|

市場調查報告書

商品編碼

1686214

汽車膠帶:市場佔有率分析、產業趨勢與成長預測(2025-2030)Automotive Adhesive Tape - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

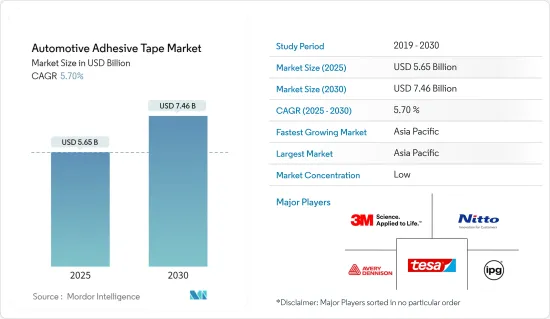

預計2025年汽車膠帶市場規模為56.5億美元,到2030年將達到74.6億美元,預測期間(2025-2030年)的複合年成長率為5.7%。

COVID-19 疫情嚴重影響了汽車膠帶市場,擾亂了供應鏈,導致生產放緩和停頓,並引發景氣衰退。儘管 COVID-19 最初的影響是負面的,但市場預計將在預測期內復甦。

主要亮點

- 由於電動車對輕量化密封解決方案的需求不斷增加,預計預測期內膠帶需求將會成長。此外,膠帶是傳統機械緊固方法的一種有吸引力的替代方案,在電動車製造領域發揮重要作用。

- 電氣化和自動化的不斷發展給汽車製造商帶來了越來越大的挑戰。電動車的高成本是一個可能限制需求成長的挑戰。

- 對耐熱和低VOC汽車膠帶的需求為提高溫度控管效率創造了有利可圖的機會。這與內燃機汽車和電動車相關,也將增加內裝設計的自由度。

- 隨著電動和傳統汽車產量和銷量的不斷成長,亞太地區佔據全球市場佔有率。

汽車膠帶市場趨勢

電動和混合動力汽車中膠帶的使用日益增多

- 膠帶在電動車電池中的應用越來越多,以提高安全性並減輕車輛整體重量。預計在預測期內,用膠帶代替緊固件以改善汽車美觀度的趨勢將推動市場發展。

- 在汽車工業中,膠帶用於將零件固定到車身外部,防止清漆時磨損,並在組裝中提供支撐。膠帶也用於汽車內飾的各種特殊應用。

- 電動車因其運行成本低、駕駛平穩等優勢,在世界各地越來越受歡迎。汽車製造商正在投資透過使用輕量材料(包括複合材料和輕質粘合、連接和緊固解決方案)來提高功率重量比。

- 電動車(EV)是實現全球零碳排放的關鍵一步。許多政府正在支持電動車的生產並幫助投資者建立必要的基礎設施。此外,政府也透過各種補貼支持消費者購買電動車。

- 全球各地多家汽車製造商正在投資電動車。日產汽車、豐田汽車、賓士、特斯拉、現代等紛紛開始生產電動車,為汽車膠帶市場帶來利多。

- 歐盟計劃在 2030 年之前在道路上引入 3000 萬輛電動車,以減少該地區交通運輸部門的排放。各國均根據歐盟計畫採取了各種措施。例如,英國已宣佈2030年禁止內燃機汽車。

- 根據開姆尼茨汽車研究所的數據,預計德國 2022 年將生產近 57 萬輛電動車,2023 年將生產近 100 萬輛。德國已獲得多項電動車投資,電動車產量可能增加。例如,領先的電動車製造商特斯拉計劃將其在德國的生產能力提高一倍。

- 法國新註冊的電動車數量正在增加。預計到2023年9月,法國電動車銷量將增加至34.1萬輛,比2022年同期成長25%。根據媒體報道,特斯拉是法國最大的電動車品牌。

- 根據國際能源總署(IEA)的數據,美國是世界第三大市場。預計2023年第三季電動車銷量將超過30萬輛,較2022年第三季成長近49.8%。此外,美國企業平均燃油經濟性(CAFE)法規旨在2025年將新型和改進型汽車的平均燃油經濟性提高到每加侖54.5英里,從而減少對石油的依賴。

- 根據巴西電動車協會(ABVE)統計,2023年第一季輕型電動車銷量總計1,4787輛,較2022年同期(9,844輛)成長50%,創下該系列車型歷史最高銷量。

- 沙烏地阿拉伯正在大力發展電動車。政府正在推廣電動車以減少碳排放。政府的目標是到 2030 年生產 50 萬輛。

- 此外,電動車在南非越來越受歡迎。根據媒體報道,2022年南非註冊了502輛新的純電動車。

- 預計未來幾年,世界各國的新能源汽車強制規定、各種補貼和燃油經濟法規等政策將推動輕型電動車的需求。這可能會推動汽車生產對膠帶的需求。

亞太地區佔市場主導地位

- 亞太地區是全球最大的電動車生產地區。其次是歐洲和北美洲。中國、印度和日本是亞太地區領先的電動車生產國。

- 預計未來膠帶將成為汽車行業不可或缺的一部分,而且這不僅僅是出於數量的原因。電動汽車電池會產生熱和電壓,需要加以保護以確保使用者的安全。因此,製造商開發了自己的雙面膠帶和薄膜來防止突波。電池可能包裹在耐高溫的不易燃產品中。這反過來又推動了汽車產業對膠帶的需求。

- 根據國際貿易管理局(ITA)的數據,中國仍然是全球最大的汽車市場(按年銷售量和製造產量計算)。預計2025年國內產量將達3,500萬輛。為因應疫情,中國政府推出了促進汽車消費的措施。這些措施包括允許無限制銷售符合中國5.5排放氣體標準的汽車、推廣使用電動車、降低汽車銷售稅、加強平行輸入政策等。預計這項變更將使每年的支出增加約 300 億美元。

- 為了因應汽車產業成長放緩並促進電動車市場的發展,中國政府在 2023 年上半年部分重新運作了這些支持措施。 2021 年 6 月,中華人民共和國政府宣布了針對汽車產業的巨額稅收優惠政策。該計劃將在四年內實施,預計價值 723 億元人民幣(5,200 億美元)。

- 該激勵措施專門用於促進電動和其他環保汽車的銷售。這項稅收減免是中國政府迄今針對汽車業提供的最大規模的減免政策,反映了政府在汽車銷售低迷時期刺激成長的努力。

- 根據國際汽車工業協會(OICA)預測,2022年中國汽車產量將成長3%,從2021年的26,121,712輛增加至2022年的27,026,155輛。

- 印度是一個不斷成長的電動車市場。在印度,電動車和零件製造業蓬勃發展,受到政府32億美元獎勵計畫的支持,共吸引了83億美元的投資。 2023年第三季電動車銷量達371,214輛,較2022年第三季成長40%。

- 日本汽車製造商協會發布的新車註冊資料顯示,2023年9月日本新車市場銷量較上月的395,163輛成長近11%,達到437,493輛。繼八月市場表現積極之後,九月也迎來了強勁成長。日本市場在連續三個月放緩之後,8月開始加速。 8月汽車年銷量達到5.36億輛,較7月的低迷成長了28%。

- 此外,根據日本汽車經銷商協會 (JADA) 的數據,2022 年電動車銷量將會增加,日本將擁有 58,813 輛電池式電動車(BEV),是 2021 年的 2.7 倍。為了刺激對電動車的需求,日本政府繼續為購買新電動車提供補貼,2022 會計年度的補充預算中將提供 700 億日圓(5.01 億美元)的補貼。

- 韓國的電動車市場正在迅速擴張。根據韓國電力交易所預測,2022年電動車銷量預計將達到16萬輛,較2021年成長60%。韓國也正在進行各種與電動車相關的投資。例如,現代汽車於2023年11月開始建造電動車工廠,投資額為15.2億美元。

- 推動市場發展的主要因素是該地區大量的汽車製造廠、低成本勞動力、低廉的原料價格以及不斷成長的城市人口。

- 所有上述因素將在預測期內推動亞太地區對汽車膠帶的需求。

汽車膠帶產業概況

汽車膠帶市場部分整合。主要公司(排名不分先後)包括 3M、Nitto Denko、Tesa SE、IPG 和 AVERY DENNISON CORPORATION。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查結果

- 調查前提

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 電動和混合動力汽車中膠帶的使用日益增多

- 汽車輕量材料的採用

- 其他促進因素

- 限制因素

- 電動車和充電站高成本

- 熱熔膠取代膠帶

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 背襯材料

- 聚對苯二甲酸乙二醇酯(PET)

- 聚氯乙烯(PVC)

- 聚丙烯(PP)

- 紙

- 聚醯胺

- 其他基材(發泡聚苯乙烯、布料等)

- 黏合劑類型

- 環氧樹脂

- 丙烯酸纖維

- 聚氨酯

- 矽膠

- 其他黏合劑類型(橡膠黏合劑、聚酯等)

- 應用

- 外部的

- 內部的

- 動力傳動系統

- 電子產品

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 墨西哥

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- 3M

- American Biltrite Inc.

- Avery Dennison Corporation

- Berry Global Inc.

- Certoplast Technische Klebebander Gmbh

- Coroplast Fritz Muller Gmbh & Co. Kg

- Godson Tapes Private Limited

- IPG

- L&L Products

- Lintec Corporation

- Lohmann Gmbh & Co. Kg

- Nitto Denko Corporation

- Saint-Gobain

- Scapa Group Ltd

- Shurtape Technologies, LLC

- Sika AG

- Tesa SE

- VIBAC Group SPA

第7章 市場機會與未來趨勢

- 汽車膠帶的優勢

- 汽車對耐熱、低VOC膠帶的需求

The Automotive Adhesive Tape Market size is estimated at USD 5.65 billion in 2025, and is expected to reach USD 7.46 billion by 2030, at a CAGR of 5.7% during the forecast period (2025-2030).

The COVID-19 pandemic significantly impacted the automotive adhesive tape market by disrupting the supply chain, causing production to slow and shut down and an economic downturn. While the initial impact of COVID-19 was negative, the market is on a recovery path during the forecast period.

Key Highlights

- The adhesive tapes are anticipated to witness growth due to the rising demand for a lightweight sealing solution in electric vehicles over the forecast period. In addition, adhesive tapes offer an attractive alternative to traditional mechanical fastening methods and play a vital role in the EV manufacturing sector.

- Growing trends of electrification and automation are resulting in rising challenges for automotive manufacturers. The high cost of electric vehicles is a challenge that is likely to restrict the growing demand.

- Demand for heat-resistant and low VOC automotive adhesive tapes creates lucrative opportunities to improve heat management efficiency. It is associated with IC engine cars and electric vehicles, as well as increasing the degree of freedom in vehicle interior design.

- The Asia-Pacific region accounted for the most significant global automotive adhesive tape market share, considering the increasing production and sales of electric vehicles and conventional automobiles.

Automotive Adhesive Tape Market Trends

Rising Use of Adhesive Tapes in Electric and Hybrid Vehicles

- The adhesive tapes are increasingly used in electric vehicle batteries to increase safety and reduce the vehicle's overall weight. The growing replacement of fasteners with adhesive tapes to improve the vehicle's aesthetics is anticipated to drive the market over the forecast period.

- Adhesive tapes are used in the automotive industry to attach parts onto the outer surfaces of a car's body, offering protection against abrasion during varnishing and providing support during assembly. Adhesive tapes also serve a variety of purposes specific to automotive interiors.

- Electric vehicles are gaining popularity across the globe owing to their benefits, such as being cheap to run and smooth to drive. Automotive manufacturers are investing in improving the power-to-weight ratio using lightweight materials, including composites and weight-saving bonding, joining, and fixing solutions.

- Electric vehicles (EVs) are one of the important steps towards zero carbon emission initiatives globally. Many governments are supporting electric production and helping investors set up the necessary infrastructure. Moreover, the governments are also helping consumers through various subsidies to promote the use of electric vehicles.

- Several automotive manufacturers across the globe are investing in electric vehicles. Nissan Motors, Toyota Motor Corporation, Mercedes-Benz, Tesla, Hyundai Motors, etc., started electric vehicle production, benefitting the automotive adhesive tapes market.

- The European Union aimed to introduce 30 million electric vehicles on the road by 2030 to reduce emissions from the transportation sector in the region. Countries implemented different measures in line with the EU plan. For instance, the United Kingdom announced a ban on internal combustion engine vehicles by 2030.

- According to the Chemnitz Automotive Institute, Germany produced nearly 570,000 units in 2022 and is expected to produce nearly 1 million electric vehicles by 2023. Germany received some investments in electric vehicles, which is likely to increase EV production. For instance, Tesla, a leading manufacturer of EVs, is planning to double its production capacity in Germany.

- New electric vehicle registrations are rising in France. Until September 2023, the country's EV sales increased to 341,000 units, indicating 25% growth compared to the same period in 2022. According to media reports, Tesla is the leading EV brand in France.

- According to the International Energy Agency (IEA), the United States is the third largest market in the world. In Q3 2023, the sales of EVs surpassed 300,000 units, which is a nearly 49.8% increase compared to Q3 2022. Furthermore, the Corporate Average Fuel Economy (CAFE) regulations in the United States aim to raise the average fuel efficiency of new cars and vehicles to 54.5 miles per gallon by 2025 to reduce the nation's dependence on oil.

- According to the Brazilian Association of Electric Vehicles (ABVE), the first quarter of 2023 recorded the highest sales in the historical series, with 14,787 light electric vehicles sold, 50% more than the same period in 2022 (9,844).

- Saudi Arabia is focusing on electric vehicles. The government is promoting EVs to reduce carbon emissions. The government aims to manufacture 500,000 units by 2030.

- Furthermore, the electric vehicles are becoming popular in South Africa. In 2022, new 502 battery electric vehicles were registered in South Africa, according to the media reports.

- Policies like new energy vehicle mandates, various subsidies, and fuel economy regulations in countries across the globe are anticipated to drive the demand for lightweight electric vehicles over the coming years. It is likely to propel the demand for adhesive tapes for automotive production.

Asia-Pacific to Dominate the Market

- Asia-Pacific is the largest producer of electric vehicles in the globe. Europe and North America follow it. China, India, and Japan are some of Asia-Pacific's leading electric vehicle-producing countries.

- Adhesive tape is expected to be an essential part of the automotive industry in the future, and not just for volume reasons. The battery of an electric car produces heat and voltage that must be protected to keep the user safe. As a result, manufacturers are developing double-sided adhesive tape and a unique film that prevents power surges. Batteries can be wrapped in nonflammable products that can withstand high temperatures. It, in turn, is significantly promoting the demand for adhesive tapes from the automotive industry.

- As per the International Trade Administration (ITA), China remains the world's largest vehicle market in terms of annual sales volume and manufacturing output. Domestic production is expected to hit 35 million vehicles in 2025. In response to the pandemic, China's government implemented measures to boost automobile consumption. The measures include allowing China 5 5-emission standard vehicles to be sold without restrictions, promoting the use of electric vehicles, reducing car sales tax, and enhancing parallel import policies. The changes are expected to boost consumption by about USD 30 billion annually.

- To address the slow growth of the automotive industry and to promote the EV market, the government of China partially reinvigorated these support measures in the first six months of 2023. In June 2021, the government of the People's Republic of China announced a huge tax incentive package for the automotive industry. The package, which will be implemented over four years, is estimated to amount to CNY 72.3 billion (USD 520 billion).

- The incentives are specifically designed to promote the sale of electric vehicles and other eco-friendly vehicles. It is the most significant tax incentive package ever offered by the Chinese government for the automotive industry and reflects the government's efforts to promote growth amid slow auto sales.

- According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), automotive production in China registered an increase of 3% in 2022, increasing from 26,121,712 units in 2021 to 27,020,615 units in 2022.

- India is a growing market for EVs. In India, EV and component manufacturing is ramping up, supported by the government's USD 3.2 billion incentive program, attracting investments totaling USD 8.3 billion. In the third quarter of 2023, the electric vehicle sales reached 371,214 units, registering a growth of 40% compared to Q3 in 2022.

- In September 2023, Japan's new vehicle market grew by nearly 11% to reach 437.493 units from 395.163 units in the previous month, according to new vehicle registration data published by JAMA. The strong September growth follows a positive market development in August. After slowing for three consecutive months, the Japanese market picked up speed in August. The August sales rate reached an impressive 5,36 million units per year, a 28% increase from the weak July.

- Furthermore, as per the Japan Automobile Dealers Association (JADA), EV sales increased in 2022 to reach 58,813 battery electric vehicles (BEVs) in Japan, 2.7 times more than in 2021. To encourage demand for EVs, the Japanese government continues to offer subsidies for purchases of new EVs with a revised budget of JPY 70 billion ( USD 501 million) for the fiscal year 2022.

- The South Korean EV market is increasing at a fast pace. According to the Korea Power Exchange, EV sales reached 160 thousand units in 2022, an increase of 60% compared to 2021. The country is also receiving various investments related to electric vehicles. For instance, Hyundai Motors initiated an EV plant construction with an investment of USD 1.52 billion in November 2023.

- The market is majorly driven by the availability of low labor at low cost, low raw material prices, and the growing urban population in the region, in addition to many automotive manufacturing plants.

- All the factors above, in turn, boost the demand for automotive adhesive tapes in the Asia-Pacific region during the forecast period.

Automotive Adhesive Tape Industry Overview

The automotive adhesive tape market is partially consolidated in nature. The major players (not in any particular order) include 3M, Nitto Denko Corporation, Tesa SE, IPG, and AVERY DENNISON CORPORATION, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Use of Adhesive Tapes In Electric and Hybrid Vehicles

- 4.1.2 Adoption of Lightweight Materials in Automotive

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of Electric Vehicles and Charging Stations

- 4.2.2 Hot-melt Adhesives are Replacing Adhesive Tapes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Value)

- 5.1 Backing Material

- 5.1.1 Polyethylene Terephthalate (PET)

- 5.1.2 Polyvinyl Chloride (PVC)

- 5.1.3 Polypropylene (PP)

- 5.1.4 Paper

- 5.1.5 Polyamide

- 5.1.6 Other Backing Material (Foam, Cloth, etc.)

- 5.2 Adhesive Type

- 5.2.1 Epoxy

- 5.2.2 Acrylic

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Adhesive Types (Rubber-Based Adhesives, Polyesters, etc.)

- 5.3 Application

- 5.3.1 Exterior

- 5.3.2 Interior

- 5.3.3 Powertrain

- 5.3.4 Electronics

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Mexico

- 5.4.2.3 Canada

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 American Biltrite Inc.

- 6.4.3 Avery Dennison Corporation

- 6.4.4 Berry Global Inc.

- 6.4.5 Certoplast Technische Klebebander Gmbh

- 6.4.6 Coroplast Fritz Muller Gmbh & Co. Kg

- 6.4.7 Godson Tapes Private Limited

- 6.4.8 IPG

- 6.4.9 L&L Products

- 6.4.10 Lintec Corporation

- 6.4.11 Lohmann Gmbh & Co. Kg

- 6.4.12 Nitto Denko Corporation

- 6.4.13 Saint-Gobain

- 6.4.14 Scapa Group Ltd

- 6.4.15 Shurtape Technologies, LLC

- 6.4.16 Sika AG

- 6.4.17 Tesa SE

- 6.4.18 VIBAC Group S.P.A.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Benefits of Automotive Adhesive Tapes

- 7.2 Demand For Heat-resistant and Low VOC Automotive Adhesive Tapes

汽車膠帶市場報告:黏合劑黏合劑類型、化學成分、應用和地區分類(2026-2034 年)

汽車膠帶市場報告:黏合劑黏合劑類型、化學成分、應用和地區分類(2026-2034 年) 汽車用膠帶市場:按膠帶類型、黏合劑類型、黏合技術、應用、最終用途和銷售管道分類——2026-2032年全球市場預測

汽車用膠帶市場:按膠帶類型、黏合劑類型、黏合技術、應用、最終用途和銷售管道分類——2026-2032年全球市場預測 2026年全球汽車膠帶市場報告

2026年全球汽車膠帶市場報告 汽車膠帶市場規模、佔有率及成長分析(黏合劑類型、基材、應用、最終用途和地區分類)-2026-2033年產業預測

汽車膠帶市場規模、佔有率及成長分析(黏合劑類型、基材、應用、最終用途和地區分類)-2026-2033年產業預測 2030 年汽車膠帶市場預測:按類型、樹脂、基材、技術、應用、最終用戶和地區進行的全球分析

2030 年汽車膠帶市場預測:按類型、樹脂、基材、技術、應用、最終用戶和地區進行的全球分析 2024-2028年全球汽車膠帶市場

2024-2028年全球汽車膠帶市場 全球汽車膠帶市場規模研究(按黏合劑類型、膠帶類型、應用、部署和區域預測)2022-2032 年

全球汽車膠帶市場規模研究(按黏合劑類型、膠帶類型、應用、部署和區域預測)2022-2032 年