|

市場調查報告書

商品編碼

1685673

氰化氫-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Hydrogen Cyanide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

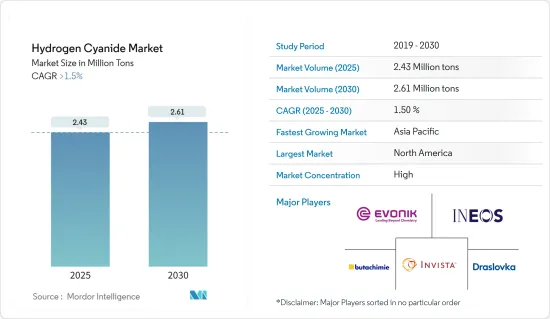

預計 2025 年氫氰酸市場規模為 243 萬噸,2030 年將達到 261 萬噸,預測期間(2025-2030 年)的複合年成長率將超過 1.5%。

產生的氫氰酸大部分用作生產己二腈的原料,而己二腈又用於製造尼龍 66,用於纖維和塑膠生產。己二腈(AND)用於生產六亞甲基二胺(HMDA),其中大部分(約92%)用於製造尼龍6,6纖維和樹脂。

從中期來看,對氰化鈉和氰化鉀的高需求以及在己二腈生產中氰化氫的使用增加是推動市場成長的關鍵因素。

另一方面,氰化氫毒性極強,阻礙了市場成長。

在尚未開發的市場中使用氰化氫生產螯合劑可能會在未來帶來機會。

預計北美將主導全球氰化氫市場,而亞太地區預計將成為預測期內成長最快的市場。

氰化氫市場趨勢

氰化鈉和氰化鉀的應用將成為成長最快的領域

- 氰化氫是氰化鈉和氰化鉀的前驅物,常用於電鍍和銀、金等金屬的開採。

- 在濕式製程中,它是透過用氫氧化鈉中和氰化鈉(NaCN)或氰化氫來生產的。以氣體或液體形式添加氰化氫,並以水溶液形式添加 NaOH,形成 NaCN 水溶液。此外,在 NaCN 水溶液蒸發過程中可能會形成固體NaCN結晶。

- 氰化鉀(KCN)是透過用氫氧化鉀水溶液處理氰化氫,然後在真空下蒸發溶液而生成的。

- 氰化鈉和氰化鉀都是用於各種工業製程的重要化學品,包括黃金提取、電鍍和化學製造。

- 氰化鈉和氰化鉀主要用於從低品位礦石中提取金和銀。

- 氰化鉀和氰化鈉也廣泛用於生產腈和羧酸。

- 根據美國地質調查局的數據,2022年全球黃金產量將達3,100噸。預計到 2022 年,中國金礦產量將達到 330 噸,位居全球首位;其次是澳大利亞,同年產量約 320 噸。

- 估計黃金蘊藏量最多的國家是澳洲、俄羅斯和南非。此外,加拿大採礦業是世界上最大的鉀肥生產國,也是五大黃金生產國之一。加拿大最新的金礦,PureGold 位於安大略省的紅湖礦計劃,預計將於 2021 年 8 月開始商業營運,每年增加 87.8 層黃金。

- 繼俄羅斯入侵烏克蘭之後,化學工業在 2022 年經歷了能源和原料成本上漲、疫情、經濟不確定性和政治動盪的一年,這些因素進一步加劇了本已因疫情而緊張的全球供應鏈的瓶頸。

- 根據BASF發布的2022年報告,預計2023年全球化學品產量(不包括醫藥)將與前一年同期比較增2.0%,與前一年同期比較2.2%。

- 在中國這個全球最大的化學品市場,預計2023年化學品產量成長將略有放緩。 2022年,中國化學品產量增加了5.9%。預計中國經濟的開放將促進國內需求的成長,特別是在消費品和健康與營養領域,從而為該行業的積極成長做出貢獻。

- 考慮到所有這些因素,預計整體市場在預測期內將呈現正成長。

北美佔據市場主導地位

- 根據ITC貿易地圖,美國將在2022年成為最大的氰化氫出口國,出口量約87噸。

- 目前,全國範圍內尚無禁止氰化物產品的重大法規。然而,包括蒙大拿州、科羅拉多和威斯康辛州在內的一些州制定了一些法規,禁止在其境內使用某些氰化物。

- 該地區對氰化氫的需求主要源於以下應用:用於生產尼龍和聚醯胺的己二腈、用於油漆和被覆劑的丙烯酸塑膠的丙酮氰醇、用於回收黃金的氰化鈉和氰化鉀,以及用於農藥和其他農產品的氰尿醯氯。

- 該國是世界主要黃金和白銀生產國之一。根據美國地質調查局的數據,2022 年該國成為世界第五大黃金生產國,總產量約 170 噸。

- 根據白銀協會的數據,2022 年美國白銀產量將位居世界第九,達到 4,110 萬盎司(約 1,165.17 噸),比 2021 年的產量增加 6%。

- 除了上述用途外,該國所研究的市場需求也受到該國農業產業的推動,因為使用氰化氫生產的氰尿醯氯也用於製造殺蟲劑和其他農產品。

- 塑膠產業對丙酮氰醇的需求進一步刺激了市場消費。

- 目前,大量塑膠廢棄物造成環境污染日益嚴重,影響塑膠工業的發展。根據加拿大政府統計,該國每年使用約150億個塑膠購物袋和5,700萬根塑膠吸管。

- 含氫氰酸的化學物質,即氰化鈉和氰化鉀,在金礦和銀礦開採過程中有著重要的應用。

- 據美國地質調查局稱,該國是繼中國、澳洲和俄羅斯之後的第四大黃金生產國,預計 2022 年黃金產量將達到約 220 噸。

- 它也是世界十五大白銀生產國之一。根據白銀協會的數據,政府白銀產量約為 870 萬盎司(246.64 噸),與 2021 年相比下降了約 5%。

- 農業對殺蟲劑和其他化學物質的需求也導致該國氫氰酸消耗量居高不下。

- 農業是加拿大經濟的主要貢獻者。根據加拿大農業和食品部(AAFC)的數據,2022 年,加拿大是世界第五大農業出口國。

- 所有這些趨勢都可能影響預測期內的市場需求。

氰化氫產業概況

全球氰化氫市場已部分整合。主要企業包括(排名不分先後)INVISTA、Evonik Industries、INEOS、Butachimie Chalampe、Drasslok 和 Asahi Kasei。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 氰化鈉和氰化鉀生產需求旺盛

- 己二腈生產中氫氰酸的使用增加

- 限制因素

- 氫氰酸毒性大

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 結構類型

- 液態氰化氫

- 氰化氫氣體

- 應用

- 氰化鈉和氰化鉀

- 己二腈

- 丙酮氰醇

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 馬來西亞

- 泰國

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 俄羅斯

- 土耳其

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率分析(%)**/排名分析

- 主要企業策略

- 公司簡介

- Air Liquide

- Asahi Kasei Corporation

- Ascend Performance Materials

- Butachimie

- Draslovka

- Evonik Industries AG

- Hindusthan Chemicals Company

- INEOS

- INVISTA

- Kuraray Co. Ltd

- Matheson Tri-Gas Inc.

- Sumitomo Chemical Co. Ltd

- Taekwang Industrial Co. Ltd

第7章 市場機會與未來趨勢

The Hydrogen Cyanide Market size is estimated at 2.43 million tons in 2025, and is expected to reach 2.61 million tons by 2030, at a CAGR of greater than 1.5% during the forecast period (2025-2030).

The majority of the hydrogen cyanide manufactured is used as a raw material for adiponitrile production, which is used in producing nylon 66 for fiber and plastic production. Adiponitrile (AND) is used to make hexamethylene diamine (HMDA), the majority of which (approximately 92%) is used to make nylon 6,6 fibers and resins.

Over the medium term, the major factors driving market growth were the high demand for sodium and potassium cyanide and the increasing use of hydrogen cyanide in producing adiponitrile.

On the flip side, the highly toxic nature of hydrogen cyanide hampers the market's growth studied.

Its use in the production of chelating agents in untapped markets is likely to present opportunities in the future.

North America is expected to dominate the global hydrogen cyanide market, while the Asia-Pacific region is expected to be the fastest-growing market during the forecast period.

Hydrogen Cyanide Market Trends

Sodium and Potassium Cyanide Application to be the Fastest Growing Segment

- Hydrogen cyanide, as a precursor of sodium cyanide and potassium cyanide, is commonly used for electroplating and mining of metals such as silver and gold.

- The wet process produces sodium cyanide (NaCN) or the neutralization of hydrogen cyanide with sodium hydroxide. The HCN is added both in the form of a gas or liquid, and NaOH is added as an aqueous solution to form an aqueous NaCN solution. Furthermore, solid NaCN crystals can be formed during evaporation of the aqueous NaCN solution.

- Potassium cyanide (KCN) is formed by the treatment of hydrogen cyanide with an aqueous potassium hydroxide solution, followed by the vacuum evaporation of the solution.

- Both sodium cyanide and potassium cyanide are important chemicals used in various industrial processes, including gold extraction, electroplating, and chemical manufacturing.

- Sodium cyanide and potassium cyanide are majorly used in the extraction of gold and silver from low-grade ores.

- Potassium cyanide and sodium cyanide are also widely used for the production of nitriles and carboxylic acids.

- According to the US Geological Survey, in 2022, global gold production reached 3,100 metric tons. China led global gold mine production, with an estimated 330 metric tons produced in 2022, followed by Australia, producing about 320 metric tons in the same year.

- The countries with the largest estimated gold reserves are Australia, Russia, and South Africa. Furthermore, Canada's mining industry is the world's biggest producer of potash and is in the top five producers of gold. The Pure Gold Red Lake Mine project in Ontario, Canada's newest gold mine, began commercial operations in August 2021 and was estimated to add 87.8 koz of gold yearly.

- Following Russia's invasion of Ukraine, the chemical industry experienced a year marked by further bottlenecks in global supply chains already strained by rising energy and raw material costs, a pandemic, economic uncertainty, and political turmoil in 2022.

- According to a report published by BASF 2022, global chemical production (excluding pharmaceuticals) is expected to increase by 2.0% in 2023, with a Y-o-Y increase of 2.2% from 2022.

- In China, the world's largest chemicals market, a slight slowdown in chemical production growth is expected in 2023. The country's chemical production grew by 5.9% in 2022. The opening up of the Chinese economy is expected to boost domestic demand growth in China, especially in the consumer goods and health and nutrition sectors, and contribute to positive growth in the industry.

- With the consideration of all these factors, the overall market is expected to witness positive growth during the forecast period.

North America to Dominate the Market

- According to the ITC trade map, the United States was the largest exporter of hydrogen cyanide in the year 2022, exporting about 87 tons of hydrogen cyanide in 2022.

- Currently, there are no major country-wide regulations regarding the cyanide product ban. However, states such as Montana, Colorado, and Wisconsin have some restrictions preventing specific cyanide usage in the country.

- The demand for hydrogen cyanide in the region is driven by applications such as the production of adiponitrile, which is used for nylon and polyamides production; the production of acetone cyanohydrin for acrylic plastics, which is further used in paints and coatings; for production of sodium cyanide and potassium cyanide for gold recovery, and cyanuric chloride for pesticides and other agriculture products.

- The country is among the world's major producers of gold and silver. According to the US Geological Survey, in 2022, the country was the 5th largest producer of gold globally, with a total production of about 170 metric tons.

- According to the Silver Institute, the United States was the world's ninth-largest producer of silver in 2022, producing 41.1 million ounces (~1,165.17 metric tons) of silver, which is 6% more than the production in 2021.

- Along with the abovementioned applications, the demand for the market studied in the country is also driven by the agricultural industry in the country, as cyanuric chloride produced using hydrogen cyanide is also used for the production of pesticides and other agricultural products.

- Plastic industries' demand for acetone cyanohydrin further adds to the market's consumption.

- The plastic industry's growth is currently affected by increasing environmental pollution due to the huge amount of plastic waste. According to the Canadian government, about 15 billion plastic bags and about 57 million plastic straws are used annually in the country.

- Hydrogen cyanide-based chemicals, i.e., sodium cyanide and potassium cyanide, find significant applications in the mining process of gold and silver.

- According to USGS, the country is 4th largest producer of gold after China, Australia, and Russia, with gold production of about 220 tons in the year 2022.

- The country is also among the top 15 major silver-producing nations in the world. According to the Silver Institute, the government has produced about 8.7 million ounces of silver (246.64 metric tons ), a decline of about 5% compared to 2021.

- The agriculture industry's demand for pesticides and other products also contributes to the country's significant consumption of hydrogen cyanide.

- The agriculture industry is a significant contributor to the Canadian economy. Agriculture and Agri-Food Canada (AAFC) said that in 2022, Canada was the world's fifth largest agricultural exporter.

- All such trends are likely to impact the market demand over the forecast period.

Hydrogen Cyanide Industry Overview

The global hydrogen cyanide market is partially consolidated. The major companies include (not in a particular order) INVISTA, Evonik Industries, INEOS, Butachimie Chalampe, Drasslok, and Asahi Kasei Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Favorable Demand for Manufacturing of Sodium Cyanide and Potassium Cyanide

- 4.1.2 Increasing Usage of Hydrogen Cyanide for the Production of Adiponitrile

- 4.2 Restraints

- 4.2.1 Highly Toxic Nature of Hydrogen Cyanide

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Structure Type

- 5.1.1 Hydrogen Cyanide Liquid

- 5.1.2 Hydrogen Cyanide Gas

- 5.2 Application

- 5.2.1 Sodium Cyanide and Potassium Cyanide

- 5.2.2 Adiponitrile

- 5.2.3 Acetone Cyanohydrin

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Malaysia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Turkey

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis (%)** /Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Liquide

- 6.4.2 Asahi Kasei Corporation

- 6.4.3 Ascend Performance Materials

- 6.4.4 Butachimie

- 6.4.5 Draslovka

- 6.4.6 Evonik Industries AG

- 6.4.7 Hindusthan Chemicals Company

- 6.4.8 INEOS

- 6.4.9 INVISTA

- 6.4.10 Kuraray Co. Ltd

- 6.4.11 Matheson Tri-Gas Inc.

- 6.4.12 Sumitomo Chemical Co. Ltd

- 6.4.13 Taekwang Industrial Co. Ltd