|

市場調查報告書

商品編碼

1636470

歐洲電動車電池製造:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Europe Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

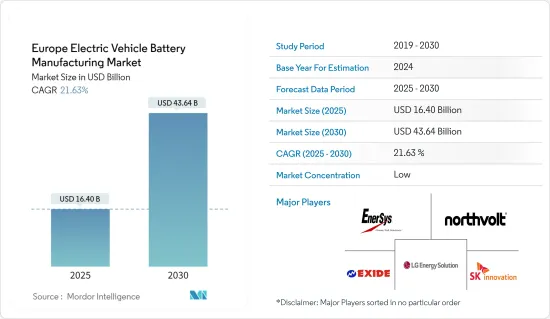

歐洲電動車電池製造市場規模預計到2025年為164億美元,預計2030年將達到436.4億美元,預測期內(2025-2030年)複合年成長率為21.63%。

主要亮點

- 從中期來看,電池產能投資的增加以及電池原料成本的下降預計將在預測期內提振電動車電池製造的需求。

- 相反,原料蘊藏量的缺乏給電動車電池製造市場的成長帶來了重大挑戰。

- 然而,電動車雄心勃勃的長期目標,例如提高產能、技術進步和降低成本,可能在不久的將來為電動車電池製造市場創造重大機會。

- 在電動車普及率激增的推動下,德國處於歐洲電動汽車電池製造成長的前沿。該國強大的技術基礎設施和有利的政府政策進一步推動了這一成長。

歐洲電動車電池製造市場趨勢

鋰離子電池類型主導市場

- 鋰離子 (Li-ion) 電池徹底改變了電動車 (EV) 市場,並刺激了電池製造的創新。鋰離子電池的關鍵特性,如高能量密度、長循環壽命和快速充電,使其成為當今電動車的選擇。

- 此外,鋰離子二次電池具有優異的容量重量比,這使得它們優於其他技術。儘管鋰離子二次電池往往比其他技術更昂貴,但市場主要企業正在增加研發投資、增加產量、加劇競爭並壓低價格。

- 儘管電動車電池組和電池能源儲存系統(BESS)的平均價格有所上漲,但在 2023 年大幅下降至 139 美元/kWh(下降 13%)。據預測,這種下降趨勢預計將持續下去,到2025年將達到113美元/千瓦時,並在2030年降至80美元/千瓦時。

- 此外,世界各國政府正在實施政策和獎勵,以促進電動車(EV)的採用並鼓勵鋰離子電池製造的成長。為了因應快速成長的鋰離子電池需求,世界各國政府不僅進行大量投資,也積極推動鋰離子二次電池的生產。

- 例如,2023年11月,英國政府宣布投資5,000萬英鎊(6,300萬美元),建立以鋰離子電池為重點的強大電池供應鏈。該舉措符合英國雄心勃勃的電動車生產目標。該電池策略將持續到 2030 年,承諾為零排放汽車、電池及其供應鏈提供量身定做的支持,包括新資本和研發資金。這些措施旨在提高英國的電池產量,並推動未來對鋰離子電池的需求。

- 此外,鋰離子電池需求的激增促使了被稱為「超級工廠」的大型生產設施的出現。這些設施旨在批量生產電池,確保我們滿足電動車 (EV) 不斷成長的需求。由於預計電動車電池的需求很快就會激增,該地區的領先公司正在推出多個計劃來提高鋰離子電池產能。

- 例如,2024年5月,法國Blue Solutions宣布計畫投資約20億歐元(21.7億美元)在法國東部興建一座超級工廠。該工廠旨在生產用於電動車的新型固態電池,快速充電時間為 20 分鐘,預計將於 2030 年開始生產。這些努力將在未來幾年擴大國內電池產量。

- 因此,這些努力將在預測期內提高鋰離子電池的產量並顯著擴大電動車電池的產能。

德國正在經歷顯著的成長

- 德國憑藉其強大的汽車工業、先進的製造能力和對永續性的堅定承諾,處於電動車 (EV) 革命的前沿。隨著電動車需求的飆升,德國正在大力投資加強電動車電池製造。

- 中國不僅在向清潔能源邁進,而且還專注於向電動車的轉型,這已成為許多公司的優先事項。德國電動車銷量正在經歷令人印象深刻的成長。國際能源總署(IEA)報告稱,2023年德國電動車銷量將達到70萬輛,與2022年的數字相當,但比2019年高出5.5倍。憑藉這一勢頭以及最近歐洲政府舉措的支持,電動車銷量預計將增加,對電動車電池生產的需求也將增加。

- 作為歐洲電池聯盟的主要企業,德國正在主導努力在歐洲建立具有競爭力和永續的電池製造生態系統。該聯盟旨在減少對非歐洲電池供應商的依賴並促進歐盟內部的創新。同時,德國政府宣布對研究、基礎設施和獎勵進行大量投資,以加速電動車的普及。

- 值得注意的是,2024 年 1 月,瑞典著名鋰離子電池製造商 Norstvolt 獲得了歐盟的核准,並獲得了德國高達 9.02 億歐元(9.8643 億美元)的國家支持。該投資將在德國海德建造電動和混合動力汽車電池生產設施,符合德國和歐盟的淨零排放目標。此類舉措預計將在未來幾年提高德國的電池產量。

- 此外,德國企業和研究機構也致力於開發固態電池,與傳統鋰離子電池相比,固態電池具有更好的能量密度、安全性和壽命。頂級區域公司之間的合作可能會暫時推動電動車電池的需求。

- 例如,2024 年 5 月,由 VARTA主要企業的由 15 家公司和大學研究人員組成的聯盟宣布了創新的鈉離子電池技術。他們的目標是為電動車和其他應用生產高性能、經濟高效且環保的電池。該聯盟的目標是在 2027 年中期完成計劃的最後階段。這些突破預計將在預測期內增加對先進電動車電池的需求,從而促進該地區的電池製造。

- 鑑於這些發展,顯然這些措施不僅會增強電動車的需求,還會顯著增加未來幾年對電動車電池製造的需求。

歐洲電動車電池製造業概況

歐洲電動車電池製造市場已減少一半。主要企業(排名不分先後)包括 EnerSys、SK Innovation、Northvolt AB、Exide Industries Ltd 和 LG Energy Solution。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規政策

- 市場動態

- 促進因素

- 投資增加電池產能

- 電池原物料成本下降

- 抑制因素

- 原料蘊藏量不足

- 促進因素

- 供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品/服務的威脅

- 競爭公司之間的敵對關係

- 投資分析

第5章市場區隔

- 透過電池

- 鋰離子

- 鉛酸電池

- 鎳氫電池

- 其他

- 依電池形狀分類

- 方形

- 袋型

- 圓柱形

- 搭車

- 客車

- 商用車

- 其他

- 透過促銷

- 電池電動車

- 油電混合車

- 插電式混合動力電動車

- 按地區

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 北歐的

- 俄羅斯

- 土耳其

- 其他歐洲國家

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- BYD Co. Ltd

- SK Innovation

- Northvolt AB

- EnerSys

- Energizer Holdings Inc.

- LG Chem Ltd

- Italvolt

- Envision AESC

- Saft Groupe SA

- Samsung SDI

- Exide Industries Ltd

- 其他知名企業名單

- 市場排名分析

第7章 市場機會及未來趨勢

- 電動車的長期目標

簡介目錄

Product Code: 50003737

The Europe Electric Vehicle Battery Manufacturing Market size is estimated at USD 16.40 billion in 2025, and is expected to reach USD 43.64 billion by 2030, at a CAGR of 21.63% during the forecast period (2025-2030).

Key Highlights

- In the medium term, increased investments in battery production capacity, coupled with a decline in the costs of battery raw materials, are poised to boost the demand for electric vehicle battery manufacturing during the forecast period.

- Conversely, a shortage of raw material reserves poses a significant challenge to the growth of the electric vehicle battery manufacturing market.

- However, ambitious long-term targets for electric vehicles-such as scaling up production capacity, advancing technology, and cutting costs-are set to unlock substantial opportunities for the electric vehicle battery manufacturing market in the near future.

- Germany is at the forefront of electric vehicle battery manufacturing growth in Europe, fueled by a surge in electric vehicle adoption. The nation's robust technological infrastructure, combined with favorable government policies, further accelerates this growth.

Europe Electric Vehicle Battery Manufacturing Market Trends

Lithium-Ion Battery Type Dominate the Market

- Lithium-ion (Li-ion) batteries have revolutionized the electric vehicle (EV) market, driving innovations in battery production. Their key attributes-high energy density, long cycle life, and swift charging-make them the preferred choice for today's EVs.

- Moreover, lithium-ion rechargeable batteries surpass other technologies due to their excellent capacity-to-weight ratio. Although they tend to be more expensive than alternatives, major players in the market are boosting R&D investments and ramping up production, heightening competition, and pushing prices down.

- Despite rising average battery pack prices for EVs and battery energy storage systems (BESS), 2023 witnessed a significant dip, with prices falling to USD 139/kWh-a 13% reduction. Projections suggest this downward trajectory will persist, with prices anticipated to reach USD 113/kWh by 2025 and further decline to USD 80/kWh by 2030, driven by relentless technological and manufacturing progress.

- Furthermore, governments worldwide are implementing policies and incentives to promote electric vehicle (EV) adoption and stimulate lithium-ion battery manufacturing growth. In response to the soaring demand for lithium-ion batteries, governments are not only committing significant investments but are also actively promoting the production of these rechargeable batteries.

- For example, in November 2023, the United Kingdom government announced a GBP 50 million (USD 63 million) investment to establish a robust battery supply chain, emphasizing lithium-ion batteries. This initiative aligns with the UK's ambitious EV production targets. The Battery Strategy, extending to 2030, promises tailored support for zero-emission vehicles, batteries, and their supply chains, including new capital and R&D funding. Such initiatives are poised to boost battery production in the UK and elevate the demand for lithium-ion batteries in the future.

- Additionally, the surging demand for Li-ion batteries has catalyzed the emergence of large-scale production facilities, dubbed Gigafactories. These facilities are engineered to produce battery cells en masse, ensuring they meet the rising electric vehicle (EV) demand. Major regional players are launching multiple projects to enhance their lithium-ion battery production capabilities, foreseeing a spike in EV battery demand soon.

- For instance, in May 2024, French firm Blue Solutions revealed plans for a gigafactory in eastern France, with an investment of around 2 billion euros (USD 2.17 billion). This facility aims to produce a new solid-state battery for electric vehicles, boasting a rapid 20-minute charging time, with production slated to commence by 2030. Such endeavors are set to amplify battery production in the nation in the ensuing years.

- Consequently, these initiatives are poised to bolster lithium-ion battery production and significantly expand EV battery manufacturing capacity during the forecast period.

Germany to Witness Significant Growth

- Germany is at the forefront of the electric vehicle (EV) revolution, leveraging its strong automotive industry, advanced manufacturing capabilities, and steadfast commitment to sustainability. As the demand for EVs surges, Germany is making significant investments to enhance its EV battery manufacturing.

- The country is not only shifting towards clean energy but also emphasizing the transition to electric vehicles, a priority for numerous companies. EV sales in Germany have experienced remarkable growth. In 2023, the International Energy Agency (IEA) reported that Germany sold 0.7 million electric vehicles, matching 2022's numbers but representing a 5.5-fold increase since 2019. With this momentum and support from recent European government initiatives, EV sales are projected to rise, driving an increased demand for EV battery production.

- As a key player in the European Battery Alliance, Germany is leading efforts to establish a competitive and sustainable battery cell manufacturing ecosystem in Europe. This alliance aims to reduce dependence on non-European battery suppliers and foster innovation within the EU. In tandem, the German government has announced substantial investments in research, infrastructure, and incentives to promote EV adoption.

- In a notable move, in January 2024, Northvolt, a prominent Swedish lithium-ion battery manufacturer, received a substantial EUR 902 million (USD 986.43 million) state aid package from Germany, with EU approval. This investment is directed towards building a battery production facility for electric and hybrid vehicles in Heide, Germany, aligning with the net-zero emissions goals of both Germany and the EU. Such endeavors are poised to boost battery production in the nation in the coming years.

- Additionally, German firms and research institutions are at the helm of developing solid-state batteries, which promise better energy density, safety, and longevity compared to traditional lithium-ion batteries. Collaborations among top regional companies are set to drive the demand for EV batteries in the foreseeable future.

- For example, in May 2024, a consortium of 15 companies and university researchers, led by VARTA, introduced innovative sodium-ion battery technology. Their ambition is to produce high-performance, cost-effective, and environmentally friendly batteries for EVs and other applications. The consortium aims to wrap up the project's final phase by mid-2027. Such breakthroughs are anticipated to boost the demand for advanced EV batteries and, consequently, the region's battery manufacturing during the forecast period.

- Given these developments, it's clear that these initiatives will not only bolster EV demand but also significantly heighten the need for EV battery manufacturing in the coming years.

Europe Electric Vehicle Battery Manufacturing Industry Overview

Europe's electric vehicle battery manufacturing market is semi-fragmented. Some of the key players (not in particular order) are EnerSys, SK Innovation, Northvolt AB, Exide Industries Ltd, LG Energy Solution, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Investments to Enhance the battery production capacity

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Lack of Raw Material Reserves

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Nickel Metal Hydride Battery

- 5.1.4 Others

- 5.2 Battery Form

- 5.2.1 Prismatic

- 5.2.2 Pouch

- 5.2.3 Cylindrical

- 5.3 Vehicle

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Others

- 5.4 Propulsion

- 5.4.1 Battery Electric Vehicle

- 5.4.2 Hybrid Electric Vehicle

- 5.4.3 Plug-in Hybrid Electric Vehicle

- 5.5 Geography

- 5.5.1 Germany

- 5.5.2 France

- 5.5.3 United Kingdom

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 NORDIC

- 5.5.7 Russia

- 5.5.8 Turkey

- 5.5.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 SK Innovation

- 6.3.3 Northvolt AB

- 6.3.4 EnerSys

- 6.3.5 Energizer Holdings Inc.

- 6.3.6 LG Chem Ltd

- 6.3.7 Italvolt

- 6.3.8 Envision AESC

- 6.3.9 Saft Groupe SA

- 6.3.10 Samsung SDI

- 6.3.11 Exide Industries Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term ambitious targets for electric vehicles

02-2729-4219

+886-2-2729-4219

中國電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中國電動汽車電池製造:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲電動車電池製造設備:市場佔有率分析、產業趨勢和成長預測(2025-2030)中東和非洲電動車電池製造:市場佔有率分析、產業趨勢和成長預測(2025-2030)亞太地區電動汽車電池製造設備:市場佔有率分析、產業趨勢與成長預測(2025-2030)亞太地區電動汽車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美電動車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)北美電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美洲電動汽車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)南美洲電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)

中國電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中國電動汽車電池製造:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲電動車電池製造設備:市場佔有率分析、產業趨勢和成長預測(2025-2030)中東和非洲電動車電池製造:市場佔有率分析、產業趨勢和成長預測(2025-2030)亞太地區電動汽車電池製造設備:市場佔有率分析、產業趨勢與成長預測(2025-2030)亞太地區電動汽車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美電動車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)北美電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美洲電動汽車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)南美洲電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)

▼