|

市場調查報告書

商品編碼

1684574

醫藥泡殼包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Pharmaceutical Blister Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

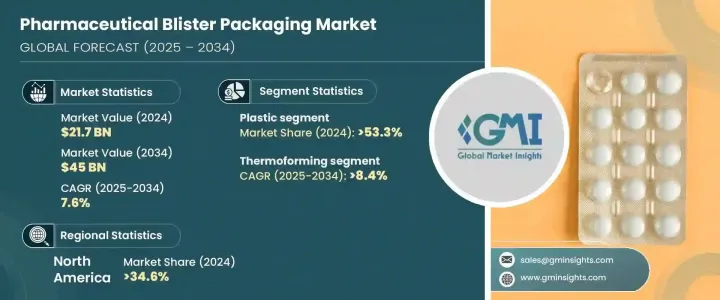

2024 年全球醫藥泡殼包裝市場價值為 217 億美元,預計 2025 年至 2034 年期間複合年成長率將達到 7.6%。這一成長反映了全球對安全、高效和保護性醫藥產品包裝解決方案的需求激增。藥品泡殼包裝因其能夠提供增強的產品保護、延長保存期限並提高藥物依從性而成為製造商和醫療保健提供者的首選。

包裝材料和技術的不斷進步,加上對永續解決方案的日益重視,進一步推動了市場的成長。製藥業的蓬勃發展、慢性病發病率的上升以及對符合嚴格監管標準的包裝解決方案的需求也推動了這一需求。此外,泡殼包裝提供的便利性和易用性,例如內容物的清晰可視性和防篡改功能,繼續鞏固其作為現代醫藥包裝基本解決方案的地位。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 217億美元 |

| 預測值 | 450億美元 |

| 複合年成長率 | 7.6% |

就材料而言,市場分為塑膠、鋁箔和紙張,其中塑膠領域處於領先地位,到 2024 年將佔據 53.3% 的市場佔有率。 PVC、PET 和聚碳酸酯等塑膠因其用途廣泛且具有成本效益的特性而被廣泛使用,使其成為保護敏感醫藥產品免受潮濕、光照和污染的理想選擇。這些材料還具有出色的阻隔性能,使製造商能夠設計各種形狀和尺寸的泡殼包裝,滿足製藥公司的多樣化需求。塑膠的柔韌性和耐用性使製造商能夠在設計上進行創新,同時確保遵守安全和品質標準。

市場也根據技術進行細分,包括冷成型、熱成型和熱封。尤其是熱成型,其發展勢頭十分迅猛,預計將以 8.4% 的強勁複合年成長率成長,到 2034 年將達到 245 億美元。該技術因其能夠大規模生產高品質、高成本效益的泡殼包裝而脫穎而出。透過將塑膠片材加熱至柔韌狀態並將其塑造成精確的腔體尺寸,熱成型可確保藥片、膠囊和其他藥品得到安全存放,從而最大限度地降低儲存和運輸過程中損壞或污染的風險。

2024年,北美佔據藥品泡殼包裝市場的34.6%,其中美國的成長最為顯著。以患者為中心的醫療保健包裝的需求不斷成長以及對永續解決方案的日益關注刺激了該地區的創新。製造商正在引入可回收材料,如可生物分解的塑膠和紙質替代品來解決環境問題。此外,包裝設計也得到了增強,具有防篡改功能和更高的可用性,支持更好地遵守藥物治療並確保患者安全,進一步鞏固了該地區在市場上的主導地位。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 中斷

- 未來展望

- 製造商

- 經銷商

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 推出永續且符合法規要求的泡殼包裝解決方案

- 慢性病盛行率不斷上升推動藥品消費

- 學名藥生產擴張

- 冷成型箔技術進步增強了藥物保護

- 電子藥局的成長和對防竄改包裝解決方案的需求

- 產業陷阱與挑戰

- 針對不同藥物配方訂製泡殼包裝的複雜性

- 經濟放緩對醫藥包裝投資的影響

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按材料,2021 年至 2034 年

- 主要趨勢

- 塑膠

- 鋁箔

- 紙

第 6 章:市場估計與預測:按技術,2021 年至 2034 年

- 主要趨勢

- 冷成型

- 熱成型

- 熱封

第 7 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 片劑和膠囊

- 醫療設備

- 注射劑

- 其他

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- ACG

- Amcor

- Aptar

- Borealis

- Caprihans

- Carcano

- Constantia

- Dow

- Honeywell

- Huhtamaki

- Renolit

- Rohrer

- Romaco

- Sonoco

- Sudpack

- Syensqo

- Tekni-Plex

- Tjoapack

- VinylPlus

- WestRock

- Winpak

The Global Pharmaceutical Blister Packaging Market was valued at USD 21.7 billion in 2024 and is projected to grow at an impressive CAGR of 7.6% between 2025 and 2034. This growth reflects a surging demand for secure, efficient, and protective packaging solutions for pharmaceutical products worldwide. Pharmaceutical blister packaging has emerged as a preferred choice among manufacturers and healthcare providers due to its ability to offer enhanced product protection, extended shelf life, and improved medication adherence.

Rising advancements in packaging materials and technologies, coupled with an increasing emphasis on sustainable solutions, are further fueling market growth. The demand is also driven by the growing pharmaceutical industry, rising prevalence of chronic diseases, and a need for packaging solutions that comply with stringent regulatory standards. Moreover, the convenience and ease of use offered by blister packaging, such as clear visibility of contents and tamper-evident features, continue to solidify its position as an essential solution for modern pharmaceutical packaging.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.7 Billion |

| Forecast Value | $45 Billion |

| CAGR | 7.6% |

In terms of material, the market is categorized into plastic, aluminum foil, and paper, with the plastic segment leading, holding 53.3% of the market share in 2024. Plastics such as PVC, PET, and polycarbonate are widely used due to their versatile and cost-effective nature, making them an ideal choice for protecting sensitive pharmaceutical products from moisture, light, and contamination. These materials also offer excellent barrier properties and enable manufacturers to design blister packs in a wide array of shapes and sizes, meeting the diverse needs of pharmaceutical companies. The flexibility and durability of plastics allow manufacturers to innovate in design while ensuring adherence to safety and quality standards.

The market is also segmented by technology, including cold forming, thermoforming, and heat sealing. Thermoforming, in particular, is gaining significant traction and is projected to grow at a robust CAGR of 8.4%, reaching USD 24.5 billion by 2034. This technology stands out for its ability to produce high-quality and cost-efficient blister packs on a large scale. By heating plastic sheets into a pliable state and molding them into precise cavity dimensions, thermoforming ensures that tablets, capsules, and other pharmaceutical products are securely housed, minimizing the risk of damage or contamination during storage and transport.

In 2024, North America accounted for 34.6% of the pharmaceutical blister packaging market, with the United States experiencing remarkable growth. The increasing demand for patient-centric healthcare packaging and the rising focus on sustainable solutions have spurred innovation in the region. Manufacturers are introducing recyclable materials like biodegradable plastics and paper-based alternatives to address environmental concerns. Additionally, packaging designs are being enhanced with tamper-evident features and improved usability, supporting better medication adherence and ensuring patient safety, further solidifying the region's dominance in the market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Disruptions

- 3.1.3 Future outlook

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.2 Profit margin analysis

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Introduction of sustainable and regulatory-compliant blister packaging solutions

- 3.5.1.2 Growing prevalence of chronic diseases driving pharmaceutical consumption

- 3.5.1.3 Expansion of generic drug manufacturing

- 3.5.1.4 Advancements in cold form foil technology for enhanced drug protection

- 3.5.1.5 Growth in e-pharmacies and demand for tamper-evident packaging solutions

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Complexities in customization of blister packaging for diverse drug formulations

- 3.5.2.2 Impact of economic slowdowns on pharmaceutical packaging investments

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Aluminum foil

- 5.4 Paper

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Cold forming

- 6.3 Thermoforming

- 6.4 Heat seal

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Tablets & capsules

- 7.3 Medical devices

- 7.4 Injectables

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ACG

- 9.2 Amcor

- 9.3 Aptar

- 9.4 Borealis

- 9.5 Caprihans

- 9.6 Carcano

- 9.7 Constantia

- 9.8 Dow

- 9.9 Honeywell

- 9.10 Huhtamaki

- 9.11 Renolit

- 9.12 Rohrer

- 9.13 Romaco

- 9.14 Sonoco

- 9.15 Sudpack

- 9.16 Syensqo

- 9.17 Tekni-Plex

- 9.18 Tjoapack

- 9.19 VinylPlus

- 9.20 WestRock

- 9.21 Winpak

全球藥品泡殼包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球藥品泡殼包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 藥品泡殼包裝市場規模、佔有率、成長分析(按產品類型、技術類型、材料類型、應用和地區分類)-2026-2033年產業預測泡罩包裝藥品市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,以及2024年至2032年的預測

藥品泡殼包裝市場規模、佔有率、成長分析(按產品類型、技術類型、材料類型、應用和地區分類)-2026-2033年產業預測泡罩包裝藥品市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,以及2024年至2032年的預測 全球醫療保健泡殼包裝市場

全球醫療保健泡殼包裝市場 醫藥泡殼包裝市場規模、佔有率、成長分析(按類型、按材料、按最終用途、按技術和按地區)- 行業預測,2025 年至 2032 年

醫藥泡殼包裝市場規模、佔有率、成長分析(按類型、按材料、按最終用途、按技術和按地區)- 行業預測,2025 年至 2032 年 藥品泡殼包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)

藥品泡殼包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030) 全球藥品泡殼包裝市場:按材料、技術、產品、應用、最終用戶、地區 - 趨勢分析、競爭格局、預測,2019-2030

全球藥品泡殼包裝市場:按材料、技術、產品、應用、最終用戶、地區 - 趨勢分析、競爭格局、預測,2019-2030 2030 年藥品泡殼包裝市場預測:按產品類型、材料、技術、應用、最終用戶和地區進行的全球分析

2030 年藥品泡殼包裝市場預測:按產品類型、材料、技術、應用、最終用戶和地區進行的全球分析 醫療保健泡殼包裝市場:成長、未來前景、競爭分析,2024-2032年

醫療保健泡殼包裝市場:成長、未來前景、競爭分析,2024-2032年