|

市場調查報告書

商品編碼

1755190

固態電解質市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Solid-State Electrolytes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

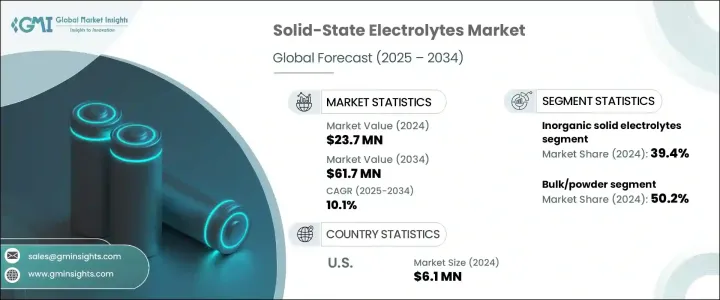

2024年,全球固態電解質市場規模達2,370萬美元,預計2034年將以10.1%的複合年成長率成長,達到6,170萬美元。這得益於對更高能量密度、更高安全性和更高性能的先進電池解決方案日益成長的需求。固態電解質取代了鋰離子電池中使用的傳統液體或凝膠電解質,提供了更安全、更有效率的替代方案。這些材料解決了諸如易燃性和洩漏等主要問題,降低了熱失控和火災事故的風險。它們能夠支援更快的充電速度並延長電池壽命,使其成為電動車、消費性電子產品和下一代儲能系統的關鍵創新。

材料的持續創新——尤其是陶瓷和聚合物複合硫化物離子導體——推動了市場的發展,並提高了離子電導率和材料相容性。隨著對更安全、高容量電池的需求不斷成長,尤其是電動車的普及以及政策對清潔能源技術的支持,固態電池正從概念走向商業化。相關法規的支持性加上技術進步,為市場擴張奠定了堅實的基礎。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2370萬美元 |

| 預測值 | 6170萬美元 |

| 複合年成長率 | 10.1% |

2024年,無機固體電解質市場佔比39.4%。這些材料因其優異的離子電導率、熱彈性和結構完整性而備受青睞,這在電動車電池和電網規模儲能系統等高應力環境中至關重要。它們的穩定性以及與鋰金屬陽極的兼容性可提高能量密度並延長電池壽命。無機電解質(尤其是硫化物和氧化物基變體)也不易燃,從而消除了傳統液體系統存在的火災風險。將它們整合到當前的生產流程中,有助於簡化製造流程並加速儲能應用的部署。

2024年,固態電解質市場中塊狀或粉狀電解質的佔有率為50.2%。粉末狀電解質的廣泛應用源自於其多功能性以及易於與各種電極材料整合的特性。這種形態有利於提高結構緻密性和活性物質的整合性,從而支持汽車和固定式應用的高效量產。硫代磷酸鋰和石榴石基材料等粉末狀化合物憑藉其出色的離子電導率和機械強度,擴大應用於下一代電池系統的試點項目,使其成為商業化規模化應用的最佳選擇。

2024年,美國固態電解質市場產值達610萬美元。旨在促進國內電池創新的聯邦資金和政策措施對美國保持市場領先地位發揮關鍵作用。主要政府項目正在透過撥款、稅收抵免以及《通膨削減法案》和《電池製造和回收補助計劃》等立法下的研究支持來加速固態電解質市場的發展。這些措施促進了固態電池領域的創新,並鼓勵美國企業擴大營運規模,減少對進口的依賴,並建立強大的本地供應鏈。

固態電解質市場的知名企業包括三星SDI、豐田汽車公司、LG化學、QuantumScape和輝能科技。為了擴大市場佔有率,這些公司投入研發資金,以推進固態電解質化學技術並提升電池性能。與汽車原始設備製造商和儲能公司的合作有助於確保長期合約和早期應用機會。與研究機構和政府機構建立策略夥伴關係,加速了原型開發和規模化進程。各公司專注於精簡製造能力並部署試點生產線,以確保在商用固態電池部署中佔據先發優勢。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 貿易統計資料(HS 編碼) 註:以上貿易統計僅提供主要國家。

- 主要出口國

- 主要進口國

- 衝擊力

- 市場促進因素

- 高能量密度電池的需求不斷成長

- 越來越關注電池安全

- 電動車普及率不斷上升

- 固態電解質材料的進展

- 市場限制

- 製造成本高

- 擴大生產面臨的技術挑戰

- 介面穩定性問題

- 來自先進液體電解質的競爭

- 市場機會

- 新型固體電解質材料的開發

- 穿戴式裝置中的新興應用

- 與再生能源儲存的整合

- 政府措施和資金

- 市場挑戰

- 在室溫下實現高離子電導率

- 解決電極-電解質界面問題

- 鋰枝晶的形成與生長

- 量產與降低成本

- 市場促進因素

- 監管框架和政府舉措

- 電池材料安全法規

- 環境法規

- 政府資助和研究計劃

- 區域監管差異

- 未來監理展望

- 成長潛力分析

- 2021-2034年價格分析(美元/噸)

- 製造和生產流程

- 固相合成

- 溶膠-凝膠工藝

- 機械化學合成

- 薄膜沉積技術

- 聚合物加工方法

- 可擴展的製造方法

- 材料表徵技術

- X光繞射分析

- 阻抗光譜

- 掃描式電子顯微鏡

- 核磁共振

- 熱分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 市佔率分析

- 戰略框架

- 併購

- 合資與合作

- 新產品開發

- 擴張策略

- 競爭基準測試

- 供應商格局

- 競爭定位矩陣

- 戰略儀表板

- 專利分析與創新評估

- 新參與者的市場進入策略

- 配電網路分析

第5章:市場估計與預測:按材料,2021-2034 年

- 主要趨勢

- 無機固體電解質

- 氧化物基電解質

- LISICON型

- NASICON型

- 鈣鈦礦型

- 石榴石型(LLZO)

- 其他

- 硫化物基電解質

- 硫代-LISICON

- 銀銻礦型

- Li2S-P2S5微晶玻璃

- 其他

- 鹵化物基電解質

- 其他

- 氧化物基電解質

- 聚合物基固態電解質

- 聚環氧乙烷(PEO)基

- 聚偏氟乙烯 (PVDF) 基

- 聚碳酸酯基

- 其他

- 複合固態電解質

- 聚合物陶瓷複合材料

- 聚合物-無機鹽複合材料

- 陶瓷-陶瓷複合材料

- 其他

- 混合固體電解質

第6章:市場估計與預測:依形式,2021-2034 年

- 主要趨勢

- 散裝/粉末

- 薄膜

- 片材/膜

- 其他

第7章:市場估計與預測:按應用,2021-2034 年

- 主要趨勢

- 電動車

- 搭乘用車

- 商用車

- 二輪車

- 消費性電子產品

- 智慧型手機和平板電腦

- 筆記型電腦和桌上型電腦

- 穿戴式裝置

- 其他

- 儲能系統

- 住宅

- 商業的

- 公用事業規模

- 醫療器材

- 植入式裝置

- 攜帶式醫療設備

- 其他

- 航太和國防

- 其他

第8章:市場估計與預測:按地區,2021-2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Ampcera

- Cymbet Corporation

- Idemitsu Kosan

- Ilika

- ION Storage Systems

- LG Energy

- Murata Manufacturing

- NEI Corporation

- Ohara

- ProLogium Technology

- QuantumScape

- Samsung SDI

- Solid Power

- TDK Corporation

- Toyota Motor Corporation

The Global Solid-State Electrolytes Market was valued at USD 23.7 million in 2024 and is estimated to grow at a CAGR of 10.1% to reach USD 61.7 million by 2034, driven by rising demand for advanced battery solutions that offer higher energy density, enhanced safety, and improved performance. Solid-state electrolytes replace the conventional liquid or gel-based electrolytes used in lithium-ion batteries, providing a safer and more efficient alternative. These materials address major concerns like flammability and leakage, reducing the risks of thermal runaway and fire incidents. Their ability to support faster charging and extend battery lifespan makes them a crucial innovation for electric vehicles, consumer electronics, and next-generation energy storage systems.

Continuous innovation in materials-particularly ceramic and polymer composite sulfide ion conductors-has pushed the market forward, improving ionic conductivity and material compatibility. As demand for safer, high-capacity batteries rises, especially with broader EV adoption and policy support for clean energy technologies, solid-state batteries are moving from concept to commercialization. Supportive regulations, combined with technological advancement, create a strong foundation for market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.7 Million |

| Forecast Value | $61.7 Million |

| CAGR | 10.1% |

The inorganic solid electrolytes segment accounted for a 39.4% share in 2024. These materials are preferred for their excellent ionic conductivity, thermal resilience, and structural integrity, essential in high-stress environments such as electric vehicle batteries and grid-scale energy storage systems. Their stability and compatibility with lithium metal anodes enhance energy density and extend battery life. Inorganic electrolytes-especially sulfide and oxide-based variants-are also non-combustible, eliminating the fire risks associated with traditional liquid systems. Their integration into current production workflows helps streamline manufacturing and accelerates deployment across energy storage applications.

The bulk or powder form segment in the solid-state electrolytes market held a 50.2% share in 2024. The widespread use of powdered electrolytes stems from their versatility and ease of integration with various electrode materials. This form allows for better structural compactness and active material incorporation, supporting efficient mass production for automotive and stationary applications. Powdered compounds such as lithium thiophosphate and garnet-based materials are increasingly used in pilot projects for next-generation battery systems, due to their outstanding ionic conductivity and mechanical strength, making them an optimal choice for commercial scaling.

U.S. Solid-State Electrolytes Market generated USD 6.1 million in 2024. Federal funding and policy initiatives aimed at domestic battery innovation play a key role in the country's market leadership. Major government programs are accelerating development through grants, tax credits, and research support under legislation such as the Inflation Reduction Act and Battery Manufacturing and Recycling Grant Program. These efforts boost innovation in the solid-state battery segment and encourage U.S.-based companies to scale up operations, reduce import dependence, and create robust local supply chains.

Prominent players in the Solid-State Electrolytes Market include Samsung SDI, Toyota Motor Corporation, LG Chem, QuantumScape, and ProLogium Technology. To expand their market presence, these companies invest in R&D to advance solid electrolyte chemistry and enhance battery performance. Collaborations with automotive OEMs and energy storage firms help secure long-term contracts and early adoption opportunities. Strategic partnerships with research institutions and government entities accelerate prototype development and scaling processes. Firms focus on streamlining manufacturing capabilities and deploying pilot production lines to ensure early-mover advantage in commercial solid-state battery deployment.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code) Note: the above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Impact forces

- 3.4.1 Market drivers

- 3.4.1.1 Growing demand for high-energy density batteries

- 3.4.1.2 increasing focus on battery safety

- 3.4.1.3 Rising adoption of electric vehicles

- 3.4.1.4 Advancements in solid-state electrolyte materials

- 3.4.2 Market restraints

- 3.4.2.1 High manufacturing costs

- 3.4.2.2 technical challenges in scaling production

- 3.4.2.3 Interface stability issues

- 3.4.2.4 Competition from advanced liquid electrolytes

- 3.4.3 Market opportunities

- 3.4.3.1 Development of new solid electrolyte materials

- 3.4.3.2 Emerging applications in wearable devices

- 3.4.3.3 Integration with renewable energy storage

- 3.4.3.4 Government initiatives and funding

- 3.4.4 Market challenges

- 3.4.4.1 Achieving high ionic conductivity at room temperature

- 3.4.4.2 Addressing electrode-electrolyte interface issues

- 3.4.4.3 Lithium dendrite formation and growth

- 3.4.4.4 Mass production and cost reduction

- 3.4.1 Market drivers

- 3.5 Regulatory framework and government initiatives

- 3.5.1 Safety regulations for battery materials

- 3.5.2 Environmental regulations

- 3.5.3 Government funding and research initiatives

- 3.5.4 Regional regulatory variations

- 3.5.5 Future regulatory outlook

- 3.6 Growth potential analysis

- 3.7 Pricing analysis (USD/Tons) 2021-2034

- 3.8 Manufacturing and production processes

- 3.8.1 Solid-state synthesis

- 3.8.2 Sol-gel processing

- 3.8.3 Mechanochemical synthesis

- 3.8.4 Thin film deposition techniques

- 3.8.5 Polymer processing methods

- 3.8.6 Scalable manufacturing approaches

- 3.9 Material characterization techniques

- 3.9.1 X-ray diffraction analysis

- 3.9.2 Impedance spectroscopy

- 3.9.3 Scanning electron microscopy

- 3.9.4 Nuclear magnetic resonance

- 3.9.5 Thermal analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis

- 4.2 Strategic framework

- 4.2.1 Mergers & acquisitions

- 4.2.2 Joint ventures & collaborations

- 4.2.3 New product developments

- 4.2.4 Expansion strategies

- 4.3 Competitive benchmarking

- 4.4 Vendor landscape

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

- 4.7 Patent analysis & innovation assessment

- 4.8 Market entry strategies for new players

- 4.9 Distribution network analysis

Chapter 5 Market Estimates and Forecast, By Material, 2021–2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Inorganic solid electrolytes

- 5.2.1 Oxide-based electrolytes

- 5.2.1.1 LISICON-type

- 5.2.1.2 NASICON- type

- 5.2.1.3 Perovskite- type

- 5.2.1.4 Garnet- type (LLZO)

- 5.2.1.5 Others

- 5.2.2 Sulfide- based electrolytes

- 5.2.2.1 Thio-LISICON

- 5.2.2.2 Argyrodite- type

- 5.2.2.3 Li2S-P2S5 glass-ceramics

- 5.2.2.4 Others

- 5.2.3 Halide- based electrolytes

- 5.2.4 Others

- 5.2.1 Oxide-based electrolytes

- 5.3 Polymer-based solid electrolytes

- 5.3.1 Polyethylene oxide (PEO)-based

- 5.3.2 Polyvinylidene fluoride (PVDF)- based

- 5.3.3 Polycarbonate- based

- 5.3.4 Others

- 5.4 Composite solid electrolytes

- 5.4.1 Polymer-ceramic composites

- 5.4.2 Polymer-inorganic salt composites

- 5.4.3 Ceramic-ceramic composites

- 5.4.4 Others

- 5.5 Hybrid solid electrolytes

Chapter 6 Market Estimates and Forecast, By Form, 2021–2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Bulk/powder

- 6.3 Thin films

- 6.4 Sheets/membranes

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021–2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Electric vehicles

- 7.2.1 Passenger vehicles

- 7.2.2 Commercial vehicles

- 7.2.3 Two-wheelers

- 7.3 Consumer electronics

- 7.3.1 Smartphones and tablets

- 7.3.2 Laptops and computers

- 7.3.3 Wearable devices

- 7.3.4 Others

- 7.4 Energy storage systems

- 7.4.1 Residential

- 7.4.2 Commercial

- 7.4.3 Utility-Scale

- 7.5 Medical devices

- 7.5.1 Implantable devices

- 7.5.2 Portable medical equipment

- 7.5.3 Others

- 7.6 Aerospace and defense

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021–2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Ampcera

- 9.2 Cymbet Corporation

- 9.3 Idemitsu Kosan

- 9.4 Ilika

- 9.5 ION Storage Systems

- 9.6 LG Energy

- 9.7 Murata Manufacturing

- 9.8 NEI Corporation

- 9.9 Ohara

- 9.10 ProLogium Technology

- 9.11 QuantumScape

- 9.12 Samsung SDI

- 9.13 Solid Power

- 9.14 TDK Corporation

- 9.15 Toyota Motor Corporation

固體電解質材料市場預測至2034年-按類型、應用和地區分類的全球分析

固體電解質材料市場預測至2034年-按類型、應用和地區分類的全球分析 電池電解市場規模、佔有率、趨勢和預測:按電池類型、電解類型、最終用戶和地區分類,2026-2034年

電池電解市場規模、佔有率、趨勢和預測:按電池類型、電解類型、最終用戶和地區分類,2026-2034年 2026年全球電池電解市場報告

2026年全球電池電解市場報告 鋰離子電池電解市場(依電解形態、鋰鹽、溶劑體系、添加劑和應用分類)-全球預測(2026-2032年)

鋰離子電池電解市場(依電解形態、鋰鹽、溶劑體系、添加劑和應用分類)-全球預測(2026-2032年) 鋅電池電解液市場規模、佔有率及成長分析(按類型、應用和地區分類)-產業預測,2026-2033年

鋅電池電解液市場規模、佔有率及成長分析(按類型、應用和地區分類)-產業預測,2026-2033年 電池電解市場規模、佔有率及成長分析(按電池類型、電解類型、最終用途和地區分類)-2026-2033年產業預測

電池電解市場規模、佔有率及成長分析(按電池類型、電解類型、最終用途和地區分類)-2026-2033年產業預測 固態電池電解液市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)全球固體電解質材料市場:預測(至2032年)-按類型、材料、應用、最終用戶和地區分類的分析

固態電池電解液市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)全球固體電解質材料市場:預測(至2032年)-按類型、材料、應用、最終用戶和地區分類的分析 固體電解質(SSE)-全球市場佔有率和排名、總收入和需求預測(2025-2031年)

固體電解質(SSE)-全球市場佔有率和排名、總收入和需求預測(2025-2031年) 全球電池電解質市場(按電池類型、電解質類型、最終用途、材料和地區分類)- 預測至 2030 年

全球電池電解質市場(按電池類型、電解質類型、最終用途、材料和地區分類)- 預測至 2030 年