|

市場調查報告書

商品編碼

1690944

靈活燃料汽車:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Flex-fuel Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

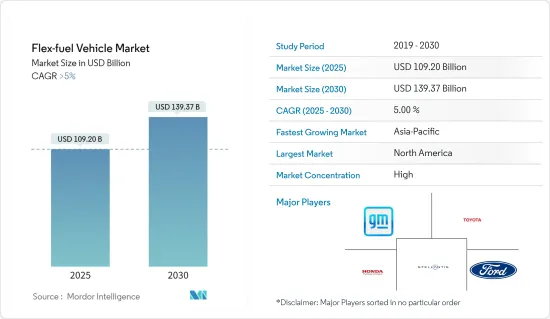

預計 2025 年靈活燃料汽車市場規模為 1,092 億美元,到 2030 年將達到 1,393.7 億美元,預測期內(2025-2030 年)的複合年成長率將超過 5%。

靈活燃料汽車(FFV)市場受到的影響不如其他汽車產業嚴重。然而,由於市場上 FFV 選項有限以及政府限制,銷量略有下降。然而,隨著情況緩和、生活恢復正常,預計 FFV 市場將在預測期內成長。

道路上的大多數汽車都使用傳統石化燃料,導致有害廢氣排放增加。為了遏止汽車污染,一些地方政府已經推出了針對內燃機汽車的排放法規。這些規定為使用靈活燃料的汽車的研究開闢了更大的空間。

市場上有許多不同類別和類型的 FFV,從 E10 到 E85 及以上。測試表明,使用 E85 燃料的 FFV 可使 NOx 減少 23%,CO 減少 30%,CO2 減少 4-6%。由於多種因素,包括廢氣排放的減少、國內乙醇燃料的生產能力以及對天然石化燃料使用的限制,預計預測期內對 FFV 的需求將會增加。

美國和拉丁美洲對靈活燃料汽車的需求正在強勁成長。據估計,全球超過84%的乙醇產自美國和巴西。

彈性燃料汽車市場趨勢

更嚴格的排放法規的批准推動柴油燃料類型的細分市場

- 所有使用石化燃料的車輛排放的廢氣都在增加,污染空氣。空氣品質差導致嚴重呼吸系統疾病增加。在歐洲,機動車造成的空氣污染佔總污染量的30%以上,包括NOx、VOC、PM2.5、PM10等。

- 為了規範汽車廢氣排放,各國汽車管理部門都禁止汽車排氣管排放氮氧化物、硫氧化物等溫室氣體和其他有害污染物。

- 例如,在歐洲,廢氣法規每年都變得越來越嚴格。根據監管機構歐洲環境署(EEA)介紹,2005年實施的歐4標準將氮氧化物標準設定為0.08g/km,但2009年該標準下調至0.06g/km,此後輕型乘用車的氮氧化物標準保持不變。

- 同樣,2015年,標準乘用車的二氧化碳排放量不得超過130克/公里。 2020年,該標準修訂為95G/km。歐盟委員會也計劃在2025年將這一數字降至70克/公里。

- 減少廢氣產生的溫室氣體可能會對長期健康產生重大影響。此外,由於靈活燃料比傳統柴油更清潔,預計未來幾年靈活燃料市場的需求將會增加。

亞太地區成長強勁

- 目前,亞太地區超過70%的國家依賴進口石化燃料來驅動其汽車。原油成本及其精製成本大幅增加了消費者的燃料成本。由於印度和中國等新興市場,亞太地區預計將顯著成長。

- 例如,在印度,公路運輸和公路部(MoRTH)為在該國引入乙醇燃料設定了各種期限,以抑制石化燃料消耗並降低燃料成本。此外,印度佔全球彈性燃料產量的2%,不足以滿足該國的需求。因此,未來幾年國內乙醇產量的目標是從 7,000 萬公升增加到 1.5 億公升。

- 運輸部計劃逐步擴大乙醇燃料的使用。 E10 計劃於 2022 年 4 月投產,E20 計劃於 2025 年開始生產。國內汽車製造商也被要求從 2023 年 4 月起擴大對 E10 車型的研究,從 2025 年 4 月起擴大對 E20 車型的研究。

- 由於可以使用甘蔗等可再生原料在國內生產彈性燃料,因此乙醇混合燃料減少了進口原料燃料的數量,並有助於降低最終用戶的燃料成本。

- 隨著乙醇基靈活燃料的普及,作為世界第二人口大國的印度,對彈性燃料汽車的需求可能會大幅增加。

靈活燃料汽車產業概況

靈活燃料汽車市場由各種參與企業組成,形成一個整合的市場。憑藉著種類繁多的靈活燃料產品和不斷尋找替代燃料的努力,市場前五名主要企業佔據了相當大的市場佔有率。例如,通用汽車有大約 13 種車型,福特馬達有 11 種,而 Stallintis NV 有 7 種車型使用乙醇混合。

排名前五的公司包括通用汽車、福特馬達、豐田汽車公司、Stellantis NV、工業和現代汽車公司。其他參與企業包括日產汽車、斯巴魯公司和大眾汽車公司。

2023 年 8 月,印度聯邦部長推出了世界上第一輛電動彈性燃料汽車,即 BS-VI(Stage-II),以推廣替代燃料的使用。這款卓越的汽車旨在使用多種燃料,包括氫氣、靈活燃料和生質燃料,減少對傳統燃料來源的依賴。

此外,豐田還將推出一款令人驚嘆的新款Innova,這是第一款以 100% 乙醇驅動的汽車。這款創新汽車還具有成為全球首款符合 BS-VI(第二階段)標準的電動靈活燃料汽車的市場機會。更重要的是,它產生的電力增加了驚人的40%,大大降低了乙醇的實際價格。

這些開創性的舉措是朝著更清潔、更永續的未來邁出的一步,標誌著更清潔能源選擇的轉變。很高興看到在優先考慮環境友善性和努力減少碳排放方面取得如此進展。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 批准嚴格的排放法規

- 市場限制

- 電動車銷量成長可能會阻礙市場成長

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 乙醇混合型

- E10 至 E25

- E25至E85

- E85以上

- 汽車模型

- 搭乘用車

- 商用車

- 燃料類型

- 汽油

- 柴油引擎

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 西班牙

- 英國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 韓國

- 日本

- 其他亞太地區

- 其他

- 南美洲

- 中東和非洲

- 北美洲

第6章競爭格局

- 供應商市場佔有率

- 公司簡介

- General Motors

- Toyota Motor Corporation

- Honda Motor Company

- Stellantis NV

- Ford Motor Company

- Hyundai Motor Company

- Nissan Motor Company

- Subaru Corporation

- Volkswagen AG

- BMW AG

- Volvo Car Corporation

第7章 市場機會與未來趨勢

The Flex-fuel Vehicle Market size is estimated at USD 109.20 billion in 2025, and is expected to reach USD 139.37 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The market for flex-fuel vehicles (FFV) was not impacted by the COVID-19 pandemic as severely as other automotive industries. However, with limited options for an FFV in the market, it did witness a slight decline in sales, considering the restrictions imposed by the respective governments. However, with the situation easing and life returning to normalcy, the FFV market is anticipated to grow during the projected period.

Most of the vehicles running are fueled using conventional fossil fuels, which has led to an increase in toxic exhaust gas emissions. To control vehicular pollution, multiple county governments have put forth several emission restrictions for IC (internal combustion) engine-powered vehicles. These restrictions have opened the scope for research on vehicles running on flex fuels.

In the market, there are various categories and types of FFV from E10 to E85 and above. According to the tests conducted, FFVs running on E85 fuel produce 23% less NOx, 30% less CO, and 4-6% lower CO2. Due to numerous factors, including reduced tailpipe emissions, domestic production capabilities of ethanol-based fuels, and limiting the use of naturally occurring fossil fuels, the demand for FFVs is expected to increase during the forecast period.

The demand for flex-fuel vehicles is growing significantly in the United States and the Latin American region. It is estimated that more than 84% of the world's ethanol is produced by the United States and Brazil.

Flex-fuel Vehicle Market Trends

Ratification of Stringent Exhaust Emission Regulations will Diesel Fuel Type Segment

- The increase in vehicle exhaust emissions from all types of vehicles using fossil fuels has contaminated the atmosphere. The poor air quality has led to an increase in a plethora of serious respiratory diseases. In Europe, vehicular pollution contributes to over 30% of total air pollution, including NOx, VOCs, PM2.5, PM10, and others.

- To bring exhaust emissions under control, country-specific vehicle authorities have barricaded the production of greenhouse gasses like NOx, SOx, and other harmful pollutants from vehicle tailpipes.

- For instance, in Europe, exhaust emission norms have become even more strict over the years. According to the regulatory authority European Environmental Agency (EEA), in Euro 4, launched in 2005, the NOx standards were affixed at 0.08g/km, whereas in 2009, it got reduced to 0.06g/km, and it has remained the same for light passenger cars since.

- Similarly, for CO2 emissions in 2015, standard passenger cars were not allowed to exceed 130g/km of CO2. In 2020, it was revised to 95g/km. The European Commission also targets to reduce this number to 70g/km by 2025.

- The reduced amount of greenhouse gases from the exhaust will have a significant impact on health in the long run. Alongside, this will also allow the flex-fuel market to witness an increase in demand in the upcoming years as it is a clean-burning fuel as compared to conventional diesel.

Asia-Pacific to Witness Significant Growth

- More than 70% of the countries in the Asia-Pacific region currently rely upon the import of fossil fuels to run vehicles. The cost of crude oil and its refinement significantly increases the consumer cost of fuel. With emerging markets like India and China, the Asia-Pacific region is expected to witness significant growth.

- For instance, in India, to curb the consumption of fossil fuels and tone down fuel costs, MoRTH (Ministry of Road Transport and Highways) has put forward various deadlines to introduce ethanol-based fuel in the country. Additionally, India accounts for 2% of the global flex-fuel production, which is not enough to fulfill the country's requirements. Hence, the domestic production of ethanol is targeted to rise from 70 to 150 million liters in the next few years.

- The transport ministry is planning to roll out the use of ethanol-based fuel in phases. E10 production is expected to be in motion from April 2022 and E20 from 2025. Various vehicle manufacturers in the country have also been notified to scale up the research to run vehicles on E10 from April 2023 and E20 from April 2025.

- As flex fuels can be manufactured domestically using renewable materials like sugar cane, the ethanol-blended fuel will reduce the quantity of raw fuel imported, helping reduce the fuel cost for end users.

- With the increase in the availability of ethanol-based flex-fuel, the demand for flex-fuel vehicles may witness significant growth as India is the world's second-most populated country.

Flex-fuel Vehicle Industry Overview

The flex-fuel vehicle market constitutes various players accounting for a consolidated market. Owing to a wide range of products running on flex fuels and constant developments to find an alternative fuel, the top five players in the market account for a significant market share. For instance, General Motors has about 13 vehicle models, Ford Motor Co. has 11 vehicle models, and Stallintis NV has seven vehicle models running on ethanol blend fuel.

The top five players include General Motors, Ford Motor Co., Toyota Motor Corp., Stellantis NV, Honda Motor Co., and Hyundai Motor Co. Other players include Nissan Motor Company, Subaru Corporation, and Volkswagen AG.

In August 2023, the Union Minister of India has introduced the world's first electric flex-fuel vehicle, known as BS-VI (Stage-II), in an effort to promote the use of alternative fuels. This remarkable car runs on a variety of fuels such as hydrogen, flex-fuel, and biofuel, aiming to reduce our reliance on traditional fuel sources.

Adding to the mix, Toyota is all set to launch an incredible new variant of the Innova, the first of its kind to be powered entirely by 100% ethanol. This innovative car also holds the title of being the world's first electrified flex-fuel vehicle under the BS-VI (Stage-II) standards. Additionally, it generates a remarkable 40% electric power, significantly lowering the effective price of ethanol.

These ground-breaking initiatives are a step towards a greener and more sustainable future, showcasing the shift towards cleaner energy options. It's great to see such advancements that prioritize environmental well-being and strive for a decrease in our carbon footprint.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Ratification of Stringent Exhaust Emission Regulations

- 4.2 Market Restraints

- 4.2.1 Increase Sales of Electric Vehicle May Restraint the Growth of the Market

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products and Services

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Ethanol Blend Type

- 5.1.1 E10 to E25

- 5.1.2 E25 to E85

- 5.1.3 E85 and Above

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Fuel Type

- 5.3.1 Petrol

- 5.3.2 Diesel

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 Spain

- 5.4.2.4 United Kingdom

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 South Korea

- 5.4.3.4 Japan

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 General Motors

- 6.2.2 Toyota Motor Corporation

- 6.2.3 Honda Motor Company

- 6.2.4 Stellantis NV

- 6.2.5 Ford Motor Company

- 6.2.6 Hyundai Motor Company

- 6.2.7 Nissan Motor Company

- 6.2.8 Subaru Corporation

- 6.2.9 Volkswagen AG

- 6.2.10 BMW AG

- 6.2.11 Volvo Car Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

靈活燃料汽車:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

靈活燃料汽車:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 靈活燃料引擎市場(按燃料類型、混合類型、引擎容量、車輛類型、應用、最終用戶和銷售管道)——2025-2032 年全球預測

靈活燃料引擎市場(按燃料類型、混合類型、引擎容量、車輛類型、應用、最終用戶和銷售管道)——2025-2032 年全球預測 全球彈性燃料市場

全球彈性燃料市場 靈活燃料引擎市場,按組件類型、燃料類型、技術、應用、國家和地區分類 - 2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測

靈活燃料引擎市場,按組件類型、燃料類型、技術、應用、國家和地區分類 - 2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測 全球靈活燃料汽車市場按燃料類型、車輛類型、引擎容量和地區分類全球彈性燃料市場依燃料結構、應用、原料來源、燃料種類及地區分類靈活燃料引擎市場,按類型、車輛類型、混合類型、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

全球靈活燃料汽車市場按燃料類型、車輛類型、引擎容量和地區分類全球彈性燃料市場依燃料結構、應用、原料來源、燃料種類及地區分類靈活燃料引擎市場,按類型、車輛類型、混合類型、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測