|

市場調查報告書

商品編碼

1689789

厭氧膠:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Anaerobic Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

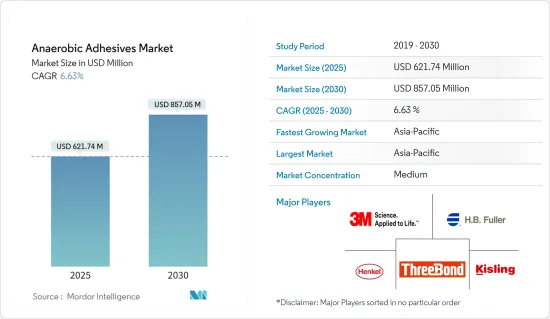

厭氧膠合劑市場規模預計在 2025 年為 6.2174 億美元,預計到 2030 年將達到 8.5705 億美元,預測期內(2025-2030 年)的複合年成長率為 6.63%。

2020 年,新冠疫情對市場產生了負面影響。然而,由於電氣和電子、建築和施工等各個終端用戶行業的消費增加,市場在 2021 年顯著復甦。

關鍵亮點

- 從中期來看,汽車產業的復甦以及電氣電子產業需求的成長將推動研究市場的成長。

- 另一方面,厭氧膠的高成本阻礙了厭氧膠市場的成長。

- 研發和生物基原料的增加,加上對可再生能源市場的日益關注,可能為研究市場帶來豐厚的機會。

- 亞太地區在全球厭氧膠市場佔據主導地位,並且很可能在預測期內以最高的複合年成長率成長。

厭氧膠市場趨勢

汽車和運輸業的需求增加

- 固持化合物、管道密封劑、墊片密封劑和螺紋鎖固膠在汽車工業中已廣泛應用。

- 這些用於引擎和防火牆密封、引擎監控感測器、引擎插頭密封劑、螺紋軟管連接器密封劑、引擎室內管道和直螺紋的螺紋軟管接頭密封劑、螺紋鎖緊螺絲、螺栓和螺母的內部密封應用、車輪軸承、汽車鎖定應用、汽車車體/車架螺栓、懸吊區域、煞車、後端、變速箱和許多其他應用。

- 厭氧膠也用於航太工業的維護、維修和操作 (MRO) 應用,例如螺紋鎖定、固定、墊片和螺紋密封。這些黏合劑可幫助製造商避免在 MRO 期間對大面積機器零件進行不必要的加工。

- 近期從內燃機到電動車的轉變正在推動自動駕駛技術的創新。厭氧膠可取代機械緊固件,因為它們可以適應熱膨脹引起的運動,且不易腐蝕。

- 與傳統連接方法相比,黏合劑更受青睞,因為它們可以防止接觸腐蝕,並提供承受馬達高動態所必需的抗衝擊性。

- 世界領先的汽車製造商已宣布計劃透過開發新的產品線和改造現有的製造設施來加速其電動車的未來發展。例如

- 豐田宣布,到 2030 年將推出 30 款電池電動車 (BEV)。

- 沃爾沃承諾在2030年成為一家全電動汽車公司。

- 通用汽車的目標是到2025年在北美擁有30款電動車,產能達到100萬輛。

- 2021年全球汽車產量為8,014萬輛。這比2020年成長了3%。歐洲汽車產量較2020年下降4%至1633萬輛。在美國,銷量較2020年成長3%,達1,615萬輛。

- 亞太地區在2021年呈現顯著成長,較2020年成長6%,達4,673萬輛;非洲地區在2021年呈現顯著成長,較2020年成長16%,達到93萬輛。

- 2022年,我們的合資企業廣汽本田將在中國廣州開始建造新工廠。該工廠每年可生產12萬輛電動車,預計2024年投入生產。預計投資額為34.9億元(約5億美元)。

- 這些趨勢正在推動厭氧膠市場的發展。

亞太地區佔市場主導地位

- 亞太地區由各種新興市場主導,尤其是中國和印度等國家。

- 中國是世界上最大的汽車製造國。根據OICA預測,2021年汽車產量將達到2,608萬輛,較2020年的2,523萬輛成長3%。

- 2021年11月,與2020年同期相比,純電動車銷量成長了106%。 2021年11月電動車銷量達約413,094輛。市場佔有率也增加到 19%,其中 15% 為純電動車,4% 為插混合動力汽車。

- 中國也是最大的飛機製造國之一,也是國內航空客運的最大市場之一。此外,該國的飛機零件和組裝製造業正在蓬勃發展,超過 200 家小型飛機零件製造商對厭氧膠的使用和需求正在增加。根據波音公司《2021-2040年商業展望》,到2040年中國將交付約8,700架新飛機,市場服務價值達1.8兆美元。此類新交付可能會增加所研究市場的需求。

- 此外,根據 OICA 的數據,2021 年印度生產了約 43,991,112 輛汽車,比 2020 年的 3,381,819 輛產量增加 30%。

- 在航太領域,根據印度品牌資產基金會(IBEF)的數據,印度航空業預計將在未來四年吸引 3,500 億印度盧比(約 49.9 億美元)的投資。預計未來20年中國將需要2,100架飛機,銷售額預計將超過2,900億美元。由於這些因素,預計未來航太領域對厭氧膠的需求將會增加。

- 預計到 2025 年,印度將成為全球第五大家用電子電器產業。此外,4G/LTE 網路和物聯網 (IoT) 的推出等技術轉型正在推動印度電子產品的普及。 「數位印度」和「智慧城市」計劃等措施正在推動該國對物聯網的需求。

- 印度龐大的建築業預計在2022年成為世界第三大建築市場。印度政府採取的各項舉措,包括「智慧城市」計劃和「2022年全民住宅」計劃,預計將為低迷的建築業提供急需的提振。例如,在「Pradhanmantri Awas Yojana」計畫下,印度政府決定向低收入住宅提供最高貸款額 12,000 印度盧比(約 14,550 美元)和 9,000 印度盧比(約 10,920 美元)的 3% 和 4% 的利息補貼,以幫助低收入家庭購買和房屋。

- 總體而言,所有這些因素都可能影響預測期內該地區對厭氧膠的需求。

厭氧膠產業概況

全球厭氧膠市場由各地區的全球和國內參與企業固體。然而,市場排名前五的公司佔據了全球大部分市場佔有率。厭氧膠合劑市場的主要企業包括漢高公司、3M、HB Fuller Company、Kisling AG、ThreeBond Holdings 等(排名不分先後)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 汽車產業復甦

- 電氣和電子產業需求增加

- 限制因素

- 厭氧膠成本高

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 產品類型

- 螺紋鎖固劑

- 螺紋密封劑

- 固定化合物

- 墊片密封膠

- 最終用戶產業

- 汽車與運輸

- 電氣和電子

- 工業的

- 建築與施工

- 其他

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 合併、收購、合資、合作和協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- 3M

- Anabond Limited

- Asec Co., Ltd

- HB Fuller Company

- Henkel AG and Co. KGaA

- Hi-Bond Chemicals

- Kisling AG

- Krylex(Chemence)

- Metlok Private Limited

- Novachem Corporation ltd

- Parson Adhesives, Inc.

- Permabond LLC.

- ThreeBond Holdings Co., Ltd

第7章 市場機會與未來趨勢

- 增加生物基材料的研究、開發與使用

- 可再生能源市場日益受到關注

The Anaerobic Adhesives Market size is estimated at USD 621.74 million in 2025, and is expected to reach USD 857.05 million by 2030, at a CAGR of 6.63% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020. However, the market recovered significantly in 2021, owing to rising consumption from various end-user industries such as electrical and electronics, building and construction, and others.

Key Highlights

- Over the medium term, recovering the automotive industry and increasing demand from electrical and electronics industries are driving the growth of the studied market.

- On the flip side, the high cost of anaerobic adhesives hinders the growth of the anaerobic adhesives market.

- Nevertheless, increasing research and development and bio-based raw materials, coupled with growing prominence in the renewable energy market, are likely to act as lucrative opportunities for the studied market.

- Asia-Pacific is likely to dominate the global anaerobic adhesives market and is likely to grow with the highest CAGR during the forecast period.

Anaerobic Adhesives Market Trends

Increasing Demand from the Automotive and Transportation Industry

- In the automotive industry, retaining compounds, pipe sealants, gasket sealants, and thread-locking adhesives are widely used.

- They are used in the applications of engine and firewall sealing, engine monitor sensors, engine plug sealants, threaded hose connector sealants, threaded hose nipple sealants for pipes and straight threads of engine compartments, for interior sealing applications of thread-locking screws, bolts, and nuts, wheel bearings, automotive locking applications, automotive body/frame bolts, suspension areas, brakes, rear end, and transmission and many other applications.

- Anaerobic adhesives are also used in aerospace industry maintenance, repair, and operation (MRO) applications for applications including thread-locking, retaining, gasketing, and thread sealing. These adhesives help manufacturers avoid unnecessary machining of a wide range of mechanical components during MRO.

- The recent shift from Internal Combustion Engines to electric vehicles is driving innovation in automation technologies. Anaerobic adhesives replace mechanical fasteners as they may accommodate movements caused by thermal expansion and are not susceptible to corrosion.

- Adhesives are also preferred over conventional joining methods as they can prevent contact corrosion and provide impact resistance that is essential for withstanding the high dynamic forces of electric motors.

- The major automakers globally have announced plans to accelerate their electric vehicle future by developing new product lines and converting existing manufacturing facilities. For example:

- Toyota announced the roll-out of 30 Battery Electric Vehicles (BEV) models by 2030.

- Volvo is committed to becoming a fully electric car company by 2030.

- General Motors aims for 30 EV models and an installed production capacity of 1 million units in North America by 2025.

- In 2021, globally, 80.14 million automobile units were produced. This was an increase of 3% compared to 2020. The production of automobiles in Europe reduced by 4% compared to 2020, to 16.33 million units. The production increased by 3% compared to 2020 in America to 16.15 million units.

- The Asian-Pacific region witnessed a growth of 6% in 2021 compared to 2020 to 46.73 million units, while Africa witnessed a significant growth of 16% in 2021 compared to 2020 to reach 0.93 million units.

- In 2022, the joint venture company GAC Honda started the construction of a new car plant in Guangzhou, China. The plant is expected to have a capacity to produce 120,000 electric vehicles per year and is expected to start production by 2024. The investment amount is expected to be CNY 3.49 billion (~USD 0.5 billion).

- Such trends are driving the market for anaerobic adhesives.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific dominates the market owing to various emerging markets in the region, specifically in countries like China and India.

- China is the largest manufacturer of automobiles globally. In 2021, according to the OICA, the automotive production in the country reached 26.08 million, which increased by 3%, compared to 25.23 million vehicles produced in 2020.

- A growth of 106% in battery-plugged-in electric vehicles was witnessed in November 2021 compared to the same period in 2020. The country's sales of electric vehicles reached around 413,094 units in November 2021. In addition, the market share also increased to 19%, including 15% of all-electric and 4% of plug-in hybrid cars.

- China is also one of the largest aircraft manufacturers and one of the largest markets for domestic air passengers. Moreover, the country's aircraft parts and assembly manufacturing sector has been growing rapidly, with over 200 small aircraft parts manufacturers increasing the usage and demand for anaerobic adhesives. According to the Boeing Commercial Outlook 2021-2040, in China, around 8,700 new deliveries will be made by 2040, with a market service value of USD 1,800 billion. Owing to such new deliveries in the country, the demand for the market studied is likely to rise.

- Furthermore, in India, according to OICA, around 43,99,112 vehicles were produced in 2021, which increased by 30% compared to 3,381,819 units manufactured in 2020.

- In the aerospace sector, according to the India Brand Equity Foundation (IBEF), the country's aviation industry is expected to witness INR 35,000 crore (~USD 4.99 billion) investment in the next four years. The country is projected to have a demand for 2,100 aircraft over the next two decades, amounting to over USD 290 billion in sales. Owing to these factors, the demand for anaerobic adhesives from the aerospace sector is expected to rise in the future.

- India is expected to become the global fifth-largest consumer electronics and appliances industry by 2025. Additionally, in India, technology transitions, such as the rollout of 4G/LTE networks and IoT (Internet of Things), are driving the adoption of electronic products. Initiatives, such as 'Digital India' and 'Smart City' projects, raised the demand for IoT in the country.

- India's huge construction sector is expected to become the global third-largest construction market by 2022. Various policies implemented by the Indian government, such as the Smart Cities project, Housing for all by 2022, etc., are expected to bring the needed impetus to the slowing construction industry. For instance, in the Pradhanmantri Awas Yojana, the Indian government has decided to provide interest subvention of 3% and 4% for loans of up to INR 12 lakhs (~USD 14.55 thousand) and INR 9 lakhs (USD 10.92 thousand), respectively, for the lower strata of society concerning buying and building homes.

- Overall, all such factors will affect the demand for anaerobic adhesives in the region over the forecast period.

Anaerobic Adhesives Industry Overview

The global anaerobic adhesives market is semi-consolidated, with various global and domestic players across different regions. However, the top five players in the market control a majority share of the global market. Key players in the anaerobic adhesives market include Henkel AG & Co. KGaA, 3M, H. B. Fuller Company, Kisling AG, and ThreeBond Holdings Co., Ltd, among others ( not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Recovering Automotive Industry

- 4.1.2 Increasing Demand From The Electrical And Electronics Industries

- 4.2 Restraints

- 4.2.1 High Cost Of Anaerobic Adhesives

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products And Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Threadlockers

- 5.1.2 Thread Sealants

- 5.1.3 Retaining Compound

- 5.1.4 Gasket Sealants

- 5.2 End-user Industry

- 5.2.1 Automotive and Transportation

- 5.2.2 Electrical and Electronics

- 5.2.3 Industrial

- 5.2.4 Building and Construction

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Anabond Limited

- 6.4.3 Asec Co., Ltd

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG and Co. KGaA

- 6.4.6 Hi-Bond Chemicals

- 6.4.7 Kisling AG

- 6.4.8 Krylex (Chemence)

- 6.4.9 Metlok Private Limited

- 6.4.10 Novachem Corporation ltd

- 6.4.11 Parson Adhesives, Inc.

- 6.4.12 Permabond LLC.

- 6.4.13 ThreeBond Holdings Co., Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Research And Development and Usage of Bio-based Raw Materials

- 7.2 Growing Prominence in Renewable Energy Market

厭氧黏合劑市場-2026-2032年全球市場預測

厭氧黏合劑市場-2026-2032年全球市場預測 厭氧黏合劑市場規模、佔有率、成長、全球產業分析、區域趨勢及2026年至2034年預測

厭氧黏合劑市場規模、佔有率、成長、全球產業分析、區域趨勢及2026年至2034年預測 厭氧黏合劑市場分析及預測(至2035年):類型、產品、應用、技術、最終用戶、形態、材料類型、部署形式、製程、安裝類型

厭氧黏合劑市場分析及預測(至2035年):類型、產品、應用、技術、最終用戶、形態、材料類型、部署形式、製程、安裝類型 厭氧黏合劑市場規模、佔有率和成長分析(按產品、黏合劑類型、基材、最終用戶和地區分類)—產業預測(2026-2033 年)

厭氧黏合劑市場規模、佔有率和成長分析(按產品、黏合劑類型、基材、最終用戶和地區分類)—產業預測(2026-2033 年) 厭氧膠黏劑市場-全球產業規模、佔有率、趨勢、機會及預測,按膠黏劑類型、基材類型、應用、最終用戶、地區及競爭格局細分,2020-2030 年厭氧膠全球市場規模:依產品、基材、最終用戶和地區分類的範圍和預測

厭氧膠黏劑市場-全球產業規模、佔有率、趨勢、機會及預測,按膠黏劑類型、基材類型、應用、最終用戶、地區及競爭格局細分,2020-2030 年厭氧膠全球市場規模:依產品、基材、最終用戶和地區分類的範圍和預測 厭氧膠黏劑市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

厭氧膠黏劑市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 厭氧黏合劑市場報告:趨勢、預測和競爭分析(至 2030 年)

厭氧黏合劑市場報告:趨勢、預測和競爭分析(至 2030 年)