|

市場調查報告書

商品編碼

1693512

越南特種肥料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Vietnam Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

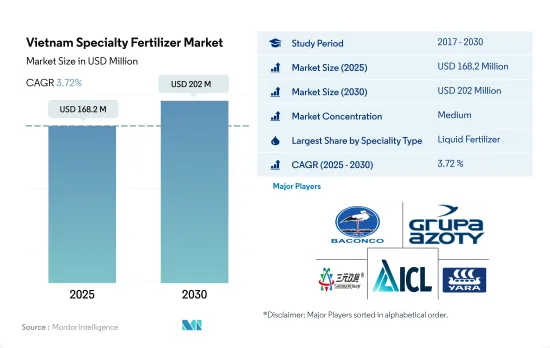

越南特種肥料市場規模預計在 2025 年為 1.682 億美元,預計到 2030 年將達到 2.02 億美元,預測期內(2025-2030 年)的複合年成長率為 3.72%。

高效能肥料需求不斷成長推動了特種肥料的需求

- 在越南特種肥料市場,水溶性肥料預計到2022年將達到6,590萬美元。水溶性肥料使農民能夠靈活地調整營養濃度,以適應植物的生長週期。透過在植物根部附近施用可溶性肥料,與整個生長季節大面積集中施肥相比,農民可以節省成本。這些優勢正在推動越南對水溶性肥料的需求。

- 2020年越南特種肥料市場規模減少了1,510萬美元,主因新冠疫情封鎖導致國際貿易中斷。這一下降趨勢與去年同期一致。此外,市場還面臨氣溫波動、降雨不穩定和乾旱等挑戰。

- 越南特種肥料市場以液體肥料為主。隨著對提高作物品質、滿足出口標準和採用精密農業的日益重視,預計該領域園藝作物的價值在 2023 年至 2030 年期間的複合年成長率將達到 4.6%。

- 控釋肥料(CRF)和緩釋肥料(SRF)會根據土壤條件逐漸、持續地釋放養分,以滿足作物整個季節的需求。 CRF 和 SRF 的這一獨特特性不僅減少了肥料的使用和環境破壞,而且還為農民帶來了經濟效益。因此,預計這些肥料的市場將在 2023 年至 2030 年間經歷顯著成長。

越南特種肥料市場趨勢

越南政府正在推行降低生產成本的政策,預計將增加田間作物的種植面積。

- 越南將大量土地用於田間作物,主要種植水稻、玉米等主糧。多樣化的氣候和地形使得越南可以種植多種作物。然而,在研究期間,田間作物種植面積減少了 6.6%。

- 米是越南的主食,也是越南的主要田間作物。佔總種植面積的81.8%,其次是玉米,佔10.2%。預計2022年越南米產量將達到4,390萬噸左右,鞏固其世界主要出口國之一的地位。

- 越南經歷三個不同的生長季節:冬季到春季(早期)、夏季到秋季(中期)和秋季到冬季(長雨季)。越南主要的農業基地是紅河Delta、湄公河Delta和南部階地。米是這三個地區的主要作物,光是湄公河三角洲地區就佔越南米出口的一半。

- 越南政府正在實施旨在降低生產成本的政策。這些措施包括減少化肥和農藥的使用,推廣本地生產的化肥,並強調化肥在提高田間作物產量、品質和盈利方面的作用。由於營養缺乏而導致的農作物減產不斷增加,以及需要高效肥料來對抗植物矮化,也是越南肥料市場強勁發展的因素。

氮是許多田間作物必需的營養元素,其施用量已顯著增加。

- 2022年,越南田間作物主要養分平均施用量為每公頃123.94公斤。在這一領域,穀類已成為化肥的最大消費品。其中,水稻、小麥和玉米位居越南穀類作物之首,同年主要養分平均施用量分別為每公頃155.49公斤、每公頃228.90公斤和每公頃148.49公斤。

- 在主要養分中,氮肥施用量最高,田間作物平均施用量為221.43公斤/公頃。對氮的重視源於其在促進作物生長許多方面的作用,包括犁地、葉面積發育、籽粒形成、灌漿和蛋白質合成。氮對產量和品質也有正面的影響。施氮量最高的是小麥,為492.06公斤/公頃,其次是水稻,為328.04公斤/公頃。

- 在越南永福省,有很大一部分土壤遭受劣化,其特徵是有機質含量低,總有效氮 (TAV) 含量低於 0.08%,總磷 (TP) 含量低於 0.04%,總鉀 (K) 含量低於 1.0%。此外,有效磷含量低於10 ppm。這些短缺導致越南的化肥消費量激增,從 1969 年的每公頃 49.2 公斤增加到 2018 年的每公頃 415.3 公斤,複合年成長率為 6.71%。

- 儘管越南43%的人口從事農業,但農業對GDP的貢獻卻很小,僅約12.36%。然而,隨著該國致力於穩定農業,預計對肥料的需求將繼續增加,從而推動2023年至2030年越南肥料市場的成長。

越南特種肥料產業概況

越南特種肥料市場適度整合,前五大公司佔60.32%。該市場的主要企業有:Baconco、Grupa Azoty SA(Compo Expert)、河北三元九七化肥、ICL Group Ltd 和 Yara International ASA(按字母順序排列)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 主要作物種植面積

- 田間作物

- 園藝作物

- 平均養分施用量

- 微量營養素

- 田間作物

- 園藝作物

- 主要營養素

- 田間作物

- 園藝作物

- 次要宏量營養素

- 田間作物

- 園藝作物

- 微量營養素

- 灌溉農田

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 專業類型

- CRF

- 聚合物塗層

- 聚合硫塗層

- 其他

- 液體肥料

- SRF

- 水溶性

- CRF

- 施肥方式

- 受精

- 葉面噴布

- 土壤

- 作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Baconco

- Grupa Azoty SA(Compo Expert)

- Haifa Group

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- ICL Group Ltd

- Yara International ASA

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

The Vietnam Specialty Fertilizer Market size is estimated at 168.2 million USD in 2025, and is expected to reach 202 million USD by 2030, growing at a CAGR of 3.72% during the forecast period (2025-2030).

The rising demand for highly efficient fertilizers is driving the demand for specialty fertilizers

- The Vietnamese specialized fertilizer market witnessed water-soluble fertilizers reaching a value of USD 65.9 million in 2022. These fertilizers offer farmers the flexibility to adjust nutrient concentrations as per the evolving needs of plants during their growth cycle. By applying soluble fertilizers near the plant's root zone, farmers can save costs compared to intensive fertilization across a large area for the entire growing season. These advantages are fueling the demand for water-soluble fertilizers in Vietnam.

- The year 2020 saw the Vietnam specialty fertilizer market value decline by USD 15.1 million, primarily due to disruptions in international trade caused by the COVID-19 lockdown. This decline followed a trend from the previous year. Additionally, the market faced challenges from temperature fluctuations, erratic rainfall, and droughts.

- Liquid fertilizers dominate the specialty fertilizer market in Vietnam. With a growing emphasis on improving crop quality, meeting export standards, and adopting precision farming, the value of horticulture crops in this segment is projected to register a CAGR of 4.6% from 2023 to 2030.

- Control-release fertilizers (CRFs) and slow-release fertilizers (SRFs) gradually release nutrients at a consistent pace, catering to crop needs throughout the season, influenced by soil conditions. This unique feature of CRFs and SRFs not only reduces fertilizer usage and environmental degradation but also brings economic benefits to farmers. Consequently, the market for these fertilizers is poised for significant growth during 2023-2030.

Vietnam Specialty Fertilizer Market Trends

The Vietnamese government has been promoting policies to reduce production costs, which is expected to increase the cultivation area under field crops

- Vietnam allocates significant land to field crops, with major focuses on rice, maize (corn), and other staples. Owing to its diverse climate and topography, Vietnam can cultivate a wide array of crops. However, the country witnessed a 6.6% decline in the area dedicated to field crop cultivation during the study period.

- Rice takes center stage as Vietnam's primary field crop, given its status as a staple food. It dominates the cultivation landscape, accounting for 81.8% of the total area, followed by corn at 10.2%. In 2022, Vietnam's rice production reached around 43.9 million metric tons, solidifying its position as a leading global exporter.

- Vietnam experiences three distinct cropping seasons: winter-spring (early season), summer-autumn (midseason), and autumn-winter (longer rainy season). Key agricultural hubs in the country encompass the Red River Delta, Mekong River Delta, and Southern Terrace. Rice stands as the primary crop across all three regions, with the Mekong Delta alone contributing to half of Vietnam's rice exports.

- The Vietnamese government has implemented policies aimed at reducing production costs. These measures include cutting back on fertilizer and pesticide usage, promoting locally-sourced fertilizers, and emphasizing their role in enhancing field crop productivity, quality, and profitability. The increase in crop failures due to nutrient deficiencies and the need for high-efficiency fertilizers to combat plant dwarfism are additional factors bolstering Vietnam's fertilizers market.

Nitrogen is a vital nutrient required for a range of field crops, and its application is notably higher

- In 2022, field crops in Vietnam saw an average application rate of 123.94 kg per hectare for primary nutrients. Within this segment, grains and cereals emerged as the largest consumers of fertilizers. Notably, rice, wheat, and maize stood out as the top cereal crops in Vietnam, with average primary nutrient application rates of 155.49 kg/ha, 228.90 kg/ha, and 148.49 kg/ha, respectively, in the same year.

- Among the primary nutrients, nitrogen took the lead, with an average application rate of 221.43 kg/hectare for field crops. This emphasis on nitrogen stems from its role in bolstering various aspects of crop growth, such as tillering, leaf area development, grain formation, filling, and protein synthesis. It also positively impacts both yield and quality. Wheat took the crown for the highest nitrogen application rate at 492.06 kg/ha, followed by rice at 328.04 kg/ha.

- In Vietnam's Vinh Phuc province, significant portions of soil suffer from degradation, characterized by low organic matter, total available nitrogen below 0.08%, total phosphorus below 0.04%, and total potassium below 1.0%. Additionally, available phosphorus falls below 10 ppm. These deficiencies have contributed to a surge in fertilizer consumption in Vietnam, rising from 49.2 kg/ha in 1969 to 415.3 kg/ha by 2018, marking an average annual growth rate of 6.71%.

- Despite 43% of Vietnam's population being involved in agriculture, the sector's contribution to the country's GDP remains modest, accounting for only about 12.36%. However, as the nation strives for agricultural stability, the demand for fertilizers continues to rise, propelling the growth of Vietnam's fertilizers market during 2023-2030.

Vietnam Specialty Fertilizer Industry Overview

The Vietnam Specialty Fertilizer Market is moderately consolidated, with the top five companies occupying 60.32%. The major players in this market are Baconco, Grupa Azoty S.A. (Compo Expert), Hebei Sanyuanjiuqi Fertilizer Co., Ltd., ICL Group Ltd and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Baconco

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.5 ICL Group Ltd

- 6.4.6 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

晶體肥料市場:2026-2032年全球市場預測(依養分類型、應用、形態、作物類型、作用機制與銷售管道)特種肥料市場:2026-2032年全球市場預測(依產品形式、作物類型、養分類型、施用方法、通路和最終用途分類)

晶體肥料市場:2026-2032年全球市場預測(依養分類型、應用、形態、作物類型、作用機制與銷售管道)特種肥料市場:2026-2032年全球市場預測(依產品形式、作物類型、養分類型、施用方法、通路和最終用途分類) 特種肥料市場規模、佔有率和趨勢分析報告:按技術、作物、類型、應用、地區和細分市場預測(2026-2033 年)

特種肥料市場規模、佔有率和趨勢分析報告:按技術、作物、類型、應用、地區和細分市場預測(2026-2033 年) 特種肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

特種肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球特種肥料市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球特種肥料市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球特種肥料市場報告

2026年全球特種肥料市場報告 特種肥料市場規模、佔有率和成長分析(按類型、技術、形態、作物類型、應用方法和地區分類)-2026-2033年產業預測全球特種肥料市場規模(依特種肥料類型、作物類型、施用方法、區域範圍及預測)

特種肥料市場規模、佔有率和成長分析(按類型、技術、形態、作物類型、應用方法和地區分類)-2026-2033年產業預測全球特種肥料市場規模(依特種肥料類型、作物類型、施用方法、區域範圍及預測) 特種肥料市場 - 全球產業規模、佔有率、趨勢、機會和預測,按作物類型、形式、應用方式、技術、地區和競爭細分,2020-2030 年中國特種肥料市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)

特種肥料市場 - 全球產業規模、佔有率、趨勢、機會和預測,按作物類型、形式、應用方式、技術、地區和競爭細分,2020-2030 年中國特種肥料市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)