原型製作市場:按組件、技術、部署模式、應用、車輛類型和最終用戶分類-2026-2032年全球市場預測

電動車虛擬原型製作市場:按組件、技術、部署模式、應用、車輛類型和最終用戶分類-2026-2032年全球市場預測 2026年全球V2B(車輛到建築)電力市場報告

2026年全球V2B(車輛到建築)電力市場報告 全電動多用途貨車市場規模、佔有率和成長分析:按產能、應用、終端用戶產業、地區和產業預測,2026-2033年

全電動多用途貨車市場規模、佔有率和成長分析:按產能、應用、終端用戶產業、地區和產業預測,2026-2033年 長續航里程電動車市場規模、佔有率和成長分析:按車輛類型、電池類型、充電基礎設施、續航里程、消費群體、動力系統、功率輸出和地區分類-2026-2033年產業預測

長續航里程電動車市場規模、佔有率和成長分析:按車輛類型、電池類型、充電基礎設施、續航里程、消費群體、動力系統、功率輸出和地區分類-2026-2033年產業預測 800V電動車架構市場規模、佔有率和成長分析:按車輛、架構、充電方式、組件、應用和地區分類-2026-2033年產業預測

800V電動車架構市場規模、佔有率和成長分析:按車輛、架構、充電方式、組件、應用和地區分類-2026-2033年產業預測 電動車售後市場規模、佔有率和成長分析:按零件類型、車輛類型、服務類型、動力系統、銷售管道、最終用戶、地區和產業預測,2026-2033年

電動車售後市場規模、佔有率和成長分析:按零件類型、車輛類型、服務類型、動力系統、銷售管道、最終用戶、地區和產業預測,2026-2033年 電動車(零能耗汽車)市場規模、佔有率和成長分析:按車輛類型、電源管理方法、充電基礎設施、電池技術、最終用戶和地區分類-產業預測(2026-2033 年)

電動車(零能耗汽車)市場規模、佔有率和成長分析:按車輛類型、電源管理方法、充電基礎設施、電池技術、最終用戶和地區分類-產業預測(2026-2033 年) 2026-2030年全球電動車市場

2026-2030年全球電動車市場 歐洲電動車市場:依動力類型(純電動車 (BEV)、燃料電池電動車 (FCEV)、插電式混合動力車 (PHEV)、混合動力車 (HEV))、功率輸出(100kW 以下、100kW-250kW)、應用(個人用途、商業用途)和地區劃分 - 全球預測至 2036 年

歐洲電動車市場:依動力類型(純電動車 (BEV)、燃料電池電動車 (FCEV)、插電式混合動力車 (PHEV)、混合動力車 (HEV))、功率輸出(100kW 以下、100kW-250kW)、應用(個人用途、商業用途)和地區劃分 - 全球預測至 2036 年 中國電動車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

中國電動車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

▼