|

市場調查報告書

商品編碼

1693623

印度電動車:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)India Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

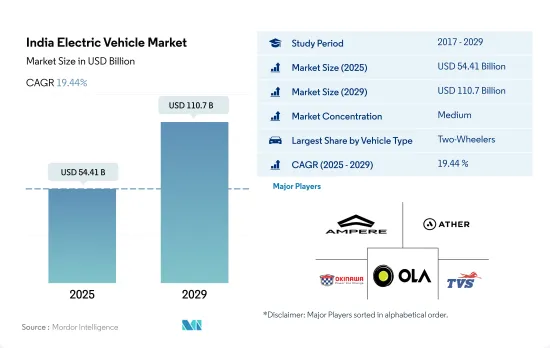

印度電動車市場規模預計在 2025 年為 544.1 億美元,預計到 2029 年將達到 1,107 億美元,預測期內(2025-2029 年)的複合年成長率為 19.44%。

印度在各個車型中採用電動車(EV)的綜合戰略正在推動向永續交通的轉變。

- 印度電動車(EV)市場根據車型分為乘用車、商用車和二輪車,正在經歷重大變革時期,這反映了該國致力於採用清潔能源和減少二氧化碳排放的承諾。每個部分都迎合不同的市場動態、用戶需求和成長潛力,描繪出印度邁向電動車的全貌。

- 受消費者意識增強、政府政策利好以及國內外製造商日益增多的影響,電動乘用車在印度市場正穩步普及。儘管目前與傳統汽車相比規模較小,但該細分市場正在迅速擴張,從面向大眾市場的經濟型車型到面向豪華市場的高檔電動車。

- 電動商用車產業雖然仍處於起步階段,但預計將呈現顯著成長。這種成長的動力源自於物流和運輸業對永續性和成本效率的日益關注。在政府旨在減少污染和促進公共交通和貨物運輸電動化的措施的支持下,電動公車、卡車和貨車正逐步引入都市區車隊。電動商用車的營運成本優勢,加上各州和中央政府的激勵措施,正在鼓勵車隊營運商和公司轉向電動選項。這一領域的成長對於實現印度雄心勃勃的環境目標和改善城市空氣品質至關重要。

印度電動車市場趨勢

政府措施和嚴格規範推動印度電動車市場快速成長

- 隨著印度政府制定積極的策略來對抗污染,印度的電動車 (EV) 市場正處於成長階段。 2015年啟動的Fame India計畫在推動汽車電氣化方面發揮了關鍵作用。基於其成功經驗,Fame 第二階段計劃將持續到 2022 年 4 月,預計將進一步推動電動車的銷量,尤其是在 2021 年,政府將為電池容量高達 15kWh 的電動車提供 10,000 印度盧比(約 1,000 萬美元)的補貼。

- 印度各邦政府正大力引進電動公車,以擺脫內燃機(ICE)公車的束縛。此舉不僅可以降低營運成本,還可以抑制碳排放並改善空氣品質。引人注目的是,德里政府已於 2021 年 3 月批准採購 300 輛新型低地板電動(AC)公車,其中 100 輛將於 2022 年 1 月上路。這些舉措導致印度對電動商用車的需求大幅成長,2022 年與 2021 年相比成長了 62.58%。

- 受政府嚴格標準的推動,近年來電動車的需求激增。 2021年8月,印度政府宣布了一項車輛報廢政策,旨在逐步淘汰污染嚴重且不合規的車輛,無論其使用年限為何。該政策將於 2024 年實施,旨在推動消費者購買電動車。此外,政府還設定了一個雄心勃勃的目標,即到 2030 年使印度 30% 的汽車實現電動化。這些舉措預計將在 2024 年至 2030 年期間促進印度的電動車銷售。

印度電動汽車產業概況

印度電動車市場適度整合,前五大廠商佔43.74%的市場。市場的主要企業有:Ampere Vehicle Private Limited、Ather Energy Pvt。有限公司、沖繩汽車技術私人有限公司有限公司、Ola Electric Mobility Pvt. Ltd. 和 TVS Motor Company Limited(按字母順序)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 人口

- 人均GDP

- 消費者汽車支出(cvp)

- 通貨膨脹率

- 汽車貸款利率

- 共乘

- 電氣化的影響

- 電動車充電站

- 電池組價格

- 新款 Xev 車型發布

- 二手車銷售

- 燃油價格

- OEM生產統計

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 車輛類型

- 商用車

- 公車

- 大型商用卡車

- 輕型商用皮卡車

- 輕型商用廂型車

- 中型商用卡車

- 搭乘用車

- 掀背車

- 多用途車輛

- 轎車

- SUV

- 摩托車

- 商用車

- 燃料類別

- FCEV

- HEV

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Ampere Vehicle Private Limited

- Ather Energy Pvt. Ltd.

- BYD India Private Limited

- Hero Electric Vehicles Pvt. Ltd.

- Hyundai Motor India Limited

- JBM Auto Limited

- Mahindra & Mahindra Limited

- MG Motor India Private Limited

- Okinawa Autotech Pvt. Ltd.

- Ola Electric Mobility Pvt. Ltd.

- Olectra Greentech Ltd.

- Switch Mobility(Ashok Leyland Limited)

- Tata Motors Limited

- Toyota Kirloskar Motor Pvt. Ltd.

- TVS Motor Company Limited

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

The India Electric Vehicle Market size is estimated at 54.41 billion USD in 2025, and is expected to reach 110.7 billion USD by 2029, growing at a CAGR of 19.44% during the forecast period (2025-2029).

India's comprehensive strategy to adopt electric vehicles (EVs) across various vehicle categories is driving the nation's transition toward sustainable mobility

- India's electric vehicle (EV) market, segmented by vehicle type into passenger cars, commercial vehicles, and two-wheelers, is undergoing a significant transformation, reflecting the country's commitment to embracing clean energy and reducing carbon emissions. Each segment caters to distinct market dynamics, user needs, and growth potential, painting a comprehensive picture of India's journey toward electric mobility.

- Electric passenger cars are steadily gaining traction in the Indian market, driven by increasing consumer awareness, favorable government policies, and the growing presence of both international and local manufacturers. Although currently small compared to conventional vehicles, the segment is witnessing a rapid expansion in offerings, ranging from affordable models aimed at the mass market to premium electric cars catering to the luxury segment.

- The electric commercial vehicle sector, though still in its early stages, is set to witness significant growth. This growth is being driven by a rising emphasis on sustainability and cost-effectiveness within the logistics and transportation sectors. Electric buses, trucks, and vans are gradually making their way into urban fleets, supported by government initiatives aimed at reducing pollution and promoting electric mobility in public transportation and goods delivery. The operational cost benefits of electric commercial vehicles, coupled with various state and central government incentives, are encouraging fleet operators and businesses to transition toward electric options. This segment's growth is critical for achieving India's ambitious environmental targets and improving urban air quality.

India Electric Vehicle Market Trends

Government initiatives and stringent norms drive rapid growth in the electric vehicle market in India

- India's electric vehicle (EV) market is in a growth phase, with the government actively formulating strategies to combat pollution. The Fame India scheme, launched in 2015, has played a pivotal role in driving vehicle electrification. Building on its success, Fame Phase 2, active till April 2022, further bolstered EV sales, especially in 2021, with the government offering subsidies like INR 10,000 grants for electric cars with battery capacities up to 15 kWh.

- State governments across India are increasingly incorporating electric buses into their fleets, aiming to transition from internal combustion engine (ICE) buses. This move not only cuts operational costs but also curbs carbon emissions and improves air quality. In a notable move, the Delhi government greenlit the procurement of 300 new low-floor electric (AC) buses in March 2021, with 100 of them hitting the roads in January 2022. These initiatives contributed to a significant 62.58% surge in demand for electric commercial vehicles in India in 2022 over 2021.

- The demand for electric cars has surged in recent times, driven by the government's introduction of stringent norms. In August 2021, the Indian government unveiled the Vehicle Scrappage Policy, targeting the phasing out of polluting and unfit vehicles, irrespective of their age. This policy, set to be implemented by 2024, is steering consumers toward electric cars. Additionally, the government has set an ambitious target of having 30% of all cars in India electrified by 2030. These initiatives are poised to propel electric car sales during the 2024-2030 period in India.

India Electric Vehicle Industry Overview

The India Electric Vehicle Market is moderately consolidated, with the top five companies occupying 43.74%. The major players in this market are Ampere Vehicle Private Limited, Ather Energy Pvt. Ltd., Okinawa Autotech Pvt. Ltd., Ola Electric Mobility Pvt. Ltd. and TVS Motor Company Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Impact Of Electrification

- 4.8 EV Charging Station

- 4.9 Battery Pack Price

- 4.10 New Xev Models Announced

- 4.11 Used Car Sales

- 4.12 Fuel Price

- 4.13 Oem-wise Production Statistics

- 4.14 Regulatory Framework

- 4.15 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Buses

- 5.1.1.2 Heavy-duty Commercial Trucks

- 5.1.1.3 Light Commercial Pick-up Trucks

- 5.1.1.4 Light Commercial Vans

- 5.1.1.5 Medium-duty Commercial Trucks

- 5.1.2 Passenger Vehicles

- 5.1.2.1 Hatchback

- 5.1.2.2 Multi-purpose Vehicle

- 5.1.2.3 Sedan

- 5.1.2.4 Sports Utility Vehicle

- 5.1.3 Two-Wheelers

- 5.1.1 Commercial Vehicles

- 5.2 Fuel Category

- 5.2.1 FCEV

- 5.2.2 HEV

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ampere Vehicle Private Limited

- 6.4.2 Ather Energy Pvt. Ltd.

- 6.4.3 BYD India Private Limited

- 6.4.4 Hero Electric Vehicles Pvt. Ltd.

- 6.4.5 Hyundai Motor India Limited

- 6.4.6 JBM Auto Limited

- 6.4.7 Mahindra & Mahindra Limited

- 6.4.8 MG Motor India Private Limited

- 6.4.9 Okinawa Autotech Pvt. Ltd.

- 6.4.10 Ola Electric Mobility Pvt. Ltd.

- 6.4.11 Olectra Greentech Ltd.

- 6.4.12 Switch Mobility (Ashok Leyland Limited)

- 6.4.13 Tata Motors Limited

- 6.4.14 Toyota Kirloskar Motor Pvt. Ltd.

- 6.4.15 TVS Motor Company Limited

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

電動車市場(按車輛類型、電池技術、推進類型、組件類型、最終用戶和銷售管道分類)—2025-2032 年全球預測

電動車市場(按車輛類型、電池技術、推進類型、組件類型、最終用戶和銷售管道分類)—2025-2032 年全球預測 全球電動車融資市場

全球電動車融資市場 2025年全球小型電動車市場報告2025年全球電動車市場報告

2025年全球小型電動車市場報告2025年全球電動車市場報告 電動車市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032 年)

電動車市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032 年) 印度電動車市場,2024-2031年

印度電動車市場,2024-2031年 EV的各地區預測 - 北美全球電動車太陽能天窗市場

EV的各地區預測 - 北美全球電動車太陽能天窗市場 全球電動車充電管理軟體平台市場:按應用、產品和國家分析和預測(2025-2034年)

全球電動車充電管理軟體平台市場:按應用、產品和國家分析和預測(2025-2034年) 日本電動車市場報告(按零件、充電類型、推進類型(電池電動車、燃料電池電動車、插電式混合動力電動車、混合動力電動車)、車輛類型和地區分類)2025 年至 2033 年

日本電動車市場報告(按零件、充電類型、推進類型(電池電動車、燃料電池電動車、插電式混合動力電動車、混合動力電動車)、車輛類型和地區分類)2025 年至 2033 年