|

市場調查報告書

商品編碼

1640491

熱噴塗:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Thermal Spray - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

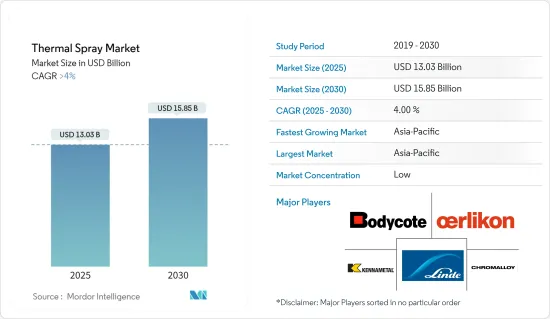

2025 年熱噴塗市場規模預計為 130.3 億美元,預計到 2030 年將達到 158.5 億美元,預測期內(2025-2030 年)的複合年成長率將超過 4%。

熱噴塗市場受到了COVID-19疫情的負面影響。最初,停工和供應鏈中斷減緩了製造活動,暫時減少了對熱噴塗料的需求。然而,隨著各行業採用新規範並更加重視衛生和保護,醫療保健、汽車和航太等產業對熱噴塗塗層的需求不斷成長。

主要亮點

- 熱噴塗陶瓷塗層在醫療設備中的日益普及、熱噴塗塗層在航太工業中的應用不斷增加以及硬鉻塗層的替代是推動熱噴塗市場需求的一些因素。

- 然而,有關製程可靠性和一致性的問題,以及最近出現的硬質三價鉻塗層,可能會阻礙市場成長。

- 石油和天然氣行業對熱噴塗的需求不斷增加、熱噴塗處理材料的回收利用以及熱噴塗技術(冷噴塗製程)的進步預計將在未來幾年為市場提供豐厚的成長機會。

- 預計預測期內亞太地區將主導熱噴塗市場。

熱噴塗市場趨勢

航太業可望主導市場

- 航太零件經常暴露在惡劣的環境中,包括高溫、腐蝕性化學物質和極端天氣條件。熱噴塗塗層可有效防止腐蝕,並延長渦輪葉片、引擎零件和機身等關鍵零件的使用壽命。

- 熱噴塗塗層為航太零件提供輕量化解決方案,有助於提高燃油效率和整體飛機性能。具有客製化特性的塗層可以取代較重的材料,同時保持結構完整性。

- 航太業正在經歷快速的技術進步和創新,從而帶來飛機製造業的繁榮。根據波音《2023-2042 年商用飛機展望》,隨著國際旅行復甦和國內旅行恢復到疫情前的水平,該公司預計到 2042 年全球對新型商用噴射機的需求將達到 48,575 架。

- 根據國際航空旅客協會的數據,2023年8月國內民航機客運量比疫情前增加了9.2%。空中交通量的增加可能會刺激對民航機的需求,這反過來可能會在預測期內推動對黏合劑的需求。

- 全球領先的飛機製造商空中巴士公司將於2023年交付735架民航機,與前一年同期比較成長11%。

- 預計上述因素將在預測期內推動航太工業對熱噴塗的需求。

亞太地區佔市場主導地位

- 亞太地區正經歷快速工業化,尤其是中國、印度、日本和韓國等國家。該地區蓬勃發展的製造業,包括汽車、航太、電子和能源,正在推動對可提高零件性能和耐用性的熱噴塗塗層的需求。

- 亞太地區各國政府正大力投資交通、能源和建築等基礎建設計劃。熱噴塗塗層可保護關鍵基礎設施組件免受腐蝕、磨損和侵蝕,延長其使用壽命並降低維護成本。

- 中國是世界上最大的飛機製造國之一,根據中國民航局的數據,中國也是國內航空客運市場。此外,還有超過200家小型飛機零件製造商,零件及組裝產業正在快速成長。

- 中國是全球最大的電子產品製造基地。智慧型手機、電視、有線電視、行動電腦、遊戲機和其他家用電器等電子產品都在中國積極生產。根據CEIC統計,2023年12月中國電子產品出口額為216.3億美元。

- 2023年,韓國累計獲得外資將達188億美元,與前一年同期比較成長3.4%。其中,電子業投資額佔比最大,達30億美元,成為頭部小型產業。

- 中國是世界上最大的鋼鐵生產國之一。官方數據顯示,2023年前11個月,原鋼產量達9.5214億噸,年增1.5%。

- 印度汽車工業在技術進步和宏觀經濟擴張中發揮著至關重要的作用。根據印度汽車工業協會(SIAM)統計,2023 年 4 月至 2024 年 3 月期間汽車銷量達到 23,853,463 輛,較 23 會計年度同期的 21,204,846 輛成長 12.5%。

- 由於上述因素,預計該地區將在預測期內佔據市場主導地位。

熱噴塗產業概況

熱噴塗市場比較分散。主要企業(不分先後順序)包括 OC Oerlikon Management AG、Linde PLC(Praxair ST Technologies Inc.)、Chromalloy Gas Turbine LLC、Bodycote 和 Kennametal Inc.

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 熱噴塗塗層在醫療設備的應用不斷擴大

- 熱噴塗陶瓷塗層越來越受歡迎

- 硬鉻塗層的替代品

- 熱噴塗塗料在航太工業的應用日益廣泛

- 限制因素

- 硬質三價鉻塗層的出現

- 流程可靠性和一致性問題

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第 5 章 市場區隔(以金額為準的市場規模)

- 依產品類型

- 塗層材料

- 粉末

- 陶瓷

- 金屬

- 聚合物和其他粉末

- 線材/棒材

- 其他塗裝材料(輔助材料)

- 熱噴塗設備

- 熱噴塗系統

- 除塵器

- 噴槍和噴嘴

- 送料裝置

- 備用零件

- 隔音罩

- 其他熱噴塗設備

- 熱噴塗塗層和表面處理

- 燃燒

- 電能

- 塗層材料

- 按最終用戶產業

- 航太

- 工業用燃氣渦輪機

- 車

- 電子產品

- 石油和天然氣

- 醫療設備

- 能源和電力

- 鋼

- 纖維

- 印刷和紙張

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 土耳其

- 俄羅斯

- 北歐的

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 奈及利亞

- 埃及

- 卡達

- 阿拉伯聯合大公國

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Thermal Spray Material Companies

- Aimtek Inc.

- AISher APM LLC

- AMETEK Inc.

- C&M Technologies GmbH

- CASTOLIN EUTECTIC

- CenterLine(Windsor)Limited(Supersonic Spray Technologies Division)

- CRS Holdings LLC

- Fisher Barton

- Global Tungsten & Powders

- HC Starck Inc.

- HAI Inc

- Hoganas AB

- Hunter Chemical LLC

- Kennametal Inc.

- Linde PLC(Praxair ST Technologies Inc.)

- LSN Diffusion Limited

- Metallisation Limited

- Metallizing Equipment Co. Pvt. Ltd

- OC Oerlikon Management AG

- Polymet

- Powder Alloy Corporation

- Saint-Gobain

- Sandvik AB

- Thermion

- Thermal Spray Coatings Companies

- APS Materials Inc.

- Bodycote

- Chromalloy Gas Turbine LLC

- Curtiss-Wright Corporation(FW Gartner)

- Fisher Barton

- FM Industries

- Hannecard Roller Coatings, Inc(ASB Industries Inc.)

- Lincotek Trento SpA

- Linde PLC(Praxair ST Technologies Inc.)

- OC Oerlikon Management AG

- Thermion

- TOCALO Co. Ltd

- Thermal Spray Equipment Companies

- Air Products and Chemicals Inc.

- Arzell Inc.

- ASB Industries Inc.(Hannecard Roller Coatings Inc.)

- Bay State Surface Technologies Inc.(Aimtek Inc.)

- Camfil Air Pollution Control(APC)

- CASTOLIN EUTECTIC

- Centerline(Windsor)Ltd(SUPERSONIC SPRAY TECHNOLOGIES)

- Donaldson Company Inc.

- Flame Spray Technologies BV

- GTV Verschleibschutz GmbH

- HAI Inc.

- Imperial Systems Inc.

- Kennametal Inc.

- Lincotek Equipment SpA

- Linde PLC(Praxair ST Technologies Inc.)

- Metallisation Limited

- Metallizing Equipment Co. Pvt. Ltd

- OC Oerlikon Management AG

- Plasma Powders

- Powder Feed Dynamics Inc.

- Progressive Surface

- Saint-Gobain

- Thermion

- Thermal Spray Material Companies

第7章 市場機會與未來趨勢

- 熱噴塗技術(冷噴塗製程)的進展

- 熱噴塗材料的回收利用

- 石油和天然氣產業的需求不斷成長

The Thermal Spray Market size is estimated at USD 13.03 billion in 2025, and is expected to reach USD 15.85 billion by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The thermal spray market was negatively affected by the COVID-19 pandemic. Initially, there was a slowdown in manufacturing activities due to lockdowns and supply chain disruptions, leading to a temporary decrease in demand for thermal spray coatings. However, as industries adopted new norms and increased their emphasis on hygiene and protection, there was a growing demand for thermal spray coatings in industries such as healthcare, automotive, and aerospace.

Key Highlights

- The increasing popularity of thermal spray ceramic coatings due to their usage in medical devices, the rising use of thermal spray coatings in the aerospace industry, and the replacement of hard chrome coatings are some factors driving the demand for the thermal spray market.

- However, issues regarding process reliability and consistency and the emergence of hard trivalent chrome coatings in recent years are likely to hinder the market's growth.

- The increasing demand for thermal spray from the oil and gas industry, recycling of thermal spray processing materials, and advancements in spraying technology (cold spray process) are expected to provide lucrative growth opportunities for the market in the coming years.

- Asia-Pacific is expected to dominate the thermal spray market over the forecast period.

Thermal Spray Market Trends

The Aerospace Industry is Expected to Dominate the Market

- Aerospace components are often exposed to harsh environments, including high temperatures, corrosive chemicals, and extreme weather conditions. Thermal spray coatings provide an effective barrier against corrosion, extending the lifespan of critical components such as turbine blades, engine parts, and airframes.

- Thermal spray coatings offer lightweight solutions for aerospace components, contributing to fuel efficiency and overall aircraft performance. Coatings with tailored properties can replace heavier materials while maintaining structural integrity.

- The aerospace industry is undergoing rapid technological advancements and innovation, creating upswings for aircraft manufacturing. According to the Boeing Commercial Outlook 2023-2042, with a resurgence in international traffic and domestic air travel back to pre-pandemic levels, the company has projected global demand for 48,575 new commercial jets by 2042.

- According to the International Air Travel Association, domestic commercial aircraft passenger traffic increased by 9.2% over the pre-pandemic timeline in August 2023. Increased air traffic may raise the demand for commercial aircraft and propel the demand for adhesives during the forecast period.

- Airbus, a major aircraft manufacturer worldwide, delivered 735 commercial aircraft in 2023, an increase of 11% compared to the previous year.

- The factors mentioned above are expected to boost the demand for thermal spray in the aerospace industry during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is experiencing rapid industrialization, particularly in countries like China, India, Japan, and South Korea. The region's booming manufacturing sector, including the automotive, aerospace, electronics, and energy industries, is driving significant demand for thermal spray coatings to enhance component performance and durability.

- Governments in Asia-Pacific are investing heavily in infrastructure projects, including transportation, energy, and construction. Thermal spray coatings protect critical infrastructure components from corrosion, wear, and erosion, thereby extending their lifespan and reducing maintenance costs.

- China is one of the world's biggest aircraft manufacturers and a market for domestic air passengers, as stated by the Chinese Civil Aviation Administration. In addition, with more than 200 small aircraft component manufacturers, there has been rapid growth in the parts and assembly industry.

- China is the largest electronics manufacturing base in the world. Electronic products such as smartphones, televisions, cables, mobile computers, gaming systems, and other consumer electronic equipment are being produced in China on an active basis. According to the CEIC, in December 2023, the export value of Chinese electronics products was USD 21.63 billion.

- In 2023, South Korea received a total of USD 18.8 billion in investments from abroad, marking a 3.4% increase from the previous year. Specifically, the electronics industry saw the largest share of this investment, with USD 3 billion allocated, standing out as the top sub-industry.

- China is one of the largest producers of steel globally. According to official figures, the nation's primary steel production reached 952.14 million tons during the initial 11 months of 2023, marking a 1.5% increase compared to the same period in the previous year.

- The automotive industry in India plays a crucial role in technological advancements and macroeconomic expansion. According to the Society of Indian Automobile Manufacturers (SIAM), the number of vehicles sold from April 2023 to March 2024 reached 23,853,463, marking an increase of 12.5% from the 21,204,846 units sold in the same timeframe during FY 2023.

- Due to the above-mentioned factors, the region is projected to dominate the market during the forecast period.

Thermal Spray Industry Overview

The thermal spray market is fragmented in nature. The major players (not in any particular order) include OC Oerlikon Management AG, Linde PLC (Praxair ST Technologies Inc.), Chromalloy Gas Turbine LLC, Bodycote, and Kennametal Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage of Thermal Spray Coatings in Medical Devices

- 4.1.2 Rising Popularity of Thermal Spray Ceramic Coatings

- 4.1.3 Replacement of Hard Chrome Coating

- 4.1.4 Rising Use of Thermal Spray Coatings in the Aerospace Industry

- 4.2 Restraints

- 4.2.1 Emergence of Hard Trivalent Chrome Coatings

- 4.2.2 Issues Regarding Process Reliability and Consistency

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Coatings Materials

- 5.1.1.1 Powders

- 5.1.1.1.1 Ceramics

- 5.1.1.1.2 Metal

- 5.1.1.1.3 Polymers and Other Powders

- 5.1.1.2 Wires/Rods

- 5.1.1.3 Other Coating Materials (Auxiliary Material)

- 5.1.2 Thermal Spray Equipment

- 5.1.2.1 Thermal Spray Coating System

- 5.1.2.2 Dust Collection Equipment

- 5.1.2.3 Spray Gun and Nozzle

- 5.1.2.4 Feeder Equipment

- 5.1.2.5 Spare Parts

- 5.1.2.6 Noise-reducing Enclosures

- 5.1.2.7 Other Thermal Spray Equipment

- 5.1.1 Coatings Materials

- 5.2 Thermal Spray Coatings and Finishes

- 5.2.1 Combustion

- 5.2.2 Electric Energy

- 5.3 End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Industrial Gas Turbines

- 5.3.3 Automotive

- 5.3.4 Electronics

- 5.3.5 Oil and Gas

- 5.3.6 Medical Devices

- 5.3.7 Energy and Power

- 5.3.8 Steel Making

- 5.3.9 Textile

- 5.3.10 Printing and Paper

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Turkey

- 5.4.3.7 Russia

- 5.4.3.8 NORDIC

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Nigeria

- 5.4.5.4 Egypt

- 5.4.5.5 Qatar

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Thermal Spray Material Companies

- 6.4.1.1 Aimtek Inc.

- 6.4.1.2 AISher APM LLC

- 6.4.1.3 AMETEK Inc.

- 6.4.1.4 C&M Technologies GmbH

- 6.4.1.5 CASTOLIN EUTECTIC

- 6.4.1.6 CenterLine (Windsor) Limited (Supersonic Spray Technologies Division)

- 6.4.1.7 CRS Holdings LLC

- 6.4.1.8 Fisher Barton

- 6.4.1.9 Global Tungsten & Powders

- 6.4.1.10 H.C. Starck Inc.

- 6.4.1.11 HAI Inc

- 6.4.1.12 Hoganas AB

- 6.4.1.13 Hunter Chemical LLC

- 6.4.1.14 Kennametal Inc.

- 6.4.1.15 Linde PLC (Praxair ST Technologies Inc.)

- 6.4.1.16 LSN Diffusion Limited

- 6.4.1.17 Metallisation Limited

- 6.4.1.18 Metallizing Equipment Co. Pvt. Ltd

- 6.4.1.19 OC Oerlikon Management AG

- 6.4.1.20 Polymet

- 6.4.1.21 Powder Alloy Corporation

- 6.4.1.22 Saint-Gobain

- 6.4.1.23 Sandvik AB

- 6.4.1.24 Thermion

- 6.4.2 Thermal Spray Coatings Companies

- 6.4.2.1 APS Materials Inc.

- 6.4.2.2 Bodycote

- 6.4.2.3 Chromalloy Gas Turbine LLC

- 6.4.2.4 Curtiss-Wright Corporation (FW Gartner)

- 6.4.2.5 Fisher Barton

- 6.4.2.6 FM Industries

- 6.4.2.7 Hannecard Roller Coatings, Inc (ASB Industries Inc.)

- 6.4.2.8 Lincotek Trento SpA

- 6.4.2.9 Linde PLC (Praxair ST Technologies Inc.)

- 6.4.2.10 OC Oerlikon Management AG

- 6.4.2.11 Thermion

- 6.4.2.12 TOCALO Co. Ltd

- 6.4.3 Thermal Spray Equipment Companies

- 6.4.3.1 Air Products and Chemicals Inc.

- 6.4.3.2 Arzell Inc.

- 6.4.3.3 ASB Industries Inc. (Hannecard Roller Coatings Inc.)

- 6.4.3.4 Bay State Surface Technologies Inc. (Aimtek Inc.)

- 6.4.3.5 Camfil Air Pollution Control (APC)

- 6.4.3.6 CASTOLIN EUTECTIC

- 6.4.3.7 Centerline (Windsor) Ltd (SUPERSONIC SPRAY TECHNOLOGIES)

- 6.4.3.8 Donaldson Company Inc.

- 6.4.3.9 Flame Spray Technologies BV

- 6.4.3.10 GTV Verschleibschutz GmbH

- 6.4.3.11 HAI Inc.

- 6.4.3.12 Imperial Systems Inc.

- 6.4.3.13 Kennametal Inc.

- 6.4.3.14 Lincotek Equipment SpA

- 6.4.3.15 Linde PLC (Praxair ST Technologies Inc.)

- 6.4.3.16 Metallisation Limited

- 6.4.3.17 Metallizing Equipment Co. Pvt. Ltd

- 6.4.3.18 OC Oerlikon Management AG

- 6.4.3.19 Plasma Powders

- 6.4.3.20 Powder Feed Dynamics Inc.

- 6.4.3.21 Progressive Surface

- 6.4.3.22 Saint-Gobain

- 6.4.3.23 Thermion

- 6.4.1 Thermal Spray Material Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Spraying Technology (Cold Spray Process)

- 7.2 Recycling of Thermal Spray Processing Materials

- 7.3 Increasing Demand From The Oil and Gas Industry

熱噴塗設備市場(依製程、最終用途產業、應用、材料與設備類型分類)-2025-2032年全球預測

熱噴塗設備市場(依製程、最終用途產業、應用、材料與設備類型分類)-2025-2032年全球預測 全球熱噴塗材料市場

全球熱噴塗材料市場 熱噴塗設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

熱噴塗設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 熱噴塗市場規模、佔有率和成長分析(按材料、技術、應用和地區)- 產業預測 2025-2032熱噴塗材料:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

熱噴塗市場規模、佔有率和成長分析(按材料、技術、應用和地區)- 產業預測 2025-2032熱噴塗材料:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 全球熱噴塗材料市場(2024-2028)

全球熱噴塗材料市場(2024-2028) 2024 - 2032 年熱噴塗服務市場機會、成長動力、產業趨勢分析與預測熱噴塗設備市場機會、成長動力、產業趨勢分析與預測 2024 - 2032

2024 - 2032 年熱噴塗服務市場機會、成長動力、產業趨勢分析與預測熱噴塗設備市場機會、成長動力、產業趨勢分析與預測 2024 - 2032