|

市場調查報告書

商品編碼

1642063

英國包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)United Kingdom Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

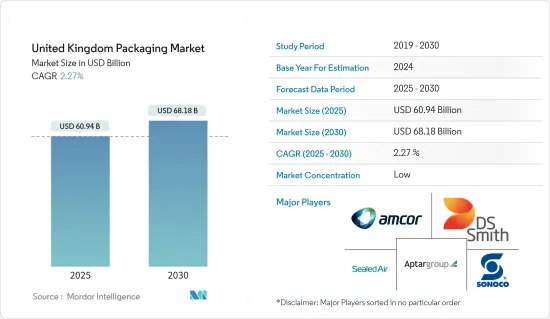

預計 2025 年英國包裝市場規模為 609.4 億美元,到 2030 年將達到 681.8 億美元,預測期內(2025-2030 年)的複合年成長率為 2.27%。

主要亮點

- 由於製造業活動的增加,英國包裝市場正在經歷顯著的成長。 2024 年 2 月,可口可樂計劃暫時去除雪碧和零度雪碧便攜瓶上的標籤,並在英國進行「無標籤」包裝的有限試驗,在 500 毫升瓶子的包裝正面印上標誌,以表明該國包裝市場的需求。

- 電子商務銷售額的成長、食品和飲料製造商對環保和可回收包裝的需求不斷增加、產品個人化需求不斷成長以及工業包裝領域的成長,正在推動該國包裝市場的成長。根據英國國際貿易部 2023 年 11 月的報告,英國擁有僅次於中國和美國的全球第三大電子商務市場,預計未來幾年將支持該國對包裝解決方案的需求。

- 預計塑膠使用法規的加強將對市場產生重大影響。透過阻止使用不永續材料,英國政府同時提高了可回收塑膠的市場價值,培育了具有全球影響力的永續循環經濟。 2024年4月,英國推出CAPA(藥品初級包裝循環性加速器)舉措,制定並實施製藥設備和藥品包裝報廢回收戰略,在該國啟動可回收包裝解決方案。

- 在英國包裝市場上,包裝選擇的永續性和可負擔性之間的衝突變得越來越明顯。隨著消費者在環保選擇的經濟影響方面苦苦掙扎,更便宜、更不永續的選擇趨勢變得越來越普遍,影響了採用永續包裝解決方案日益增加的市場挑戰。

- 然而,COVID-19 疫情對市場產生了影響,市場上的一些公司開始轉向使用一次性塑膠。供應鏈不堪重負,難以滿足一次性塑膠包裝和醫療用品不斷成長的需求。塑膠需求的大幅成長可能會暫時改變向循環經濟轉型的短期努力和目標。除此之外,預計這也將為塑膠包裝生產鏈帶來壓力。此外,俄羅斯和烏克蘭之間的戰爭正在影響整個包裝生態系統。

英國包裝市場趨勢

食品領域預計將推動市場成長

- 加工食品的需求不斷增加以及輕質和軟包裝的日益普及正在推動市場發展,並在短期、中期和長期產生各種影響。由於消費者對產品品質的重視,冷凍食品包裝市場正在快速成長。生活方式的改變推動了英國對冷凍食品包裝的需求增加。

- 為了追求永續性,該國的食品製造商擴大用紙質產品取代塑膠產品,預計將推動市場成長。例如,2023年9月,永續包裝和紙張領域的全球領導者Mondi與屢獲殊榮的米供應商Veetee合作推出了英國首款紙盒乾米,標誌著食品包裝領域的市場成長。

- 立式袋預計將在整個預測期內保持標準包裝形式,因為它們能夠保持食品新鮮度並延長產品保存期限。此外,袋子的外觀美觀,增強了產品的行銷效果。由此,小袋包裝被廣泛採用作為其他形式的穩定替代品,預計在預測期內,其需求和客戶接受度將進一步提高。

- 在英國,永續性和可回收性在提高消費者對品牌的偏好方面發揮關鍵作用。為滿足市場對消費後回收 (PCR) 包裝解決方案日益成長的需求,軟包裝公司 ProAmpac 宣布推出其 ProActivePCR殺菌袋。此殺菌袋適用於包裝寵物食品和人類食品,符合 FDA 和 EU 在蒸餾應用中的食品接觸要求。殺菌袋由至少 30% 的消費後回收 (PCR) 包裝材料製成,並且使用最少的原生樹脂。這些巧妙的袋子也符合英國塑膠包裝稅(PPT)的規定。

- 在新冠疫情期間大幅成長並推動消費行為轉向線上訂餐行為後,網路食品銷售額的年變化率已達到疫情前的水平。 2023 年 12 月,Eviosys 重新啟動了位於剪切機旺蒂奇的研發中心,致力於成為食品業首選的永續包裝合作夥伴,展示了該國的市場需求。

PET(聚對苯二甲酸乙二醇酯)預計將佔據主要市場佔有率

- 在英國,隨著飲料公司增加可回收塑膠的使用,寶特瓶被廣泛應用於各行各業。食品和飲料市場是寶特瓶和容器的主要用戶之一。寶特瓶寶特瓶成本低、重量輕,其在食品、飲料、化妝品和藥品等各種終端用途的使用日益增多,推動了該國塑膠瓶市場的發展。

- 此外,新灌裝技術和耐熱寶特瓶的發展為市場提供了新的可能性和選擇。雖然寶特瓶已成為多個行業的標準,但聚乙烯 (PE) 瓶在飲料、化妝品、衛生產品和清潔劑領域佔據主導地位,這支持了國內市場的成長。

- 英國快速消費品品牌所有者對 PET 塑膠材料的需求仍然很高。 2024 年 5 月,回收技術公司 Polytag 任命英國零售商 M&S 為 Polytag Ecotrace 計畫的創始成員,該計畫旨在最佳化英國一次性塑膠包裝的追蹤和回收。 Polytag EcoTrace 計畫將在大量廢棄物回收中心部署 Polytag 的隱形紫外線標籤偵測設備,幫助該國回收寶特瓶。

- 寶特瓶市場正在見證瓶子設計的進步,以便更容易裝載到托盤上並運輸到超級市場,這表明市場對寶特瓶的需求。例如,2024 年 3 月,英國Aldi 推出了自有品牌的扁平再生 PET 葡萄酒瓶,據稱該瓶由 100% 再生 PET 製成,這表明該市場未來具有成長潛力。

- 根據英國國家統計局的報告,英國消費者在食品和非酒精飲料上的支出正在增加,這將支持對瓶子包裝的需求並推動PET的採用,這與可回收PET的需求和這種材料在飲料包裝中的優勢相一致。

英國包裝產業概況

英國包裝市場較為分散,由多家全球和地區參與者組成。目前,一些參與者在整體佔有率上佔據市場主導地位。憑藉顯著的市場佔有率,這些領先的公司正致力於擴大其終端用戶的基本客群。這些公司包括 Amcor PLC、DS Smith PLC、AptarGroup Inc.、Sealed Air Corporation 和 Sonoco Products Company,正在利用戰略合作計劃來增加市場佔有率和盈利。

- 2024 年 2 月歐洲造紙和包裝公司 DS Smith PLC 計劃在其位於英格蘭東南部的 Kemsley 再生紙廠投資約 6000 萬美元建設一條新的纖維準備生產線。這將使公司透過提高效率和節省成本而獲益。這表明供應商進行了投資以支持所研究市場的內部成長。

- 2023年11月,Amcor與Saputo Dairy UK在英國包裝獎中榮獲「年度最佳軟塑膠包裝」獎。這兩家公司因美國最受歡迎的起司品牌 Cathedral City 開發新的可回收碎起司包裝而獲得認可。這表明了該國對乳製品包裝的需求以及相關人員之間的合作,以在英國保持競爭力。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

- COVID-19 對包裝產業的影響

- 包裝永續性技術分析

- 全球包裝市場概況

第5章 市場動態

- 市場促進因素

- 千禧世代對消費品優質包裝的需求日益成長

- 電子商務包裝需求激增

- 軟包裝持續成長

- 市場限制

- 開發成本上升和回收意識增強

- 日益嚴重的環境問題

第6章 市場細分

- 按行業

- 食物

- 飲料

- 衛生保健

- 化妝品、個人護理和家居用品

- 工業

- 透過塑膠包裝

- 材料類型

- PE(聚乙烯)

- PP(聚丙烯)

- PVC(聚氯乙烯)

- PET(聚對苯二甲酸乙二醇酯)

- 其他材料類型

- 按類型

- 硬質塑膠包裝

- 瓶子和罐子

- 托盤和容器

- 其他產品類型

- 軟質塑膠包裝

- 袋子和包包

- 薄膜和包裝

- 其他產品類型

- 材料類型

- 依包裝材料類型

- 紙

- 紙板

- 瓦楞紙和箱板紙

- 其他類型

- 玻璃

- 金屬(罐、桶、蓋子、封蓋、散裝容器)

- 紙

第7章 競爭格局

- 公司簡介

- Amcor PLC

- DS Smith PLC

- Owens Illinois Inc.

- Crown Holdings Inc.

- Berry Global Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Graphic Packaging International LLC

- Greif Inc.

- Ball Corporation

- Westrock Company

- Silgan Holdings Inc.

- AptarGroup Inc.

- Huhtamaki Oyj

- Mondi Group

- Tetra Pak International SA

- Can-Pack UK Ltd

- Ardagh Group

第8章投資分析

第9章:市場的未來

The United Kingdom Packaging Market size is estimated at USD 60.94 billion in 2025, and is expected to reach USD 68.18 billion by 2030, at a CAGR of 2.27% during the forecast period (2025-2030).

Key Highlights

- The packaging market in the United Kingdom has been witnessing significant growth owing to increased manufacturing activities. In February 2024, Coca-Cola planned to temporarily remove labels from Sprite and Sprite Zero on-the-go bottles in a limited trial of "label-less" packaging for 500-ml bottles with an embossed logo on the front of the pack in the United Kingdom, which shows the demand for the packaging market in the country.

- The growth of e-commerce sales, increased demand from food and beverage manufacturers for eco-friendly and recyclable packaging, increasing demand for product personalization, and the growing industrial packaging sector are driving the growth of the packaging market in the country. In November 2023, the International Trade Administration reported that the United Kingdom has the third-largest e-commerce market in the world after China and the United States, which is expected to support the demand for packaging solutions in the country in the coming years.

- The increase in regulations for plastic use is anticipated to affect the market significantly. By disincentivizing the usage of unsustainable materials, the UK government is simultaneously incentivizing the market value of recyclable plastic, fostering a sustainable circular economy that will have global repercussions. In April 2024, the United Kingdom launched the Circularity in Primary Pharmaceutical Packaging Accelerator (CAPA) initiative to develop and implement strategies for the end-of-use recycling of medicinal devices and pharmaceutical packaging, fueling the country's recyclable packaging solutions.

- The conflict between sustainability and affordability in packaging choices has been increasingly evident in the UK packaging market. As consumers grapple with the financial implications of eco-friendly alternatives, a trend toward cheaper, non-sustainable options is becoming more prevalent, impacting a rising market challenge for adopting sustainable packaging solutions.

- However, with the COVID-19 pandemic affecting the market studied, multiple companies in the market shifted toward the usage of single-use plastics. Supply chains strained to meet a surge in demand for single-use plastic packaging and medical supplies. Such a significant spike in plastic demand is likely to lead to a temporary change in the short-term initiatives and goals of transitioning toward a circular economy. Apart from this, it is also expected to put pressure on the plastic packaging manufacturing chain. Furthermore, the war between Russia and Ukraine has an impact on the overall packaging ecosystem.

United Kingdom Packaging Market Trends

Food Segment Expected to Drive Market Growth

- The increasing demand for processed food and the growing adoption of lightweight, flexible packaging drive the market, with varying impacts over the short, medium, and long term. The market for frozen food packaging is witnessing an upsurge due to the country's consumer appreciation of product quality. The demand for frozen food packaging has increased in the United Kingdom due to changing lifestyles.

- The country's food manufacturers are increasingly replacing plastic-based products in line with their paper-based counterparts for sustainability, which is expected to fuel the market's growth. For instance, in September 2023, Mondi, a global leader in sustainable packaging and paper, launched paper-packed dry rice in the United Kingdom for the first time by collaborating with award-winning rice supplier Veetee, showing the market's growth in the food packaging segment.

- Stand-up pouches are anticipated to become a standard form of packaging throughout the forecast period due to their capacity to maintain the freshness of food products and increase product shelf life. Furthermore, the pouches also offer a great visible aesthetic, which adds to the product's marketing benefits. This has led to the wide adoption of pouches as a stable alternative to other formats and is expected to take further momentum in terms of demand and customer acceptance during the forecast period.

- In the United Kingdom, sustainability and recyclability play a significant role in raising consumer preference for brands. Responding to the expanded market demand for post-consumer recycled (PCR) packaging solutions, a flexible packaging company, ProAmpac, announced the launch of its ProActivePCR Retort pouches. The retort pouches are intended for pet and human food packaging and are both FDA and EU-compliant for food contact in retort applications. They provide packaging with a post-consumer recycled (PCR) content of 30% or more, minimizing the use of virgin resins. These inventive pouches also adhere to United Kingdom Plastics Packaging Tax regulations (PPT).

- The percentage change in annual internet food sales has reached a pre-pandemic level after a significant increase during the COVID-19 pandemic, which has raised consumer behavior to prefer online ordering of foods. In December 2023, Eviosys relaunched Eviosys's R&D center in Wantage, Oxfordshire, to become the food industry's sustainable packaging partner of choice, which shows the demand for the market in the country.

PET (Polyethylene Terephthalate) Expected to Hold Major Market Share

- Plastic bottles are widely used in various industries in the United Kingdom due to the beverage companies' growing use of recyclable plastics. The food and beverage market is one of the major users of plastic bottles and containers. The rising use of PET bottles drives the country's plastic bottle market due to their low cost and lightweight in various end-user applications, including food, beverage, cosmetics, and pharmaceuticals.

- Furthermore, newer filling technologies and the development of heat-resistant PET bottles provided new possibilities and options in the market. While PET bottles are standard in multiple segments, beverages, cosmetics, sanitary products, and detergents are largely sold in polyethylene (PE) bottles, which is supporting the market's growth in the country.

- PET plastic materials sustain high demand from FMCG brand owners in the United Kingdom. In May 2024, the recycling technology firm Polytag named the UK retailer M&S as a founding member of its Polytag Ecotrace Programme, an initiative set to optimize the tracing and recycling of single-use plastic packaging in the United Kingdom. The Polytag Ecotrace Programme would deploy a vast network of Polytag's invisible UV tag detection equipment in strategically chosen recycling centers that handle high volumes of waste, which would support the recycled PET bottles in the country.

- The market has been registering advancements in the design of bottles to make them easy to load onto pallets and transport to supermarkets, which shows the demand for PET bottles in the market. For instance, in March 2024, Aldi in the United Kingdom launched its own-brand flat recycled PET wine bottles, which it said are made from 100% recycled PET, showing the market's future growth potential.

- The Office for National Statistics (United Kingdom) reported that consumer spending on food and non-alcoholic beverages in the United Kingdom has been increasing, which would support the demand for bottle packaging and fuel PET adoptions in line with the demand for recyclable PET and the advantage of PET material in beverage packaging.

United Kingdom Packaging Industry Overview

The packaging market in the United Kingdom is fragmented and consists of several global and regional players. Some of the players currently dominate the market in terms of overall share. These major players with prominent market share focus on expanding their customer base across end users. These companies, such as Amcor PLC, DS Smith PLC, AptarGroup Inc., Sealed Air Corporation, and Sonoco Products Company, leverage strategic collaborative initiatives to increase their market share and profitability.

- February 2024: The European paper and packaging company DS Smith PLC planned to invest about USD 60 million in a new fiber preparation line at its Kemsley recycled paper mill in southeast England. This would enable the company to deliver returns through improved efficiency and reduced costs. This shows the investments by the market vendors to support their organic growth in the market studied.

- November 2023: Amcor and Saputo Dairy UK won 'Flexible Plastic Pack of the Year' at the UK Packaging Awards. The companies were recognized for developing new, recycle-ready grated cheese packaging for the nation's favorite cheese brand, Cathedral City. This shows the demand for dairy product packaging in the country and the collaborations among the stakeholders to be competitive in the United Kingdom.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Packaging Industry

- 4.5 Analysis of Technologies for Sustainability in Packaging

- 4.6 Overview of the Global Packaging Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand from the Millennials for Luxury Packaging for Consumer Goods

- 5.1.2 Soaring Demand for E-commerce Packaging

- 5.1.3 Flexible Packaging Continues to Grow Faster

- 5.2 Market Restraints

- 5.2.1 High Cost of Development and the Rising Concept of Recycling

- 5.2.2 The Rising Environmental Concerns

6 MARKET SEGMENTATION

- 6.1 By End-User Vertical

- 6.1.1 Food

- 6.1.2 Beverage

- 6.1.3 Healthcare

- 6.1.4 Cosmetics, Personal Care, and Household Care

- 6.1.5 Industrial

- 6.2 By Plastic Packaging

- 6.2.1 Material Type

- 6.2.1.1 PE (Polyethylene)

- 6.2.1.2 PP (Polypropylene)

- 6.2.1.3 PVC (Poly Vinyl Chloride)

- 6.2.1.4 PET (Polyethylene Terephthalate)

- 6.2.1.5 Other Material Types

- 6.2.2 By Type

- 6.2.2.1 Rigid Plastic Packaging

- 6.2.2.1.1 Bottles and Jars

- 6.2.2.1.2 Trays and Containers

- 6.2.2.1.3 Other Product Types

- 6.2.2.2 Flexible Plastic Packaging

- 6.2.2.2.1 Pouches & Bags

- 6.2.2.2.2 Films and Wraps

- 6.2.2.2.3 Other Product Types

- 6.2.1 Material Type

- 6.3 By Packaging Material Type

- 6.3.1 Paper

- 6.3.1.1 Carton Board

- 6.3.1.2 Containerboard and Linerboard

- 6.3.1.3 Other Types

- 6.3.2 Glass

- 6.3.3 Metal (Cans, Drums, Caps and Closures, and Bulk Containers)

- 6.3.1 Paper

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 DS Smith PLC

- 7.1.3 Owens Illinois Inc.

- 7.1.4 Crown Holdings Inc.

- 7.1.5 Berry Global Inc.

- 7.1.6 Sealed Air Corporation

- 7.1.7 Sonoco Products Company

- 7.1.8 Graphic Packaging International LLC

- 7.1.9 Greif Inc.

- 7.1.10 Ball Corporation

- 7.1.11 Westrock Company

- 7.1.12 Silgan Holdings Inc.

- 7.1.13 AptarGroup Inc.

- 7.1.14 Huhtamaki Oyj

- 7.1.15 Mondi Group

- 7.1.16 Tetra Pak International SA

- 7.1.17 Can-Pack UK Ltd

- 7.1.18 Ardagh Group

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025年Thermocol包裝全球市場報告2025年無塑膠包裝全球市場報告2025年全球包裝產品市場報告2025年全球包裝市場報告

2025年Thermocol包裝全球市場報告2025年無塑膠包裝全球市場報告2025年全球包裝產品市場報告2025年全球包裝市場報告 2032 年追蹤包裝市場預測:按產品類型、系統類型、技術、追蹤方法、最終用戶、地區進行的全球分析2032 年隔熱包裝市場預測:按產品類型、材料類型、功能、應用、最終用戶和地區進行的全球分析

2032 年追蹤包裝市場預測:按產品類型、系統類型、技術、追蹤方法、最終用戶、地區進行的全球分析2032 年隔熱包裝市場預測:按產品類型、材料類型、功能、應用、最終用戶和地區進行的全球分析 輕量化包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測2025年全球塑合板包裝市場報告再生材料包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測極簡包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

輕量化包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測2025年全球塑合板包裝市場報告再生材料包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測極簡包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測