|

市場調查報告書

商品編碼

1693549

美國柔版印刷:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)United States Flexographic Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

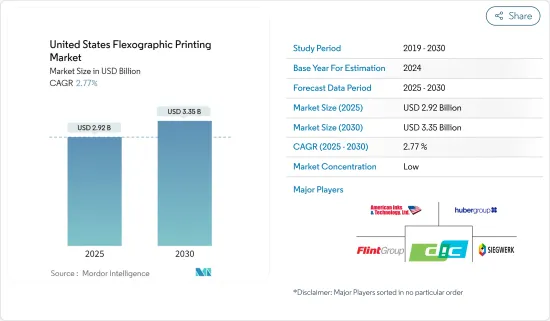

預計 2025 年美國柔版印刷市場規模為 29.2 億美元,到 2030 年將達到 33.5 億美元,預測期內(2025-2030 年)的複合年成長率為 2.77%。

主要亮點

- 柔版印刷的速度高達每分鐘 750 公尺(或 2,000 英尺)。該工藝透過在單一途徑中高效結合印刷和幾乎所有附加操作,實現了顯著的規模經濟效益。包裝印刷商和轉換器擴大使用柔版印刷作為其業務的關鍵工具。這是因為柔版印刷具有轉換速度快、影像品質高、自動化程度高且成本低等特點。

- 柔版印刷的改進是由受益於卓越印刷效果的最終用戶所推動的。推動柔版印刷產業技術進步的兩個關鍵因素是:對產品多樣性的需求不斷增加以及生產週期縮短的趨勢。向這些新興國家擴張的目的是提高日益數位化的市場的效率。

- UV柔版油墨和清漆被廣泛使用並且越來越受歡迎。採用UV固化技術的主要原因是它不使用溶劑,從而減少了排放,這可能是最初的好理由之一。然而,目前許多與印刷相關的領域正在考慮使用紫外線固化油墨。這是因為它具有出色的印刷品質、對軟性和各種其他基材的良好附著力、高耐化學性和耐產品性以及快速的運行速度。

- 紫外線固化柔版印刷油墨可用於在各種最終產品基材上進行印刷。其中包括優格杯和瓶蓋、湯和香辛料紙盒、軟質包裝、牛奶和果汁紙盒、寵物食品包裝、香菸盒等。

- 此外,隨著消費者、零售商和客戶需求的變化,包裝印刷市場也迅速變化。對新產品品種和更短交貨時間的需求不斷增加,推動了柔版印刷技術的進步,以提高日益數位化的市場的效率。

- 例如,Imageworks 計劃於 2023 年 4 月在賓州萊維敦開設一個新部門和柔印創新中心。該物業位置便利,可輕鬆前往費城國際機場和紐瓦克國際機場。該中心是產業供應商展示柔版印刷產業先進技術的協作空間。

- 相反,數位技術最初的成本可能比印刷技術高,但從長遠來看,它會為您節省金錢。這一因素有望為柔版印刷帶來有效的競爭,因為價格比較是同類的。此外,數位印刷的更長的使用壽命和更高的轉售價值也影響這些系統的採用。

美國柔版印刷市場的趨勢

標籤和標誌越來越受歡迎

- 柔版印刷是標籤印刷行業中一個快速成長的領域。這種方法可以實現高速生產,比其他印刷方法更快地生產自訂的高品質標籤。柔版印刷用於化妝品、藥品、食品和使用自動貼標設備的行業。事實證明,對於小批量到大批量的標籤列印應用來說,這一流程都是高效且快速的。

- 此外,技術的進步使得美國的柔版標籤印刷機在效率和速度方面超越了其他幾種標籤印刷技術。柔版標籤印刷機已成為食品飲料、藥品和消費品的首選印刷技術,因為它們可以快速印刷各種材料的標籤卷,而不會影響品質。

- 人們越來越重視消費者的便利性和品牌差異化,這推動了對創新且有吸引力的包裝解決方案的需求。標籤對於品牌推廣、提供重要產品資訊和確保法規合規性至關重要。

- 根據美國人口普查局的數據,到 2023 年,食品和飲料零售商的價值將達到約 9,853 億美元,而 2018 年為 7,498 億美元。

- 此外,隨著零售食品和飲料行業的興起,包裝(包括標籤和標籤)的需求也在增加。隨著生產和銷售的產品越來越多,對標籤解決方案的需求也越來越大,以確保產品識別、品牌推廣和法規遵循。

折疊紙盒佔據很大市場佔有率

- 美國是折疊紙盒最大的生產國和消費國之一,下游產業需求龐大。美國紙包裝出口也一直在穩定成長。

- 美國也是國際紙業公司、WestRock、美國包裝公司、Sonoco Production Company、Sealed Air Corp 和 Graphic Packaging International 等重要折疊紙盒公司的所在地。

- 該市場已經出現了多種專注於折疊紙盒包裝應用的柔版印刷機產品創新。例如,2024年2月,BOBST推出了針對標籤和包裝印刷產業的擴展色域技術oneECG。

- 此外,這項創新將被整合到BOBST窄幅和中幅印刷機中,旨在重新定義效率和品質標準。透過提高效率和質量,這項創新使加工商受益並加強了 BOBST 在印刷技術領域的地位。

- 值得注意的是,Catapult Print 於 2024 年 1 月安裝 Nilpeter FA-26 印刷機,標誌著其在重新定義印刷、顛覆市場和改變美國軟包裝市場的使命上邁出了重要一步。這款先進印刷機的推出彰顯了 Catapult Print 對印刷業創新與品質的承諾。此舉表明 Catapult Print 致力於保持行業領先地位並提供印刷解決方案。

- 此外,柔版印刷採用凸版印刷將圖案印在包裝上,確保長期保持一致的高品質印刷。柔版印刷具有成本效益,特別是對於折疊式紙盒等較小的計劃。伊利諾伊州折疊式紙板盒製造業的成長顯示對包裝材料的需求不斷增加,預計到 2024 年銷售額將達到 9.8569 億美元。

- 這一趨勢支持了柔版印刷的需求。隨著企業尋求可靠、經濟的印刷解決方案,柔印的多功能性和品質使其成為首選。柔印能夠保持印刷品質且價格實惠,因此非常適合滿足市場需求不斷成長的包裝行業不斷變化的需求。

美國柔版印刷產業概況

美國柔版印刷市場較為分散,由許多國內外公司組成。公司透過夥伴關係、投資和收購來增強其產品供應並獲得永續的競爭優勢。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場動態

- 市場促進因素

- 可以以合理的成本提高生產速度

- 紫外線固化油墨需求不斷成長

- 包裝產業預計將推動設備和油墨類別的需求

- 市場限制

- 新印刷技術的出現與數位媒體的轉變

第6章市場區隔

- 透過印刷油墨

- 按油墨技術

- 水性

- 溶劑型

- UV固化型

- 按應用

- 包裹

- 靈活的

- 難的

- 標籤和標記

- 紙印刷

- 按油墨技術

- 按設施

- 按應用程式類型

- 窄帶

- 中型網路

- 送紙

- 其他印刷設備

- 按階段

- 預印本

- 後列印

- 按最終用戶

- 紙容器

- 軟包裝

- 標籤

- 印刷媒體

- 其他最終用戶

- 按應用程式類型

第7章競爭格局

- 公司簡介

- DIC Corporation

- Siegwerk Group

- Flint Group

- Hubergroup USA Inc.

- American Inks & Technology

- Inx International Ink Co.

- Wikoff Color Corporation

- ACTEGA GmbH

- Zeller+Gmelin Corporation

- Kolorcure Corporation

- Comexi Group Industries SAU

- Bobst Group SA

- Heidelberger Druckmaschinen AG

- Omet Americas Inc.(Omet Group)

- MPS Systems BV

- Mark Andy Inc.

- Windmoller & Holscher KG

- CMS Industrial Technologies LLC

- Nilpeter USA Inc.

第8章 市場投資

第9章:市場的未來

簡介目錄

Product Code: 92637

The United States Flexographic Printing Market size is estimated at USD 2.92 billion in 2025, and is expected to reach USD 3.35 billion by 2030, at a CAGR of 2.77% during the forecast period (2025-2030).

Key Highlights

- Flexographic printing offers speeds of up to 750 m (or 2,000 ft) per minute. The process offers significant economies of scale by efficiently combining printing with almost any additional process into a single-pass operation. Package printers and converters increasingly use flexographic printing as a crucial tool for their businesses because it offers quicker changeovers, high image quality, and sophisticated automation at a lesser cost.

- The improvements in flexography are driven by end users who gain from the excellent print results. The flexographic industry is experiencing technological advancements driven by two key factors: the growing demand for product variety and the trend toward shorter production runs. These developments aim to enhance efficiency in a market that is becoming increasingly digitalized.

- UV flexo printing inks and varnishes are widely used and continue gaining popularity. A primary justification for using UV curing technology is the absence of solvents, which lowers emissions and is probably one of the original justifications. However, UV-cured inks are currently being considered in many printing-related fields because of their superior print quality, good adhesion to flexible and various other substrates, high chemical and product resistance, and fast running speeds.

- UV-curing flexo inks are used to print on a wide array of finished product substrates. These include yogurt cups and tops, soup and spice packets, flexible packaging, milk and juice cartons, pet food packaging, and cigarette packs.

- Further, the packaging printing marketplace is changing rapidly, with consumer, retailer, and client demand shifting. Increasing demand for new variety and shorter run lengths are driving advancements in flexographic technology, which aims to improve efficiency in an increasingly digitalized market.

- For instance, in April 2023, Imageworx planned to establish a new division and the Flexographic Innovation Center in Levittown, Pennsylvania. The facility's location provides easy access from Philadelphia and Newark International airports. This center is a collaborative space for industry vendors to demonstrate their advanced technologies to the flexographic printing industry.

- On the contrary, digital technologies may initially incur more significant expenses than printed materials but will present long-term savings. This factor is poised to provide effective competition to flexographic printing, which is identical in the price comparison. Further, the longer lifespan and high resale value of digital printing also influence the adoption of these systems.

United States Flexographic Printing Market Trends

Tags and Labels to Witness Significant Growth

- Flexographic printing has emerged as the fastest-growing segment in the label printing industry. This method offers high-speed production capabilities, creating custom, high-quality labels significantly faster than other printing techniques. Industries such as cosmetics, pharmaceuticals, food, and those employing automatic labeling equipment utilize flexographic printing. This process proves efficient and rapid for label printing applications ranging from low to high volumes.

- Additionally, due to technological advancements, flexographic label printing machines outperform several other label printing techniques in terms of efficiency and speed in the United States. Flexographic label presses are the printing technology for food, beverage, pharmaceutical, and consumer items since they can quickly print label rolls of varied materials without compromising quality.

- The increasing emphasis on consumer convenience and brand differentiation drives the need for innovative and attractive packaging solutions. Labels are pivotal in branding, providing essential product information, and ensuring regulatory compliance.

- According to the US Census Bureau, the value of retail food and beverage stores was approximately USD 985.30 billion in 2023, compared with USD 749.8 billion in 2018.

- Futhermore, With the rise of the retail food and beverage industry, there is a corresponding increase in the demand for packaging, which includes tags and labels. As more products are produced and sold, there is a greater need for labeling solutions to ensure product identification, branding, and compliance with regulations.

Folding Carton Holds a Significant Market Share

- The United States has been one of the largest folding carton box producers and consumers, owing to the significant demand in its downstream industries. Folding carton packaging exports from the United States are also steadily increasing.

- The United States is also home to significant folding carton companies, including International Paper Company, WestRock, Packaging Corporation of America, Sonoco Production Company, Sealed Air Corp, and Graphic Packaging International.

- The market witnessed various product innovations in flexographic presses specifically for folding carton packaging applications. For instance, in February 2024, BOBST introduced oneECG, an extended colour gamut technology, in the label and packaging printing industry.

- Furthermore, This innovation is integrated into BOBST narrow and mid-web printing presses, aiming to redefine efficiency and quality standards. By enhancing efficiency and quality, this innovation benefits converters and solidifies BOBST's position as a player in printing technology.

- Notably, in January 2024, Catapult Print's installation of the Nilpeter FA-26 press marked a significant stride in its mission to redefine print, disrupt the market, and induce change in the US flexible packaging market. Introducing this advanced press underscored Catapult Print's commitment to innovation and quality in the printing industry. This move signifies Catapult Print's dedication to staying at the forefront of the industry and delivering printing solutions.

- Furthermore, flexographic printing employs relief plates to stamp designs onto packaging, ensuring consistent, high-quality prints over time. It is cost-effective, particularly for small-scale projects like foldable carton boxes. The growth in Illinois' folding paperboard box manufacturing industry, with revenue expected to reach USD 985.69 million in 2024, indicates increasing demand for packaging materials.

- This trend supports the demand for flexographic printing. As businesses seek reliable, affordable printing solutions, flexo's versatility and quality position it as a preferred choice. Its ability to maintain print quality and affordability makes it ideal for meeting the evolving needs of the packaging industry amid growing market demands.

United States Flexographic Printing Industry Overview

The United States flexographic printing market is fragmented due to the presence of numerous players, both domestic and global. Players are adopting partnerships, investments, and acquisitions to enhance their product offerings and gain sustainable competitive advantages.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Enables Higher Production Speeds Within Reasonable Cost Overlay

- 5.1.2 Growing Demand for UV-curable Inks

- 5.1.3 The Packaging Industry Is Expected To Drive Demand For Both Equipment And Inks Category

- 5.2 Market Restraints

- 5.2.1 Advent of New Printing Technologies and Shift to Digital Mediums

6 MARKET SEGMENTATION

- 6.1 By Printing Ink

- 6.1.1 By Ink Technology

- 6.1.1.1 Water-based

- 6.1.1.2 Solvent-based

- 6.1.1.3 UV-curable

- 6.1.2 By Application Type

- 6.1.2.1 Packaging

- 6.1.2.1.1 Flexible

- 6.1.2.1.2 Rigid

- 6.1.2.2 Tags and Labels

- 6.1.2.3 Paper-based Printing

- 6.1.1 By Ink Technology

- 6.2 By Equipment

- 6.2.1 By Application Type

- 6.2.1.1 Narrow Web

- 6.2.1.2 Medium Web

- 6.2.1.3 Sheetfed

- 6.2.1.4 Other Printing Equipment

- 6.2.2 By Phase

- 6.2.2.1 Pre-print

- 6.2.2.2 Post-print

- 6.2.3 By End User

- 6.2.3.1 Folding Carton

- 6.2.3.2 Flexible Packaging

- 6.2.3.3 Labels

- 6.2.3.4 Print Media

- 6.2.3.5 Other End Users

- 6.2.1 By Application Type

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 DIC Corporation

- 7.1.2 Siegwerk Group

- 7.1.3 Flint Group

- 7.1.4 Hubergroup USA Inc.

- 7.1.5 American Inks & Technology

- 7.1.6 Inx International Ink Co.

- 7.1.7 Wikoff Color Corporation

- 7.1.8 ACTEGA GmbH

- 7.1.9 Zeller+Gmelin Corporation

- 7.1.10 Kolorcure Corporation

- 7.1.11 Comexi Group Industries SAU

- 7.1.12 Bobst Group SA

- 7.1.13 Heidelberger Druckmaschinen AG

- 7.1.14 Omet Americas Inc. (Omet Group)

- 7.1.15 MPS Systems BV

- 7.1.16 Mark Andy Inc.

- 7.1.17 Windmoller & Holscher KG

- 7.1.18 CMS Industrial Technologies LLC

- 7.1.19 Nilpeter USA Inc.

8 INVESTMENT OF THE MARKET

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

柔版印刷版材市場規模、佔有率及成長分析(依規格、類型、應用、設計、油墨相容性及地區分類)-2026-2033年產業預測

柔版印刷版材市場規模、佔有率及成長分析(依規格、類型、應用、設計、油墨相容性及地區分類)-2026-2033年產業預測 柔版印刷機:全球市佔率及排名、總收入及需求預測(2025-2031年)

柔版印刷機:全球市佔率及排名、總收入及需求預測(2025-2031年) 柔版印刷電子市場分析與至2034年的預測-按類型、產品、技術、應用、材料類型、組件、過程、最終用戶和功能分類

柔版印刷電子市場分析與至2034年的預測-按類型、產品、技術、應用、材料類型、組件、過程、最終用戶和功能分類 柔版印刷機市場按類型、技術、基材、油墨類型、應用和最終用途產業分類-全球預測,2025-2032

柔版印刷機市場按類型、技術、基材、油墨類型、應用和最終用途產業分類-全球預測,2025-2032 2034年全球柔版印刷技術市場機會與策略2025年全球柔版印刷技術市場報告2025年柔版印刷機全球市場報告

2034年全球柔版印刷技術市場機會與策略2025年全球柔版印刷技術市場報告2025年柔版印刷機全球市場報告 柔版印刷市場:2025-2030 年預測

柔版印刷市場:2025-2030 年預測 柔版印刷:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)柔版印刷機:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

柔版印刷:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)柔版印刷機:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

▼