|

市場調查報告書

商品編碼

2035079

UV固化印刷油墨:市場佔有率分析、產業趨勢與統計數據以及成長預測(2026-2031年)UV Cured Printing Inks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

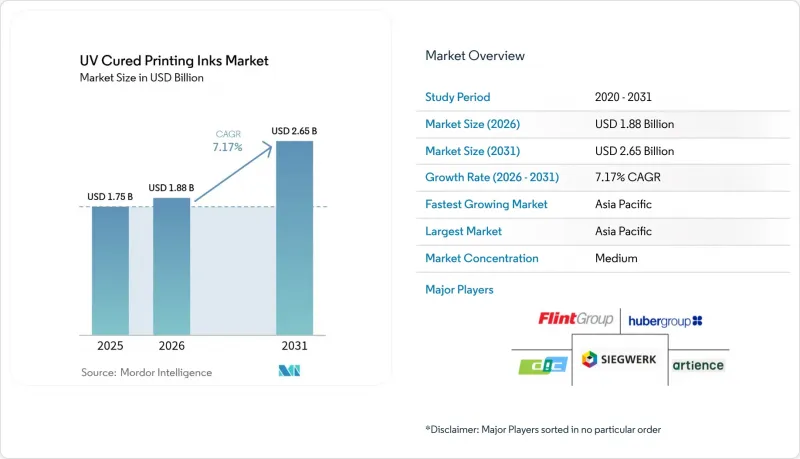

2025 年 UV 固化印刷油墨市場價值為 17.5 億美元,預計到 2031 年將達到 26.5 億美元,而 2026 年為 18.8 億美元,預測期(2026-2031 年)複合年成長率為 7.17%。

節能型LED固化技術可降低印刷機60-65%的能耗,同時無需維護汞燈並消除VOC(揮發性有機化合物)排放,是成長要素。隨著亞太地區、歐盟和北美地區食品接觸法規的日益嚴格,包裝加工商正加速採用低致敏性油墨。 OEM廠商推出無需新增資本投資即可將印刷速度提升30-50%的改裝LED系統,目標現有設備基數不斷擴大,進入門檻也隨之降低。同時,光引發劑劑的供應風險以及水性油墨和電子束(EB)固化油墨等替代技術的出現,給供應商帶來了競爭壓力,他們必須透過創新和柔軟性的採購方式來應對這些挑戰。

全球UV固化印刷油墨市場趨勢及洞察

數位印刷和噴墨印刷的需求不斷成長

客製印刷的普及使出版商能夠大幅降低倉儲成本,並滿足客戶對更快交貨時間的期望。 UV固化油墨無需印後乾燥時間,即可在塗佈紙和無塗布紙基材上呈現清晰的影像。隨著品牌將觸感元素融入數位宣傳活動,廣告信量正在復甦,這增加了對耐用、耐磨且能承受郵寄處理的UV印刷品的需求。FUJIFILM的專利展示了其在表面活性劑改性噴墨配方研發方面的強勁勢頭,該配方可減少色彩滲漏並提高光澤均勻性,進一步增強UV油墨與高速壓電噴頭的兼容性。擁有網路印刷平台的商業印刷公司正在抓住小批量、個人化訂單的商機,這些訂單受益於即時固化和更短的作業等待時間。儘管傳統出版物的發行量持續下降,但價值向可變數據和特殊材料的轉變正在為UV固化油墨市場的成長創造積極的動力。

包裝和標籤轉換器的擴展

在印尼、印度和越南,由於日常消費品(FMCG)區域需求不斷成長以及全球品牌供應鏈向近岸外包,加工商的產能正在擴張。新的印刷生產線通常採用LED UV或混合固化方法,以減少設置浪費並滿足工廠的ESG標準。對柔版印刷機的升級,例如Miracron的FLEXCEL NX平台,使加工商能夠在使用薄版和低油墨用量(適用於UV油墨配方)的情況下,實現與凹版印刷相媲美的視覺效果。 UV LED固化的節能優勢在品牌擁有者的永續發展評估中日益受到重視,促使加工商不斷創新技術。符合食品接觸法規和降低整體擁有成本(TCO)的雙重需求,正在鞏固包裝產業對UV固化印刷油墨市場的需求。

傳統商業印刷的衰退

隨著廣告主將預算轉向數位平台,報紙和雜誌的發行量持續下降,傳統UV膠印油墨的需求也隨之減少。未能轉型至包裝、標籤或高價值裝飾印刷的商業印刷商面臨印刷機運轉率下降的問題,直接導致油墨消耗量減少。雖然高利潤、短交貨期、小批量印刷在一定程度上緩解了收入下滑,但印刷量的下降仍在繼續,這一限制構成了結構性阻力。

細分市場分析

預計2025年,LED系統將佔據UV固化印刷油墨市場56.14%的佔有率,到2031年將維持9.13%的複合年成長率。這表明,這項技術正被優先考慮能源效率的加工商廣泛接受。改裝方案降低了資本投資門檻,使營運商能夠在保留現有印刷機平台的同時,大幅減少停機時間。較低的疊紙溫度可消除薄膜紙張變形,並允許更高的壓輥壓力,即使在超過18,000張/小時的印刷速度下也能保持套準精度。這些特性共同鞏固了LED在UV固化印刷油墨市場的主導地位。

在某些需要寬光譜來觸發陽離子光化學頻譜的寬幅印刷和絲網印刷應用中,弧光燈固化仍然佔有一席之地。然而,隨著近期高功率LED二極體功率密度達到25 W/cm²,傳統上在固化深度方面的差距正在縮小,並且由於混合型燈罩允許用戶在工作期間切換模式,這種轉變的步伐正在加快。隨著政府對汞的監管日益嚴格,弧光燈的經濟效益將進一步下降,進一步凸顯LED的優勢。

《UV固化印刷油墨市場報告》依固化製程(電弧固化和LED固化)、油墨類型(UV柔版油墨、UV膠印油墨、UV低能耗/LED膠印油墨等)、應用領域(包裝、商業和出版等)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

區域分析

預計到2025年,亞太地區將佔全球銷售額的48.05%,並在2031年之前以9.08%的複合年成長率成長。這主要得益於中國全國範圍內強制執行GB 4806.14-2023標準的最後期限,以及印度強制執行IS:15495標準,該標準限制了食品包裝油墨中甲苯的使用。區域領導者,例如UFlex,正在推出可黏附於金屬化薄膜的聚酯丙烯酸酯類產品,使加工商能夠在單一製程中同時實現阻隔性和遷移性目標。政府對節能設備成本最高可達30%的補貼獎勵,進一步加速了LED UV技術在新凹版和柔版印刷廠的應用,鞏固了該地區在UV固化印刷油墨市場的領先地位。

北美擁有雄厚的技術基礎,早在2016年,一些先驅就開始使用LED設備。由於美國環保署(EPA)的建議以及《通貨膨脹削減法案》提供的清潔製造補貼,2024年至2025年間,眾多設備升級項目獲得了資金支持。樹脂和添加劑產能的提升有助於穩定國內油墨製造商的供應,例如,路博潤公司在俄亥俄州將其Solsperse超分散劑的產量增加了一倍。

儘管中東、非洲和南美洲目前僅佔銷售量的一小部分,但隨著包裝製造商為滿足出口客戶的審核要求而從溶劑型生產線過渡到LED平台,這些市場蘊藏著巨大的成長潛力。巴西標籤印刷商採用混合UV-EB柔版印刷生產線的趨勢凸顯了新技術的快速發展,如果宏觀經濟情勢趨於穩定,這些新技術有望縮短實施週期。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 數位印刷和噴墨印刷的需求不斷成長

- 包裝和標籤公司的擴張

- 加強揮發性有機化合物和永續性法規

- 快速過渡到節能型LED紫外線系統

- 食品和藥品包裝中低遷移油墨的應用

- 市場限制因素

- 傳統商業印刷的衰退

- 與水性及電子束固化體系的競爭

- 光引發劑供應鏈波動(中國監管力道加強)

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 透過固化過程

- 電弧固化

- LED固化

- 按墨水類型

- UV柔版印刷油墨

- UV膠印油墨

- UV低耗能/LED膠印油墨(不含UV膠印油墨)

- UV網版印刷油墨

- 其他類型的UV固化印刷油墨

- 透過使用

- 包裝

- 商業/出版

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、合資、合作)

- 市佔率(%)/排名分析

- 公司簡介

- ALTANA

- APV Engineered Coatings

- artience Co. Ltd.(TOYO INK CO., LTD.)

- Avery Dennison Corporation

- DIC Corporation

- Flint Group

- FUJIFILM Corporation

- Huber Group

- Marabu GmbH & Co. KG

- MIMAKI ENGINEERING CO., LTD.

- Nazdar

- SAKATA INX CORPORATION

- Siegwerk Druckfarben AG & Co. KGaA

- T&K TOKA Corporation

- TOKYO PRINTING INK MFG. CO., LTD.

- Van Son Ink Corporation

第7章 市場機會與未來展望

The UV Cured Printing Inks Market size was valued at USD 1.75 billion in 2025 and estimated to grow from USD 1.88 billion in 2026 to reach USD 2.65 billion by 2031, at a CAGR of 7.17% during the forecast period (2026-2031).

Energy-efficient LED curing, which lowers press power consumption by 60-65% while removing mercury lamp maintenance and VOC emissions, is the primary growth driver. Packaging converters are accelerating adoption because low-migration formulations meet tightening food-contact rules in Asia-Pacific, the European Union, and North America. As OEMs release retrofit LED systems that raise press speeds 30-50% without new capital outlay, the addressable installed base widens and barriers to entry fall. At the same time, photoinitiator supply risks and emerging water-based or EB-curable alternatives inject competitive pressure that suppliers must manage through innovation and sourcing agility.

Global UV Cured Printing Inks Market Trends and Insights

Growing Demand from Digital and Inkjet Printing

Print-on-demand adoption lets publishers slash warehousing expenses and meet rapid turnaround expectations, and UV-cured inks enable crisp imagery on coated and uncoated substrates without post-press drying delays. Direct mail volumes are rebounding as brands integrate tactile pieces with digital campaigns, reinforcing demand for durable, scuff-resistant UV impressions that withstand postal handling. Research and development momentum is visible in FUJIFILM's patent covering surfactant-modified inkjet formulations that reduce inter-color bleeding and heighten gloss uniformity, an advance that strengthens UV compatibility with high-speed piezo heads. Commercial shops that add web-to-print storefronts tap short-run personalized jobs where instant curing shortens job queues. Although legacy publication volumes keep shrinking, the value shift to variable-data and specialty substrates produces a net positive pull on UV-cured printing inks market growth.

Expansion of Packaging and Label Converters

Converter capacity is rising across Indonesia, India, and Vietnam as regional FMCG demand climbs and global brands nearshore supply chains; each new press line typically specifies LED UV or hybrid curing to cut make-ready waste and satisfy factory ESG benchmarks. Flexographic press upgrades, exemplified by Miraclon's FLEXCEL NX platform, let converters match gravure aesthetics while using thinner plates and lower ink laydowns that suit UV formulations. Brand-owner sustainability scorecards increasingly credit energy savings from UV LED curing, nudging converters toward technology refresh. The dual need to meet food-contact rules and lower total cost of ownership cements packaging's pull on the UV-cured printing inks market.

Decline of Conventional Commercial Printing

Newspaper and magazine pagination keeps sliding as advertisers channel budgets into digital platforms, eroding legacy UV offset ink demand. Commercial printers that fail to pivot toward packaging, labels, or value-added embellishments face press under-utilization that directly reduces ink consumption. While high-margin short runs temper revenue loss, volume attrition persists, marking this restraint as a structural headwind.

Other drivers and restraints analyzed in the detailed report include:

- Stricter VOC/Sustainability Regulations

- Rapid Shift to Energy-Efficient LED UV Systems

- Competition from Water-Based and EB-Curable Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

LED systems accounted for 56.14% of the UV-cured printing inks market size in 2025 and are forecast to post a 9.13% CAGR to 2031, underlining the technology's broad acceptance among converters focused on energy metrics. The retrofit option lowers capital hurdles, letting operators preserve existing press platforms while sharply reducing downtime. Lower stack temperatures eliminate sheet distortion on thin films and enable higher nip pressures that maintain registration accuracy at press speeds above 18,000 sph. These attributes collectively sustain LED's leadership in the UV-cured printing inks market.

Arc-lamp curing retains a toehold in certain wide-web and screen-printing applications that need broadband spectra to trigger cationic photochemistry. However, recent high-output LED diodes reaching 25 W/cm2 narrow the former gap in cure depth, and hybrid lamp housings let users toggle modes mid-shift, hastening the migration curve. As government restrictions on mercury escalate, arc-lamp economics will further erode, reinforcing LED's dominant trajectory.

The UV-Cured Printing Inks Report is Segmented by Curing Process (Arc Curing and LED Curing), Ink Type (UV Flexo Inks, UV Offset Inks, UV Low Energy/LED Offset Inks, and More), Application (Packaging, Commercial and Publication, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 48.05% of 2025 revenue and is tracking a 9.08% CAGR to 2031, led by China's nationwide GB 4806.14-2023 compliance deadline and India's IS:15495 enforcement that restricts toluene in food packaging inks. Local leaders such as UFlex have introduced polyester acrylates that bond to metallized films, enabling converters to meet both barrier and migration goals in a single pass. Government incentives that refund up to 30% of energy-saving equipment costs further accelerate LED UV adoption across new gravure and flexo halls, cementing the region's pull on the UV-cured printing inks market.

North America holds a technology-rich base where early adopters embraced LED units as early as 2016. The U.S. EPA's endorsement and the Inflation Reduction Act's clean-manufacturing credits financed numerous retrofits during 2024-25. Resin and additive capacity expansions, exemplified by Lubrizol's doubling of Solsperse hyperdispersant output in Ohio, bolster supply assurance for domestic ink makers.

The Middle East and Africa, and South America contribute modest volume shares today, yet represent latent upside as packaging converters migrate from solvent lines to LED platforms to comply with export customer audits. Brazilian label printers installing hybrid UV-EB flexo lines attest to an emerging technology leapfrog that could compress adoption timelines once macroeconomic conditions stabilize.

- ALTANA

- APV Engineered Coatings

- artience Co. Ltd. (TOYO INK CO., LTD.)

- Avery Dennison Corporation

- DIC Corporation

- Flint Group

- FUJIFILM Corporation

- Huber Group

- Marabu GmbH & Co. KG

- MIMAKI ENGINEERING CO., LTD.

- Nazdar

- SAKATA INX CORPORATION

- Siegwerk Druckfarben AG & Co. KGaA

- T&K TOKA Corporation

- TOKYO PRINTING INK MFG. CO., LTD.

- Van Son Ink Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand from Digital and Inkjet Printing

- 4.2.2 Expansion of Packaging and Label Converters

- 4.2.3 Stricter VOC/Sustainability Regulations

- 4.2.4 Rapid Shift to Energy-Efficient LED UV Systems

- 4.2.5 Adoption of Low-Migration Inks in Food and Pharma Packs

- 4.3 Market Restraints

- 4.3.1 Decline of Conventional Commercial Printing

- 4.3.2 Competition from Water-Based and EB-Curable Systems

- 4.3.3 Photoinitiator Supply-Chain Volatility (China Clampdowns)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Curing Process

- 5.1.1 Arc Curing

- 5.1.2 LED Curing

- 5.2 By Ink Type

- 5.2.1 UV Flexo Inks

- 5.2.2 UV Offset Inks

- 5.2.3 UV Low Energy/LED Offset Inks (Except UV Offset Inks)

- 5.2.4 UV Screen Printing Inks

- 5.2.5 Other UV Cured Printing Inks Type

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.2 Commercial and Publication

- 5.3.3 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Mergers and Acquisitions, JV, Partnerships)

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ALTANA

- 6.4.2 APV Engineered Coatings

- 6.4.3 artience Co. Ltd. (TOYO INK CO., LTD.)

- 6.4.4 Avery Dennison Corporation

- 6.4.5 DIC Corporation

- 6.4.6 Flint Group

- 6.4.7 FUJIFILM Corporation

- 6.4.8 Huber Group

- 6.4.9 Marabu GmbH & Co. KG

- 6.4.10 MIMAKI ENGINEERING CO., LTD.

- 6.4.11 Nazdar

- 6.4.12 SAKATA INX CORPORATION

- 6.4.13 Siegwerk Druckfarben AG & Co. KGaA

- 6.4.14 T&K TOKA Corporation

- 6.4.15 TOKYO PRINTING INK MFG. CO., LTD.

- 6.4.16 Van Son Ink Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

凹版印刷油墨市場:2026-2032年全球市場預測(依油墨類型、形態、承印類型、包裝、顏色及最終用途產業分類)

凹版印刷油墨市場:2026-2032年全球市場預測(依油墨類型、形態、承印類型、包裝、顏色及最終用途產業分類) 全球網版印刷油墨市場規模、佔有率、趨勢及成長分析報告(2026-2034年)印刷油墨市場:2026-2032年全球市場預測(依產品類型、印刷製程、樹脂類型、銷售管道和應用分類)

全球網版印刷油墨市場規模、佔有率、趨勢及成長分析報告(2026-2034年)印刷油墨市場:2026-2032年全球市場預測(依產品類型、印刷製程、樹脂類型、銷售管道和應用分類) 印刷油墨市場分析及預測(至2035年):類型、產品類型、技術、應用、材料類型、形態、最終用戶、製程、功能

印刷油墨市場分析及預測(至2035年):類型、產品類型、技術、應用、材料類型、形態、最終用戶、製程、功能 美國印刷油墨:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球UV固化印刷油墨市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球印刷油墨市場規模、佔有率、趨勢和成長分析報告(2026-2034年)凹版印刷油墨全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

美國印刷油墨:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球UV固化印刷油墨市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球印刷油墨市場規模、佔有率、趨勢和成長分析報告(2026-2034年)凹版印刷油墨全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球凹版印刷油墨市場報告2026年全球印刷油墨市場報告

2026年全球凹版印刷油墨市場報告2026年全球印刷油墨市場報告