|

市場調查報告書

商品編碼

1683767

歐洲建築塗料:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)Europe Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

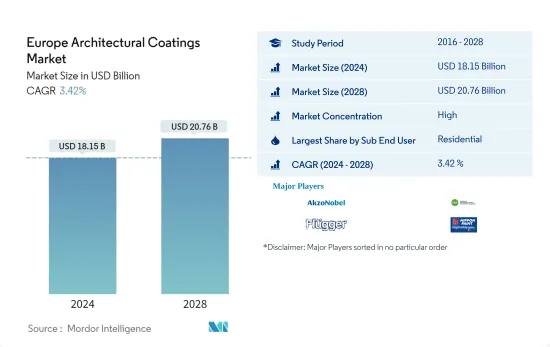

預計 2024 年歐洲建築塗料市場規模為 181.5 億美元,預計到 2028 年將達到 207.6 億美元,預測期內(2024-2028 年)的複合年成長率為 3.42%。

主要亮點

- 最終用戶最大的細分市場—住宅:在歐洲,由於住宅建築與商業建築相比成長相對緩慢,住宅被覆劑的佔有率有所下降。

- 按技術分類的最快細分市場—溶劑型:水性塗料是規模最大、技術發展最快的類型,這得益於消費者意識和歐盟 REACH 等法規以及各國法規的共同推動。

- 按樹脂分類的最大細分市場:丙烯酸:丙烯酸是歐洲最主要的樹脂類型。由於丙烯酸乳膠乳化有望取代溶劑型塗料,因此丙烯酸的主導地位預計將持續下去。

歐洲建築塗料市場的趨勢

按終端用戶細分,住宅是最大的細分市場

- 在終端用戶細分市場中,住宅細分市場在 2020 年佔據了建築業的主導地位,對歐洲市場的建築塗料需求最高,佔比為 71.61%。

- 由於住宅建築與商業建築相比成長相對緩慢,過去五年住宅被覆劑的佔有率有所下降。然而,2020年,由於許多國家住宅DIY領域的強勁成長和商業塗料消費量的下降,住宅塗料在歐洲建築塗料市場的佔有率飆升。

- 預計商業領域的成長將略微超過住宅領域,可能導致預測期內商業佔有率略有回升。

德國是最大的市場

- 在歐洲,德國是建築塗料最大的消費量,佔有率超過17%,其次是俄羅斯、法國、義大利和英國。預計到 2020 年,西班牙、波蘭和北歐地區的佔有率將分別達到 5% 左右。由於人均占地面積和油漆使用量的增加,波蘭和俄羅斯等東歐國家所佔佔有率預計會增加。

- 波蘭是歐洲成長最快的建築市場,預計預測期內成長率約為 4%,其次是俄羅斯、西班牙和法國,成長率均為 3% 左右。預計德國和義大利等成熟市場的成長速度將放緩,銷售成長約 2%。

- 2020 年,波蘭、義大利和德國等許多國家的住宅消費強勁成長,這得益於住宅DIY 領域消費量的強勁成長。

歐洲建築塗料產業概況

歐洲建築塗料市場呈現中度整合態勢,前五大企業合計佔有41.46%的市佔率。該市場的主要企業是:AkzoNobel NV、DAW SE、Flugger group A/S、Nippon Paint Holdings 和 PPG Industries, Inc.(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第 2 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第3章 產業主要趨勢

- 占地面積趨勢

- 法律規範

- 價值鏈與通路分析

第 4 章 市場細分

- 次級終端用戶

- 商業的

- 住宅

- 技術領域

- 溶劑型

- 水

- 樹脂

- 丙烯酸纖維

- 醇酸

- 環氧樹脂

- 聚酯纖維

- 聚氨酯

- 其他樹脂

- 國家

- 法國

- 德國

- 義大利

- 北歐國家

- 波蘭

- 俄羅斯

- 西班牙

- 英國

- 歐洲其他地區

第5章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介

- AkzoNobel NV

- Brillux GmbH & Co. KG

- CIN, SA

- DAW SE

- Flugger group A/S

- Hempel A/S

- KOBER SRL

- Nippon Paint Holdings Co., Ltd.

- POLICOLOR SA

- PPG Industries, Inc.

- Sniezka SA

第6章 執行長的關鍵策略問題

第7章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 93084

The Europe Architectural Coatings Market size is estimated at USD 18.15 billion in 2024, and is expected to reach USD 20.76 billion by 2028, growing at a CAGR of 3.42% during the forecast period (2024-2028).

Key Highlights

- Largest Segment by End-user - Residential : The share of residential coatings has been declining in Europe due to the relatively slow growth of residential constructions compared to commercial constructions.

- Fastest Segment by Technology - Solventborne : Waterborne coatings are the largest and fastest technology type due to consumer awareness and regulations, such as EU REACH, combined with various country-level regulations.

- Largest Segment by Resin - Acrylic : Acrylics are the most dominant resin type in Europe. They are expected to continue their dominance as acrylic latex emulsions are expected to replace solvent-borne coatings.

Europe Architectural Coatings Market Trends

Residential is the largest segment by Sub End User.

- Among the end-user segments, the residential segment dominated the construction sector in 2020, generating the highest demand for architectural coatings in the European market, with a share of 71.61%.

- The share of residential coatings has been declining over the past five years due to the relatively slow growth of residential construction compared to commercial. However, in 2020, the high growth of the residential DIY segment in many countries and the contraction of commercial paint consumption contributed to the sudden increase in the share of residential coatings in the European architectural coatings market.

- The growth of the commercial segment is expected to be slightly higher than its residential counterpart, which may result in a slight recovery of the commercial share during the forecast period.

Germany is the largest segment by Country.

- In Europe, Germany has the largest architectural coatings consumption, with more than 17% share, followed by Russia, France, Italy, and the United Kingdom. Spain, Poland, and Nordic regions were estimated to have had a share of around 5% each during 2020. The share of eastern block countries such as Poland and Russia is expected to increase due to the increasing median floor area and paint per capita.

- Poland is estimated to be the fastest-growing architectural market in Europe, with around 4% growth during the forecast period, followed by Russia, Spain, and France, with around 3% growth rates. Mature markets such as Germany and Italy are expected to have lower growth rates of less than and around 2% in volume.

- Many countries such as Poland, Italy, and Germany saw huge increases in residential consumption in 2020 due to huge growth in consumption in the residential DIY segment.

Europe Architectural Coatings Industry Overview

The Europe Architectural Coatings Market is moderately consolidated, with the top five companies occupying 41.46%. The major players in this market are AkzoNobel N.V., DAW SE, Flugger group A/S, Nippon Paint Holdings Co., Ltd. and PPG Industries, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Floor Area Trends

- 3.2 Regulatory Framework

- 3.3 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION

- 4.1 Sub End User

- 4.1.1 Commercial

- 4.1.2 Residential

- 4.2 Technology

- 4.2.1 Solventborne

- 4.2.2 Waterborne

- 4.3 Resin

- 4.3.1 Acrylic

- 4.3.2 Alkyd

- 4.3.3 Epoxy

- 4.3.4 Polyester

- 4.3.5 Polyurethane

- 4.3.6 Other Resin Types

- 4.4 Country

- 4.4.1 France

- 4.4.2 Germany

- 4.4.3 Italy

- 4.4.4 Nordic Countries

- 4.4.5 Poland

- 4.4.6 Russia

- 4.4.7 Spain

- 4.4.8 United Kingdom

- 4.4.9 Rest Of Europe

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles

- 5.4.1 AkzoNobel N.V.

- 5.4.2 Brillux GmbH & Co. KG

- 5.4.3 CIN, S.A.

- 5.4.4 DAW SE

- 5.4.5 Flugger group A/S

- 5.4.6 Hempel A/S

- 5.4.7 KOBER SRL

- 5.4.8 Nippon Paint Holdings Co., Ltd.

- 5.4.9 POLICOLOR SA

- 5.4.10 PPG Industries, Inc.

- 5.4.11 Sniezka SA

6 KEY STRATEGIC QUESTIONS FOR ARCHITECTURAL COATINGS CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

建築塗料市場分析及預測(至2035年):依類型、產品類型、技術、應用、材質、製程、最終用戶、功能、應用方法及解決方案分類

建築塗料市場分析及預測(至2035年):依類型、產品類型、技術、應用、材質、製程、最終用戶、功能、應用方法及解決方案分類 建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球含鋅底漆市場報告2026年全球外牆塗料市場報告2026年全球富鋅塗料市場報告2026年全球建築塗料市場報告

2026年全球含鋅底漆市場報告2026年全球外牆塗料市場報告2026年全球富鋅塗料市場報告2026年全球建築塗料市場報告 建築塗料市場-全球產業規模、佔有率、趨勢、機會與預測(2021-2031)

建築塗料市場-全球產業規模、佔有率、趨勢、機會與預測(2021-2031) 唇釉市場按分銷管道、產品類型、配方和包裝類型分類,全球預測(2026-2032年)壓克力外牆塗料市場:依技術、色彩、應用、最終用途及通路分類-2026-2032年全球預測

唇釉市場按分銷管道、產品類型、配方和包裝類型分類,全球預測(2026-2032年)壓克力外牆塗料市場:依技術、色彩、應用、最終用途及通路分類-2026-2032年全球預測 建築塗料市場-2026-2031年預測

建築塗料市場-2026-2031年預測

▼