|

市場調查報告書

商品編碼

1687937

生產印表機:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Production Printer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

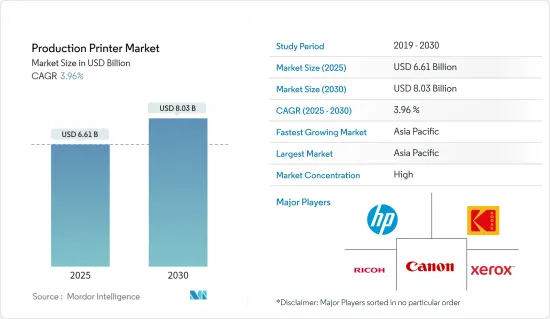

預計 2025 年生產印表機市場規模為 66.1 億美元,到 2030 年將達到 80.3 億美元,預測期內(2025-2030 年)的複合年成長率為 3.96%。

關鍵亮點

- 包裝應用的成長推動了市場擴張:生產印表機市場正在經歷顯著成長,主要由包裝領域推動。 2022年,包裝應用佔據43.7%的市場佔有率。這是因為品牌擁有者越來越重視使用創意包裝來吸引消費者的注意。 2022年生產印表機市場中包裝應用的市場規模預計為25.306億美元,2023年至2028年的複合年成長率為4.35%,到2028年將達到32.972億美元。

- 電子商務熱潮:電子商務的興起刺激了對創新包裝解決方案的需求,產品製造商轉向數位印刷,為目標消費群組訂製包裝。

- 折疊紙盒:對設計、永續性和數位印刷的投資使折疊紙盒越來越受歡迎,尤其是在食品行業。

- 菸草、藥品和酒類包裝:動態法規和防偽措施正在推動這些產品對高品質印刷的需求

- 高效能噴墨印表機推動市場成長:高效能噴墨印表機在市場擴張中發揮關鍵作用,噴墨生產領域的市場規模預計在 2022 年達到 50.813 億美元。到 2028 年,該領域預計將成長到 64.567 億美元,實現 3.92% 的複合年成長率。噴墨技術因其速度、客製化選項和效率而受到青睞,可以滿足現代印刷生產需求。

- 主導參與企業:全錄、佳能、理光、惠普和利盟透過不斷創新提升品質和可靠性,引領噴墨印表機市場。

- 最新發布的產品:Canon的 ProStream 3,000 系列(2023 年 2 月發布)提供具有膠印品質的高速工業印刷。 Markem-Imaje 的新款 9750+ 噴墨印表機(將於 2023 年 4 月推出)可使用染料和顏料墨水進行進階編碼。

- 市場細分與區域動態:生產印表機市場根據類型、生產方法、技術和地區進行細分。連續進紙印表機在 2022 年佔據了 95.6% 的市場佔有率,被證明是一種經濟高效的大量列印解決方案。按地區來看,亞太地區佔44.9%的市佔率。

- 亞太優勢:印度、印尼、越南等新興市場成長強勁,為該地區整體市場領先地位做出貢獻。

- 美國市場趨勢:2022 年美國市場價值為 13.762 億美元,預計到 2028 年將達到 17.139 億美元,由於支持商業印刷的有利政策,複合年成長率為 3.57%。

- 競爭格局與技術進步:生產印表機市場高度整合,全錄、惠普、理光和佳能等主要參與者在市場上佔有重要地位。

- 全錄與惠普的創新:全錄的產品組合包括 IRIDESSE PRODUCTION PRESS 等數位印刷機,而惠普的 Designjet Z6800 在照片製作領域處於領先地位。為了保持競爭力,公司也正在投資雲端技術和人工智慧解決方案。

生產印表機市場趨勢

單色印表機佔據生產型印表機市場的主導地位

2022 年單色市場價值為 36.378 億美元,預計到 2028 年將成長至 45.591 億美元,複合年成長率為 3.68%。推動這一成長的是單色印表機的成本效益和速度,這在不需要彩色列印的大批量列印環境中至關重要。

- 經濟高效:單色印表機具有更快的列印速度和更低的營運成本,使其成為注重大批量輸出的辦公室和行業的理想選擇。

- 技術進步:佳能的 varioPRINT 140 QUARTZ (2024) 和Konica Minolta的 bizhub 950i 和 850i (2024) 為小型印刷廠提供了處理生產高峰和維持營運彈性的工具。

- 主要應用:單色印刷對於圖書出版、使用手冊和交易表格等領域至關重要,這些領域需要以最低的成本實現一致、大量的產出。

亞太地區:生產型印表機市場的成長引擎

亞太地區正成為生產型印表機的最大市場,2022 年的市場佔有率為 44.9%。預計該地區將從 2022 年的 26.019 億美元成長到 2028 年的 33.796 億美元,複合年成長率為 4.30%。

- 中國佔據領先地位 到 2022 年,中國將以 53.39% 的佔有率主導區域市場,而印度是成長最快的國家,預計複合年成長率為 4.38%。

- 行業多樣性:從食品到家用電子電器等廣泛的行業都促進了該地區對印刷解決方案的需求不斷成長。

- 創新:富士軟片商業創新公司等公司不斷透過 Revorias Press EC1100 和 Revorias Press SC180/SC170 等型號突破技術界限,提供高品質的生產力解決方案。

生產印表機市場概覽

全球參與企業主導整合市場:生產印表機市場持續整合,全錄、惠普、Canon和Ricoh等全球大型企業引領市場。這些公司利用其廣泛的產品系列、創新能力和財務實力來保持其市場主導地位。

進入門檻高:由於生產印表機行業大型企業的主導地位以及高昂的開發成本,新參與企業面臨巨大的挑戰。

端到端解決方案:市場領導者提供整合硬體、軟體和服務的綜合產品,以滿足各領域的廣泛客戶需求。

創新和全面的解決方案推動領先地位:為了保持競爭力,公司專注於技術創新,尤其是高速噴墨技術、數位印刷和自動化。Canon和惠普透過提供特定細分市場的差異化產品,始終展現出領先地位。

未來策略:主要企業正在探索符合市場永續發展需求的成長機會,例如 3D 列印、人工智慧解決方案和環保技術。向工業和包裝印刷等高成長領域擴張也為我們帶來了戰略優勢。

未來市場成功的策略:成功的公司是那些能夠成功擁抱技術創新以及雲端基礎的列印和數位服務等新市場趨勢的公司。夥伴關係、收購和研發投資將繼續在擴大市場佔有率和技術專長方面發揮核心作用。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業相關人員分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場動態

- 市場促進因素

- 包裝印刷應用的擴大有望推動成長

- 推出高性能噴墨印表機,噴墨印表機銷售增加

- 市場限制

- 數位行銷與線上閱讀的成長

- COVID-19 對生產印表機供應鏈分銷的全球影響

第6章 重大技術投入

- 雲端技術

- 人工智慧

- 網路安全

- 數位服務

第7章市場區隔

- 按類型

- 單色

- 顏色

- 按生產方式

- 切進

- 收藏的動態

- 依技術

- 噴墨

- 碳粉

- 按應用

- 商業的

- 出版

- 包裝

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 其他亞太地區

- 其他

- 北美洲

第8章競爭格局

- 公司簡介

- Xerox Corporation

- Hewlett-Packard Development Company LP

- Ricoh Company Ltd

- Canon Inc.

- Eastman Kodak Company

- Konica Minolta Inc.

- Miyakoshi Printing Machinery Co. Ltd

- Inca Digital Printers Ltd(Dainippon Screen Mfg. Co. Ltd)

第9章投資分析

第10章 市場機會與未來趨勢

The Production Printer Market size is estimated at USD 6.61 billion in 2025, and is expected to reach USD 8.03 billion by 2030, at a CAGR of 3.96% during the forecast period (2025-2030).

Key Highlights

- Growth in Packaging Applications Drives Market Expansion: The Production Printer Market is undergoing significant growth, with the packaging sector being a primary driver. In 2022, packaging applications accounted for 43.7% of the market share. The rising demand for customization in product packaging is pushing this growth, as brand owners increasingly focus on using creative packaging to capture consumer attention. In 2022, the market size for packaging applications in the production printer market was valued at USD 2,530.6 million, and it is projected to reach USD 3,297.2 million by 2028, growing at a CAGR of 4.35% from 2023 to 2028.

- E-commerce boom: The rise in e-commerce is fueling demand for innovative packaging solutions, with product manufacturers using digital printing to customize packaging for targeted consumer groups.

- Folding cartons: Investments in design, sustainability, and digital printing have popularized folding cartons, especially within the food industry.

- Tobacco, pharmaceutical, and alcohol packaging: Dynamic regulations and anti-counterfeiting measures are boosting the demand for high-quality printing on these products.

- High-Performance Inkjet Printers Fuel Market Growth: High-performance inkjet printers play a pivotal role in market expansion, with the inkjet production segment valued at USD 5,081.3 million in 2022. By 2028, this segment is expected to grow to USD 6,456.7 million, achieving a CAGR of 3.92%. Inkjet technology is favored due to its speed, customization options, and efficiency in handling modern print production demands.

- Dominant players: Xerox, Canon, Ricoh, HP, and Lexmark lead the inkjet printer market with continuous innovations that enhance quality and reliability.

- Recent launches: Canon's ProStream 3000 series (launched in February 2023) offers high-speed industrial printing with offset quality. Markem-Imaje's new 9750+ inkjet printer (April 2023) allows for advanced coding using both dye and pigment inks.

- Market Segmentation and Regional Dynamics: The Production Printer Market is divided by type, production method, technology, and geography. Continuous feed printers held 95.6% of the market share in 2022, proving to be a cost-effective solution for high-volume printing. Regionally, the Asia-Pacific area dominated the market with a 44.9% share.

- Asia-Pacific dominance: Emerging markets in India, Indonesia, and Vietnam are showing strong growth, contributing to the region's overall market leadership.

- U.S. market trends: The U.S. market was valued at USD 1,376.2 million in 2022, and is expected to grow at a CAGR of 3.57% to reach USD 1,713.9 million by 2028, driven by favorable policies supporting commercial printing.

- Competitive Landscape and Technological Advancements: The production printer market is highly consolidated, with major players like Xerox, HP, Ricoh, and Canon holding a strong market presence.

- Xerox and HP innovations: Xerox's portfolio includes digital presses like the IRIDESSE PRODUCTION PRESS, while HP's Designjet Z6800 leads in photo production. Companies are also investing in cloud technologies and AI-driven solutions to stay competitive.

Production Printer Market Trends

Monochrome Segment Dominates Production Printer Landscape

The monochrome segment, valued at USD 3,637.8 million in 2022, is expected to grow to USD 4,559.1 million by 2028, representing a CAGR of 3.68%. This growth is driven by the cost-efficiency and speed of monochrome printers, which are crucial for high-volume print environments that do not require color printing.

- Cost-efficiency: Monochrome printers offer faster print speeds and lower operational costs, making them the preferred choice for offices and industries focused on high-volume output.

- Technological advancements: Canon's varioPRINT 140 QUARTZ (2024) and Konica Minolta's bizhub 950i and 850i (2024) provide small-scale print shops with the tools to handle production peaks and maintain operational flexibility.

- Critical applications: Monochrome printing is essential for sectors like book publishing, user manuals, and transactional forms, which require consistent high-volume output at minimal cost.

Asia-Pacific: The Growth Engine of Production Printer Market:

The Asia-Pacific region has emerged as the largest market for production printers, with a 44.9% market share in 2022. The region is expected to grow from USD 2,601.9 million in 2022 to USD 3,379.6 million by 2028, with a CAGR of 4.30%.

- China leads the way: China dominates the regional market with a 53.39% share in 2022, while India is showing rapid growth with a projected CAGR of 4.38%.

- Industrial diversity: The wide range of industries, from food to consumer electronics, contributes to the region's growing demand for printing solutions.

- Innovation: Companies like FUJIFILM Business Innovation Corp. continue to push technological boundaries with models like the Revoria Press EC1100 and Revoria Press SC180/SC170, offering high-quality productivity solutions.

Production Printer Market Overview

Global Players Dominate Consolidated Market: The Production Printer Market remains consolidated, with major global players such as Xerox, HP, Canon, and Ricoh leading the space. These companies leverage their extensive product portfolios, innovation capabilities, and financial resources to maintain market dominance.

High entry barriers: New entrants face significant challenges due to the dominance of large players and high development costs in the production printer industry.

End-to-end solutions: Leaders in the market provide comprehensive offerings that integrate hardware, software, and services, addressing a wide range of customer needs across different sectors.

Innovation and Comprehensive Solutions Drive Leadership: Companies are focusing on innovation, particularly in high-speed inkjet technology, digital printing, and automation, to maintain their competitive edge. Canon and HP have consistently demonstrated leadership by offering differentiated products tailored to specific market segments.

Future strategies: Key players are exploring growth opportunities in 3D printing, AI-powered solutions, and eco-friendly technologies, aligning with market demands for sustainability. Expanding into high-growth areas like industrial and packaging printing also offers strategic advantages.

Strategies for Future Success in the Market: In addition to technological innovation, companies that can successfully tap into emerging market trends, such as cloud-based printing and digital services, are expected to thrive. Partnerships, acquisitions, and R&D investments will remain central to expanding market share and technological expertise.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth of Printing Applications in Packaging is Expected to Drive Growth

- 5.1.2 Increasing Inkjet Sales Due to Introduction of High-performance Inkjet Printers

- 5.2 Market Restraints

- 5.2.1 Growth of Digital Marketing and the Practice of Online Reading

- 5.3 Impact of COVID-19 in Supply Chain Distribution of Production Printer Globally

6 KEY TECHNOLOGY INVESTMENTS

- 6.1 Cloud Technology

- 6.2 Artificial Intelligence

- 6.3 Cyber Security

- 6.4 Digital Services

7 MARKET SEGMENTATION

- 7.1 By Type

- 7.1.1 Monochrome

- 7.1.2 Color

- 7.2 By Production Method

- 7.2.1 Cut Fed

- 7.2.2 Continuous Feed

- 7.3 By Technology

- 7.3.1 Inkjet

- 7.3.2 Toner

- 7.4 By Application

- 7.4.1 Commercial

- 7.4.2 Publishing

- 7.4.3 Packaging

- 7.5 By Geography

- 7.5.1 North America

- 7.5.1.1 United States

- 7.5.1.2 Canada

- 7.5.2 Europe

- 7.5.2.1 Germany

- 7.5.2.2 United Kingdom

- 7.5.2.3 France

- 7.5.2.4 Italy

- 7.5.2.5 Rest of Europe

- 7.5.3 Asia-Pacific

- 7.5.3.1 India

- 7.5.3.2 China

- 7.5.3.3 Japan

- 7.5.3.4 Rest of Asia-Pacific

- 7.5.4 Rest of the World

- 7.5.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Xerox Corporation

- 8.1.2 Hewlett-Packard Development Company LP

- 8.1.3 Ricoh Company Ltd

- 8.1.4 Canon Inc.

- 8.1.5 Eastman Kodak Company

- 8.1.6 Konica Minolta Inc.

- 8.1.7 Miyakoshi Printing Machinery Co. Ltd

- 8.1.8 Inca Digital Printers Ltd (Dainippon Screen Mfg. Co. Ltd)