|

市場調查報告書

商品編碼

1644363

北美貨櫃型資料中心:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)North America Containerized Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

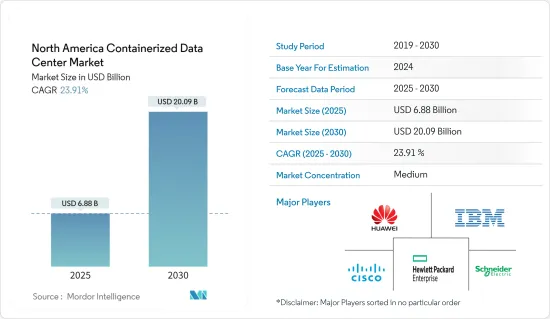

北美貨櫃型資料中心市場規模預計在 2025 年為 68.8 億美元,預計到 2030 年將達到 200.9 億美元,預測期內(2025-2030 年)的複合年成長率為 23.91%。

關鍵亮點

- 近年來,由於雲端運算的普及和資料生成的不斷增加,該地區對貨櫃型資料中心的需求呈指數級成長。這些資料中心在製造工廠中製造並透過貨櫃運送給最終用戶。在這種類型的資料中心中,大多數組件都是預先安裝的,限制了更換或升級組件的靈活性。

- 貨櫃型資料中心解決方案單元簡化了您的實體IT基礎設施。模組化方法可以集中在資料中心或更精細的層面上。例如,更精細的方法可以深入到機架層級。隨著基於 x86 的伺服器、儲存和網路設備市場的成長,各垂直市場的最終用戶都在尋找更有效的方式來部署和管理他們的資料中心設備。

- 此外,巨量資料和物聯網(IoT)在該地區的滲透預計將顯著改變下一代模組化資料中心的規模和範圍。現有的競爭迫使企業在 IT 可擴展性和容量方面不斷發展。隨著資料、混合雲端和外包給第三方資料中心的快速成長,貨櫃型資料中心因其能夠在最短時間內靈活地建立中心而越來越受歡迎。

- 此外,主要工業領域數位化程度的提高、技術的穩步進步以及智慧連網型設備的不斷普及正在促進北美物聯網的發展。

- 組織正在轉向模組化服務,透過從可用的整合產品組合中選擇所需的服務來最佳化其基礎設施。此外,我們的標準化交付部署意味著可以透過我們的線上目錄獲得多種服務選項。這些選項列出了可減少企業前期投資的功能。 IBM 的整合託管基礎架構服務就是這種情況的一個例子。

- 然而,高昂的初始投資和低資源可用性對這個市場構成了挑戰。此外,這些資料中心是容器化的,體積小,可以從一個地方移動到另一個地方。因此,計算效率受到限制。

- 在新冠疫情封鎖期間,隨著越來越多的人遠距辦公,對資料中心的需求增加。由於雲端服務的使用日益增多,資料流量的增加對所研究的市場產生了影響。

北美貨櫃型資料中心市場趨勢

政府機構預計將顯著成長

- 政府機構也廣泛採用貨櫃型資料中心來增強安全性。員工社保號、軍事地址和平民資訊等敏感資料將儲存在由人工智慧系統操作的模組化資料中心,提供額外的保護。

- 政府措施和公共存取平台的數位化是全球對貨櫃型資料中心的最大需求來源。這推動了對模組化資料中心的需求。

- 例如,2022年9月,美國能源局宣布將提供4,200萬美元的資金,幫助減少用於冷卻資料中心的能源,並在2050年實現淨零碳排放。

- 此外,2023 年 2 月,亞馬遜網路服務 (AWS) 向美國政府推出了模組化資料中心 (MDC),這將使在偏遠地區部署臨時的 AWS 管理的 Bitburn 變得更加容易。 AWS MDC 是美國國防部 (DoD) 機構的自足式模組化資料中心單元,可透過增加其他單元進行擴充。每個單元都安置在一個堅固的貨櫃內,可以透過船、鐵路、卡車甚至軍用貨機運輸。

- 考慮到加拿大的環境,加拿大政府 (GC) 透過其「雲端優先」策略概述了在進行資訊技術 (IT) 投資、舉措、策略和計劃時將雲端服務確定和評估為主要交付選項。

美國:預計將大幅成長

- 北美企業開始將超融合視為傳統資料中心的可行替代方案。超融合將儲存、網路和運算結合到單一系統中,從而降低了資料中心的複雜性並提高了可擴展性。因此,超融合式基礎架構平台的採用正在增加,推動了貨櫃型資料中心市場的發展。

- 根據 Coldwell Banker Richard Ellis (CBRE) 的報告,2022 年上半年美國主要資料中心市場的總容量成長了 10.5%,達到 352.9 兆瓦 (MW)。該國目前還有 1,600 兆瓦的額外發電容量正在建設中。因此,美國主要批發資料中心市場在 2022 年上半年的總合淨吸收量達到 453.4MW,是 2021 年上半年的三倍多。

- 邊緣資料中心的發展完全由貨櫃型資料中心推動。此外,它還具有便攜性、安裝快速、可擴展、無論身在何處都可以隨時配備伺服器功能等特點,因此被廣泛採用。因此,市場相關人員正在致力於製造用於貨櫃型資料中心的伺服器。

- 2022年9月,提案在深海建立商業資料中心的公司Subsea Cloud宣布計畫在華盛頓州安吉利斯港附近安裝一個吊艙。這些伺服器艙將安置在長 6 公尺(20 英尺)的貨櫃內,深度約為 9 米,最初將容納 800 台伺服器,並計劃最終擴展到 100 個這樣的伺服器艙。

- 此外,該地區擁有強大的模組化資料中心提供者基礎,從而推動了成長。 IBM 公司、HPE、Vertiv 公司、思科系統、戴爾 EMC 等

- 例如,Google已宣布計劃在2022年終前在美國投資95億美元設立新辦公室和資料中心。此外,Google還在 26 個美國的辦公室和資料中心投資超過 370 億美元。該地區主要企業的重大投資預計將推動貨櫃型資料中心的發展。

北美貨櫃型資料中心產業概況

北美貨櫃型資料中心市場包括 IBM 公司、惠普企業、戴爾公司、思科系統、Rittal GmbH & Co. KG 和華為技術等主要參與者。這些參與企業正在進行併購和產品推出,以開發並向市場推出新技術和新產品。因此,預計市場集中度將處於中等水平。

2022 年 10 月,IBM 宣布將把 Red Hat 的儲存產品藍圖和 Red Hat 關聯團隊加入其 IBM 儲存業務部門,以在本地基礎設施和雲端提供一致的應用程式和資料儲存。透過此舉,IBM 將整合 Red Hat OpenShift Data Foundation (ODF) 的儲存技術作為 IBM Spectrum Fusion 的基礎。此舉將 IBM 和 Red Hat 的資訊服務容器儲存技術整合在一起,並加速 IBM 在快速成長的 Kubernetes 平台市場中的能力。

此外,2022 年 10 月,Oracle 宣布推出新服務以簡化雲端中的管理、安全性和開發,其中包括一項託管無伺服器 Kubernetes 服務,適用於希望建立容器化應用程式而無需管理 Kubernetes 基礎架構的客戶。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈/供應鏈分析

- COVID-19 工業影響評估

第5章 市場動態

- 市場概況

- 市場促進因素

- 對便攜性的需求以及對可擴展資料中心解決方案日益成長的需求

- 節能資料中心的需求不斷增加

- 市場限制

- 運算能力有限

第6章 市場細分

- 按最終用戶產業

- 資訊科技/通訊

- BFSI

- 政府

- 其他

- 按國家

- 美國

- 加拿大

第7章 競爭格局

- 公司簡介

- Hewlett Packard Enterprise Company

- IBM Corporation

- Dell Inc.

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd.

- Emerson Network Power(Emerson Electric Co.)

- Schneider Electric SE(acquired AST Modular)

- Rittal Gmbh & Co. KG

第8章投資分析

第9章:市場的未來

The North America Containerized Data Center Market size is estimated at USD 6.88 billion in 2025, and is expected to reach USD 20.09 billion by 2030, at a CAGR of 23.91% during the forecast period (2025-2030).

Key Highlights

- With the growing adoption of the cloud and increasing data generation, the demand for containerized data centers in the region has spiked drastically over the past few years. These data centers are fabricated in a manufacturing facility and shipped to the end user in the container. Most of the components in this type of data center are preinstalled and offer limited flexibility in replacing and upgrading components.

- Containerized data center solution units facilitate the physical IT infrastructure. The modular approach can focus on the data center or a more granular level. For instance, more granular approaches can go down to the rack level. As the market for x86-based servers, storage, and network equipment has grown, end users across a broad spectrum of vertical markets have been exploring ways to find more effective methods of installing and managing data center equipment.

- Moreover, big data and Internet of Things (IoT) penetration in the region is expected to significantly transform the size and scope of the next-generation modular data centers. With the existing competition, organizations are under pressure to evolve IT scalability and capacity. With the exponential growth of data, hybrid cloud, and outsourcing third-party data centers, containerized data centers are gaining traction, owing to their flexibility in installing a center within the least possible time.

- Further, rising digitization throughout the industrial emphasis areas, steady technological advancements, and rising penetration of smart connected devices have all contributed to the growth of IoT in the North American region.

- Organizations are looking at modular services to optimize their infrastructure by selecting the desired services from the available integrated portfolio. In addition, with the standardized delivery deployment, several service options are made available from online catalogs. These options offer the ability to lower the upfront investment for companies. IBM integrated managed infrastructure service is an example of this situation.

- However, higher initial investments and low resource availability are some factors presenting challenges to this market. Further, these data centers are containerized; they are in small sizes and can be moved from one place to another. As a result of this, they have limited computing efficiency.

- During the COVID-19 lockdown, the demand for data centers grew as more people started working remotely. Increased data traffic impacted the market studied due to the expanding use of cloud services.

North America Containerized Data Center Market Trends

Government Sector Expected to Witness Significant Growth

- Government agencies are also broadly adopting containerized data centers to bolster security. The sensitive data, such as employees' social security numbers, addresses of service members, and citizens' information, are stored in modular data centers operated by AI systems for an additional layer of protection.

- Government initiatives and the digitalization of public accessibility platforms are the greatest sources of demand for containerized data centers worldwide. This is increasing the demand for modular data centers.

- For instance, in September 2022, the US Department of Energy announced that it is providing USD 42 million in funding for initiatives to lower the energy consumed for cooling in data centers and reach net zero carbon dioxide emissions by 2050.

- Moreover, in February 2023, Amazon Web Services (AWS) pitched a modular data center (MDC) to the US government to make it easier to deploy makeshift bit barns managed by AWS in remote locations. AWS MDC is a self-contained modular data center unit for US Department of Defense (DoD) agencies, which can scale by deploying additional units. Each is housed inside a ruggedized shipping container for freight transportation via ship, rail, truck, or even air transport using military cargo aircraft.

- Considering the Canadian environment, the Government of Canada (GC), by its "cloud-first" strategy, outlined that cloud services are identified and evaluated as the principal delivery option when initiating information technology (IT) investments, initiatives, strategies, and projects.

United States Expected to Witness Significant Growth

- Enterprises in the North American region have started to view hyper-convergence as a viable alternative to the traditional data center. It combines storage, networking, and computing into a single system, reducing data center complexity and increasing scalability. As a result, an increase in adopting a hyper-converged infrastructure platform is driving the containerized data center market.

- According to a report by Coldwell Banker Richard Ellis (CBRE), the total capacity of the US primary data center markets grew by 352.9 megawatts (MW) or 10.5% in H1 2022. The country is expanding its capacity by more than 1600 MW, currently under construction. As a result, the primary US wholesale data center market recorded a combined 453.4 MW of net absorption in H1 2022, more than triple H1 2021's level and almost 60% of it in Northern Virginia.

- The development of edge data centers attributes solely to containerized data centers, as it tends to meet an organization's new-age demands. Moreover, it is highly adopted due to its portable format, quick to install, scalable, and equipped with server functionality at a given point in time, regardless of location. Therefore, market players are observed to manufacture servers compatible with containerized data centers.

- In September 2022, Subsea Cloud, the company proposing to put commercial data centers in deep ocean waters, announced its plan to install a pod near Port Angeles, Washington State. The pod will start with a 6m (20ft) shipping container around nine meters underwater, holding 800 servers, eventually scaling to 100 such pods.

- Moreover, the region has a strong foothold of modular data center providers, which adds to its growth. Some include IBM Corporation, HPE, Vertiv Co., Cisco Systems, and Dell EMC.

- For instance, Google announced its plan to invest USD 9.5 billion in new offices and data centers in the US by the end of 2022. Moreover, Google has spent over USD 37 billion on its offices and data centers across 26 US states. Such significant investments by the key players in the region are expected to boost the development of containerized data centers.

North America Containerized Data Center Industry Overview

The North America containerized data center market includes major players such as IBM Corporation, Hewlett Packard Enterprise, Dell Inc., Cisco Systems Inc., Rittal GmbH & Co. KG, and Huawei Technologies Co. Ltd, among others. These players are undertaking mergers and acquisitions and product launches to develop and introduce new technologies and products to the market. As a result of this, market concentration will be medium.

In October 2022, IBM announced it would add Red Hat storage product roadmaps and Red Hat associate teams to the IBM Storage business unit, bringing consistent application and data storage across on-premises infrastructure and cloud. With the move, IBM will integrate the Red Hat OpenShift Data Foundation (ODF) storage technologies as the foundation for IBM Spectrum Fusion. This combines IBM and Red Hat's container storage technologies for data services and helps accelerate IBM's capabilities in the burgeoning Kubernetes platform market.

Moreover, in October 2022, Oracle announced the launch of new services to simplify management, security, and development in the cloud, including a managed serverless Kubernetes service for customers who want to build containerized applications without having to manage the Kubernetes infrastructure.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain / Supply Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Need for Portability and Increasing Demand for Scalable Data Center Solutions

- 5.2.2 Rising Demand for Energy Efficient Data Centers

- 5.3 Market Restraints

- 5.3.1 Limited Computing Performance

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 IT & Telecommunications

- 6.1.2 BFSI

- 6.1.3 Government

- 6.1.4 Other End-users

- 6.2 Country

- 6.2.1 The United States

- 6.2.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Hewlett Packard Enterprise Company

- 7.1.2 IBM Corporation

- 7.1.3 Dell Inc.

- 7.1.4 Cisco Systems Inc.

- 7.1.5 Huawei Technologies Co. Ltd.

- 7.1.6 Emerson Network Power(Emerson Electric Co.)

- 7.1.7 Schneider Electric SE (acquired AST Modular)

- 7.1.8 Rittal Gmbh & Co. KG

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025年全球人工智慧資料中心市場報告

2025年全球人工智慧資料中心市場報告 容器化資料中心市場-全球產業規模、佔有率、趨勢、機會和預測(按容器類型、企業類型、產業、地區和競爭格局分類,2020-2030 年預測)

容器化資料中心市場-全球產業規模、佔有率、趨勢、機會和預測(按容器類型、企業類型、產業、地區和競爭格局分類,2020-2030 年預測) 貨櫃型資料中心市場:按解決方案組件、貨櫃類型、冷卻技術、機架數量、企業規模和最終用戶分類 - 全球預測(2025-2032 年)2025年全球貨櫃型資料中心市場報告

貨櫃型資料中心市場:按解決方案組件、貨櫃類型、冷卻技術、機架數量、企業規模和最終用戶分類 - 全球預測(2025-2032 年)2025年全球貨櫃型資料中心市場報告 2025 年至 2033 年貨櫃資料中心市場報告(按貨櫃類型、組織規模、應用、最終用途產業和地區分類)

2025 年至 2033 年貨櫃資料中心市場報告(按貨櫃類型、組織規模、應用、最終用途產業和地區分類) 貨櫃型資料中心:市場佔有率分析、產業趨勢、統計資料和成長預測(2025-2030 年)全球貨櫃型資料中心市場:2034 年的機會與策略

貨櫃型資料中心:市場佔有率分析、產業趨勢、統計資料和成長預測(2025-2030 年)全球貨櫃型資料中心市場:2034 年的機會與策略 貨櫃型資料中心市場分析及2034年預測:類型、產品、服務、技術、組件、應用、結構、部署、最終用戶、模組

貨櫃型資料中心市場分析及2034年預測:類型、產品、服務、技術、組件、應用、結構、部署、最終用戶、模組 貨櫃型資料中心市場規模、佔有率、成長分析(按貨櫃類型、部署規模、應用、最終用途和地區)- 產業預測(2025 年至 2032 年)

貨櫃型資料中心市場規模、佔有率、成長分析(按貨櫃類型、部署規模、應用、最終用途和地區)- 產業預測(2025 年至 2032 年) 全球貨櫃資料中心市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測

全球貨櫃資料中心市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測