|

市場調查報告書

商品編碼

1632099

藥品泡殼包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)Pharmaceutical Blister Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

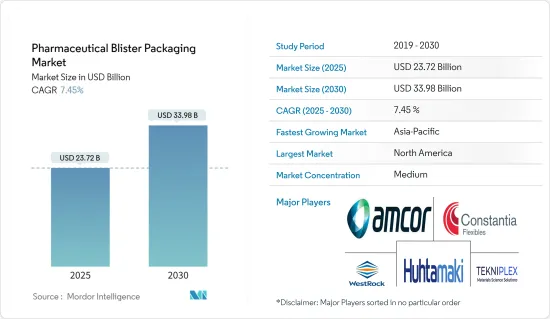

預計2025年藥品泡殼包裝市場規模為237.2億美元,預估至2030年將達339.8億美元,預測期間(2025-2030年)複合年成長率為7.45%。

主要亮點

- 泡殼包裝在製藥業極為重要。這些專門的包裝解決方案可確保藥品到達患者手中時不會被篡改或損壞。泡殼包裝可保護治療藥物免受濕氣和外部污染物的影響。

- 感測器增強型泡殼包裝在監測給藥活動和確保臨床測試的準確性方面發揮關鍵作用。考慮一下 WestRock 的 CerePak泡殼包裝。此泡殼包裝包含微處理器,並以導電墨水印製以記錄每次劑量的日期、時間和位置。這項特徵對於不同劑量的治療方法或安慰劑和活性藥物的組合尤其重要。

- 泡殼包裝通常由熱成型塑膠製成,蓋子由紙、塑膠、鋁箔或其組合製成。僅使用透過冷拔工藝製成的箔也是常見的。也可以選擇不透明的選項來保護光敏藥物免受有害紫外線的影響。

- 泡殼包裝是包裝和運輸醫療必需品的耐用解決方案。保護內容物免受衝擊、潮濕和高溫,延長藥品的保存期限和可運輸性。泡殼包裝的好處在大流行期間變得顯而易見,當時其表面在藥品的國際運輸和儲存中發揮著至關重要的作用。然而,病毒透過這些表面傳播的潛力凸顯了需要改進的領域,特別是在覆材方面。

- 然而,針對塑膠包裝的嚴格法規和措施預計將成為預測期內藥品泡殼包裝領域成長的潛在挑戰。例如,美國(已有 16 個州已通過,預計會有更多州)和歐洲已頒布了遏制塑膠廢棄物的法律。

藥品泡殼包裝市場趨勢

紙泡殼明顯成長的潛力

- 紙泡殼,通常稱為泡殼板,通常用於非處方藥和處方箋藥、維生素和補充劑,可以將紙板層壓到箔片上來製成。此外,還可以將這種紙板與薄膜層壓,從而將其應用擴展到各種醫療包裝材料。醫療和製藥行業的包裝材料由於其最終用途,還需要可追溯的製造流程和先進的品管系統。

- 通常認為由紙或紙板製成的包裝比其他包裝材料更環保。此外,CEPI 報告稱,紙和紙板產品在各個行業的採用正在增加,特別是在製藥行業。

- 對永續包裝不斷成長的需求促使市場相關人員推出創新產品。例如,2024年6月,紙板包裝專家Keystone Folding Box推出了Push-Pak,這是一款專為藥品錠劑設計的紙板泡殼錢包。此解決方案具有簡單的推入式開啟系統,無需複雜的開啟說明。此外,更緊密、更濃縮的泡殼陣列可最大限度地減少整體包裝尺寸。

- 紙泡殼包裝是一種輕盈、靈活且環保的包裝解決方案。隨著世界各國政府加強禁止使用非生物分解的塑膠和其他對環境有害的材料,對紙張和紙板藥品泡殼包裝的需求預計將增加。

- 此外,Suzano 的報告指出,未來幾年紙張消費量將增加,預計到 2032 年將達到 4.76 億噸。鑑於世界紙張生產的很大一部分用於包裝行業,這種上升趨勢表明對藥品紙包裝的需求不斷成長。

亞太地區實現最快的產業成長

- 中國醫藥產業的蓬勃發展,為醫藥塑膠包裝產業提供了無數商機。中國政府加速醫療改革的措施也可能支持藥品包裝產業的成長。

- 活性藥物成分 (API) 製造和開發的最新進展增加了對泡殼包裝組件的需求。隨著印度擴大原料藥的生產規模,對藥物包裝選擇的需求也隨之激增。注意到這一趨勢,印度聯邦衛生部長於 2023 年 8 月宣布,根據生產連結獎勵(PLI)計劃,印度在過去一年半的時間裡增加了 38 種原料藥的產量,而此前一直依賴於宣布開始進口。

- 該地區不斷上漲的醫療成本對泡殼包裝市場產生了積極影響。亞洲國家,包括中國、印度、印尼、馬來西亞、菲律賓和泰國,擴大採用增強的醫療診斷和標準,導致醫療保健支出增加。此外,已開發市場和新興市場的藥品取得情況均有所改善,導致藥品消費量大幅增加。

- 2024 年 2 月,AP 穆勒-馬士基進行了一項研究,強調印度藥品供應鏈的重大變化。在全球化、技術進步、監管變化和醫療產品需求增加的推動下,這種轉變已將焦點從手動交易轉向自動化和策略創新。由於製藥業的這些變化,泡殼包裝市場可望進一步成長。

- 根據 IQVIA 報告,中國在原始品牌藥品上的支出已從 2018 年的 290 億美元飆升至 2023 年的 440 億美元。藥品支出的增加將與泡殼包裝的需求相對應。

- 此外,印度等國家正在修改其製藥法和指南,以加強醫療保健並促進藥品出口。這些措施預計將擴大對單位劑量藥品包裝的需求並使之多樣化。印度品牌資產基金會的報告顯示,2023年印度藥品出口額從173億美元飆升至254億美元。這種成長趨勢預計將持續下去,進一步推動國內藥品泡殼包裝的需求,以實現更安全的運輸。

醫藥泡殼包裝產業概況

藥品泡殼包裝市場按 Amcor PLC、Constantia Flexibles 和 WestRock Company 的存在進行細分。該市場由提供原料和包裝服務的大型企業以及本地參與企業組成。包裝和薄膜材料的最新發展正在塑造市場。

- 2024 年 1 月,總部位於賓州韋恩的 TekniPlex Healthcare 與 Alpek Polyester 合作推出醫藥級聚對苯二甲酸乙二醇酯 (PET)泡殼膜。這種創新薄膜含有 30% 的消費後回收 (PCR) 單體。據該公司稱,當這種泡殼薄膜與該公司的 Teknilid Push 聚酯蓋相結合時,只要必要的基礎設施到位,薄膜+蓋子泡殼系統就可以在聚酯回收鏈內完全回收。

- 2023 年 7 月,Constantia Flex 推出了 REGULA CIRC,這是一種「完全屏障」和回收再生用冷泡沫箔解決方案,適用於永續藥品泡殼包裝應用。聚乙烯密封層將取代傳統的 PVC 解。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 產業價值鏈分析

第5章市場動態

- 市場促進因素

- 單位劑量包裝的需求增加

- 各行業增加使用可回收材料

- 市場限制因素

- 禁止使用塑膠包裝材料

第6章 市場細分

- 按材質

- 塑膠(聚氯乙烯(PVC)、聚丙烯(PP))

- 紙

- 鋁

- 依技術

- 冷成型

- 熱成型

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲/紐西蘭

- 中東/非洲

- 拉丁美洲

第7章 競爭格局

- 公司簡介

- Amcor PLC

- Constantia Flexibles

- WestRock Company

- Tekni-Plex Inc.

- Huhtamaki Oyj

- Sonoco Products Company

- Winpak Ltd

- ACG Pharmapack Pvt. Ltd

- Aptar CSP Technologies Inc.

- The Dow Chemical Company

第8章投資分析

第9章 市場未來展望

簡介目錄

Product Code: 91309

The Pharmaceutical Blister Packaging Market size is estimated at USD 23.72 billion in 2025, and is expected to reach USD 33.98 billion by 2030, at a CAGR of 7.45% during the forecast period (2025-2030).

Key Highlights

- Blister packaging is crucial in the pharmaceutical industry. These specialized packaging solutions guarantee that medicinal products reach patients without tampering or damage. Blister packaging safeguards therapeutic commodities, keeping them moisture-free and shielded from external contaminants.

- Blister packaging, enhanced with sensors, plays a key role in monitoring dosing activities and ensuring clinical trials' accuracy. Consider WestRock's CerePak blister packs: they come equipped with concealed microprocessors and printed conductive inks, meticulously logging the date, time, and location of each dose. This feature is especially vital for treatment regimens that involve fluctuating dosages or a combination of placebo and active medications.

- Blister packaging typically consists of thermoformed plastic, with lids made from paper, plastic, foil, or a combination. Another common variant utilizes solely foil, crafted through a cold-stretching process. Opaque options are available to shield light-sensitive medications from harmful UV rays.

- Blister packaging is a durable solution for packaging and transporting medical essentials. It shields contents from impacts, moisture, and heat, enhancing the medicines' shelf life and transportability. The advantages of blister packaging became evident during the pandemic, as its surfaces were pivotal in the international transport and storage of medications. Yet, the potential for virus transfer via these surfaces highlighted areas for improvement, particularly in the outer materials, which packaging manufacturers will likely prioritize in the future.

- However, strict regulations and policies targeting plastic packaging are expected to present a potential challenge to the growth of the pharmaceutical blister packaging segment during the forecast period. For instance, the United States (with 16 states already on board and more anticipated) and Europe have enacted laws to curb plastic waste.

Pharmaceutical Blister Packaging Market Trends

The Paper Blister Segment May Witness Significant Growth

- Commonly referred to as blister board, the paper blister is often used for over-the-counter and prescription pharmaceuticals, vitamins, and supplements and can have its paperboard laminated to foil. Additionally, this paperboard can be laminated to film, broadening its application in diverse medical packaging materials. Moreover, given their end-use, packaging materials in the healthcare and pharmaceutical industries mandate traceable manufacturing processes and sophisticated quality control systems.

- Generally, packaging made from paper and paperboard is considered more environmentally friendly than other packaging materials. Moreover, CEPI reports a growing adoption of paper and board products across various industries, notably in the pharmaceutical industry.

- Market players are introducing innovative products in response to the rising demand for sustainable packaging. For example, in June 2024, Keystone Folding Box, a specialist in paperboard packaging, launched the "Push-Pak," a paperboard blister wallet designed for medicine tablets. This solution features a straightforward push-through opening system, eliminating the need for complex opening instructions. Additionally, its tighter and more condensed blister arrangement minimizes the overall size of the package.

- Paper blister packs provide a lightweight, flexible, and eco-friendly packaging solution. As governments worldwide intensify their bans on non-biodegradable plastics and other environmentally harmful materials, the demand for paper and paperboard pharmaceutical blister packaging is anticipated to rise.

- Further, as per a report by Suzano, paper consumption is set to climb, reaching an estimated 476 million tons by 2032. Given that a significant share of global paper production caters to the packaging industry, this upward trajectory signals a growing demand for pharmaceutical paper packaging.

Asia-Pacific to Witness Fastest Growth in the Industry

- China's booming pharmaceutical industry is set to open numerous opportunities for its pharmaceutical plastic packaging businesses. Also, initiatives by the Chinese government aimed at accelerating healthcare system reforms are likely to bolster the growth of the pharmaceutical packaging industry.

- Recent advancements in the manufacturing and development of active pharmaceutical ingredients (API) have increased the demand for blister packaging components. As India ramps up its production of APIs, the demand for pharma packaging options is witnessing a parallel surge. Highlighting this trend, the Union Health Minister announced in August 2023 that, under the production-linked incentive (PLI) scheme, India has begun producing 38 APIs previously reliant on imports over the past year and a half.

- Rising medical expenditures in the region are positively influencing the blister packaging market. Countries in Asia, including China, India, Indonesia, Malaysia, the Philippines, and Thailand, are increasingly adopting enhanced healthcare diagnostics and standards, leading to heightened medical spending. Also, advancements in drug accessibility in both developed and emerging markets have significantly boosted drug consumption, thereby elevating the demand for blister packaging in pharmaceuticals.

- In February 2024, A.P. Moller-Maersk conducted a study highlighting a major transformation in India's pharmaceutical supply chain. This shift, driven by globalization, technological advancements, regulatory changes, and increasing demand for healthcare products, moved the focus from manual transactions to automation and strategic innovation. As a result of these changes in the pharmaceutical industry, the market for blister packaging is poised for further growth.

- An IQVIA report highlights that China's spending on original branded pharmaceuticals surged from USD 29 billion in 2018 to an impressive USD 44 billion in 2023. This increase in pharmaceutical spending is set to drive a corresponding demand for blister packs.

- Moreover, countries like India are revising their pharmaceutical laws and guidelines to enhance healthcare and boost medicine exports. These initiatives are likely to drive a growing and diversifying demand for unit-dose pharmaceutical packaging. As reported by the India Brand Equity Foundation, India's pharmaceutical exports surged to USD 25.4 billion in 2023, a notable increase from USD 17.3 billion. This upward trend is anticipated to continue, further fueling the demand for pharmaceutical blister packs in the country for safer shipments.

Pharmaceutical Blister Packaging Industry Overview

The pharmaceutical blister packaging market is fragmented with the presence of Amcor PLC, Constantia Flexibles, and WestRock Company. The market comprises major and local players supplying raw materials and packaging services. The latest developments in packaging and film materials are shaping the market.

- January 2024: TekniPlex Healthcare, headquartered in Wayne, Pennsylvania, partnered with Alpek Polyester to introduce a pharmaceutical-grade polyethylene terephthalate (PET) blister film. This innovative film incorporates 30% post-consumer recycled (PCR) monomers. According to the company, when this blister film is paired with its Teknilid Push polyester lidding, the resulting film-plus-lidding blister system can be fully recycled within the polyester recycling stream, provided the necessary infrastructure is in place.

- July 2023: Constantia Flexibles revealed REGULA CIRC, its 'total barrier,' designed-for-recycling cold-form foil solution for sustainable pharmaceutical blister packaging applications. A polyethylene sealing layer is set to replace traditional PVC solutions; a transition is seeking to simplify the sorting process, improve the pack's recyclability, and, in turn, improve material recovery.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption And Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Demand for Unit Dose Packaging

- 5.1.2 Growing Use of Recyclable Materials Across the Industry

- 5.2 Market Restraints

- 5.2.1 Ban on Plastic Packaging Materials

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastic (Poly Vinyl Chloride (PVC), Polypropylene (PP))

- 6.1.2 Paper

- 6.1.3 Aluminum

- 6.2 By Technology

- 6.2.1 Cold Forming

- 6.2.2 Thermoformed

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Middle East and Africa

- 6.3.6 Latin America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Constantia Flexibles

- 7.1.3 WestRock Company

- 7.1.4 Tekni-Plex Inc.

- 7.1.5 Huhtamaki Oyj

- 7.1.6 Sonoco Products Company

- 7.1.7 Winpak Ltd

- 7.1.8 ACG Pharmapack Pvt. Ltd

- 7.1.9 Aptar CSP Technologies Inc.

- 7.1.10 The Dow Chemical Company

8 INVESTMENT ANALYSIS

9 MARKET FUTURE OUTLOOK

02-2729-4219

+886-2-2729-4219

醫用泡殼包裝市場規模、佔有率和趨勢分析報告:按材料、技術、類型、應用、地區和細分市場分類(2026-2033 年)

醫用泡殼包裝市場規模、佔有率和趨勢分析報告:按材料、技術、類型、應用、地區和細分市場分類(2026-2033 年) 全球藥品泡殼包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球藥品泡殼包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 藥品泡殼包裝市場規模、佔有率、成長分析(按產品類型、技術類型、材料類型、應用和地區分類)-2026-2033年產業預測泡罩包裝藥品市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,以及2024年至2032年的預測

藥品泡殼包裝市場規模、佔有率、成長分析(按產品類型、技術類型、材料類型、應用和地區分類)-2026-2033年產業預測泡罩包裝藥品市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,以及2024年至2032年的預測 全球醫療保健泡殼包裝市場

全球醫療保健泡殼包裝市場 醫藥泡殼包裝市場規模、佔有率、成長分析(按類型、按材料、按最終用途、按技術和按地區)- 行業預測,2025 年至 2032 年

醫藥泡殼包裝市場規模、佔有率、成長分析(按類型、按材料、按最終用途、按技術和按地區)- 行業預測,2025 年至 2032 年 全球藥品泡殼包裝市場:按材料、技術、產品、應用、最終用戶、地區 - 趨勢分析、競爭格局、預測,2019-2030

全球藥品泡殼包裝市場:按材料、技術、產品、應用、最終用戶、地區 - 趨勢分析、競爭格局、預測,2019-2030 2030 年藥品泡殼包裝市場預測:按產品類型、材料、技術、應用、最終用戶和地區進行的全球分析

2030 年藥品泡殼包裝市場預測:按產品類型、材料、技術、應用、最終用戶和地區進行的全球分析 醫療保健泡殼包裝市場:成長、未來前景、競爭分析,2024-2032年

醫療保健泡殼包裝市場:成長、未來前景、競爭分析,2024-2032年