|

市場調查報告書

商品編碼

1689759

抗輻射電子產品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Radiation Hardened Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

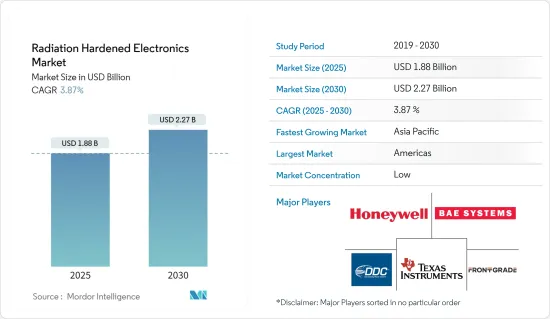

預計 2025 年抗輻射電子產品市場規模將達到 18.8 億美元,到 2030 年預計將達到 22.7 億美元,預測期內(2025-2030 年)的複合年成長率為 3.87%。

關鍵亮點

- 抗輻射電子設備旨在承受極端輻射暴露,對於情報、監視和偵察 (ISR) 系統至關重要。監控、情報收集和邊境管制等安全措施的需求不斷成長,推動了對這些專用電子設備的需求。在高輻射環境中,電子設備的損壞會對安全性構成威脅,因此適當的電源管理對於輻射固化材料至關重要。因此,在這樣的設施中,可靠的、抗輻射的電源管理系統至關重要。

- 抗輻射電子產品在太空產業的廣泛使用對市場成長做出了重大貢獻。例如,根據衛星工業協會的數據,預計2022年全球太空經濟將創造3,840億美元的收益。而且,截至2022年,大約有7,316顆活躍衛星繞地球運行,與前一年同期比較增加了51%,在過去五年增加了321%。

- 軌道衛星暴露在太空環境中典型的高能量帶電粒子和電磁輻射下。衛星受到的輻射水平取決於它們與地球的距離,位於熱層內的低軌道衛星更容易受到紫外線的照射,這會影響電子材料的分子組成。

- 在核能發電,電氣和電子系統暴露在高能量輻射下,這會嚴重影響其功能和整體安全。核能發電中的電離輻射會產生電子空穴對,進而改變電晶體參數並造成破壞。

- 此外,這種輻射也會在電路之間造成漏電流。因此,安裝適當屏蔽的防輻射電氣/電子系統對於系統設計人員至關重要,這是推動市場成長的關鍵因素。

- 儘管各行各業對抗輻射電子元件的需求不斷成長,但市場仍面臨設計和開發成本上升的挑戰。製造能夠承受惡劣操作條件的電子元件需要特殊的設計考慮,這會增加開發成本。此外,嚴格的測試對於確保產品可靠性至關重要,這進一步增加了抗輻射電子產品的成本。

抗輻射電子產品市場趨勢

核能發電廠大幅成長

- 隨著核能發電廠管理人員擴大部署抗輻射電子設備來改善訊號完整性、提高核子反應爐安全性和效率並減少因輻射引起的工廠設備性能下降,核電廠對抗輻射劣化設備的需求也日益增加。

- 事實證明,抗輻射(rad-hard)電子設備的整合對於核能感測和測量至關重要。將先進的感測器和相關電子設備更靠近核子反應爐核心有望提高訊號的精度、準確性和保真度,最佳化核子反應爐的控制和運作。這項進步使得能源生產過程更加安全、有效率。

- 由於核能設施嚴重依賴電子系統,因此非常需要能夠承受大量輻射的設備。在核能發電廠中,使用抗輻射電子設備進行無線監控至關重要。這些電子設備在核能發電廠調查中也扮演關鍵角色。這在事故發生後的危急情況下或輻射水平極高的地區通訊基礎設施故障的情況下尤其重要。

- 由於開發中地區投資的增加,預計在可預見的未來,全球運作中的核子反應爐數量仍將保持相當水準。例如,根據世界核能協會 (EIA) 和核能總署(IAEA) 的資料,2022 年全球共有 411 座核子反應爐在運作,到 2023 年 5 月這一數字將躍升至 436 座。因此,對核能發電廠的持續投資將推動研究市場的機會。

- 電磁輻射和熱輻射是發電和配電基礎設施中常見的現象,增加了常見電子元件故障的可能性。因此,由於迫切需要確保在如此惡劣的條件下具有穩健的性能,預計預測期內抗輻射電子產品的採用將會增加。

- 核能發電技術的應用不僅在核能發電廠,還在核能等各個領域推廣。近年來出現的幾個新型核能計劃預計將維持並推動所研究市場進一步的機會。

亞太地區預計將經歷強勁成長

- 民用航太計劃的興起推動了亞太地區抗輻射電子元件市場的成長。近期,我國在FPGA、CPU等航太核心積體電路研發方面取得重大進展,這些積體電路正應用於載人航太、月球探勘等重大航太計劃。

- 依上述摘要,中國明確2023年將大幅加強國家航太科技活動,包括天舟六號貨運太空船、神舟十六號、神舟十七號等大型任務,並進一步加強天宮太空站活動。今年,中國航太也將加速新一代商用遠端監測衛星建設,並抓緊進行發射任務。同時,北斗三號導航衛星系統也將發射三顆備援衛星。

- 2023年,中國將繼續開發和研究抗輻射技術。中國致力於增加抗輻射晶片的本土產量。透過將 AI/ML 功能與機載抗輻射晶片結合起來,空間儀器可以執行全方位的高級分析,包括影像識別、影像分類、自動決策和及時行動。

- 此外,該地區半導體產業的興起也促進了市場的成長。中國正在尋求軍事和國防領域的本土化,以促進競爭和創新,進一步加強軍事準備,並降低與對外依賴相關的風險。半導體對國內安全的重要性不言而喻。

- 中國強調安全與微電子之間的關係基於四個理由:強大的晶片產業將有助於解放軍實現現代化,並提高其發動常規戰爭的能力。解放軍可以利用本土先進的半導體技術發動資訊戰,增強其發動非常規戰爭的能力;就防禦性資訊戰而言,強大的國內產業可以減輕依賴不可靠的外國關鍵半導體供應的風險。中國認知到半導體的雙重用途特性以及在軍事系統中使用商用現貨(COTS)產品的附帶趨勢,正在將其新興的商用晶片工業基礎整合到軍事應對措施中。

- 此外,還可以製造能夠承受核子反應爐中的高溫和輻射水平的抗輻射電子產品,從而對整體銷售產生積極影響。根據世界核能協會的數據,2022年全球在建核子反應爐數量中,亞洲佔39座。 2021-2023年期間,印度的核能發電總裝置容量約為6.8吉瓦。

抗輻射電子產品市場概述

抗輻射電子產品市場主要由霍尼韋爾國際公司、BAE 系統公司、德州儀器、數據設備公司和 Frontgrade Technologies 等主要參與者瓜分。這些公司正在採取聯盟和收購等策略來加強產品系列建立持久的競爭優勢。

- 2023 年 8 月,Frontgrade Technologies 完成對 Aethercom 的收購,後者是一家專門從事高功率射頻 (RF) 固態功率放大器、發射和接收模組以及高功率RF 開關的公司。此次收購將使 Frontgrade Technologies 能夠為航太和國防領域的客戶提供量身定做的全面、整合、承包解決方案。

- 2023年2月,德州儀器與Teledyne e2v合作開發抗輻射DDR4模組化平台。該舉措旨在幫助衛星OEM透過減少時間和工程工作量來最佳化其系統開發流程。硬體包括經過現場驗證的 Teledyne e2v DDR4T0xG72 DDR4 記憶體模組(容量為 4GB/8GB),並輔以 TI 的 TPS7H3301-SP DDR 終端低壓差 (LDO) 穩壓器,以確保 DDR4 模組的穩定供應。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 抗輻射加固部件的原料分析

第5章市場動態

- 市場促進因素

- 衛星發射和太空探勘活動增加

- 抗輻射電子設備在電源管理和核能環境中的應用日益廣泛

- 市場挑戰/限制

- 設計和開發成本高

第6章市場區隔

- 按最終用戶

- 宇宙

- 航太與國防

- 核能發電廠

- 按組件

- 離散的

- 感應器

- 積體電路

- 微控制器和微處理器

- 記憶

- 按地區

- 美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 供應商排名分析

- 公司簡介

- Honeywell International Inc.

- BAE Systems PLC

- Texas Instruments

- Data Device Corporation

- Frontgrade Technologies

- STMicroelectronics International NV

- Infineon Technologies AG

- Microchip Technology Inc.

- Micropac Industries Inc.

- Renesas Electronic Corporation

- Solid State Devices Inc.

- Advanced Micro Devices, Inc.

- Everspin Technologies Inc.

- Vorago Technologies

第8章 市場機會與未來趨勢

The Radiation Hardened Electronics Market size is estimated at USD 1.88 billion in 2025, and is expected to reach USD 2.27 billion by 2030, at a CAGR of 3.87% during the forecast period (2025-2030).

Key Highlights

- Radiation-hardened electronics, designed to withstand extreme radiation exposures, are integral to Intelligence, Surveillance, and Reconnaissance (ISR) systems. The increased demand for security measures like monitoring, information collection, and border control is driving the need for these specialized electronics. In high radiation environments, proper power management is crucial for radiation-hardened materials, as any electronic damage can pose safety hazards. Thus, reliable radiation-hardened power management systems are essential in such facilities.

- The space industry extensively employs radiation-hardened electronics, contributing significantly to the market's growth. For example, in 2022, the global space economy generated USD 384 billion in revenue, according to the Satellite Industry Association. Additionally, as of 2022, approximately 7,316 active satellites were orbiting the Earth, marking a 51% increase from the previous year and a 321% increase over the past five years.

- Satellites in orbit face substantial exposure to highly energetic charged particles and electromagnetic radiation unique to the space environment. The radiation levels they encounter depend on their distance from Earth; satellites in low earth orbit, situated within the thermosphere, are more exposed to UV radiation, potentially impacting the molecular composition of electronic materials.

- Inside nuclear power plants, electrical and electronic systems are subjected to high-energy radiation that can severely affect their functionality and overall safety. Ionizing radiation within these plants creates electron-hole pairs, altering transistor parameters and potentially causing their destruction.

- Additionally, this radiation can induce leakage currents between circuits. Therefore, installing radiation-hardened electrical/electronic systems with proper shielding is critical for system designers, a key factor driving market growth.

- Despite increasing demand for radiation-hardened electronic components across various industries, the market faces challenges due to higher design and development costs. Specific design considerations are necessary to create electronics that can withstand harsh operating conditions, contributing to increased development costs. Furthermore, stringent testing is essential to ensure product reliability, further elevating the cost of radiation-hardened electronics.

Radiation Hardened Electronics Market Trends

Nuclear Power Plants to Witness Significant Growth

- The demand for radiation-hardened electronics within nuclear power plants is on the rise as facility managers increasingly deploy these specialized components to enhance signal integrity, bolster the safety and efficiency of nuclear reactors, and mitigate radiation-induced degradation of plant equipment.

- The integration of radiation-hardened (rad-hard) electronics has proven instrumental in nuclear sensing and instrumentation. Placing advanced sensors and associated electronics closer to reactor cores holds promise for optimizing reactor control and operation by ensuring heightened signal accuracy, precision, and fidelity. This advancement translates into safer and more efficient energy production processes.

- Given the extensive reliance on electronic systems within nuclear facilities, there's a crucial need for devices capable of withstanding substantial radiation exposure. Wireless monitoring in nuclear power plants, facilitated by radiation-hardened electronics, is paramount. These electronics also serve a critical role in surveying nuclear power plants, especially in scenarios where communication infrastructure fails during critical post-accident situations or in areas with exceedingly high radiation fields.

- The number of operational nuclear reactors worldwide is expected to maintain a significant presence in the foreseeable future, driven by increasing investments in developing regions. For instance, data from the World Nuclear Association, EIA, and the International Atomic Energy Agency (IAEA) indicated 411 operational nuclear reactors globally in 2022, a figure that surged to 436 by May 2023. Consequently, the continued investments in nuclear power plants are poised to fuel opportunities within the studied market.

- Electromagnetic and thermal radiation represent common occurrences in electricity generation and distribution infrastructures, heightening the susceptibility of general electronic components to malfunction. Consequently, the anticipated growth in the adoption of radiation-hardened electronics during the forecast period is driven by the imperative to ensure robust performance under such demanding conditions.

- Beyond nuclear power plants, the adoption of nuclear energy generation technology is expanding into various sectors, including nuclear submarines. The emergence of several new nuclear-powered submarine projects in recent years is expected to sustain and drive further opportunities within the studied market.

Asia Pacific is Expected to Witness Significant Growth

- Due to a growing number of commercial space projects, the market for radiation-hardened electronic components is driving market growth in the Asia Pacific region. In recent years, China has made significant progress in developing several aerospace core integrated circuits, including FPGA and CPU, which major aerospace projects like human spaceflight and moon exploration have utilized.

- Adhering to the above synopsis, China revealed that the country's space science and technology activities will significantly boost in 2023, including big-ticket missions like the Tianzhou-6 cargo craft, the Shenzhou-16 and the Shenzhou-17 flight missions to solidify its Tiangong space station activities further. The corporation will also take steps to speed up the construction of a new generation of commercial remote monitoring satellites this year and launch these missions. Meanwhile, the BeiDou-3 Navigation Satellite System will witness the launch of three backup satellites.

- China will continue developing and researching radiation-hardened technologies in 2023. It has undertaken to increase the local production of radiation-hardened chips. Space equipment could enable itself to perform all advanced analytics, such as image recognition, picture classification, automated decisions, and timely actions, by incorporating AI/ML functionality in conjunction with radiation-hardened chips on board.

- Moreover, the flourishing semiconductor industry in the region is another factor contributing to market growth. China is trying to indigenize the military and defense sector to promote its competitiveness and technology innovation, further strengthening the military and mitigating risks related to foreign dependence. There is an obvious importance of semiconductors for domestic security.

- China's emphasis on the relationship between security and microelectronics is predicated on four arguments: a strong chip industry will help modernize the PLA and enhance its ability to conduct conventional warfare; the PLA can wage information warfare (IW) by exploiting home-grown advanced semiconductor technologies that enhance its ability to wage unconventional war; as regards defensive IW, a robust indigenous industry can mitigate the risks of dependence on unreliable foreign supplies of critical semiconductors; and China recognizes semiconductors' dual-use nature and the trend of spin-on in its policy of using commercial off-the-shelf (COTS) items in military systems to integrate its rising commercial chip industrial base into its military counterpart.

- Furthermore, it is possible to manufacture radiation-hardened electronics that can endure high temperatures and radiation levels found in nuclear reactors, which have a favorable impact on their total sales. According to the World Nuclear Association, in 2022, Asia accounted for 39 units in the number of reactors under construction worldwide. India's total nuclear power capacity reached about 6.8 gigawatts of electricity from 2021 to 2023.

Radiation Hardened Electronics Market Overview

The radiation-hardened electronics market showcases fragmentation with major players like Honeywell International Inc., BAE Systems PLC, Texas Instruments, Data Device Corporation, and Frontgrade Technologies. These entities employ strategies such as partnerships and acquisitions to fortify their product portfolios and establish enduring competitive edges.

- In August 2023, Frontgrade Technologies finalized its acquisition of Aethercomm, a company specializing in high-power radio frequency (RF) solid-state power amplifiers, transmit/receive modules, and high-power RF switches. This acquisition positions Frontgrade Technologies to offer a comprehensive, integrated, and turnkey solution tailored for aerospace and defense clientele.

- Another notable collaboration occurred in February 2023 between Texas Instruments and Teledyne e2v, focusing on a novel radiation-tolerant DDR4 modular platform. This initiative aims to assist satellite OEMs in optimizing their system development process by reducing time and engineering efforts. The hardware comprises a field-proven 4GB/8GB capacity DDR4T0xG72 DDR4 memory module from Teledyne e2v, complemented by a TI TPS7H3301-SP DDR termination low drop-out (LDO) voltage regulator, ensuring a stable supply for the DDR4 module.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Raw Material Analysis for Radiation-Hardened Components

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Instances of Satellite Launches and Space Exploration Activities

- 5.1.2 Growing Adoption of Radiation Hardened Electronics in Power Management and Nuclear Environment

- 5.2 Market Challenges/Restraints

- 5.2.1 High Designing and Development Cost

6 MARKET SEGMENTATION

- 6.1 By End-user

- 6.1.1 Space

- 6.1.2 Aerospace and Defense

- 6.1.3 Nuclear Power Plants

- 6.2 By Component

- 6.2.1 Discrete

- 6.2.2 Sensors

- 6.2.3 Integrated Circuit

- 6.2.4 Microcontrollers and Microprocessors

- 6.2.5 Memory

- 6.3 By Geography

- 6.3.1 Americas

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Ranking Analysis

- 7.2 Company Profiles

- 7.2.1 Honeywell International Inc.

- 7.2.2 BAE Systems PLC

- 7.2.3 Texas Instruments

- 7.2.4 Data Device Corporation

- 7.2.5 Frontgrade Technologies

- 7.2.6 STMicroelectronics International NV

- 7.2.7 Infineon Technologies AG

- 7.2.8 Microchip Technology Inc.

- 7.2.9 Micropac Industries Inc.

- 7.2.10 Renesas Electronic Corporation

- 7.2.11 Solid State Devices Inc.

- 7.2.12 Advanced Micro Devices, Inc.

- 7.2.13 Everspin Technologies Inc.

- 7.2.14 Vorago Technologies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年抗輻射電子產品全球市場報告

2025年抗輻射電子產品全球市場報告 日本抗輻射電子產品市場報告(按產品類型、材料類型、技術(按設計抗輻射、按工藝抗輻射、按軟體抗輻射)、組件類型、應用和地區)2025 年至 2033 年

日本抗輻射電子產品市場報告(按產品類型、材料類型、技術(按設計抗輻射、按工藝抗輻射、按軟體抗輻射)、組件類型、應用和地區)2025 年至 2033 年 耐放射線強化電子產品市場,規模,佔有率,產業分析報告:各產品,各零件,各製造技術,各用途,各地區,2025年~2034年的市場預測

耐放射線強化電子產品市場,規模,佔有率,產業分析報告:各產品,各零件,各製造技術,各用途,各地區,2025年~2034年的市場預測 耐輻射 FPGA 市場 - 全球及區域分析:按應用、類型、材料、製造技術、運作頻率和國家 - 分析與預測(2024 年至 2034 年)

耐輻射 FPGA 市場 - 全球及區域分析:按應用、類型、材料、製造技術、運作頻率和國家 - 分析與預測(2024 年至 2034 年) 輻射固化電子產品市場(按產品、製造技術、材料類型和應用)—2025 年至 2030 年全球預測

輻射固化電子產品市場(按產品、製造技術、材料類型和應用)—2025 年至 2030 年全球預測 抗輻射電子產品市場報告:2031 年趨勢、預測與競爭分析2025 年至 2033 年抗輻射電子產品市場報告,按產品類型、材料類型、技術(按設計抗輻射、按工藝抗輻射、按軟體抗輻射)、組件類型、應用和地區分類

抗輻射電子產品市場報告:2031 年趨勢、預測與競爭分析2025 年至 2033 年抗輻射電子產品市場報告,按產品類型、材料類型、技術(按設計抗輻射、按工藝抗輻射、按軟體抗輻射)、組件類型、應用和地區分類 抗輻射電子產品的全球市場:各零件,各用途,各地區,範圍及預測太空抗輻射電子市場:依製造技術、零件分類 - 全球預測 2025-2030

抗輻射電子產品的全球市場:各零件,各用途,各地區,範圍及預測太空抗輻射電子市場:依製造技術、零件分類 - 全球預測 2025-2030 2024-2028 年全球抗輻射電子產品市場

2024-2028 年全球抗輻射電子產品市場