|

市場調查報告書

商品編碼

1690781

美國資料中心建置:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)United States (US) Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

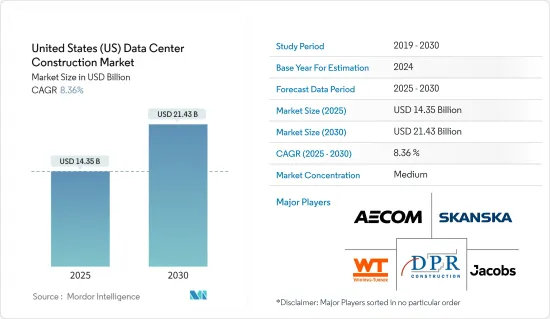

美國資料中心建設市場規模預計在2025年為143.5億美元,預計到2030年將達到214.3億美元,預測期內(2025-2030年)的複合年成長率為8.36%。

關鍵亮點

- 美國市場最為成熟,在成長和營運方面均呈現穩定成長。美國資料中心建設市場的成長歸因於物聯網的日益普及、5G網路的市場開放以及企業對雲端基礎的服務的採用。各行各業數位化的採用將促進主機託管、雲端、網際網路和通訊提供商增加資料中心投資,以及對線上娛樂內容高速串流媒體的需求。

- 由於機架功率密度的提高、與其他國家連接性的改善、資料中心微電網的安裝、5G 連接、邊緣資料中心技術以及新的 UPS 電池技術,該國的資料中心市場預計將成長。

- 美國政府正在透過一系列措施鼓勵資料中心投資,包括確保開發土地、降低電費、鼓勵購買可再生能源等。

- 例如,亞利桑那州為在其對外貿易區開展業務的公司提供各種激勵措施。貿易區內的企業可享有 72.9% 的州不動產稅和動產稅減免。這些措施可能會促進未來十年美國資料中心建設市場的成長。

- 儘管需求不斷成長,但資料中心產業在滿足高需求方面仍面臨許多挑戰。與許多其他房地產行業一樣,資料中心產業也因供應鏈中斷而面臨新建築建設延誤的問題。人事費用、建材和其他成本的增加也推高了資本支出。

- COVID-19 疫情給各行業的經濟帶來了額外壓力,也凸顯了資料中心所能提供的雲端基礎的工作環境的價值和潛力。在新冠疫情期間,53% 的美國人表示網路至關重要。這使得該國使用更多的資料中心。

美國資料中心建設市場趨勢

UPS系統引領電力基礎設施領域

- 不斷電系統(UPS) 系統對於資料中心至關重要,以確保伺服器和所有敏感運算設備不受電源線波動和電能品質問題的影響。斷電導致資料中心停機,影響資料中心效率。 UPS 系統還可以幫助在停電時自動保存寶貴的資料。平均而言,UPS 系統提供 8-10 分鐘的備用時間。

- 近期,該國惡劣天氣導致資料中心營運中斷。 2024年1月至3月,美國遭遇冰凍天氣,影響了加州和德克薩斯州電網的發電能力和運作。此次停電給該州的資料中心運作帶來了問題。使用UPS系統有助於減少因天氣變化而造成的此類損害。由於全國各地的各種企業都依賴資料中心,不斷電系統至關重要。

- 由於壽命長、體積小等多種因素,資料中心傾向採用鋰離子 UPS 系統。該國資料中心能源消耗的增加正在推動鋰離子UPS系統的採用。

- 根據勞倫斯伯克利國家實驗室的數據,超大規模資料中心通常需要每個機架 10-14kW,但對於配備資源豐富的 GPU 的支援 AI 的機架,這一數字將上升到 40-60kW。這意味著美國資料中心的總消費量將從 2022 年的 17GW 成長到 2030 年的 35GW。鋰離子 UPS 系統將徹底改變大型和小型資料中心的 UPS 系統。

- 政府也採取新措施解決資料中心的能源消耗問題,鼓勵引入模組化UPS系統。美國政府在2.3兆美元的2021年綜合撥款法案中列入了資料中心的能源效率目標和指標。該法案還要求對資料中心的能源和水消耗以及提高此類資料效率的方法進行新的研究。

- 管理資料中心的財務影響也很大,因為資料中心將其營運費用的 30% 到 50% 用於電力。根據美國美國資源保護委員會預測,到2023年,北維吉尼亞資料中心的總合電力消耗容量將達到2.6GW,位居全球第一。據Cloudscene稱,美國擁有全球最多的資料中心,數量為5,381個,而上年度為5,375個。

醫療領域將經歷顯著成長

- 透過電子健康記錄(EMR)實現醫療記錄數位化,為大量資料的產生做出了重大貢獻。醫療設備的最新技術創新和傳統操作系統的現代化(例如改進的勞動力管理和患者護理系統)正在產生大量資料,並進一步增加了對安全資料中心的需求。

- 物聯網等技術在醫療保健領域有許多應用,從遠端監控到醫療設備整合。它還可以讓患者更健康、更安全,並改善醫生的照護方式。然而,感測器、穿戴式裝置、遠端監視器和其他醫療設備正在產生大量資料。

- 遠端醫療在美國的使用日益增多,因為它具有多種優勢,包括允許任何地區的消費者聯繫他們需要的醫生。這是透過改變通常安排的諮詢來節省金錢和時間的有效方法,這反過來又會產生大量資料,突出資料中心和資料中心建設計劃的必要性。

- 根據美國衛生研究院的數據,2020 年 3 月至 2022 年 2 月期間,進行了超過 85 萬次遠端醫療,其中約 62% 透過視訊進行,約 38% 透過電話進行。根據《製藥業高管》對 398 名醫療保健專業人士的調查,即使在冠狀病毒 (COVID-19) 大流行之後,預計仍有近 20% 的患者預約將透過遠端醫療進行。

- 從技術層面來看,醫學影像和基因組研究的進步正在帶來新型更大文件尺寸的出現。這些因素正在促進醫療保健產業資料量的增加,推動預測期內該地區資料中心建設的發展。

- 此外,政府繼續認知到數位健康和技術創新在醫療保健中的作用,將其作為成功醫療保健基礎設施的重要組成部分。該國政府在推動衛生部門技術進步方面取得了長足進步,並不斷增加衛生支出以支持衛生部門的發展。例如,根據美國精算師辦公室(CMS)的資料,美國全國醫療保健支出預計將從 2021 年的 4.29 兆美元成長到 2030 年的 6.751 兆美元。

美國資料中心建設市場概況

美國資料中心建設市場半固體,主要參與者包括 AECOM、Whiting-turner Contracting Company、Jacobs Solutions Inc.、DPR Construction 和 Skanska USA。市場參與企業正在採取收購和聯盟等各種策略來豐富其產品陣容並保持市場競爭力。

- 2024年3月,瑞典著名建築開發公司Skanska宣布已在美國維吉尼亞州簽署了新契約。

- 2024 年 1 月,Google的完全子公司Design LLC 選擇了位於馬裡蘭州巴爾的摩的 Whiting Turner Contracting 公司在奧勒岡州瓦斯科縣建造一個價值 6 億美元的資料中心。擬建的這座佔地 29 萬平方英尺的工廠是俄亥俄州、愛荷華州、密蘇裡州和亞利桑那州一系列類似投資的一部分。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 市場動態

- 市場促進因素

- 雲端應用、人工智慧和巨量資料的成長

- 超大規模資料中心的採用率不斷提高

- 市場限制

- 房地產成本上漲

- 市場促進因素

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 美國主要資料中心建設統計數據

- 美國資料中心數量

- 美國在建資料中心(單位:兆瓦)

- 美國資料中心建設的平均資本支出和營運支出

- 資料中心電力吸收能力(MW)(美國選定城市)

- COVID-19 市場影響評估

第5章市場區隔

- 按基礎設施

- 電力基礎設施

- UPS系統

- 其他電力基礎設施

- 機械基礎設施

- 冷卻系統

- 架子

- 其他機械基礎設施

- 一般建築

- 電力基礎設施

- 按層級類型

- 層級和二級

- 第三層級

- IV層級

- 按最終用戶

- 銀行、金融服務和保險

- 資訊科技/通訊

- 政府和國防

- 醫療保健

- 其他

第6章 競爭格局

- 公司簡介

- AECOM

- Whiting-turner Contracting Company

- Jacobs Solutions Inc.

- DPR Construction

- Skanska USA

- Balfour Beatty US

- Hensel Phelps

- McCarthy Building Companies Inc.

- Gilbane Building Company

- Brasfield & Gorrie LLC

第7章投資分析

第8章 市場機會與未來趨勢

The United States Data Center Construction Market size is estimated at USD 14.35 billion in 2025, and is expected to reach USD 21.43 billion by 2030, at a CAGR of 8.36% during the forecast period (2025-2030).

Key Highlights

- The US market is the most mature and shows steady growth in terms of growth and operations. The growth of the US data center construction market is attributed to the increasing adoption of IoT, the development of 5G networks, and the adoption of cloud-based services by businesses. Adopting digitalization across industries would contribute to a rise in data center investments by colocation, cloud, internet, and telecommunication providers, as well as the demand for the streaming of online entertainment content at high speeds.

- The country's data center market is expected to grow owing to a rise in rack power density, connectivity improvements with other nations, the installation of microgrids in data centers, 5G connectivity, edge data center technology, and new UPS battery technologies.

- The US government is encouraging data center investments by a various means, including increasing the availability of land for development, lowering electricity tariffs, and encouraging the procurement of renewable energy.

- For example, Arizona state offers various incentives to businesses that operate in the foreign trade zone. Businesses in a trade zone are entitled to a 72.9% exemption in state real and personal property taxes. Consequently, such initiatives would contribute to the growth of the data center construction market in the United States over the next decade.

- Despite the escalating demand, the data center industry is found to be prone to some challenges when it comes to satisfying high demand. The data center industry faces new construction delays due to supply chain disruptions, as in many other real estate verticals. Increasing labor, building materials, and other costs have also boosted capital expenditures.

- The COVID-19 pandemic placed additional pressure on the overall economy across sectors and highlighted the value and potential of the cloud-based work environment provided by data centers. During the COVID-19 pandemic, 53% of Americans said that the internet had been vital. This has increased the use of more data centers in the country.

United States (US) Data Center Construction Market Trends

UPS Systems to Lead the Electrical Infrastructure Segment

- An uninterruptible power supply (UPS) system is imperative for data centers to ensure that servers and all sensitive computing equipment are never susceptible to power line fluctuations and power quality issues. Any power failure can result in data center downtime, affecting the data center's efficiency. UPS systems also assist in saving valuable data automatically during a power outage. On average, a UPS system offers backup for 8-10 minutes.

- Lately, the unfavorable weather conditions in the country have caused interruptions in data center operations. From January 2024 to March 2024, the country was hit by freezing weather, which affected the grid generation capacity and operating frequency of California and Texas. The disruption in the power supply led to issues with the state's operation of data centers. The adoption of UPS systems results in mitigating such damages by weather changes. Various companies nationwide rely on data centers, which makes an uninterrupted power source crucial.

- There is a trend in adopting lithium-ion UPS systems in data centers due to several factors, such as longer life, small form factor, etc. The increasing consumption of energy by data centers in the country has been promoting the adoption of lithium-ion UPS systems.

- As per the Lawrence Berkeley National Laboratory, while the hyperscalers typically need 10-14 kW per rack in existing data centers, this is likely to rise to 40-60 kW for AI-ready racks equipped with resource-equipped GPUs. This means that overall consumption of data centers across the United States is expected to reach 35 GW by 2030, up from 17 GW in 2022. Lithium-ion UPS systems are set to revolutionize UPS systems for large and micro data centers.

- The government has also been taking new initiatives toward energy consumption by data centers, triggering modular UPS systems. In the USD 2.3 trillion-backed Consolidated Appropriations Act 2021, the US government included data center energy efficiency targets and metrics. The act calls for a new study on energy and water consumption by data center use and ways to improve the efficiency of such data centers.

- The financial impact for data center management is also huge as a data center spends between 30% and 50% of its operational expenditure on electricity. According to the United States National Resources Defense Council, the combined electricity consumption capacity of data centers in Northern Virginia, United States, amounted to 2.6 GW in 2023, the highest globally. According to Cloudscene, the United States also has the largest number of data centers globally with 5381 currently ccompared to 5375 data centers in the previous year.

Healthcare Sector to Witness Major Growth

- Digitization of consumer health records in the form of electronic medical records (EMR) has significantly contributed to massive data generation. The latest innovations in the medical equipment and the modernization of legacy operating systems, such as management of personnel and improvement in patient response systems, generate multitude of data, further boosting the demand for secured data centers.

- Technologies like IoT have a lot of applications in healthcare, from remote monitoring to medical device integration. It has also potential to keep patients healthy and safe and improve how physicians deliver care. However, a massive amount of data is being produced by sensors, wearables, remote monitors, and other medical devices.

- Telemedicine is increasing in usage in the United States, owing to various advantages, such as consumers from any region being able to gain access to required doctors. It is an efficient method, as both money and time are being saved due to the change in typically scheduled visits, thereby generating a lot of data and thus emphasizing the need for data centers and data center construction initiatives.

- As per the National Institutes of Health, between March 2020 and February 2022, more than 850,000 telemedicine visits occurred, with approximately 62% of visits by video and 38% by telephone. Besides, according to a survey of 398 healthcare professionals conducted by the Pharmaceutical Executive magazine, it has been predicted that after the coronavirus (COVID-19) pandemic, almost 20% of patient appointments will still be conducted via telemedicine compared to 2% beforehand and 61% perhaps during the pandemic.

- At the technical level, advances in medical imaging and genomic research are introducing new types of file types that are larger in size. These factors contribute to the increasing amount of data in the healthcare industry, which boosts the data center construction developments in the region during the forecast period.

- Moreover, the government of the country continuously recognizes the role of digital health and technological innovation in healthcare as an integral part of successful healthcare infrastructure. The government is making significant strides to make the healthcare sector technologically advanced and continuously increasing its healthcare expenditure to support the healthcare sector. For instance, according to the data from CMS (Office of the Actuary), the forecasted U.S. national health expenditure was expected to reach USD 6.751 trillion in 2030 from USD 4.29 trillion in 2021.

United States (US) Data Center Construction Market Overview

The US data center construction market is semi-consolidated with the presence of major players like AECOM, Whiting-turner Contracting Company, Jacobs Solutions Inc., DPR Construction, and Skanska USA. The market players are adopting various strategies, including acquisitions and partnerships to enhance their product offerings and remain competitive in the market.

- In March 2024, Sweden-based Skanska, a prominent construction and development company, announced a new contract worth approximately USD 242 million in Virginia, the United States.

- In January 2024, Design LLC, a wholly-owned subsidiary of Google, selected Baltimore, Maryland, based Whiting-Turner Contracting Co. to build a USD 600 million data center in Wasco County, Oregon. The facility is planned for 290,000 sq. ft. and will be the latest in a string of similar investments in Ohio, Iowa, Missouri, and Arizona.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Growing Cloud Applications, AI, and Big Data

- 4.2.1.2 Rising Adoption of Hyperscale Data Centers

- 4.2.2 Market Restraints

- 4.2.2.1 Increase in Real Estate Costs

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Key United States Data Center Construction Statistics

- 4.4.1 Number of Data Centers in the United States

- 4.4.2 Data Center Under Construction in the United States, in MW

- 4.4.3 Average Capex and Opex for the United States Data Center Construction

- 4.4.4 Data Center Power Capacity Absorption, in MW, Selected Cities, United States

- 4.5 Assessment of Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Infrastructure

- 5.1.1 Electrical Infrastructure

- 5.1.1.1 UPS Systems

- 5.1.1.2 Other Electrical Infrastructure

- 5.1.2 Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.2 Racks

- 5.1.2.3 Other Mechanical Infrastructure

- 5.1.3 General Construction

- 5.1.1 Electrical Infrastructure

- 5.2 By Tier Type

- 5.2.1 Tier-I and -II

- 5.2.2 Tier-III

- 5.2.3 Tier-IV

- 5.3 By End User

- 5.3.1 Banking, Financial Services, and Insurance

- 5.3.2 IT and Telecommunications

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AECOM

- 6.1.2 Whiting-turner Contracting Company

- 6.1.3 Jacobs Solutions Inc.

- 6.1.4 DPR Construction

- 6.1.5 Skanska USA

- 6.1.6 Balfour Beatty US

- 6.1.7 Hensel Phelps

- 6.1.8 McCarthy Building Companies Inc.

- 6.1.9 Gilbane Building Company

- 6.1.10 Brasfield & Gorrie LLC

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

資料中心建置市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、材料類型、部署模式、最終用戶、設備

資料中心建置市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、材料類型、部署模式、最終用戶、設備 2026-2030年全球資料中心建置市場

2026-2030年全球資料中心建置市場 新加坡資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

新加坡資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 資料中心建置市場報告:按建設類型、資料中心類型、等級標準、產業垂直領域和地區分類(2026-2034 年)

資料中心建置市場報告:按建設類型、資料中心類型、等級標準、產業垂直領域和地區分類(2026-2034 年) 資料中心建置市場-全球產業規模、佔有率、趨勢、機會及預測(依基礎設施類型、層級、資料中心規模、最終用戶產業、地區及競爭格局分類,2021-2031)

資料中心建置市場-全球產業規模、佔有率、趨勢、機會及預測(依基礎設施類型、層級、資料中心規模、最終用戶產業、地區及競爭格局分類,2021-2031) 資料中心機械設備建置市場(依組件類型、液冷系統、建置類型、等級及計劃類型分類)-2026-2032年全球預測拉丁美洲資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

資料中心機械設備建置市場(依組件類型、液冷系統、建置類型、等級及計劃類型分類)-2026-2032年全球預測拉丁美洲資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 資料中心監控市場:按組件、按監控方式、按最終用戶、按地區分類日本資料中心建置市場報告(按建設類型、資料中心類型、等級標準、垂直產業和地區分類,2026-2034年)

資料中心監控市場:按組件、按監控方式、按最終用戶、按地區分類日本資料中心建置市場報告(按建設類型、資料中心類型、等級標準、垂直產業和地區分類,2026-2034年) 資料中心建置市場機會、成長要素、產業趨勢分析及2026年至2035年預測

資料中心建置市場機會、成長要素、產業趨勢分析及2026年至2035年預測