|

市場調查報告書

商品編碼

1644355

光波長服務-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Optical Wavelength Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

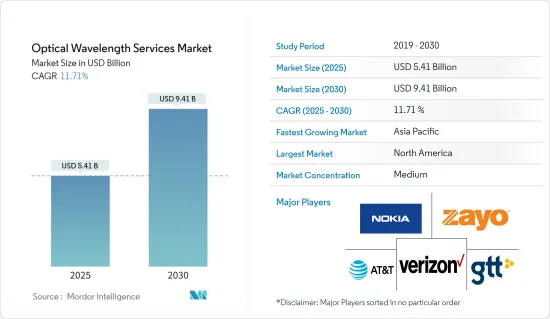

光波長服務市場規模預計在 2025 年為 54.1 億美元,預計到 2030 年將達到 94.1 億美元,預測期內(2025-2030 年)的複合年成長率為 11.71%。

預計預測期內全球資料量將加倍,這將更加需要關注每位元成本和功耗。將大波長延伸至遠距可為最終用戶提供更具成本效益和更有效率的服務。大波長還能顯著提高網路頻寬,為高清內容、5G 蜂窩網路、物聯網、遠端工作和其他應用提供必要的動力。

關鍵亮點

- 對 FTTH 系統的需求正在增加,網路連線的擴展不僅在都市區,而且在農村和偏遠地區也在加速。這些投資將加劇有線電視公司之間的競爭,以提供更密集、更強大的無線網路和更高頻寬的服務。

- 2023 年 2 月,富士通宣布推出超可靠光纖傳輸平台“1FINITY”,每波長的資料速率可達 1.2Terabit每秒 (Tbps)。該平台將有助於降低電力消耗,並將整個網路的二氧化碳排放減少 60%。

- 儘管在其網路上更廣泛地部署 FTTH 具有許多好處,但通訊業者仍對安裝額外光纖和最終用戶光纖數據機的成本感到畏懼。隨著產業轉向 50G 和 100G 等需要調變解調器連貫技術的更高頻寬,這個成本問題只會變得更加嚴重。

- 即使在 COVID-19 疫情之後,網路營運商仍在繼續增加設備和容量,以支援遠端工作、雲端基礎的服務、串流媒體視訊、物聯網和 5G 無線技術。對資料和高速網路不斷成長的需求,加上供應中斷,促使網路解決方案供應商採用更長的波長來快速擴展容量,以解決流量瓶頸和緩慢的資料傳輸速度。

光波長服務市場趨勢

10Gbps 以下頻寬市場預計將佔據較大市場佔有率

- 需要頻寬的應用程式需要高效能的連線。波長服務對於光纖傳輸技術的發展至關重要,使得單一光纖的容量能夠達到100Gbps及以上的吞吐量。結合網路管理系統,該技術使通訊業者能夠採用基於光纖的網路基礎設施來滿足未來的頻寬需求。

- 在目前部署的基於單芯光纖的光纖網路中,可以透過增加每通道的位元率或增加給定傳輸頻譜內的可用通道數量來提高資料傳輸速率。

- 連貫WDM技術是一種非常先進的光纖傳輸技術,具有許多優點,包括更高的位元率、更大的靈活性、更簡單的DWDM線路系統和更好的光學性能。該技術推動了DWDM網路中經濟高效、可靠的光纖傳輸的發展,將波長速度從前連貫時代的10Gb/s提高到100Gb/s、200Gb/s,甚至最新連貫光設備中的400Gb/s和800Gb/s。

- CWDM和DWDM是解決資訊傳輸日益成長的頻寬需求的兩種不同方法。 DWDM 使用更多窄波長頻寬或通道,而 CWDM 每個通道使用較寬的波長頻寬。

- 根據英國政府批准的廣播、通訊和郵政行業監管和競爭機構通訊 的數據,CWDM 使用的平均頻寬約為 2.9μm。平均每人每月使用約2.9GB的資料,而且隨著數位化的進步,這種需求只會增加。然而事實證明,10Gb/s 對於普通行動電話用戶來說已經足夠了。

- 2023 年 2 月,新加坡電信業者StarHub 推出了超高速寬頻,速度和頻寬比新加坡標準寬頻服務快 10 倍。這項高速寬頻服務增強了您家庭的連接能力,為線上遊戲和閃電般的內容流提供最佳響應能力。

亞太地區可望佔據主要市場佔有率

- 北美和歐洲加起來僅佔全球行動資料服務的四分之一,而印度和中國則佔全球行動流量的近一半。印度已成為行動資料服務市場的主要企業,其行動資料消費量位居全球第一,達到每位用戶每月 12GB。

- 此外,印度每季新增2,500萬智慧型手機用戶,使其成為行動資料服務的重要市場。預計到 2022 年,智慧型手機用戶數量的激增將使每位用戶每月的平均資料消耗量達到 19.5GB,這意味著對資料驅動應用程式和服務的需求將持續成長。這一發展凸顯了印度作為全球行動資料市場主要參與企業的地位,為未來的進一步成長和創新提供了巨大的潛力。

- 行動資料服務的強勁成長也刺激了對 5G 設備的需求,私營部門在 5G 網路方面的支出導致印度此類設備的出貨量強勁。據估計,印度目前5G設備出貨量已超過7,000萬台,預計到2027年私人無線網路投資將達到約2.5億美元。這將鼓勵通訊業者提供更強大的網路連線速度,進而推動光波長服務的成長。

- 新興國家政府紛紛採取舉措,加速本國通訊基礎設施的發展。亞太地區由於其廉價的勞動力和較高的工業 4.0 採用率,正成為越來越受歡迎的製造業地點。亞洲各國政府正積極推動新興企業的發展,推出「中國製造2025」等計劃,旨在支持中國製造業和工業4.0的更廣泛應用。

光波長服務業概況

目前,光波長服務市場競爭激烈,但隨著供應商計劃推出新產品、建立合作夥伴關係和進行收購,預計該領域將會成長。該領域的市場領導包括 Zayo Group、Nokia、Century Link、Verizon Wireless、Century Link 和 Windstream Communications。與其他網路設定相比,光波長網路提供了一種可擴展的解決方案,可快速增加容量以解決資料速率慢和傳輸瓶頸問題。

2023 年 2 月,諾基亞宣布將與 GlobalConnect Fiber Networks 合作對其第六代超連貫光子服務引擎進行真實世界試驗。此次試驗的目標是使用單一波長在 118 公里的城域距離內達到 1.2Tb/s 的速度,在 2,019 公里的長距離內達到 800Gb/s 的速度。部署該技術可降低網路功耗高達 60%,並將網路總體擁有成本降低高達 50%。

2022 年 3 月,通訊網路供應商 Enet 與 EXA Infrastructure 簽署契約,在都柏林與其遍布歐洲和北大西洋的資料中心之間建立新的高速資料中心間光纖網路連線。 International Wave計劃旨在提供價格具競爭力、安全、快速且透明的資料間連線。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 評估新冠肺炎對各行業的影響

第5章 市場動態

- 市場促進因素

- 網路需求不斷成長

- 加速頻寬頻寬密集型

- 市場限制

- 增量頻寬可用性有限

- 虛擬連線的需求不斷增加

第6章 市場細分

- 按頻寬

- 10Gbps 或更低

- 40Gbps

- 100Gbps

- 100Gbps 或更高

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 其他

第7章 競爭格局

- 公司簡介

- Nokia Corporation

- Zayo Group Holdings, Inc.

- Verizon Communications Inc.

- GTT Communications, Inc.

- AT&T Inc.

- Lumen Technologies Inc.

- T-Mobile US Inc.

- Crown Castle Inc.

- Comcast Corporation

- Charter Communications

- Windstream Holdings, Inc.

- Colt Technology Services Group Limited

- Cox Communications

- Jaguar Network SAS

- CarrierBid Communications

- EUnetworks Group

- Telia Carrier

- Exascale Limited

第8章投資分析

第9章:市場的未來

The Optical Wavelength Services Market size is estimated at USD 5.41 billion in 2025, and is expected to reach USD 9.41 billion by 2030, at a CAGR of 11.71% during the forecast period (2025-2030).

Global data volumes projected to double during forecasted year, there is a growing need to focus on cost and power consumption per bit. Extending large wavelengths across longer distances can make services more cost-effective and efficient for end-users. Larger wavelengths also provide significant network bandwidth expansion, essential to power high-definition content, 5G cell networks, IoT, remote work, and other applications.

Key Highlights

- The demand for fiber-to-home (FTTH) systems is increasing, accelerating the deployment of network connections not just in urban areas but also in rural and remote locations. These investments lead to more robust competition among cable companies to create a denser, higher-performance wireless network and high wavelength services.

- In February 2023, Fujitsu launched the Ultra Optical System called 1FINITY, a hyper-reliable optical transport platform delivering extreme performance and scalability with data rates of 1.2 terabits per second (Tbps) on a single wavelength. This platform helps to reduce power consumption and achieve a 60% reduction of CO2 emissions throughout networks.

- Despite the benefits of implementing FTTH more extensively across networks, carriers are still discouraged by the cost of installing additional fiber and the end-users' optical modems. As the industry transitions to larger bandwidths, such as 50G and 100G, which require coherent technology in the modems, this cost issue will worsen.

- Even after the Covid-19 pandemic, network operators continue to add more gear and capacity to support remote work, cloud-based services, streaming video, IoT, and 5G wireless technology. This increasing demand for data and high-speed networks with uninterrupted supply drives Network Solution providers to adopt high wavelengths that can quickly scale up capacity to address traffic bottlenecks or combat slower data transfer speeds.

Optical Wavelength Services Market Trends

Less than 10 Gbps Bandwidth Segment is Expected to Hold Significant Market Share

- Bandwidth-intensive applications demand high-performance connectivity. Wavelength services are essential in developing fiber optic transmission technology and can increase a single fiber's capacity to a throughput of 100 Gbps and beyond. The technology combines network management systems to enable carriers to adopt optically-based network infrastructures to meet future bandwidth demands.

- In currently deployed optical networks based on single-core fibers, the data transmission rate can be increased by using either a larger per-channel bit rate or increasing the number of available channels within a particular transmission spectrum.

- Coherent WDM technology is a highly advanced optical transmission technology that offers numerous benefits, including higher bit rates, greater flexibility, simpler DWDM line systems, and better optical performance. This technology has enabled the development of cost-effective and highly reliable optical transport in DWDM networks, with wavelength speeds increasing from 10 Gb/s in the pre-coherent era to 100 Gb/s, 200 Gb/s, and now even 400 or 800 Gb/s with the latest coherent optical equipment.

- CWDM and DWDM are two different methods for addressing the increasing bandwidth requirements for information transmission. DWDM employs a larger number of narrower wavelength bands or channels, while CWDM uses broader wavelength bands per channel.

- According to the of Communications (Ofcom), the government-approved regulatory and competition authority for the broadcasting, telecommunications, and postal industries of the United Kingdom. The average person uses around 2.9GB of data per month, and this demand is continuously increasing with the evolution of digitalization. However, this confirms that 10Gb/s is more than enough for the average phone user.

- In February 2023, StarHub, the Singaporean telco, introduced ultra-speed broadband with up to 10 times the speed and bandwidth of standard broadband services in Singapore. This high-speed broadband service will significantly enhance household connectivity, providing optimal responsiveness for online gaming and lightning-fast content streaming.

Asia Pacific is Expected to Hold Significant Market Share

- India and China are the two countries that account for nearly half of the world's mobile traffic, while North America and Europe together only account for a quarter of the global mobile data services. India, in particular, has emerged as a major player in the mobile data services market, with the highest mobile data consumption rate of 12 GB/user a month globally.

- Moreover, India witnesses a remarkable increase of 25 million new smartphone users every quarter, making it a crucial market for mobile data services. This surge in smartphone usage has led to an average data consumption rate of 19.5 GB per user per month in 2022, indicating a growing demand for data-driven applications and services. This trend highlights India's position as a key player in the global mobile data market, with enormous potential for further growth and innovation in the future.

- The strong growth of mobile data services has also fueled demand for 5G devices, with private enterprise spending on 5G networks leading to robust shipments of these devices in India. It is estimated that over 70 million 5G devices have been shipped to India, and the country's investment in private wireless networks is expected to reach approximately USD 250 million by 2027. This will encourage telecom providers to offer more powerful network connection speeds, which, in turn, will promote the growth of Optical Wavelength Services.

- Governments in developing nations are taking initiatives to encourage the development of communication infrastructure in their countries. The Asia-Pacific region, in particular, is becoming increasingly popular as a hub for manufacturing due to its cheap labor and high adoption rate of the Industry 4.0 movement. Governments in Asian countries are aggressively promoting the growth of new firms, with programs like "Made in China 2025" designed to broadly support Chinese manufacturing and the implementation of Industry 4.0.

Optical Wavelength Services Industry Overview

The Optical Wavelength Services Market currently experiences moderate competition, but this sector is expected to grow as vendors plan new product launches, partnerships, and acquisitions. Some of the market leaders in this segment include Zayo Group, Nokia, Century Link, Verizon Wireless, Century Link, and Windstream Communications. Compared to other network setups, optical wavelength networks offer a scalable solution that can quickly increase capacity to combat slower data transfer speeds or address traffic bottlenecks.

In February 2023, Nokia announced a collaboration with GlobalConnect fiber networks to conduct trials of its sixth-generation super-coherent Photonic Service Engine in real-world environments. These trials aim to achieve 1.2Tb/s over metro distances of 118km and 800Gb/s over a long-haul distance of 2,019km, both using a single wavelength. By deploying this technology, network power consumption can be reduced by up to 60%, and the total cost of network ownership can be reduced by up to 50%.

In March 2022, Enet, a telecom network provider, signed a contract with EXA Infrastructure to establish new high-speed datacentre-to-datacentre optical network connections between Dublin and data centers in Europe and the North Atlantic. This International Wave project aims to provide price-competitive, secure, high-speed, and transparent inter-datacentre connectivity.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assesment of Covid-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for the Internet

- 5.1.2 Accelerated Bandwidth-intensive Applications

- 5.2 Market Restraints

- 5.2.1 Limited Availability of Incremental Bandwidth

- 5.2.2 Increasing Demand for Virtual Connectivity

6 MARKET SEGMENTATION

- 6.1 By Bandwidth

- 6.1.1 Less than 10 Gbps

- 6.1.2 40 Gbps

- 6.1.3 100 Gbps

- 6.1.4 More Than 100 Gbps

- 6.2 Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Nokia Corporation

- 7.1.2 Zayo Group Holdings, Inc.

- 7.1.3 Verizon Communications Inc.

- 7.1.4 GTT Communications, Inc.

- 7.1.5 AT&T Inc.

- 7.1.6 Lumen Technologies Inc.

- 7.1.7 T-Mobile US Inc.

- 7.1.8 Crown Castle Inc.

- 7.1.9 Comcast Corporation

- 7.1.10 Charter Communications

- 7.1.11 Windstream Holdings, Inc.

- 7.1.12 Colt Technology Services Group Limited

- 7.1.13 Cox Communications

- 7.1.14 Jaguar Network SAS

- 7.1.15 CarrierBid Communications

- 7.1.16 EUnetworks Group

- 7.1.17 Telia Carrier

- 7.1.18 Exascale Limited

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

光波長服務市場規模、佔有率、趨勢和預測:按頻寬、介面、組織規模、應用和地區分類,2026-2034 年

光波長服務市場規模、佔有率、趨勢和預測:按頻寬、介面、組織規模、應用和地區分類,2026-2034 年 2026年全球光波長服務市場報告

2026年全球光波長服務市場報告 光波長服務市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署模式、最終用戶、功能及解決方案分類

光波長服務市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署模式、最終用戶、功能及解決方案分類 光波長服務市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2026-2034)Frost Radar:北美波長服務,2025 年

光波長服務市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2026-2034)Frost Radar:北美波長服務,2025 年 光波長服務市場-全球產業規模、佔有率、趨勢、機會及預測(按傳輸速率、按配置類型、按行業、按地區、按競爭)2020-2030F

光波長服務市場-全球產業規模、佔有率、趨勢、機會及預測(按傳輸速率、按配置類型、按行業、按地區、按競爭)2020-2030F