|

市場調查報告書

商品編碼

1693626

歐洲輕型商用車市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Europe Light Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

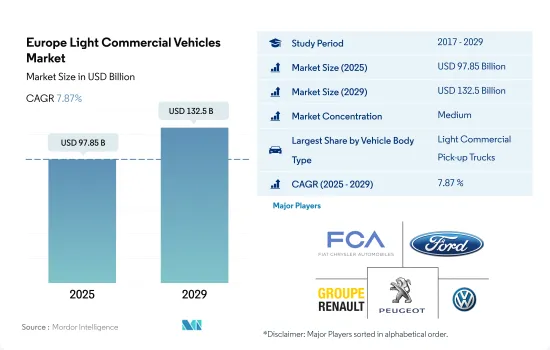

預計 2025 年歐洲輕型商用車市場規模將達到 978.5 億美元,到 2029 年將達到 1,325 億美元,預測期內(2025-2029 年)的複合年成長率為 7.87%。

歐洲輕型商用車市場因基礎設施投資和電子商務的蓬勃發展而蓬勃發展,預計在都市化和綠色舉措的推動下將繼續成長

- 2022年,歐洲輕型商用車(LCV)市場銷售量強勁成長6.2%。預計這一積極勢頭將持續下去,2023 年成長率預計將達到 3.5%。這一成長主要得益於基礎設施投資的活性化和電子商務的激增。歐盟對運輸和能源計劃的關注正在刺激對輕型商用車的需求,尤其是在建築和公共領域。疫情期間,最後一哩配送網路的擴張趨勢刺激了用於小包裹和食品配送的輕型商用貨車的購買。

- 2017年至2023年間,歐洲輕型商用車市場將顯著成長,銷售量將激增38%。這種激增是由電子商務的繁榮所推動的,電子商務刺激了配送網路的擴張,並隨之帶動了貨車銷售的成長。此外,零售、建築和服務等行業的更換需求也發揮了至關重要的作用。儘管2020年受疫情影響,市場有所萎縮,但隨著數位化的加快,市場迅速復甦。整體而言,穩定的經濟成長和強勁的基礎設施投資是這段時期歐洲輕型商用車市場擴張的主要驅動力。

- 預計歐洲輕型商用車市場在 2024 年至 2030 年期間的複合年成長率將達到 3.1%。這一成長軌跡將受到持續的基礎設施建設、最後一哩配送網路的持續擴張以及都市化趨勢的推動。這些因素,加上飯店、食品配送和建築業對輕型商用車的需求不斷成長,描繪出一幅光明的前景。然而,市場可能面臨阻力,因為不斷變化的排放氣體和都市區通行法規可能會推動替代燃料貨車的採用。

歐洲輕型商用車市場各國的趨勢凸顯了該地區減少排放氣體和提高效率的動力。

- 2022 年歐洲主要市場的輕型商用車銷售數據各不相同,反映了各自的經濟狀況。在強勁經濟的支撐下,德國經濟強勁成長 6.3%。同時,英國面臨經濟不確定性,輕型商用車銷售下降了2.1%。法國、義大利和西班牙的降幅在 3% 至 5% 之間,與更廣泛的宏觀經濟挑戰一致。然而,隨著疫情後的情況好轉,預計2023年將出現復甦,大多數國家的貿易量將成長4-6%。

- 2017 年至 2021 年間,歐洲主要的輕型商用車市場(德國、法國、義大利、西班牙和波蘭)呈現健康擴張態勢,疫情前的複合年成長率約為 3-5%。這一成長是由強勁的經濟活動所推動的,特別是建築、分銷和服務等行業。 2020 年疫情引發的經濟收縮相對短暫,但復甦並不均衡,這在很大程度上是由於財政獎勵策略的差異以及零售和餐旅服務業等行業的脆弱性。

- 歐洲輕型商用車市場正處於更穩定的成長軌跡,預計2023年至2029年間年均成長率將達到3-4%。基礎設施投資、最後一哩配送網路的興起以及持續的經濟復甦等因素預計將提振需求。然而,高通膨、能源成本和政治不確定性等因素也帶來風險。此外,市場向電動傳動系統的轉變可能會進一步影響市場動態。預計歐洲輕型商用車市場長期內將緩慢擴張。

歐洲輕型商用車市場趨勢

環境問題、政府支持和脫碳目標刺激了歐洲電動車的需求和銷售

- 近年來,歐洲國家電動車的需求和銷售量大幅成長。德國 2022 年電動車銷量與 2021 年相比成長了 22%,其次是英國,2022 年電動車銷量與 2021 年相比成長了 18.40%。日益成長的環境問題、嚴格的政府規範、電動車的優勢(例如更好的燃油經濟性、更低的服務成本、更少的碳排放)以及政府補貼是推動歐洲國家電動車成長的一些因素。

- 歐洲國家對電動商用車,特別是輕型卡車的需求逐漸增加。此外,世界各國政府也支持電動車的普及。 2021年11月,英國政府宣布承諾在2040年實現所有重型車輛零排放。這些因素將使2022年英國電動商用車銷量較2021年成長23.17%,不同國家的類似做法將推動整個歐洲對電動商用車的需求。

- 預計未來幾年歐洲國家的汽車電氣化將呈指數級成長。預計政府在脫碳方面的努力將推動歐洲電動商用車市場的發展。例如,2022年1月,德國交通部長宣布了2030年道路上電動車保有量達到1,500萬輛的目標。受這些因素影響,預計2024年至2030年間歐洲國家的電動車銷量將會成長。

歐洲輕型商用車產業概況

歐洲輕型商用車市場適度整合,前五大企業佔62.47%的市佔率。市場的主要企業是:飛雅特克萊斯勒汽車公司、福特汽車公司、雷諾集團、標緻汽車公司和大眾汽車公司(按字母順序排列)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 人口

- 人均GDP

- 消費者汽車支出(cvp)

- 通貨膨脹率

- 汽車貸款利率

- 電氣化的影響

- 電動車充電站

- 電池組價格

- 新款 Xev 車型發布

- 物流績效指數

- 燃油價格

- OEM生產統計

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 車輛類型

- 商用車

- 輕型商用皮卡車

- 輕型商用廂型車

- 商用車

- 推進類型

- 混合動力汽車和電動車

- 按燃料類別

- BEV

- FCEV

- HEV

- PHEV

- ICE

- 天然氣

- 柴油引擎

- 汽油

- LPG

- 混合動力汽車和電動車

- 國家

- 奧地利

- 比利時

- 捷克共和國

- 丹麥

- 愛沙尼亞

- 法國

- 德國

- 愛爾蘭

- 義大利

- 拉脫維亞

- 立陶宛

- 挪威

- 波蘭

- 俄羅斯

- 西班牙

- 瑞典

- 英國

- 其他歐洲國家

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Fiat Chrysler Automobiles NV

- Ford Motor Company

- Groupe Renault

- Mercedes-Benz

- Peugeot SA

- Toyota Motor Corporation

- Volkswagen AG

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 93014

The Europe Light Commercial Vehicles Market size is estimated at 97.85 billion USD in 2025, and is expected to reach 132.5 billion USD by 2029, growing at a CAGR of 7.87% during the forecast period (2025-2029).

The European LCV market thrives on infrastructure investments and e-commerce surge, with continued growth expected amid urbanization and green initiatives

- In 2022, the light commercial vehicle (LCV) market in Europe witnessed a robust 6.2% growth in sales volume. This positive momentum is expected to carry forward, with a projected growth of 3.5% in 2023. This growth is primarily fueled by heightened infrastructure investments and the surging tide of e-commerce. The EU's focus on transportation and energy projects has stimulated demand for LCVs, especially from the construction and utilities sectors. The expansion of last-mile delivery networks, a trend amplified during the pandemic, has spurred purchases of light commercial vans for parcel and food delivery.

- From 2017 to 2023, Europe's LCV market witnessed a remarkable upswing, with volumes surging by 38%. This surge was propelled by the e-commerce boom, which fueled the expansion of delivery networks and subsequently boosted van sales. Additionally, replacement demand from sectors like retail, construction, and services played a pivotal role. While the market contracted in 2020 due to pandemic disruptions, it swiftly rebounded, riding the wave of accelerated digital adoption. Overall, steady economic growth and robust infrastructure investments were key drivers of the European LCV market's expansion during this period.

- The LCV market in Europe is poised to register a CAGR of 3.1% from 2024 to 2030. This growth trajectory will be propelled by ongoing infrastructure development, the continued expansion of last-mile delivery networks, and the rising urbanization trend. These factors, coupled with the increasing demand for LCVs in services, food delivery, and construction sectors, paint a promising outlook. However, the market may face headwinds as evolving regulations on emissions and urban access could bolster the adoption of alternatively fueled vans.

Country-specific trends within the European light commercial vehicles market highlight the region's push toward reducing emissions and enhancing efficiency

- Major European markets witnessed varying LCV sales volumes in 2022, reflecting their distinct economic landscapes. Germany, buoyed by a resilient economy, saw a robust 6.3% growth. Conversely, the United Kingdom faced economic uncertainties, leading to a contraction of 2.1% in LCV sales. France, Italy, and Spain experienced declines of 3% to 5%, aligning with broader macroeconomic challenges. However, as the post-pandemic conditions improve, 2023 is projected to witness a rebound, with most countries eyeing a volume growth of 4-6%.

- From 2017 to 2021, the prominent European LCV markets - Germany, France, Italy, Spain, and Poland - showcased healthy expansion, registering a pre-pandemic CAGR of approximately 3-5%. This growth was propelled by robust economic activities, particularly in industries like construction, delivery, and services. While the pandemic-induced contractions in 2020 were relatively short-lived, the recovery has been uneven, primarily due to disparities in fiscal stimulus measures and vulnerabilities in industries such as retail and hospitality.

- The European LCV market is poised for a steadier growth trajectory, with an anticipated annual average of 3-4% from 2023 to 2029. Factors such as infrastructure investments, the rise of last-mile delivery networks, and ongoing economic recovery are expected to bolster demand. However, risks loom from factors like high inflation, energy costs, and political uncertainties. Additionally, the market's shift toward electric drivetrains will further shape its dynamics. The European LCV market is set for a gradual expansion in the long run.

Europe Light Commercial Vehicles Market Trends

Environmental concerns, government support, and decarbonization goals fuel European electric vehicle demand and sales

- The demand and sales of electric vehicles in European countries have grown significantly over the past few years. Germany witnessed a growth in the sales of electric cars by 22% in 2022 over 2021, followed by the United Kingdom with an 18.40% increase in 2022 over 2021. Growing environmental concerns, stringent governmental norms, advantages of electric vehicles such as fuel efficiency, low service cost, no carbon emissions, and subsidies by the government are some of the factors contributing to the growth of electric vehicles in European countries.

- The demand for electric commercial vehicles, especially light trucks, is growing gradually in European countries. Moreover, the governments of various countries are also supporting the adoption of electric vehicles. In November 2021, the government of the United Kingdom announced a pledge that all heavy-duty vehicles would be zero-emission by the year 2040. Such factors have increased the sales of electric commercial vehicles in the United Kingdom by 23.17% in 2022 over 2021, and similar practices in various countries are enhancing the demand for electric commercial vehicles across Europe.

- It is projected that the electrification of vehicles in European countries is expected to grow tremendously in the next few years. The efforts of the governments in the regions for decarbonization are expected to drive the electric commercial vehicle market in Europe. For instance, in January 2022, the transport minister of Germany announced a goal to put 15 million electric vehicles on the road by 2030. Such factors are expected to increase the sales of electric vehicles during the 2024-2030 period in European countries.

Europe Light Commercial Vehicles Industry Overview

The Europe Light Commercial Vehicles Market is moderately consolidated, with the top five companies occupying 62.47%. The major players in this market are Fiat Chrysler Automobiles N.V, Ford Motor Company, Groupe Renault, Peugeot S.A. and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Light Commercial Pick-up Trucks

- 5.1.1.2 Light Commercial Vans

- 5.1.1 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 CNG

- 5.2.2.1.2 Diesel

- 5.2.2.1.3 Gasoline

- 5.2.2.1.4 LPG

- 5.2.1 Hybrid and Electric Vehicles

- 5.3 Country

- 5.3.1 Austria

- 5.3.2 Belgium

- 5.3.3 Czech Republic

- 5.3.4 Denmark

- 5.3.5 Estonia

- 5.3.6 France

- 5.3.7 Germany

- 5.3.8 Ireland

- 5.3.9 Italy

- 5.3.10 Latvia

- 5.3.11 Lithuania

- 5.3.12 Norway

- 5.3.13 Poland

- 5.3.14 Russia

- 5.3.15 Spain

- 5.3.16 Sweden

- 5.3.17 UK

- 5.3.18 Rest-of-Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Fiat Chrysler Automobiles N.V

- 6.4.2 Ford Motor Company

- 6.4.3 Groupe Renault

- 6.4.4 Mercedes-Benz

- 6.4.5 Peugeot S.A.

- 6.4.6 Toyota Motor Corporation

- 6.4.7 Volkswagen AG

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

2025年全球前端加強筋市場報告

2025年全球前端加強筋市場報告 汽車輕量化市場:2025-2032年全球預測(材料類型、車輛類型、應用、動力傳動系統類型、製造流程和銷售管道)輕型商用車市場按重量等級、燃料類型、車輛類型、變速箱類型、功率輸出和最終用戶行業分類 - 全球預測 2025-2032

汽車輕量化市場:2025-2032年全球預測(材料類型、車輛類型、應用、動力傳動系統類型、製造流程和銷售管道)輕型商用車市場按重量等級、燃料類型、車輛類型、變速箱類型、功率輸出和最終用戶行業分類 - 全球預測 2025-2032 全球汽車輕量化市場(2024-2030 年)

全球汽車輕量化市場(2024-2030 年) 全球輕型車市場全球廂型車市場全球廂型車市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測全球輕型商用車市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測拉丁美洲輕型商用車(2025年):Frost Radar全球小型車市場

全球輕型車市場全球廂型車市場全球廂型車市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測全球輕型商用車市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測拉丁美洲輕型商用車(2025年):Frost Radar全球小型車市場

▼