|

市場調查報告書

商品編碼

1687148

鈮:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Niobium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

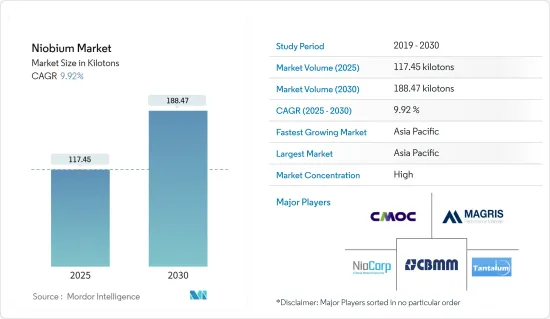

鈮市場規模預計在 2025 年為 117.45 千噸,預計在 2030 年達到 188.47 千噸,預測期內(2025-2030 年)的複合年成長率為 9.92%。

2020 年,COVID-19 疫情對市場產生了負面影響。這是因為製造設施和工廠因封鎖而關閉。供應鏈和運輸中斷進一步擾亂了市場。不過,2021年,產業復甦,市場需求回歸。

主要亮點

- 從中期來看,結構鋼的加速使用和對更輕、更省油的汽車的需求不斷成長正在推動市場成長。

- 然而,有限的供應來源和對急性暴露導致的健康問題的擔憂預計會阻礙市場的成長。

- 然而,鈮在下一代鋰離子電池中的良好應用,加上創新技術和礦山設計,預計將在預測期內提供大量機會。

- 亞太地區佔市場主導地位,其中消費量最高的國家是中國和日本。

鈮市場趨勢

建設產業佔據市場主導地位

- 建築業是全球最大的鈮消費產業。在建設產業中,高強度細合金鈮板產品用於橋樑、高架橋和高層建築的建造。重型機械和壓力容器也用於精細合金板。結構材料廣泛應用於土木工程和建築、輸電塔等,在這些領域鈮與釩形成競爭。

- 同樣地,鋼筋也用於大型水泥建築物中以增加其抵抗張伸載荷的能力。透過添加鈮和釩,可以生產出直徑更大、強度更高的鋼材,但一些較新的鋼廠正在使用水淬技術,因此無需進行細合金化。

- 目前,建設產業正在推動對高強度低合金 (HSLA) 鋼的需求,這使得更輕的建築物能夠降低成本並防止基礎設施故障。

- 近年來,建築業獲得了大量投資。根據牛津經濟研究院預測,2020年至2030年間,全球建築業規模將成長4.5兆美元(42%),達到15.2兆美元。此外,預計2020年至2030年間,中國、印度、美國和印尼將佔全球建設業成長的58.3%。

- 人口成長、從家鄉向服務業中心的遷移以及核心家庭的趨勢是推動世界各地住宅建設的一些因素。主要經濟體快速遷移到都市區、政府在房地產市場住宅方面的支出增加、以及對豪華住宅的需求不斷成長等因素都可能有利於所研究市場的成長。

- 此外,建築業是印度經濟成長的重要支柱。印度政府正在積極推動住宅建設,目標是為約13億人提供住宅。

- 投資 3000 萬美元的 Arkade Aspire 住宅綜合體計劃將在印度孟買建造一個面積為 35,366平方公尺的住宅綜合體,其中包含兩棟 18 層的住宅樓。預計建設將於2022年第二季開始,並於2025年第一季完工。在北美,美國在建設產業佔有重要佔有率。除美國外,加拿大和墨西哥對建築業的投資也貢獻巨大。

- 根據美國人口普查局的數據,2022 年 12 月美國新建設產值為 17,929 億美元。 2023年3月,非住宅部門價值為9,971.4億美元,年增18.8%。

- 此外,加拿大政府的各種計劃,如經濟適用住房舉措(AHI)、新建築加拿大計劃(NBCP)和加拿大製造將支持該行業的擴張。 2022年8月,加拿大政府宣布將在三項關鍵舉措上投資超過20億美元:三項舉措將支持在全國範圍內開發約17,000套家庭住宅,其中包括數千套經濟適用住宅。

- 此外,由於歐盟復甦基金的新投資,歐洲建築業在 2022 年成長了 2.5%。儘管大多數歐盟建設公司面臨價格壓力,但預計景氣將在 2022 年初回升並達到新冠疫情之前的水平。此外,隨著新冠疫情危機消退,建築商對投資新公司大樓和維修現有房產的積極性降低,非住宅建築預計也將增加。預計非住宅建築將加速發展,以支撐整體建築市場的成長。 2022年主要建築計劃為非住宅建築(辦公室、醫院、飯店、學校和工業建築),佔總數的31.3%。

- 因此,全球建築業的強勁成長可能會在預測期內推動鈮的消費需求。

亞太地區佔市場主導地位

- 亞太地區佔據全球市場主導地位。由於鈮在結構鋼中的應用加速,以及在中國、印度和日本等國的汽車和航太工業中的應用增加,該地區的鈮消費量正在成長。

- 在一些新興國家(例如中國和印度)的鋼鐵製造和建築業中,鈮的消費量以鈮鐵的形式顯著增加。例如,根據世界鋼鐵協會的數據,中國 2023 年 4 月鋼鐵產量估計為 9,260 萬噸,2023 年 1 月至 4 月總產量為 3.544 億噸,比 2022 年同期增加 4.1%。

- 此外,中國鋼鐵協會表示,隨著國家疫情應對力道放緩和經濟復甦力道加大,作為經濟風向標的中國鋼鐵業需求增加,該產業也因此受到提振。此外,受房地產市場穩定以及汽車、航運和建築等其他鋼鐵消費產業復甦的推動,鋼鐵業在 2023 年也將呈現上升趨勢。反過來,預計這將對市場產生積極影響。

- 中國是最大的乘用車生產國之一,背後還有其他因素推動了該國乘用車市場產量的成長,包括物流和供應鏈的改善、商業活動的活性化以及促進該國消費的政策。這增加了該國乘用車市場對鈮市場的需求。例如,根據OICA的預測,2022年中國乘用車產量將達23,836,083輛,較2021年成長11%。

- 此外,該國的汽車產業正在經歷趨勢的轉變,消費者越來越傾向於電池驅動的汽車。此外,中國政府預測,到 2025 年,電動車產量將達到 20%。這反映在該國的電動車銷售趨勢上,2022 年電動車銷售將創下歷史新高。

- 基礎建設部門是印度經濟的重要支柱。該國政府正在採取各種舉措,確保及時發展良好的基礎設施。政府重點關注鐵路、公路建設、住宅、城市發展和機場建設。

- 印度的住宅產業正在崛起,政府的支持和舉措進一步刺激了需求。據印度品牌股權基金會(IBEF)稱,住房與城市發展部(MoHUA)在其 2022-2023 年預算中撥款 98.5 億美元用於資助住宅建設和停滯計劃的完成。

- 印尼還計劃在第二季開始建造價值 27 億美元的公寓,以供數千名公務員遷往婆羅洲島的新首都。此外,印尼政府希望該計畫的80%資金來自外國投資。預計住宅建設將推動該國鈮消費市場需求增加。

- 日本是世界第三大粗鋼生產國,也是鈮市場的主要終端用戶。受全球經濟放緩影響,汽車製造業復甦緩慢、出口需求低迷,日本2022年粗鋼產量與前一年同期比較下降約7.4%。日本鋼鐵聯合會的資料顯示,2022年日本粗鋼產量將達8,920萬噸,而2021年為9,630萬噸。

- 考慮到上述因素,預測期內亞太地區鈮市場預計將穩定上升。

鈮行業概況

鈮市場趨於整合。該市場的主要企業(不分先後順序)包括 CBMM、洛陽鉬業、Magris Performance Materials、NioCorp Development Ltd、長沙南方鉭鈮等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 加速結構鋼的使用

- 對輕型、省油車的需求不斷增加

- 限制因素

- 供應來源有限

- 擔心急性暴露導致的健康問題

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 技術簡介/生產分析

- 價格趨勢

第5章 市場區隔

- 生產

- 碳酸鹽岩及碳酸鹽岩相關

- 鈮鐵礦-鉭鐵礦

- 類型

- 鈮鐵

- 氧化鈮

- 鈮金屬

- 真空級鈮合金

- 應用

- 鋼

- 高溫合金

- 超導磁鐵和電容器

- 電池

- 其他用途

- 最終用戶產業

- 建造

- 汽車和造船

- 航太和國防

- 石油和天然氣

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 俄羅斯

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Admat Inc.

- Australian Strategic Materials Ltd

- CBMM

- Changsha South Tantalum Niobium Co.,Ltd

- CMOC

- Grandview Materials

- Magris Performance Materials

- NioCorp Development Ltd.

- Titanex GmbH

第7章 市場機會與未來趨勢

- 鈮在下一代鋰離子電池中的預期用途

- 創新技術與礦山設計

The Niobium Market size is estimated at 117.45 kilotons in 2025, and is expected to reach 188.47 kilotons by 2030, at a CAGR of 9.92% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market in 2020. This was because of the shutdown of the manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the medium term, accelerating usage of structural steel and increasing demand for lighter-weight and more fuel-efficient vehicles are some of the factors driving the growth of the market studied.

- On the flip side, limited supply sources and concerns about health issues on acute exposure is expected to hinder the growth of the market.

- However, the expected usage of niobium in next-generation lithium-ion batteries and innovative techniques and mine design are anticipated to provide numerous opportunities over the forecast period.

- Asia-Pacific dominated the market with the largest consumption from countries, such as China and Japan.

Niobium Market Trends

Construction Sector to Dominate the Market

- The construction industry is the largest consumer of niobium across the world. In the construction industry, high-strength niobium micro-alloyed plate products are used to construct bridges, viaducts, high-rise buildings, etc. Heavy machinery, pressure vessels, etc., represent additional applications of micro-alloyed plates. Structural sections are widely used in civil construction, transmission towers, etc., where niobium competes with vanadium.

- Similarly, steel reinforcing bar is used in large concrete structures to increase their resistance to tensile loads. Larger diameter, high-strength grades are produced via the addition of niobium and vanadium, although some modern steel mills also use water cooling, which negates the need for microalloying.

- Furthermore, niobium has also found application in high-strength and wear-resistant rails for railway tracks operating under high axle loads.The building and construction industry is currently driving the demand for High Strength Low Alloys (HSLA) steel, which provides cost savings through weight reduction in buildings and prevents infrastructure failures.

- The construction sector has witnessed major investments in recent years. According to Oxford Economics, the global construction industry is expected to grow by USD 4.5 trillion, or 42%, between 2020 and 2030 to reach USD 15.2 trillion. Also, China, India, the United States, and Indonesia are expected to account for 58.3% of global growth in construction between 2020 and 2030.

- Growth in population, migration from hometowns to service sector clusters, and the growing trend of nuclear families are some of the factors which have been driving residential construction across the world. Factors such as rapid urban migration in major economies, increased government spending in the real estate market for residential construction, along with the growing demand for high-class residential homes are likely to benefit the growth of the market studied.

- Moreover, the construction sector is an important pillar for the growth of the Indian economy. The Indian government has been actively boosting housing construction, aiming to provide houses to about 1.3 billion people.

- The USD 30 million Arkade Aspire Residential Complex project entails the construction of a 35,366 sq. m. residential complex with two 18-story residential towers in Mumbai, India. Construction began in Q2 2022 and is expected to be completed in Q1 2025. In North America, the United States has a major share in the construction industry. Besides the United States, Canada and Mexico contribute significantly to the investments in the construction sector.

- According to the U.S. Census Bureau, the value of new construction output in the United States amounted to USD 1,792.9 billion in December 2022. The non-residential sector accounted for USD 997.14 billion in March 2023, registering a growth of 18.8% compared to the same period the previous year.

- Furthermore, in Canada, various government projects, including the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada, are set to support the sector's expansion. In August 2022, the Canadian government announced a significant investment of more than USD 2 billion to fund three important initiatives that may collectively help develop approximately 17,000 houses for families across the nation, including thousands of affordable housing units.

- Additionally, the European construction sector grew by 2.5% in 2022 due to new investments from the EU Recovery Fund. Business confidence picked up in early 2022, despite price pressures at most EU construction firms, and is expected to reach pre-COVID-19 levels. Moreover, as the crisis due to COVID-19 abates and builders become less reluctant to invest in new corporate buildings and renovate existing properties. Non-residential construction is expected to pick up the pace, thus supporting overall growth in the construction market. The major construction projects in 2022 accounted for non-residential construction (offices, hospitals, hotels, schools, and industrial buildings), accounting for 31.3% of total activity.

- Therefore, such robust growth in construction across the world is likely to boost the demand for the consumption of niobium during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific dominated the global market. With accelerating usage in structural steel and growing usage in the automobile and aerospace industry in countries such as China, India, and Japan, the consumption of niobium is increasing in the region.

- The consumption of niobium is very high in steel manufacturing in the form of ferroniobium, and the construction industry is thriving in several emerging economies, such as China and India, among others. For instance, according to the World Steel Association, China produced an estimated 92.6 million tonnes of steel in April 2023 and a total of 354.4 million tonnes from January to April 2023, a 4.1% increase compared to the same period in 2022.

- Moreover, according to the China Iron and Steel Association, the economy's benchmark China's steel industry was buoyed by increased demand after the country's declining response to the pandemic and efforts to support the economy. In addition, the steel sector is on an upward trend in 2023, supported by a stable real estate market and a recovery in other steel-consuming industries such as automobiles, ships, and construction. This, in turn, is expected to impact the market positively.

- China is one of the largest producers of passenger cars, due to the improving logistics and supply chains, increased business activity, and the country's raft of pro-consumption measures, among other factors contributing to the passenger car market products in the country. Therefore, this has increased demand for niobium market from the country's passenger car segment. For instance, according to OICA, in 2022, the passenger car production in China amounted to 2,38,36,083 units, which showed an increase of 11% compared to 2021.

- Further, the automobile industry in the country is witnessing switching trends as the consumer inclination toward battery-operated vehicles is on the higher side. Moreover, the government of China estimates a 20% penetration rate of electric vehicle production by 2025. This is reflected in the electric vehicle sales trend in the country, which went record-breaking high in 2022.

- The infrastructure sector is an important pillar of the Indian economy. The government is taking various initiatives to ensure the timely creation of excellent infrastructure in the country. The government is focusing on railways, road development, housing, urban development, and airport development.

- The residential sector in India is on an increasing trend, with government support and initiatives further boosting the demand. According to the India Brand Equity Foundation (IBEF), the Ministry of Housing and Urban Development (MoHUA) allocated USD 9.85 billion in the 2022-2023 budget to construct houses and create funds to complete the halted projects.

- Furthermore, Indonesia expects to begin construction in the second quarter on apartments worth USD 2.7 billion for thousands of civil servants due to move to its new capital city on Borneo island. Moreover, tndonesian government intends to finance it for 80% through foreign investments. Therefore, this is expected to create an upside demand for the consumption for niobium market from the contry's residential construction.

- Japan is the third-biggest producer of crude steel worldwide, which is a major end-user for the Niobium Market. The crude steel output in Japan fell by around 7.4% in 2022 from the previous year owing to a slow recovery in automobile manufacturing and weaker export demand amid a slowdown in the global economy. As per the data of the Japan Iron and Steel Federation, the crude steel production in the country reached 89.2 million tons in 2022, as compared to 96.3 million tons in 2021.

- Considering the aforementioned factors, the Asia-Pacific niobium market is anticipated to rise steadily over the forecast period.

Niobium Industry Overview

The Niobium Market is consolidated in nature. The major players in this market (not in any particular order) include CBMM, CMOC, Magris Performance Materials, NioCorp Development Ltd, and Changsha South Tantalum Niobium Co.,Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Accelerating Usage in Structural Steel

- 4.1.2 Growing Demand for Lighter-Weight and More Fuel-Efficient Vehicles

- 4.2 Restraints

- 4.2.1 Limited Supply Sources

- 4.2.2 Concerns About Health Issues on Acute Exposure

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Technological Snapshot/ Production Analysis

- 4.6 Price Trends

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Occurrence

- 5.1.1 Carbonatites and Associates

- 5.1.2 Columbite-Tantalite

- 5.2 Type

- 5.2.1 Ferroniobium

- 5.2.2 Niobium Oxide

- 5.2.3 Niobium Metal

- 5.2.4 Vacuum-Grade Niobium Alloys

- 5.3 Application

- 5.3.1 Steel

- 5.3.2 Super Alloys

- 5.3.3 Superconducting Magnets and Capacitors

- 5.3.4 Batteries

- 5.3.5 Other Applications

- 5.4 End-user Industry

- 5.4.1 Construction

- 5.4.2 Automotive and Shipbuilding

- 5.4.3 Aerospace and Defense

- 5.4.4 Oil and Gas

- 5.4.5 Other End-user Industries

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Russia

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Admat Inc.

- 6.4.2 Australian Strategic Materials Ltd

- 6.4.3 CBMM

- 6.4.4 Changsha South Tantalum Niobium Co.,Ltd

- 6.4.5 CMOC

- 6.4.6 Grandview Materials

- 6.4.7 Magris Performance Materials

- 6.4.8 NioCorp Development Ltd.

- 6.4.9 Titanex GmbH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expected Usage of Niobium in Next-Generation Lithium Ion Battery

- 7.2 Innovative Techniques and Mine Designing

五氧化二鈮市場依應用、終端用戶產業、等級、製造流程、形狀及粒徑分類-2025-2032年預測

五氧化二鈮市場依應用、終端用戶產業、等級、製造流程、形狀及粒徑分類-2025-2032年預測 五氧化二鈮市場規模、佔有率及成長分析(按等級、應用和地區)-產業預測,2025-2032

五氧化二鈮市場規模、佔有率及成長分析(按等級、應用和地區)-產業預測,2025-2032 全球五氧化二鈮市場

全球五氧化二鈮市場 2032 年鈮市場預測:按類型、純度等級、通路、應用、最終用戶和地區進行的全球分析

2032 年鈮市場預測:按類型、純度等級、通路、應用、最終用戶和地區進行的全球分析 五氧化二鈮-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

五氧化二鈮-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 全球五氧化二鈮市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球五氧化二鈮市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 全球鈮市場規模研究,按類型(鈮鐵、鈮氧化物、鈮金屬)、按應用(結構鋼、汽車鋼、管道鋼、不銹鋼等)和區域預測 2022-2032

全球鈮市場規模研究,按類型(鈮鐵、鈮氧化物、鈮金屬)、按應用(結構鋼、汽車鋼、管道鋼、不銹鋼等)和區域預測 2022-2032 五氧化二鈮市場- 按等級(3N、4N)按應用(鈮金屬、光學玻璃、合金製造、金屬提取、電容器)、按最終用途行業(催化、儲能、陶瓷和玻璃)和預測,2024 - 2032 年

五氧化二鈮市場- 按等級(3N、4N)按應用(鈮金屬、光學玻璃、合金製造、金屬提取、電容器)、按最終用途行業(催化、儲能、陶瓷和玻璃)和預測,2024 - 2032 年 鈮全球市場2024-2028

鈮全球市場2024-2028