|

市場調查報告書

商品編碼

1689838

協作機器人:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Collaborative Robot - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

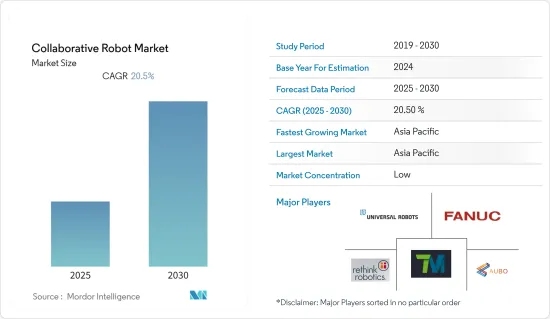

預計協作機器人市場在預測期內的複合年成長率將達到 20.5%。

隨著機器人與人類的合作越來越緊密,它們必須對使用者做出反應並調整自己的行為。未來幾年,研究人員可能會開始識別人類的基本行為,並調整機器人的行為來適應它們。在接下來的幾年裡,這可能會演變成一個更先進的程序,可以適應複雜任務的需求。

關鍵亮點

- 數位雙胞胎、虛擬實境(VR)和擴增實境(AR)等先進技術的強勁成長,以及離線編程和模擬軟體的發展,使企業能夠最佳化機器人性能。您還可以開發和測試不同的配置以找到最適合您要求的解決方案。

- 邊緣運算是一種有趣的新網路架構方法,有助於克服傳統雲端基礎的網路的限制。隨著自主機器人和醫療感測器等創新機器變得越來越普遍,邊緣運算預計將對社會產生深遠的影響。

- 人工智慧 (AI) 的快速發展使機器能夠在不斷變化的環境中精確地執行任務。整合人工智慧的協作機器人可以協助製造商進行各種應用,使業務更有效率、順暢和富有成效。配備人工智慧的協作機器人可以識別材料的方向和存在,執行檢查和測試,動態拾取和放置任務,讀取檢查後的結果並相應地指導決策。

- 更長的培訓和入職期、更高的社會福利和薪酬以及勞動力短缺是推動採用的主要因素。越來越多的倉庫、配送和履約設施正在投資自動化解決方案。隨著技術的進步和應用的日益廣泛和靈活,機器人技術正在被世界各地的更多製造業務所採用。

- 融入先進技術的機器人比傳統機器人更昂貴。機器人系統的成本與強大的硬體和高效的軟體有關。自動化設備由於採用先進的自動化技術,需要較高的資金投入。例如,自動化系統的設計、製造和安裝可能要花費數百萬美元。

協作機器人市場趨勢

汽車終端用戶領域預計將佔據主要市場佔有率

- 在汽車產業,每日產量正在大幅成長。生產現場的機器需要適當的維護,以縮短生產週期並提高生產產量。協作機器人可以輕鬆降低直接生產成本。此外,根據考慮的組裝過程,它可以實現比傳統機器人系統更高的吞吐量。這種協作機器人用於汽車產業,可應用於汽車零件製造(汽車關鍵零件的組裝)和整車組裝。

- 由於中國、印度和越南等亞洲國家汽車工廠的激增,以及北美汽車製造商對汽車機器人的需求增加,汽車應用中使用的協作機器人最近得到了大幅成長。包括寶馬、梅賽德斯-奔馳和福特在內的多家知名汽車製造商已在其生產車間部署了協作機器人,以執行焊接、汽車噴漆和組裝工作等各種功能。

- 過去幾年,汽車產業一直在組裝上使用機器人進行各種製造流程。協作機器人精確、靈活、高效且可靠,這就是汽車製造商正在研究在更多流程中使用它們的原因。這使得汽車產業成為全球最自動化的供應鏈之一,並繼續成為機器人的最大用戶之一。根據IFR預測,2024年全球工業機器人出貨量將達到約51.8萬台。

- 2022 年 4 月,Stellantis NV 的子公司汽車製造商飛雅特向米拉菲奧裡工廠投資 7 億歐元(7.5 億美元),利用協作機器人等最尖端科技生產 500 輛電動車。該公司安裝了 11 台 Universal Robots A/S 的協作機器人,以實現複雜的組裝任務和品管的自動化。

- 飛雅特使用的協作機器人執行各種組裝任務,包括品管、擰緊螺絲、上漆和目視檢查。作為該計劃的一部分,該公司正在使用協作機器人將操作員從重複的、體力要求高的手動任務中解放出來,並使他們能夠參與更高附加價值的流程。隨著這些企業的努力,預計汽車產業對協作機器人的需求將進一步增加。

亞太地區預計將佔據主要市場佔有率

- 由於亞太地區行業數量的不斷增加以及與自動化的整合以提高投資回報率,亞太地區協作機器人市場正在大幅擴張。由於中國協作機器人的生產、銷售和交易不斷增加,預計亞太協作機器人市場將由中國主導。

- 中國協作機器人市場領先歐洲、中東、非洲和美洲。例如,2021年12月21日,北京工業和資訊化部發布了機器人產業發展「十四五」規劃,重點推動技術創新,在未來五年內將機器人技術納入八大重點產業,使中國在機器人技術和產業發展方面達到全球領先水平。因此,2022年4月23日,一項名為「智慧機器人」的獨特計畫在國家重點研發計畫下啟動,資助金額為4,350萬美元。

- 印度市場正在見證協作機器人技術的穩定成長,因為許多流程沒有明確的標準化,數位化程度與其他市場相比較低,許多企業仍然以非結構化的方式運作。

- 此外,印度政府和中小企業本身透過區域和國家舉措,在中小企業中採用工業 4.0 方面有著良好的記錄。這些企業一直透過數位化中小微型企業計劃,將現有基礎設施數位化並將其轉換為雲端基礎的技術,帶頭實施工業 4.0。隨著工業數位化,協作機器人是工業4.0中發展的強大技術之一。協作機器人是工業4.0最重要的貢獻者,在打造智慧製造環境方面取得了巨大的飛躍。

- 日本正快速邁向“社會5.0”,在這個全新的超智慧社會中開啟人類發展四大階段中的第5章。一切將透過物聯網技術連接起來,所有技術將融合在一起,從而極大地改善我們的生活品質。為了實現這一新時代,日本政府採取了各種適當措施,鼓勵包括Start-Ups公司和中小企業的「隱藏人才」在內的眾多參與企業為市場帶來新的創新理念,以解決人口造成的勞動力短缺等問題。

協作機器人產業概況

協作機器人市場高度分散,有許多主要參與者,包括 Universal Robots AS、Fanuc Corp.、TechMan Robot Inc.、Rethink Robotics GmbH、AUBO Robotics USA 和 ABB Ltd.。這些市場參與企業正在利用夥伴關係、合併、創新、投資、收購等來改進其產品並獲得競爭優勢。

- 2023 年 2 月—Rapid Robotics 宣布與 Universal Robots (UR) 建立新的合作。 UR 將為 Rapid Robotics 在北美部署的協作機器人工作單元提供協作機械臂。該交易將使該公司能夠透過使用機器人勞動力來填補製造商無法填補的職位,進一步消除自動化障礙。

- 2022年11月 - Techman Robot推出協作機器人TM AI Cobots系列,將強大而精確的機械臂與原生AI推理引擎和智慧視覺系統結合。一系列智慧機械臂配備全面的AI軟體套件,包括TM AI+Training Server、TM AI+AOI Edge、TM Image Manager和TM 3DVisionTM,使企業能夠訓練和客製化系統以精確適應其應用。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- 產業價值鏈分析

- COVID-19 市場影響

- 定價分析

第5章市場動態

- 市場促進因素

- 邊緣運算和人工智慧的進步使實施變得更加容易

- 各種工業流程對自動化的需求不斷增加

- 市場限制

- 初始投資高且需熟練勞動力

第6章市場區隔

- 按有效載荷

- 5公斤以下

- 5~9Kg

- 10~20Kg

- 超過20公斤

- 按最終用戶產業

- 電子產品

- 車

- 製造業

- 飲食

- 化學品和製藥

- 其他

- 按應用

- 物料輸送

- 拾取和放置

- 組裝

- 碼垛和卸垛

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 亞洲

- 中國

- 印度

- 日本

- 澳洲和紐西蘭

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 北美洲

第7章競爭格局

- 公司簡介

- Universal Robots AS

- Fanuc Corp.

- TechMan Robot Inc.

- Rethink Robotics GmbH

- AUBO Robotics USA

- ABB Ltd.

- Kawasaki Heavy Industries Ltd.

- Precise Automation Inc.

- Siasun Robot & Automation co. Ltd.

- Staubli International AG

- Omron Corporation

- Festo Group

- Epson Robots(Seiko Epson)

- KUKA AG

第8章投資分析

第9章:市場的未來

The Collaborative Robot Market is expected to register a CAGR of 20.5% during the forecast period.

As robots work even more closely with humans, they must respond to the users and adapt their behaviors. Over the next few years, researchers are expected to recognize basic human behaviors and adapt these robots' actions to respond to them. Over the next few years, this would develop into much more advanced programs that could adapt to the needs of complex tasks.

Key Highlights

- Robust growth in advanced technologies, such as digital twins, virtual reality (VR), augmented reality (AR), and developments in offline programming and simulation software, enables companies to optimize robot performance. It also helps them develop and test different configurations to find the best solution for their requirements.

- Edge computing is an interesting new approach to network architecture that helps businesses break beyond the limitations of traditional cloud-based networks. As innovative machines like autonomous robots and medical sensors become more common, edge computing will significantly impact society.

- Rapid advancements in artificial intelligence (AI) enable them to execute tasks accurately in a continuously changing environment. AI-integrated cobots help manufacturers in various applications that make operations run efficiently, smoothly, and productively. AI-driven cobots recognize the orientation and presence of materials, perform testing and inspection, dynamically pick and place tasks, read results post-inspection, and derive decisions accordingly.

- Longer training and onboarding, increasing benefits and compensation rates, and labor shortages are significant factors driving the deployment. More and more warehousing, distribution, and fulfillment facilities are investing in automated solutions. As technology improves and the applications become broader and more flexible, robotics is being adopted by a more significant number of manufacturing operations across regions.

- The robots integrated with advanced technologies cost high as compared to traditional robots. The costs of robotic systems are associated with robust hardware and efficient software. Automation equipment involves the usage of advanced automation technologies that require high capital investment. For instance, an automated system may cost millions of Dollars for design, fabrication, and installation.

Collaborative Robots Market Trends

Automotive End-User Segment is Expected to Hold Significant Market Share

- The automotive sector is witnessing significant growth in the number of units produced per day. The machinery on the production floor requires proper maintenance to shorten production cycles and increase production output. Cobots can easily achieve lower direct unit production costs. Moreover, depending on the assembly process considered, the throughput can be higher than in traditional robotic systems. These cobots are used in the automotive industry, where they can be applied to auto part manufacturing (assembling significant parts of a vehicle) and finished vehicle assembly.

- Collaborated robotics used for automotive applications are experiencing a massive upsurge in recent times owing to the proliferation of automotive plants in eminent Asian nations, including China, India, and Vietnam, and growing demand for automotive robotics from automakers in North America. Various prominent automakers, including BMW, Mercedes Benz, and Ford, have been deploying cobotson on their production floors to carry out myriad functions such as welding, car painting, and assembly line activities.

- The automotive industry has utilized robots in its assembly lines for various manufacturing processes for the past few years. Automakers are researching the use of robotics in even more processes, as cobots are accurate, flexible, more efficient, and dependable on these production lines. This has allowed the automotive industry to remain one of the most automated supply chains globally and one of the largest robot users. According to IFR, global industrial robot shipments will amount to about 518,000 in 2024.

- In April 2022, an automotive manufacturing company, Fiat, a subsidiary of Stellantis NV, invested EUR 700 million (USD 750 million) at its Mirafiori factory to produce 500 electric vehicles using state-of-the-art technology, such as collaborative robots. The company aims to automate its complex assembly line operations and quality controls, installing 11 cobots from Universal Robots A/S.

- The cobots used by Fiat would perform various assembly tasks, including quality control, screwdriving, dispensing, and visual inspection. In line with these initiatives, the company would use collaborative automation robots to free the operators from physically demanding and repetitive manual tasks so that they can be employed on processes with greater added value. Such initiatives by the companies in the market are expected to further fuel the demand for collaborative robots in the automotive industry.

Asia Pacific is Expected to Hold Significant Market Share

- The market for collaborative robots in the Asia Pacific is expanding significantly due to the growing number of industries in the region and their integration with automation to increase the ROI. The Asia Pacific collaborative market is predicted to be dominated by China with the growing production, sales, and trade of cobots in China.

- The Chinese market for collaborative robots is leading over the EMEA and Americas regions as the country continues to take industrial automation as the primary focus goal. For instance, the Ministry of Industry and Information Technology (MIIT) in Beijing released the "14th Five-Year Plan" for Robot Industry Development on 21st December 2021, focusing on promoting innovation to make China a global leader in robot technology and industrial advancement by including it in 8 critical industries for the next five years. As a result, the essential unique program "Intelligent Robots" was launched under the National Key R&D Plan on 23rd April 2022 with a funding of USD 43.5 million.

- In India, the collaborative robot market is significantly observing steady growth as many processes in the Indian market are not clearly standardized, and a large number of businesses still run in an unstructured way with lower levels of digitization compared to other developed markets.

- Moreover, India has a proven track record of implementing Industry 4.0 in small and medium enterprises through regional and national initiatives by the Government of India and MSMEs themselves. These enterprises have spearheaded the implementation of Industry 4.0 through digital MSME schemes by converting the existing infrastructure into digital, cloud-based technologies. With the industries getting digitized, one of the powerful technologies that evolved in Industry 4.0 is collaborative robots, which have paramount importance in contributing to Industry 4.0 and have made significant breakthroughs by creating an intelligent manufacturing environment.

- Japan is rapidly moving toward "Society 5.0", thus introducing the fifth chapter to the four major stages of human development in this new ultra-smart society. All things are connected through IoT technology, and all technologies are getting integrated, dramatically improving the quality of life. To realize this new era, the Government of Japan is taking various suitable steps to encourage numerous players, including start-ups and "hidden gems" among small- and medium-sized organizations, to come up with brand-new and innovative ideas for facilitating the world with solutions with problems such as labor shortages owing to population.

Collaborative Robots Industry Overview

The collaborative robot market is highly fragmented, with the presence of many major players like Universal Robots AS, Fanuc Corp., TechMan Robot Inc., Rethink Robotics GmbH, AUBO Robotics USA, and ABB Ltd, among others. These players in the market use partnerships, mergers, innovations, investments, and acquisitions to improve their products and gain a competitive edge over others.

- February 2023 - Rapid Robotics announced a new collaboration with Universal Robots (UR), in which UR would supply collaborative robot arms for Rapid Robotics' deployment of cobot work cells across North America. Through this agreement, the company will be able to remove further obstacles to automation by using a robotic workforce to fill positions that manufacturers are unable to fill.

- November 2022 - TechmanRobot introduced its TM AI Cobotseries of collaborative robots, which combines a powerful and precise robot arm with a native AI inferencing engine and smart vision system. It is an intelligent robotic arm series with a comprehensive AI software suite, including TM AI+ Training Server, TM AI+ AOI Edge, TM Image Manager, and TM 3DVisionTM, facilitating companies to train and tailor their system to precisely meet their application.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

- 4.5 Pricing Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Advancements in Edge Computing & AI Leading to Easier Implementation

- 5.1.2 Increasing Demand for Automation in Various Industrial Processes

- 5.2 Market Restraints

- 5.2.1 High Initial Investment and the Requirement of Skilled Workforce

6 MARKET SEGMENTATION

- 6.1 By Payload

- 6.1.1 Less Than 5Kg

- 6.1.2 5-9 Kg

- 6.1.3 10-20 Kg

- 6.1.4 More Than 20 KG

- 6.2 By End-user Industry

- 6.2.1 Electronics

- 6.2.2 Automotive

- 6.2.3 Manufacturing

- 6.2.4 Food and Beverage

- 6.2.5 Chemicals and Pharmaceutical

- 6.2.6 Other End-user Industries

- 6.3 By Application

- 6.3.1 Material Handling

- 6.3.2 Pick and Place

- 6.3.3 Assembly

- 6.3.4 Palletizing and De-palletizing

- 6.3.5 Other Applications

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Universal Robots AS

- 7.1.2 Fanuc Corp.

- 7.1.3 TechMan Robot Inc.

- 7.1.4 Rethink Robotics GmbH

- 7.1.5 AUBO Robotics USA

- 7.1.6 ABB Ltd.

- 7.1.7 Kawasaki Heavy Industries Ltd.

- 7.1.8 Precise Automation Inc.

- 7.1.9 Siasun Robot & Automation co. Ltd.

- 7.1.10 Staubli International AG

- 7.1.11 Omron Corporation

- 7.1.12 Festo Group

- 7.1.13 Epson Robots(Seiko Epson)

- 7.1.14 KUKA AG

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球人機互動系統市場:預測至2032年-按組件、互動類型、負載容量、應用、最終用戶和地區分類的分析全球共用與協作消費市場:預測至2032年-依資產類型、共用方式、產業、使用者意圖、技術介面、貨幣化模式、最終使用者與地區進行分析

全球人機互動系統市場:預測至2032年-按組件、互動類型、負載容量、應用、最終用戶和地區分類的分析全球共用與協作消費市場:預測至2032年-依資產類型、共用方式、產業、使用者意圖、技術介面、貨幣化模式、最終使用者與地區進行分析 協同製造解決方案市場分析與預測(至 2034 年):類型、產品、服務、技術、組件、應用、流程、最終用戶、部署和功能協作機器人 (Cobots) 市場預測(至 2032 年):按組件、有效載荷能力、公司類型、應用、最終用戶和地區進行的全球分析協作機器人市場預測至2032年:按組件、負載容量、應用、最終用戶和地區分類的全球分析

協同製造解決方案市場分析與預測(至 2034 年):類型、產品、服務、技術、組件、應用、流程、最終用戶、部署和功能協作機器人 (Cobots) 市場預測(至 2032 年):按組件、有效載荷能力、公司類型、應用、最終用戶和地區進行的全球分析協作機器人市場預測至2032年:按組件、負載容量、應用、最終用戶和地區分類的全球分析 行動協作機器人市場(按組件類型、負載容量、應用和最終用途行業)—2025-2032 年全球預測

行動協作機器人市場(按組件類型、負載容量、應用和最終用途行業)—2025-2032 年全球預測 全球協作機器人市場成長機會(2025-2029)

全球協作機器人市場成長機會(2025-2029) 2025年協作機器人全球市場報告全球機器人關節模組市場按類型、自由度、控制類型、材料、有效載荷能力、機器人類型和最終用戶分類 - 預測至 2025-2030 年協作機器人市場按類型、負載容量、安裝類型、應用、最終用戶行業和銷售管道- 全球預測,2025-2030 年

2025年協作機器人全球市場報告全球機器人關節模組市場按類型、自由度、控制類型、材料、有效載荷能力、機器人類型和最終用戶分類 - 預測至 2025-2030 年協作機器人市場按類型、負載容量、安裝類型、應用、最終用戶行業和銷售管道- 全球預測,2025-2030 年