|

市場調查報告書

商品編碼

1636450

美國電動汽車電池製造:市場佔有率分析、行業趨勢和成長預測(2025-2030)United States Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

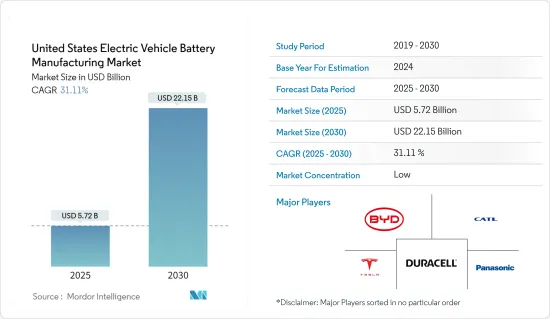

美國電動車電池製造市場規模預計到2025年為57.2億美元,預計2030年將達到221.5億美元,預測期內(2025-2030年)複合年成長率為31.11%。

主要亮點

- 從中期來看,增加電動車電池產能的投資以及電池原料(尤其是鋰離子)成本的下降預計將在預測期內推動市場發展。

- 另一方面,電池原料蘊藏量不足預計將拖累市場未來發展。

- 也就是說,美國電動車的長期雄心壯志預計將在預測期內創造重大機會。

美國電動車電池製造市場趨勢

鋰離子電池預計將佔較大佔有率

- 近年來,美國對電動車的需求迅速成長。這些車輛主要依靠基於電池的能源儲存系統,這對於全電動、插電式混合動力汽車和混合動力汽車至關重要。

- 大多數插電式混合動力汽車和全電動汽車都配備了鋰離子電池。由於鋰離子電池組價格的下降及其更高的能量密度、更長的循環壽命和效率等優點,插電式混合動力汽車對鋰電池材料的需求正在增加。

- 2023年,鋰離子電池組價格將比前一年下降14%,穩定在139美元/kWh。除了這些好處之外,正在進行的研究和開發旨在生產更有效的電動車鋰電池材料。

- 此外,美國政府已優先從國內蘊藏量中提取鋰礦石,以簡化電動車電池的供應鏈。例如,正在計劃從阿肯色州的地下鹽水礦床中提取鋰,並將其在當地轉化為電池材料。

- 2024年6月,埃克森美孚與全球領先的電動車電池開發商SK On簽署了一份不具約束力的合作備忘錄。這將使埃克森美孚能夠從其位於阿肯色州的第一個計劃中採購多達 10 萬噸 Mobil TM 鋰,並有可能簽訂多年承購協議。

- 此外,埃克森美孚計畫在 2030 年利用這種鋰每年生產約 100 萬個電動車電池,從而加強美國電動車供應鏈。鑑於這些雄心勃勃的目標,電動車製造中的鋰產業有望實現顯著成長。

- 因此,由於鋰離子電池價格下降以及美國新鋰礦石的發現,該行業可能會佔據重要的市場佔有率。

政府扶持政策可望帶動市場

- 近年來,由於政府提供稅收優惠、補貼、津貼和貸款等支持性政策,美國電動車 (EV) 電池製造業蓬勃發展。先進技術汽車製造 (ATVM) 融資計劃等聯邦舉措正在資助尖端電池技術和製造設施的開發。

- 此外,政府不僅投資研發以提高電池技術,還透過優惠的貿易政策支持國內生產。這些努力有望擴大對電動車電池製造的需求。

- 例如,2024年1月,美國能源局累計1.31億美元用於推進電動車電池和充電系統研發的計劃。這筆資金將強化電動車生態系統,有助於降低技術成本,擴大電池車的續航里程,並創造安全、永續的國內電池供應鏈。

- 隨著電動車銷量的上升,政府可能會推出進一步政策以進一步加強電池製造。國際能源總署的報告顯示,2023年美國電動車銷量將達139萬輛,較2022年的99萬輛大幅成長。

- 為此,政府正在製定新的立法,擴大國內電池製造和加工,旨在加強電動車電池的關鍵供應鏈,促進向清潔能源的過渡。

- 例如,2023年11月,《兩黨基礎設施法案》簽署成為法律後,美國能源局宣布計劃從該法案中向全國撥款高達35億美元,以促進先進電池和材料的國內生產。

- 有了這些獎勵和政府支持政策,市場可望強勁成長。

美國電動車電池製造業概況

美國電動車電池製造市場已減少一半。市場主要企業(排名不分先後)包括比亞迪有限公司、特斯拉公司、當代新能源科技有限公司、金霸王公司和松下控股公司。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規政策

- 市場動態

- 促進因素

- 投資增加電池產能

- 電池原物料成本下降

- 抑制因素

- 原料蘊藏量不足

- 促進因素

- 供應鏈分析

- PESTLE分析

- 投資分析

第5章市場區隔

- 透過電池

- 鋰離子

- 鉛酸電池

- 鎳氫電池

- 其他

- 依電池形狀分類

- 方形

- 袋型

- 圓柱形

- 搭車

- 客車

- 商用車

- 其他

- 透過促銷

- 電池電動車

- 油電混合車

- 插電式混合動力電動車

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- BYD Co. Ltd

- Contemporary Amperex Technology Co. Limited

- Duracell Inc

- EnerSys

- GS Yuasa Corporation

- SK On Co, Ltd

- Hyundai Motor Group

- LG Chem Ltd

- Tesla, Inc

- Panasonic Corporation

- List of Other Prominent Companies

- 市場排名分析

第7章 市場機會及未來趨勢

- 電動車的長期目標

簡介目錄

Product Code: 50003717

The United States Electric Vehicle Battery Manufacturing Market size is estimated at USD 5.72 billion in 2025, and is expected to reach USD 22.15 billion by 2030, at a CAGR of 31.11% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, investments to enhance electric vehicle battery production capacity, and a decline in the cost of battery raw material, especially lithium-ion, are expected to drive the market in the forecast period.

- On the other hand, the lack of battery raw materials reserves is expected to hamper the market in the future.

- Nevertheless, long-term ambitious targets for electric vehicles in the United States are expected to create a significant opportunity in the forecast period.

United States Electric Vehicle Battery Manufacturing Market Trends

Lithium-ion Battery is Expected to Have a Major Share

- In recent years, the demand for electric vehicles has surged in the United States. These vehicles rely on energy storage systems, primarily batteries, which are crucial for all-electric, plug-in hybrid, and hybrid vehicles.

- Most plug-in hybrids and all-electric vehicles are powered by lithium-ion batteries. The demand for lithium battery materials in plug-in hybrids is rising, driven by the declining prices of lithium-ion battery packs and their advantages, including high energy density, extended cycle life, and efficiency.

- In 2023, lithium-ion battery pack prices dropped by 14% from the previous year, settling at USD139/kWh. Beyond these benefits, ongoing research and development aim to produce even more effective lithium battery materials for electric vehicles.

- Moreover, the United States government is prioritizing the extraction of lithium ores from domestic reserves to streamline the EV battery supply chain. For instance, plans are underway to extract lithium from underground saltwater deposits in Arkansas and convert it into battery-grade material on-site.

- In June 2024, ExxonMobil and SK On, a leading global electric vehicle battery developer, signed a non-binding memorandum of understanding. This sets the stage for a potential multiyear offtake agreement, enabling ExxonMobil to acquire up to 100,000 metric tons of MobilTM Lithium from its first project in Arkansas.

- Additionally, ExxonMobil aims to utilize this lithium to produce approximately 1 million EV batteries each year by 2030, bolstering the U.S. EV supply chain. Given these ambitious targets, the lithium segment in electric vehicle manufacturing is poised for substantial growth.

- Consequently, with declining lithium-ion battery prices and fresh lithium ore discoveries in the United States, the segment is set to command a significant market share.

Supportive Government Policy and Schemes is Expected to Drive the Market

- In recent years, United States electric vehicle (EV) battery manufacturing has surged, due to supportive government policies offering tax incentives, subsidies, grants, and loans. Federal initiatives, such as the Advanced Technology Vehicles Manufacturing (ATVM) loan program, are channeling funds into the development of cutting-edge battery technologies and manufacturing facilities.

- Moreover, the government is not only investing in research and development to enhance battery technology but is also championing domestic production through favorable trade policies. These initiatives are poised to amplify the demand for electric vehicle battery manufacturing.

- For example, in January 2024, the U.S. Department of Energy earmarked USD 131 million for projects aimed at advancing research and development in EV batteries and charging systems. This funding is set to empower the EV ecosystem, helping to reduce technology costs, extend the driving range of battery vehicles, and forge a secure and sustainable domestic battery supply chain.

- With electric vehicle sales on the rise, the government is likely to introduce more policies to further bolster battery manufacturing. The International Energy Agency reported that United States EV car sales reached 1.39 million units in 2023, a notable increase from 0.99 million units in 2022.

- In line with this, the government is pushing for new laws to expand domestic battery manufacturing and processing, aiming to strengthen America's critical supply chains for electric vehicle batteries and facilitate the clean energy transition.

- As a case in point, in November 2023, the U.S. Department of Energy, after the signing of the Bipartisan Infrastructure Law, announced plans to allocate up to USD 3.5 billion from the law to bolster the domestic production of advanced batteries and their materials nationwide.

- Given these incentives and supportive government policies, the market is poised for significant growth.

United States Electric Vehicle Battery Manufacturing Industry Overview

The United States Electric vehicle battery manufacturing market is semi-fragmented. Some of the major players in the market (in no particular order) include BYD Company Ltd, Tesla, Inc., Contemporary Amperex Technology Co. Limited, Duracell Inc., and Panasonic Holdings Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Investments to Enhance the battery production capacity

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Lack of Raw Material Reserves

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Nickel Metal Hydride Battery

- 5.1.4 Others

- 5.2 Battery Form

- 5.2.1 Prismatic

- 5.2.2 Pouch

- 5.2.3 Cylindrical

- 5.3 Vehicle

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Others

- 5.4 Propulsion

- 5.4.1 Battery Electric Vehicle

- 5.4.2 Hybrid Electric Vehicle

- 5.4.3 Plug-in Hybrid Electric Vehicle

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 Duracell Inc

- 6.3.4 EnerSys

- 6.3.5 GS Yuasa Corporation

- 6.3.6 SK On Co, Ltd

- 6.3.7 Hyundai Motor Group

- 6.3.8 LG Chem Ltd

- 6.3.9 Tesla, Inc

- 6.3.10 Panasonic Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term ambitious targets for electric vehicles

02-2729-4219

+886-2-2729-4219

中國電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中國電動汽車電池製造:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲電動車電池製造設備:市場佔有率分析、產業趨勢和成長預測(2025-2030)中東和非洲電動車電池製造:市場佔有率分析、產業趨勢和成長預測(2025-2030)亞太地區電動汽車電池製造設備:市場佔有率分析、產業趨勢與成長預測(2025-2030)亞太地區電動汽車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美電動車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)北美電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美洲電動汽車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)南美洲電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)

中國電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中國電動汽車電池製造:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲電動車電池製造設備:市場佔有率分析、產業趨勢和成長預測(2025-2030)中東和非洲電動車電池製造:市場佔有率分析、產業趨勢和成長預測(2025-2030)亞太地區電動汽車電池製造設備:市場佔有率分析、產業趨勢與成長預測(2025-2030)亞太地區電動汽車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美電動車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)北美電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美洲電動汽車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)南美洲電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)

▼