|

市場調查報告書

商品編碼

1690203

自動卸貨卡車和礦用卡車:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)Dump Trucks and Mining Trucks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

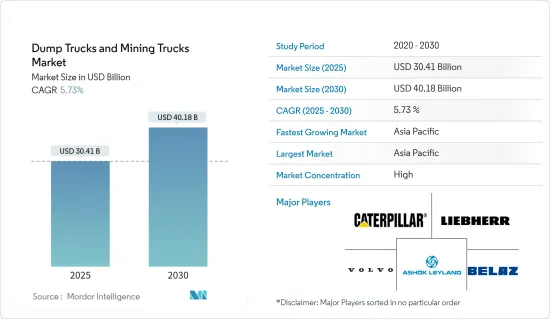

自動卸貨卡車和採礦卡車市場規模預計在 2025 年為 304.1 億美元,預計到 2030 年將達到 401.8 億美元,預測期內(2025-2030 年)的複合年成長率為 5.73%。

由於各行業和基礎設施計劃發展對礦物和礦石的需求持續增加,預計採礦活動活性化將帶動採礦卡車的需求增加。全球採礦業需要更多技術人才。此外,新冠疫情和工業停工預計將推動礦業公司提高生產效率,進而推動對更多採礦卡車的需求。此外,2021年是轉型之年,採礦活動再次進入復甦階段,展現出巨大的成長潛力。

採礦業目前面臨政府嚴格的排放和進出口管制。要提高利潤率,就需要提高生產力。這就是為什麼公司擴大透過安裝感測器和分析資料來實現採礦卡車的自動化和電氣化。隨著全球電氣化持續發展,OEM)正在提供電動動力傳動系統。此外,包括遠端資訊處理在內的技術方面也在推動需求。

預計亞太地區在採礦設備方面擁有最大的成長潛力,其中包括自卸車和採礦卡車等物料輸送設備。該地區在採礦生產和礦山方面具有巨大的潛力,增加了對自動卸貨卡車和採礦卡車的需求。由於露天採礦產量的增加、設備維護的可預測性以及露天採礦的更換週期,該地區採礦設備產量增加。

礦用自動卸貨卡車市場趨勢

預計電動卡車在預測期內將實現高成長

過去幾年,中國、印度和歐洲等自動卸貨卡車和礦用卡車的主要市場都採用了嚴格的排放氣體標準,如印度的巴拉特6標準、中國的中國6標準和歐洲的歐盟6標準。電氣化和混合動力化正變得越來越必要,特別是對於柴油引擎汽車,必須配備選擇性催化還原(SCR)和廢氣再循環(EGR)技術。這減少了柴油引擎排放的硫煙和其他含硫排放氣體的數量。這些系統在柴油引擎上的安裝,進一步提高了自動卸貨卡車等柴油車的價格。美國等許多國家也透過最近通過的《通貨膨脹削減法案》為購買電動卡車提供直接稅額扣抵,以鼓勵電動卡車的銷售。這些措施預計將加速電動卡車在採礦業的應用,因為採礦卡車佔礦山總排放的 60% 以上。例如

2022 年 9 月,瑞典 Kaunis Iron 公司開始與沃爾沃卡車合作測試一輛 74 噸的電動卡車。這輛卡車在瑞典北部考尼斯瓦拉 (Kaunisvaara) 和皮特卡耶爾維 (Pitkajärvi) 之間 160 公里長的公路上進行了運輸鐵礦石的測試。 Kaunis Iron 計劃投資 5 億瑞典克朗(4,800 萬美元),使其卡車車隊全面實現電氣化。此外,礦業公司和OEM之間簽署了重要契約,以在其礦山中測試和部署電動運輸卡車,進一步推動了全球範圍內電動自卸卡車和電動採礦卡車的採用。例如

2022 年 9 月,總部位於澳洲的 Newcrest Mining 宣布,它正逐步傾向於用電池電動卡車取代其位於加拿大不列顛哥倫比亞省 Brucejack 金銀礦的所有柴油卡車車隊。預計這一轉變將使 Newcrest Mining 在 2030 年減少 65,000 噸二氧化碳排放。 Newcrest Mining 預計其全部 12 輛柴油卡車將於 2022 年底前完成向電氣化的轉變。 Newcrest Mining 的子公司 Pretium Resources 於 2020 年在其礦場完成了山特維克 Z50 電池電動運輸卡車的試驗。

由於上述案例和基礎設施領域的發展,預計市場在預測期內將出現樂觀成長。

預計亞太地區將在預測期內引領市場

亞太地區自動卸貨卡車和採礦卡車市場成長的關鍵因素之一是中國、印度、日本和澳洲等國家採礦活動的增加。在中國東部,政府已經鋪設了通往居民住宅的天然氣管道,但居民仍無法獲得穩定的天然氣供應。因此,越來越多的人使用煤炭取暖。隨著政府放鬆嚴格的政策,中國最大的煤炭生產省份山西省計劃增加近 1,100 萬噸焦炭產能,以滿足日益成長的需求。

中國的目標是盡量減少對進口煤炭的依賴。國家發展改革委員會(原國家計委、國家發展計畫委員會)日前宣布,2021年煤炭產量將突破40億噸。此外,也計畫增加煤炭產量3億噸,相當於中國每年的進口量。預計這將大幅減少對煤炭進口的依賴。在俄羅斯入侵烏克蘭後,該國受到全球價格創紀錄的衝擊,預計生產能力的提高將使該國減少對外國進口的依賴。此外,中國是最大的鋼鐵生產國,全球約有一半的鋼鐵產自中國。中國也生產全球約90%的稀土。

此外,印度也同樣為亞太地區礦業生產的提升做出了貢獻。據印度礦業部稱,截至 22 會計年度,已有 1,245 個礦山註冊,並且在當前情況下積極報告穩定的產量。由於採礦活動龐大,採礦業的各個相關人員正在引入新一代技術來從礦場運輸礦物。例如

2021 年 9 月,印度煤炭有限公司與國營天然氣公司 GAIL 和印度採礦機械公司 OWM BEML 簽署了一份合作備忘錄,開展先導計畫,使用液化天然氣作為該國現有採礦自動卸貨卡車雙燃料運行的替代燃料。為了減少二氧化碳排放,兩家公司已開始在自動卸貨卡車上安裝液化天然氣改裝套件,該礦隸屬於馬哈納迪煤田有限公司 (MCL)。

當地企業正在贏得建設公司和採礦公司的新合約。預計上述發展將在預測期內推動市場成長。

礦用自動卸貨卡車產業概況

全球自動卸貨卡車和礦用卡車市場適度整合,國內外活躍參與者數量有限。市場的主要企業包括Caterpillar公司、斗山工程機械、日立建築機械和利勃海爾集團。公司正在開發和添加新技術到現有模型中,推出新模型,並探索新的尚未開發的市場。

隨著礦業公司投資推出營運,這可能為一些礦業設備製造商帶來機會。例如,2021年3月,力拓宣布將開始在其位於美國的肯尼科特礦場生產碲。該公司表示,將在金屬回收製程上投資 290 萬美元,年產能為 20 噸。這種金屬用於生產太陽能電池。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 市場限制

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 按卡車類型

- 側自動卸貨卡車

- 後自動卸貨卡車

- 按燃料類型

- 內燃機

- 電動式的

- 按容量類型

- 少於200噸

- 超過200噸

- 按應用

- 礦業

- 建造

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 澳洲

- 其他亞太地區

- 世界其他地區

- 巴西

- 墨西哥

- 阿拉伯聯合大公國

- 其他國家

- 北美洲

第6章競爭格局

- 供應商市場佔有率

- 公司簡介

- Caterpillar, Inc.

- Hitachi Construction Machinery Co. Ltd.

- Komatsu Ltd.

- Liebherr Group

- BAS Mining Trucks

- Sany Heavy Industry Co., Ltd.

- Volvo Group

- Daimler Group

- BelAZ

- Ashok Leyland Ltd.

- Doosan Infracore

第7章 市場機會與未來趨勢

The Dump Trucks and Mining Trucks Market size is estimated at USD 30.41 billion in 2025, and is expected to reach USD 40.18 billion by 2030, at a CAGR of 5.73% during the forecast period (2025-2030).

The demand for mining trucks is expected to rise on the backdrop of increased mining activity due to continuous demand for minerals and ores, which are necessary for various industries and infrastructural project development. The global mining industry needs more skilled human resources. Moreover, in the wake of the COVID-19 outbreak and industries shut down, the situation is expected to drive the mining companies to improve their production efficiency, which in turn is expected to drive the demand for more mining trucks. Moreover, 2021 was the year of transition where the mining activities again took their recovery phase exhibiting immense growth potential.

The mining industry is now witnessing the government's stringent emission and import-export regulations. Productivity must get improved to increase the profit margins. It is causing companies to automate and electrify mining trucks by installing sensors and analyzing their data. OEM is offering electric power trains amid rising electrification globally. In addition, technological aspects, including telematics, have also elevated the demand positively.

The Asia-pacific region is expected to hold the highest potential for the growth of mining equipment, including material handling equipment like Dump and mining trucks. The area offers immense potential in mining output and mineral mines, elevating the demand for dump trucks and mining trucks. With the increased production in surface mining, the predictable nature of equipment maintenance, and the replacement cycle in surface mining, the region observed an increase in the production of mining equipment.

Mining Dump Truck Market Trends

Electric Trucks are Projected to Witness a High Growth Rate During the Forecast Period

Over the past few years, significant markets for dump and mining trucks like China, India, and Europe have adopted stringent emissions norms, like Bharat 6 in India, China 6 standards in China, and Euro 6 in Europe. They have made electrification and hybridization necessary, especially for diesel engine vehicles, as they must be equipped with Selective Catalytic Reduction (SCR) and Exhaust Gas Recirculation (EGR) technologies. It will reduce the sulfur soot and other sulfur-based emissions from diesel engines. These systems' installation into diesel engines further pushed diesel vehicle prices, including dump trucks and mining trucks. Many countries like the United States are also promoting electric truck sales by providing direct tax credits for electric truck purchases through the recently passed Inflation Reduction Act. These measures are expected to boost electric truck adoption in the mining sector since mining trucks account for more than 60% of the total emissions from mines. For instance,

In September 2022, Kaunis Iron in Sweden began testing 74-ton electric trucks in association with Volvo Trucks. The trucks were tested to transport iron ore over a 160 km road between Kaunisvaara and Pitkajarvi in northern Sweden. Kaunis Iron plans to invest SEK 500 million (USD 48 million) to electrify its truck fleet completely. Additionally, significant contracts between mining companies and OEMs to test and deploy electric haul trucks at their mines are further boosting the adoption of electric dump and mining trucks worldwide. For instance,

In September 2022, Australia-based Newcrest Mining announced that it is slowly inclining its way towards electrifying its entire diesel truck fleet to battery-electric at its Brucejackgold-silver mine in British Columbia, Canada. This transition is expected to save 65000 tons CO2 emissions by 2030 for Newcrest Mining. Newcrest Mining expects the evolution of its entire fleet of 12 diesel-powered trucks to electrification to be completed by the end of 2022. Newcrest Mining's subsidiary Pretium Resources Inc. completed the Sandvik Z50 battery-electric haul truck trials at their mine in 2020.

Due to the abovementioned instances and developments in the infrastructure sector, the market is expected to witness optimistic growth over the forecast period.

Asia-Pacific is Projected to Lead the Market During the Forecast Period

One of the critical factors in the growth of the Asia-Pacific dump trucks and mining trucks market is the increase in mining activities in countries such as China, India, Japan, Australia, etc. In eastern China, the government fitted gas pipelines in households but had not yet supplied gas regularly. It increases the consumption of coal by people for heating purposes. China's largest coal-producing province, Shanxi, provided relaxation on stringent government policies and plans to add nearly 11 million tons of coke-producing capacities to meet growing demand.

China is aiming to minimize its coal import dependency. The NDRC (National Development and Reform Commission), formerly State Planning Commission and State Development Planning Commission, stated that the country produced more than 4 billion tons of coal in 2021. Further, they are striving to increase their coal output by 300 million tons, equal to China's annual import. It is expected to cut the reliance on coal imports dramatically. A rise in capacity would reduce the country's dependence on overseas imports after record-high world prices were hit in the wake of Russia's invasion of Ukraine. In addition, China is the largest steel producer, and about half of the world's steel is produced in the country. China also produces around 90% of the world's rare earth metals.

Moreover, India contributed equally to elevating the Asia-Pacific region's mining output. According to the Ministry of Mines in India, as of FY 2022, 1,245 mines were registered to report and produce steady throughput in the current scenario actively. Due to the immense activity from the mining industry, various stakeholders operating in the industry have been introducing new generation technologies for mineral hauling from the mine sites. For instance,

In September 2021, Coal India Limited signed an MoU with state gas utility GAIL and Indian mining equipment OWM BEML for a pilot project to use LNG as an alternative fuel for dual fuel operation of existing mining dump trucks in the country. Intending to reduce carbon emissions, the companies say they have initiated the process of fitting LNG conversion kits on two 100-ton class dump trucks at the Lakhanpurmine in Jharsuguda district, Odisha, part of Mahanadi Coalfields Ltd (MCL).

Regional players are getting new contracts from construction and mining companies. All the developments above are expected to help the market growth over the forecast period.

Mining Dump Truck Industry Overview

The global dump trucks and mining trucks market is moderately consolidated, with a limited number of active local and international players. Some major players in the market are Caterpillar, Inc., Doosan Infracore, and Hitachi Construction Machinery Co., Ltd., Liebherr Group, amongst others. The companies are developing and adding new technologies to their existing models, launching new models, and tapping into new and unexplored markets.

Mining companies are investing in setting up their operation, which might act as an opportunity pocket for several mining equipment manufacturers. For instance, in March 2021, Rio Tinto Company announced that it would start Tellurium production in Kennecott mine, US. The company announced an investment of USD 2.9 million for the metal recovery process and will have a production capacity of 20 tons per year. This metal is used in the production of photovoltaic cells.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD Billion)

- 5.1 By Truck Type

- 5.1.1 Side dump truck

- 5.1.2 Rear Dump truck

- 5.2 By Fuel Type

- 5.2.1 IC Engine

- 5.2.2 Electric

- 5.3 By Capacity Type

- 5.3.1 Less than 200 metric ton

- 5.3.2 More than 200 metric ton

- 5.4 By Application Type

- 5.4.1 Mining

- 5.4.2 Construction

- 5.4.3 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 Brazil

- 5.5.4.2 Mexico

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Other Countries

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Caterpillar, Inc.

- 6.2.2 Hitachi Construction Machinery Co. Ltd.

- 6.2.3 Komatsu Ltd.

- 6.2.4 Liebherr Group

- 6.2.5 BAS Mining Trucks

- 6.2.6 Sany Heavy Industry Co., Ltd.

- 6.2.7 Volvo Group

- 6.2.8 Daimler Group

- 6.2.9 BelAZ

- 6.2.10 Ashok Leyland Ltd.

- 6.2.11 Doosan Infracore

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

自動卸貨卡車市場:2025-2032年全球預測(按負載容量、動力和應用分類)鉸接式自動卸貨卡車市場:2025-2032年全球預測(按動力類型、負載容量、應用、最終用戶和銷售管道)

自動卸貨卡車市場:2025-2032年全球預測(按負載容量、動力和應用分類)鉸接式自動卸貨卡車市場:2025-2032年全球預測(按動力類型、負載容量、應用、最終用戶和銷售管道) 2025年全球鉸接式自動卸貨卡車輪胎市場報告

2025年全球鉸接式自動卸貨卡車輪胎市場報告 自卸卡車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

自卸卡車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 全球電動工程自動卸貨卡車市場全球建築自動卸貨卡車市場鉸接式運輸車輛的全球市場全球電動自動卸貨卡車市場2025年全球自動卸貨卡車市場報告

全球電動工程自動卸貨卡車市場全球建築自動卸貨卡車市場鉸接式運輸車輛的全球市場全球電動自動卸貨卡車市場2025年全球自動卸貨卡車市場報告 自動卸貨卡車市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032年)

自動卸貨卡車市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032年)