|

市場調查報告書

商品編碼

1939074

美國印刷油墨:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United States Printing Inks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

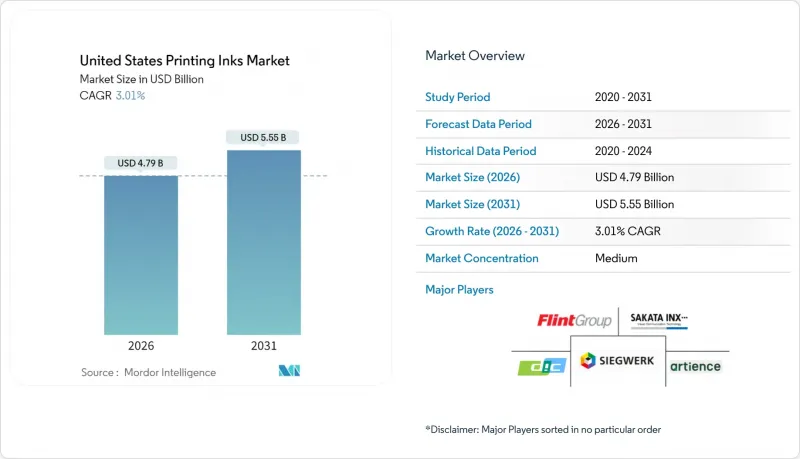

據估計,到 2026 年,美國印刷油墨市場價值將達到 47.9 億美元,高於 2025 年的 46.5 億美元。

預計到 2031 年將達到 55.5 億美元,2026 年至 2031 年的複合年成長率為 3.01%。

在整體成長速度較為溫和的背景下,包裝、數位和永續發展相關領域的快速成長超過了持續萎縮的商業印刷需求。強勁的需求主要來自電商瓦楞紙箱、食品飲料標籤和小批量促銷品,這些都需要高利潤的特殊油墨。品牌所有者也願意為低遷移的UV/LED油墨、水性油墨和生物基化學品支付溢價,這些產品有助於企業實現永續發展目標,從而為配方師帶來更高的利潤。供應側的趨勢受到顏料和樹脂產能回流、擺脫對亞洲關稅依賴以及中端供應商持續整合的影響。揮發性有機化合物(VOC)法規和職場安全壓力正在加速向能量固化和水性系統的轉變,而數位印刷機透過消除製版和設定廢棄物,正在重塑成本曲線。

美國印刷油墨市場趨勢與洞察

數位標籤和包裝印刷機的需求不斷成長

噴墨印刷機省去了製版和相關的設置成本,使加工商能夠盈利生產數百個SKU,而不是數萬個。品牌所有者正在利用噴墨印刷的柔軟性,例如限量版設計、區域語言版本和緊急個性化客製化,而這些在傳統的膠印中是無法盈利的。 UV固化噴墨油墨可瞬間固化,即使在非多孔薄膜上也能保持色彩一致性,價格比普通熱固型油墨高出兩到三倍。印刷機製造商不斷改進,致力於提高印刷寬度和墨滴定位精度,從而形成良性循環,即使印刷通道總數減少,油墨用量也能增加。能夠保證噴嘴友善黏度、低泡沫和穩定分散性的供應商,正在成為大型加工工廠安裝的數位印刷機設備的多年首選供應商。

國內按需印刷圖書的復興

圖書出版商過去為了利用膠印的經濟優勢而被迫加印,如今卻將未售出的庫存視為營運資金的負擔。高速噴墨生產線與全自動裝訂線結合,幾分鐘內即可生產300頁的小說,從而實現單冊補貨。教育機構正在採用這種模式製作客製化教學資料包,而自出版作者也找到了一個風險極低的實體通路。能夠提供濃郁黑色、減少輕薄紙張滲墨以及適用於裝訂的耐磨油墨的製造商,正受到客製印刷網路的青睞。該行業正在吸收雜誌業萎縮後留下的產能,並透過夜間運作維持老舊商業印刷機的運轉,以減少傳統印刷廠的裁員。

廣告支出轉向社群媒體與連網電視

隨著連網電視廣告曝光率變得可即時衡量和精準投放,美國行銷人員已縮減了印刷預算。預計到2024年,雜誌和產品目錄的發行量將再下降9%,進而導致輪轉印刷油墨的需求也相應下降。印刷廠產能過剩迫使中小型印刷企業破產或被迫合併,導致通用熱固型油墨的基本客群萎縮。倖存的印刷企業正轉向包裝和標牌領域,但對操作人員進行再培訓和改造印刷機需要大量資金籌措。油墨製造商在傳統商業印刷領域正面臨訂單量下降和應收帳款週期延長的困境,導致整體收入成長放緩。

細分市場分析

截至2025年,油基產品在美國印刷油墨市場仍佔據40.05%的佔有率,主要得益於企業行銷材料和高階產品目錄採用膠印製程。同時,水性化學產品在瓦楞紙箱和折疊紙盒生產線中市場佔有率不斷擴大,因為這些領域對低VOC含量有嚴格的要求。溶劑型油墨在工業圖形這一細分市場仍然至關重要,因為該領域對油墨的耐磨性要求極高。包括電子束油墨、網版印刷油墨和導電油墨在內的「其他類型」美國印刷油墨市場規模以5.02%的複合年成長率高速成長。

數位轉型正在重塑產品組合的經濟格局。 UV和LED油墨雖然產量佔比仍不到10%,但由於其每公斤成本是普通漿料油墨的兩倍,因此貢獻利潤率最高。用於儀錶板感測器薄膜和軟性RFID的導電銀箔漿料,價格約為50萬美元/公斤,儘管產量不高,卻對企業利潤產生了顯著影響。擁有卓越流變控制和亞微米顆粒技術專長的供應商正在電子產品OEM廠商中佔據安全隔離網閘地位,從而設置了很高的進入門檻。隨著品牌所有者採用循環經濟指標來區分其消費產品,預計在預測期內,生物基介質和新型無金屬顏料將從石油基系統中進一步奪取市場佔有率。

美國印刷油墨市場報告按類型(溶劑型、水性、油性、UV、UV LED 及其他)、印刷過程(捲筒紙膠印、單張紙膠印、柔版印刷、凹版印刷及其他)和應用領域(包裝、商業印刷出版、紡織品及其他)進行細分。市場預測以價值(美元)和銷售量(單位)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 數位標籤和包裝印刷機的需求不斷成長

- 國內按需印刷圖書的復興

- 電子商務推動了瓦楞紙板需求的成長。

- 品牌擁有者轉向低遷移性紫外線/LED固化樹脂

- 生物基樹脂的創新縮小了價格差距

- 市場限制

- 廣告支出轉向社群媒體與連網電視

- 日益嚴格的美國職業安全與健康管理局 (OSHA) 和各州揮發性有機化合物 (VOC) 法規限制了溶劑的使用。

- 中美貿易摩擦導致顏料供應面臨風險

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模和成長預測(價值和數量)

- 按類型

- 溶劑型

- 水溶液

- 油膩的

- UV

- UV LED

- 其他類型(EB油墨、網版印刷油墨、導電油墨)

- 透過印刷過程

- 膠印捲筒印刷

- 膠印(單張紙印刷)

- 柔版印刷

- 凹版印刷

- 數位印刷

- 其他流程

- 透過使用

- 包裝

- 硬包裝

- 紙板容器

- 瓦楞紙箱

- 硬質塑膠容器

- 金屬罐

- 其他

- 軟包裝

- 標籤

- 其他包裝

- 硬包裝

- 商業印刷/出版

- 紡織品

- 其他

- 包裝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Altana

- American Inks & Technology

- Avient Corporation

- Central Ink Corporation

- DIC Corporation(Sun Chemical)

- Flint Group

- FUJIFILM Corporation

- Hubergroup Deutschland GmbH

- Marabu GmbH & Co. KG

- Nazdar

- Polymeric Group

- Polytex Environmental Inks

- Precision Ink Corporation

- RA Kerley Ink Engineers Inc.

- Sakata Inx Corporation

- SICPA Holding SA

- Siegwerk Druckfarben AG & Co. KGaA

- Spring Coating Systems

- Superior Printing Ink Co.

- Toyo Ink Co. Ltd(artience Co. Ltd)

- Wikoff Color Corporation

- Zeller+Gmelin

第7章 市場機會與未來展望

United States Printing Inks Market market size in 2026 is estimated at USD 4.79 billion, growing from 2025 value of USD 4.65 billion with 2031 projections showing USD 5.55 billion, growing at 3.01% CAGR over 2026-2031.

Moderate growth hides rapid substitution effects as packaging, digital, and sustainability-linked niches outpace still-shrinking commercial print volumes. Demand resilience stems from e-commerce corrugated boxes, food and beverage labels, and short-run promotional items that all require higher-margin specialty formulations. Formulator margins benefit from the premium that brand owners pay for low-migration UV/LED, water-based, and bio-derived chemistries that support corporate sustainability targets. Supply-side dynamics are shaped by the onshoring of pigment and resin capacity, tariff-driven diversification away from Asia, and steady consolidation among mid-tier suppliers. Regulatory pressure on volatile organic compounds and workplace safety continues to accelerate the shift toward energy-curable and water-based systems, while digital presses rewrite cost curves by eliminating plates and makeready waste.

United States Printing Inks Market Trends and Insights

Growing Demand from Digital Label and Packaging Presses

Inkjet presses remove plates and associated setup costs, letting converters profitably produce SKU-proliferated runs measured in hundreds rather than tens of thousands. Brand owners exploit the agility for limited-edition designs, regional language versions and late-stage personalization that would cripple conventional offset economics. UV-curable inkjet chemistries cure instantly, maintain color consistency on non-porous films, and command price points 2-3 times higher than commodity heatset alternatives. Press OEMs iterate toward wider print bars and faster drop-placement accuracy, creating a virtuous cycle that lifts ink volumes even as overall lane counts fall. Suppliers able to guarantee nozzle-friendly viscosity, low foam, and stable dispersion secure multi-year preferred-supplier status with digital press fleets that now populate every major converter plant.

Resurgent Domestic On-Demand Book Printing

Book publishers, once forced to over-print to exploit offset economies, now view unsold inventory as a working-capital drag. High-speed inkjet lines paired with fully automated binding finish a 300-page novel in minutes, allowing replenishment in batches of one. Educational institutions embrace the model for custom course packs, while self-publishers find a risk-free path to physical distribution. Ink makers that deliver deep black density, reduced feathering on lightweight stocks, and binding-friendly rub resistance gain preferred approval from print-on-demand networks. The segment keeps older commercial presses running at night, absorbing capacity vacated by magazine decline and thereby slowing employment attrition in legacy plants.

Advertising Spend Shift to Social and CTV

U.S. marketers tilted budgets away from print as connected-TV impressions became addressable and measurable in real time. Magazine and catalog volumes fell another 9% in 2024, taking web offset ink demand down in lockstep. Surplus pressroom capacity forced smaller printers into bankruptcy or fire-sale mergers, eroding the customer base for commodity heatset blends. Surviving shops pivot to packaging and signage, yet retraining operators and retooling presses require capital that many cannot access. Ink makers see shrinking order sizes and longer receivable cycles in the legacy commercial segment, dampening overall revenue growth.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce-Driven Corrugated Volume Growth

- Biobased Resin Breakthroughs Lowering Price Gap

- OSHA and State VOC-Caps Tightening Solvent Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oil-based products retained 40.05% of the United States printing inks market share in 2025, thanks to entrenched offset workflows in corporate marketing collateral and high-end catalogs. Water-based chemistries captured incremental share in corrugated and folding carton lines that favor low-VOC compliance, while solvent blends remained critical for niche industrial graphics needing extreme abrasion resistance. The United States printing inks market size for Other Types, including electron beam, screen, and conductive formulations, expanded at a brisk 5.02% CAGR.

Digital disruption reshapes product-mix economics. UV and LED variants, though still under 10% by tonnage, generate the highest contribution margins thanks to per-kilo pricing that can double commodity paste inks. Conductive silver-flake pastes priced near USD 500 kg underpin dashboard sensor films and flexible RFID, creating an outsized revenue impact despite low volume. Suppliers with strong rheology control and sub-micron particle expertise command gatekeeper status with electronics OEMs, erecting formidable entry barriers. Over the forecast horizon, bio-based vehicles and novel metal-free pigments are expected to pull further share from petroleum-derived systems as brand owners embrace circular-economy scorecards to differentiate consumer offerings.

The United States Printing Inks Report is Segmented by Type (Solvent-Based, Water-Based, Oil-Based, UV, UV LED, and Other Types), Printing Process (Lithographic Web Printing, Lithographic Sheetfed Printing, Flexographic Printing, Gravure Printing, and More), Application (Packaging, Commercial and Publication, Textiles, and Others). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Altana

- American Inks & Technology

- Avient Corporation

- Central Ink Corporation

- DIC Corporation (Sun Chemical)

- Flint Group

- FUJIFILM Corporation

- Hubergroup Deutschland GmbH

- Marabu GmbH & Co. KG

- Nazdar

- Polymeric Group

- Polytex Environmental Inks

- Precision Ink Corporation

- R. A. Kerley Ink Engineers Inc.

- Sakata Inx Corporation

- SICPA Holding SA

- Siegwerk Druckfarben AG & Co. KGaA

- Spring Coating Systems

- Superior Printing Ink Co.

- Toyo Ink Co. Ltd (artience Co. Ltd)

- Wikoff Color Corporation

- Zeller+Gmelin

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand from Digital Label and Packaging Presses

- 4.2.2 Resurgent Domestic On-Demand Book Printing

- 4.2.3 E-Commerce-Driven Corrugated Volume Growth

- 4.2.4 Brand-Owner Migration to Low-Migration UV/LED Curables

- 4.2.5 Biobased Resin Breakthroughs Lowering Price Gap

- 4.3 Market Restraints

- 4.3.1 Advertising Spend Shifts to Social and CTV

- 4.3.2 OSHA and State VOC-Caps Tightening Solvent Use

- 4.3.3 Pigment Supply Risk from China-US Trade Tensions

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Type

- 5.1.1 Solvent-based

- 5.1.2 Water-based

- 5.1.3 Oil-based

- 5.1.4 UV

- 5.1.5 UV LED

- 5.1.6 Other Types (EB Inks, and Screen Printing Inks and Conductive Inks)

- 5.2 By Printing Process

- 5.2.1 Lithographic Web Printing

- 5.2.2 Lithographic Sheetfed Printing

- 5.2.3 Flexographic Printing

- 5.2.4 Gravure Printing

- 5.2.5 Digital Printing

- 5.2.6 Other Process

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.1.1 Rigid Packaging

- 5.3.1.1.1 Paperboard Containers

- 5.3.1.1.2 Corrugated Boxes

- 5.3.1.1.3 Rigid Plastic Containers

- 5.3.1.1.4 Metal Cans

- 5.3.1.1.5 Others

- 5.3.1.2 Flexible Packaging

- 5.3.1.3 Labels

- 5.3.1.4 Other Packaging

- 5.3.1.1 Rigid Packaging

- 5.3.2 Commercial and Publication

- 5.3.3 Textiles

- 5.3.4 Others

- 5.3.1 Packaging

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Altana

- 6.4.2 American Inks & Technology

- 6.4.3 Avient Corporation

- 6.4.4 Central Ink Corporation

- 6.4.5 DIC Corporation (Sun Chemical)

- 6.4.6 Flint Group

- 6.4.7 FUJIFILM Corporation

- 6.4.8 Hubergroup Deutschland GmbH

- 6.4.9 Marabu GmbH & Co. KG

- 6.4.10 Nazdar

- 6.4.11 Polymeric Group

- 6.4.12 Polytex Environmental Inks

- 6.4.13 Precision Ink Corporation

- 6.4.14 R. A. Kerley Ink Engineers Inc.

- 6.4.15 Sakata Inx Corporation

- 6.4.16 SICPA Holding SA

- 6.4.17 Siegwerk Druckfarben AG & Co. KGaA

- 6.4.18 Spring Coating Systems

- 6.4.19 Superior Printing Ink Co.

- 6.4.20 Toyo Ink Co. Ltd (artience Co. Ltd)

- 6.4.21 Wikoff Color Corporation

- 6.4.22 Zeller+Gmelin

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

凹版印刷油墨市場:2026-2032年全球市場預測(依油墨類型、形態、承印類型、包裝、顏色及最終用途產業分類)

凹版印刷油墨市場:2026-2032年全球市場預測(依油墨類型、形態、承印類型、包裝、顏色及最終用途產業分類) 2034年油墨印刷市場預測-按產品類型、化學分類、最終用途產業、通路和地區分類的全球分析

2034年油墨印刷市場預測-按產品類型、化學分類、最終用途產業、通路和地區分類的全球分析 凹版印刷油墨市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

凹版印刷油墨市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球網版印刷油墨市場規模、佔有率、趨勢及成長分析報告(2026-2034年)印刷油墨市場:2026-2032年全球市場預測(依產品類型、印刷製程、樹脂類型、銷售管道和應用分類)

全球網版印刷油墨市場規模、佔有率、趨勢及成長分析報告(2026-2034年)印刷油墨市場:2026-2032年全球市場預測(依產品類型、印刷製程、樹脂類型、銷售管道和應用分類) 印刷油墨市場分析及預測(至2035年):類型、產品類型、技術、應用、材料類型、形態、最終用戶、製程、功能全球UV固化印刷油墨市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球印刷油墨市場規模、佔有率、趨勢和成長分析報告(2026-2034年)凹版印刷油墨全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

印刷油墨市場分析及預測(至2035年):類型、產品類型、技術、應用、材料類型、形態、最終用戶、製程、功能全球UV固化印刷油墨市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球印刷油墨市場規模、佔有率、趨勢和成長分析報告(2026-2034年)凹版印刷油墨全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球凹版印刷油墨市場報告

2026年全球凹版印刷油墨市場報告