|

市場調查報告書

商品編碼

1636259

電動汽車電池電解:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

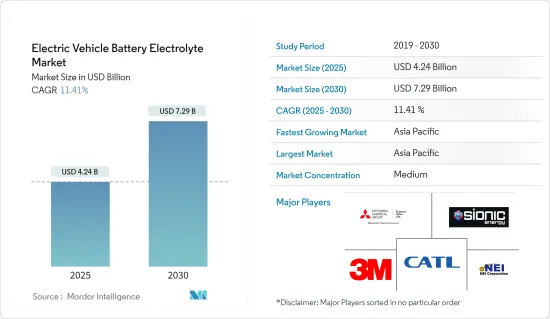

電動車電池電解市場規模預計到2025年為42.4億美元,預計到2030年將達到72.9億美元,預測期內(2025-2030年)複合年成長率為11.41%。

主要亮點

- 從中期來看,電動車需求增加和政府支持措施等因素預計將在預測期內推動市場發展。

- 另一方面,先進電解質的高成本和安全問題預計將阻礙預測期內的市場成長。

- 然而,技術創新和新興電池材料的擴展預計將在未來幾年為市場帶來重大機會。

- 由於電動車在該地區各國的滲透率不斷提高,預計亞太地區將主導市場。

電動汽車電池電解的市場趨勢

鋰離子電池領域佔市場主導地位

- 鋰離子電池傳統上主要用於家用電子電器,例如行動電話和電腦。然而,由於它們對環境的影響較小,它們擴大被重新設計為混合動力汽車和全電動汽車 (EV) 的動力來源。電動車不排放任何溫室氣體,例如二氧化碳或氮氧化物。

- 2023年,電動車(EV)電池需求與前一年同期比較快速成長40%。中國在電池生產方面繼續處於領先地位,尤其是大型電池,約12%的產量用於出口。同時,歐洲正在取得長足進步,彭博新能源財經預測,到 2030 年,歐洲在全球電池產量中的佔有率可能達到 31%。

- 隨著世界各地對電動車的需求不斷增加,有效、可靠的電池電解已變得至關重要,推動了電解配方和技術的重大進步。

- 影響鋰離子電池電解市場的主要趨勢之一是鋰離子電池價格的持續下降。例如,到2023年,鋰離子電池的平均價格將降至每千瓦時(kWh)約139美元,較2013年大幅下降82%以上。據預測,到 2025 年,價格可能會降至 113 美元/千瓦時以下,並在 2030 年達到 80 美元/千瓦時。這些價格下降趨勢使電動車對消費者來說更加實惠,並鼓勵製造商探索新的電解質成分並改進現有電解質成分,以提高電池性能和壽命。

- 新興市場擴大採用電動車也推動了鋰離子電池電解質領域的成長。世界各國政府正在採取措施和獎勵來促進電動車的普及。

- 2023年,美國政府宣布目標是到2030年新車銷量的50%為電動車。白宮也宣布了公共和私人承諾,支持美國在電動車加速挑戰下向電動車歷史性轉型。

- 這將導致電池產量和電解需求激增。隨著各國優先考慮減少溫室氣體排放並轉向清潔能源來源,高效能電池電解在實現這些永續性目標方面的作用變得越來越重要。

- 因此,隨著市場的發展,對永續性和替代技術的關注預計將塑造電池電解液領域未來的全球前景,為更綠色的汽車產業做出貢獻。

亞太地區預計將主導市場

- 亞太電動車(EV)電池電解市場正在經歷顯著成長,這主要得益於中國在電動車生產和銷售方面的主導地位。全球電動車銷量將從2019年的106萬輛激增至2023年的810萬輛,增幅超過650%,而中國對電池電解的強勁需求將對這一擴張發揮關鍵作用。

- 中國企業走在電池技術創新的前沿,不斷提高鋰離子電池的性能和效率。 2024 年 3 月取得了重大突破,研究揭示了一種新的電解質設計,可顯著提高電動車鋰離子電池的充電速度並擴大動作溫度範圍。此創新設計可在室溫下 10 分鐘內完成完整的充電/放電循環,並確保電池在 -70°C 至 60°C 的寬溫度範圍內可逆性。這些進步提高了電動車鋰離子電池的電池效率、安全性和可靠性。

- 鋰離子電池的大規模生產有助於降低製造成本,並使電動車更容易為消費者所接受。人事費用的降低和製造商之間競爭的加劇提高了整體盈利並實現了更廣泛的市場滲透。這些成本效率對於鼓勵更多消費者轉向電動車至關重要,從而推動對電解的需求。

- 除中國外,日本、韓國等亞太國家也在電動車電池電解液市場取得重大進展。日本正專注於開發固體和鈉離子電池,預計它們能夠以更低的成本提供更好的性能,而韓國則在電池生產和創新方面投入了大量資金。

- 例如,2024 年 4 月,日本研究人員發現了一種穩定、高導電性的材料,適合用作固體鋰離子電池的電解質。這種新材料比以前已知的氧化物固體電解質具有更高的離子電導率,並且可以在很寬的溫度範圍內有效運作。

- 由於技術進步、政府的大力支持、成本效率和基礎設施擴張,亞太地區電動汽車電池電解液市場預計將持續成長。隨著這些因素的融合,該地區預計將保持其在電動車電池電解市場的主導地位,並塑造永續交通的未來。

電動汽車電池電解產業概況

電動車電池電解市場正變得半固體。主要參與企業包括(排名不分先後)三菱化學集團、Sionic Energy、3M、寧德時代新能源科技有限公司(CATL)和NEI Corporation。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第2章調查方法

第3章執行摘要

第4章市場概況

- 介紹

- 至2029年市場規模及需求預測(單位:十億美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 電動車需求增加

- 政府支持措施

- 抑制因素

- 先進電解質成本高

- 促進因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 投資分析

第5章市場區隔

- 電池類型

- 鋰離子電池

- 鉛蓄電池

- 其他電池類型

- 電解質類型

- 液體電解質

- 凝膠電解質

- 固體電解質

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 北歐的

- 土耳其

- 俄羅斯

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 印尼

- 越南

- 馬來西亞

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 奈及利亞

- 卡達

- 其他中東/非洲

- 北美洲

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Mitsubishi Chemical Group

- 3M Co.

- Contemporary Amperex Technology Co. Limited(CATL)

- NEI Corporation

- Sionic Energy

- BASF SE

- Solvay SA

- UBE Industries Ltd

- LG Chem Ltd

- Targray Industries Inc.

- 市場排名/佔有率分析

- 其他知名公司名單

第7章 市場機會及未來趨勢

- 新興電池材料的擴展

簡介目錄

Product Code: 50003540

The Electric Vehicle Battery Electrolyte Market size is estimated at USD 4.24 billion in 2025, and is expected to reach USD 7.29 billion by 2030, at a CAGR of 11.41% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing demand for electric vehicles and supportive government initiatives are expected to drive the market during the forecast period.

- On the other hand, high costs of advanced electrolytes and safety concerns are expected to hinder the market growth during the forecast period.

- However, technological innovations and expansion in emerging battery materials are expected to provide significant opportunities for the market in the coming years.

- Asia-Pacific is estimated to dominate the market due to the increasing adoption rate of electric vehicles across the various countries in the region.

Electric Vehicle Battery Electrolyte Market Trends

The Lithium-ion Batteries Segment to Dominate the Market

- Lithium-ion batteries have traditionally been used mainly in consumer electronic devices like mobile phones and personal computers. Still, due to low environmental impact, they are increasingly being redesigned as the power source of choice in hybrid and the complete electric vehicle (EV) range. EVs do not emit any CO2, nitrogen oxides, or other greenhouse gases.

- In 2023, the demand for electric vehicle (EV) batteries surged by 40% compared to the previous year, driven by rising EV sales across all markets, particularly in Europe and the United States. China continues to lead in battery production, especially for heavy-duty batteries, with approximately 12% of its production being exported. Meanwhile, Europe is making significant strides, with forecasts from BloombergNEF suggesting that its share of global battery production could reach 31% by 2030.

- As the demand for electric vehicles escalates worldwide, effective and reliable battery electrolytes have become paramount, fostering significant advancements in electrolyte formulations and technologies.

- One of the primary trends influencing the lithium-ion battery electrolyte market is the continuous decline in the price of lithium-ion batteries. For instance, the average price of lithium-ion batteries fell to around USD 139 per kilowatt-hour (kWh) in 2023, representing a significant decrease of over 82% since 2013. Projections indicate that prices could decline to below USD 113/kWh by 2025 and reach USD 80/kWh by 2030. This downward pricing trend makes electric vehicles more affordable for consumers and encourages manufacturers to explore new electrolyte compositions and improve existing ones, enhancing battery performance and longevity.

- The increasing penetration of electric vehicles in emerging markets is also driving the growth of the lithium-ion battery electrolyte segment. Governments worldwide are implementing policies and incentives to promote electric vehicle adoption.

- In 2023, the US government announced a goal to have 50% of all new vehicle sales electric by 2030. The White House also announced public and private commitments to support America's historic transition to electric vehicles under the EV Acceleration Challenge.

- This leads to a surge in battery production and electrolyte demand. As countries prioritize reducing greenhouse gas emissions and transitioning to cleaner energy sources, the role of efficient battery electrolytes becomes increasingly critical in achieving these sustainability goals.

- Hence, as the market evolves, the focus on sustainability and alternative technologies is expected to shape the future landscape of the battery electrolyte segment globally, contributing to a greener automotive industry.

Asia-Pacific is Expected to Dominate the Market

- The Asia-Pacific electric vehicle (EV) battery electrolyte market is witnessing remarkable growth, primarily driven by China's leading EV production and sales position. With global electric vehicle sales skyrocketing from 1.06 million in 2019 to 8.1 million in 2023, an increase of over 650%, China's robust demand for battery electrolytes plays a pivotal role in this expansion.

- Chinese companies are at the forefront of battery innovation, continually enhancing the performance and efficiency of lithium-ion batteries. A significant breakthrough occurred in March 2024, as researchers unveiled a new electrolyte design that greatly enhances the charging speed and expands the operational temperature range of lithium-ion batteries for electric vehicles. This innovative design allows for full charge and discharge cycles within 10 minutes at room temperature and ensures battery reversibility across a wide temperature span from -70°C to 60°C. Such advancements enhance battery efficiency and improve safety, making lithium-ion batteries more reliable for electric vehicles.

- The large-scale production of lithium-ion batteries has contributed to the decline in manufacturing costs, making electric vehicles more accessible to consumers. Lower labor costs and increased competition among manufacturers have enhanced overall profitability, enabling broader market reach. These cost efficiencies are critical in encouraging more consumers to transition to electric vehicles, thereby driving demand for electrolytes.

- In addition to China, other countries in Asia-Pacific, such as Japan and South Korea, are making significant strides in the electric vehicle battery electrolyte market. Japan's focus on developing solid-state and sodium-ion batteries promises to deliver better performance at lower costs, while South Korea is investing heavily in battery production and innovation.

- For instance, in April 2024, Japanese researchers identified a stable, highly conductive material suitable for use as an electrolyte in solid-state lithium-ion batteries. This new material boasts ionic conductivity surpassing that of any previously known oxide solid electrolytes and operates effectively over a wide temperature range.

- The Asia-Pacific electric vehicle battery electrolyte market is poised for continued growth, fueled by technological advancements, strong government support, cost efficiencies, and an expanding infrastructure. As these factors converge, the region is expected to maintain its dominance in the market for EV battery electrolytes, shaping the future of sustainable transportation.

Electric Vehicle Battery Electrolyte Industry Overview

The electric vehicle battery electrolyte market is semi-consolidated. Some of the major players include (not in particular order) Mitsubishi Chemical Group, Sionic Energy, 3M Co., Contemporary Amperex Technology Co. Limited (CATL), and NEI Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand of Electric Vehicles

- 4.5.1.2 Supportive Government Initiatives

- 4.5.2 Restraints

- 4.5.2.1 High Costs of Advanced Electrolytes

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Batteries

- 5.1.2 Lead-acid Batteries

- 5.1.3 Other Battery Types

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 NORDIC

- 5.3.2.6 Turkey

- 5.3.2.7 Russia

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Thailand

- 5.3.3.6 Indonesia

- 5.3.3.7 Vietnam

- 5.3.3.8 Malaysia

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 Qatar

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Mitsubishi Chemical Group

- 6.3.2 3M Co.

- 6.3.3 Contemporary Amperex Technology Co. Limited (CATL)

- 6.3.4 NEI Corporation

- 6.3.5 Sionic Energy

- 6.3.6 BASF SE

- 6.3.7 Solvay SA

- 6.3.8 UBE Industries Ltd

- 6.3.9 LG Chem Ltd

- 6.3.10 Targray Industries Inc.

- 6.4 Market Ranking/Share Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion in Emerging Battery Materials

02-2729-4219

+886-2-2729-4219

電動車電池電解質市場-全球產業規模、佔有率、趨勢、機會和預測,按電池類型、電解質類型、應用、地區和競爭情況細分,2020-2030 年

電動車電池電解質市場-全球產業規模、佔有率、趨勢、機會和預測,按電池類型、電解質類型、應用、地區和競爭情況細分,2020-2030 年 中國電動汽車電池電解:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲電動汽車電池電解市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030)亞太地區電動汽車電池電解:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)北美電動車電池電解:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美洲電動車電池電解:市場佔有率分析、產業趨勢、成長預測(2025-2030)印度電動車電池電解:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)德國電動車電池電解:市場佔有率分析、產業趨勢、成長預測(2025-2030)東協國家電動車電池電解:市場佔有率分析、產業趨勢、成長預測(2025-2030)歐洲電動車電池電解:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國電動汽車電池電解:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲電動汽車電池電解市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030)亞太地區電動汽車電池電解:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)北美電動車電池電解:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美洲電動車電池電解:市場佔有率分析、產業趨勢、成長預測(2025-2030)印度電動車電池電解:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)德國電動車電池電解:市場佔有率分析、產業趨勢、成長預測(2025-2030)東協國家電動車電池電解:市場佔有率分析、產業趨勢、成長預測(2025-2030)歐洲電動車電池電解:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

▼