|

市場調查報告書

商品編碼

1521635

全球磁性市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Magnetics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

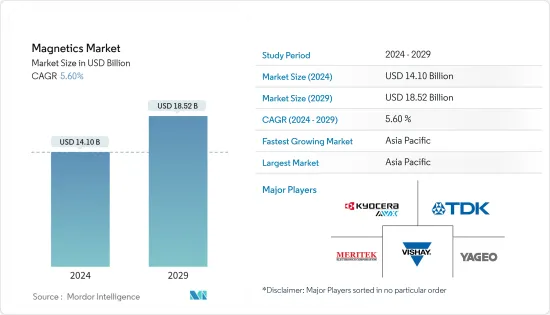

預計2024年全球磁材市場規模將達141億美元,2024年至2029年複合年成長率為5.60%,2029年將達到185.2億美元。

磁性元件廣泛應用於先進工業設備和消費性電器產品,從冰箱、電視到通訊設備。磁性元件在汽車、儀表板顯示器電壓監控、內部和外部照明、氣候控制以及其他系統電源方面發揮關鍵作用。這些零件用於行動電話、電腦、通訊系統和其他電子產品。

主要亮點

- 全球對 HPC 和 AI 的需求爆炸性成長。同樣,對智慧型手機、個人電腦和基礎設施的需求保持穩定。智慧型手機銷售量預計將在 2024 年大幅復甦,從而推動對這些磁性元件的需求。行動電話中使用高頻電感,幫助您快速穩定地上網。此外,隨著行動通訊網路的進步,智慧型手機中安裝的電感器數量顯著增加。電感器增強了智慧型手機的各種功能,例如彩色液晶顯示器和延長的電池壽命。

- 智慧型手機OEM將在 2024 年透過生成式 AI 功能和額外的儲存容量來增強其支援人工智慧的智慧型手機,從而產生對更長電池壽命的需求。此外,隨著技術的進步,消費者更喜歡具有先進技術的產品而不是舊設備,這推動了智慧型手機的銷售。

- 全球對基於國家電網連接(超級電網)和直流電的再生能源來源(例如燃料電池、風力發電和太陽能發電)的需求不斷成長,對磁性元件的需求也在成長。

- 傳統上,變壓器是由鐵製成的,但隨著材料的發展,矽鋼、非晶質鋼、鐵氧體陶瓷等材料由於其高滲透性已開始用作變壓器的鐵芯材料。同樣,鐵或鐵氧體等磁性材料用作電感器和 EMI 濾波器的核心材料,銅通常用於線圈。

- 目前,隨著自動駕駛技術和ADAS技術的快速發展,汽車配備了雷達、攝影機、LiDAR等眾多感測器,磁性元件也隨之快速成長。隨著汽車產業的不斷發展,主要供應商不斷投資於產品開發和改進,以滿足消費者的需求。

- 例如,2024 年 1 月,TDK 公司推出了 KLZ2012-A 系列新型電感器,為汽車音訊匯流排 (A2B) 應用提供高耐用性、寬工作範圍和高電感容差。量產將於 2024 年 1 月開始。 A2B 技術的開發是為了減輕各種通訊總線電纜線束的重量,最終目標是提高車輛燃油效率。

磁性市場趨勢

工業用途(馬達/UPS)推動成長

- 工業馬達是一種將電能轉換為機械能的電氣設備。它通常由交流 (AC) 源供電,例如發電機或電網。工業馬達專門設計用於為各行業使用的各種設備和機器提供動力和運動。由於它們需要承受高負載並在惡劣環境中運行,因此這些馬達通常比住宅或商業環境中使用的馬達更耐用、更強大。工業馬達和應用對磁電感不斷成長的需求將推動市場的發展。

- 根據工業能源加速器的報告,全球企業消耗的大部分電力來自數以百萬計的運作中的馬達。這些馬達對於為各個領域的基本工業流程和輔助系統提供動力至關重要,包括通風、壓縮空氣生成和抽水。此外,工業馬達市場最近推出了設計用於交流和直流電源運行的通用馬達。對這些馬達的需求不斷成長以及各個供應商不斷增加的開發可能會增加磁性元件的應用。

- 工業馬達的設計和功能在很大程度上依賴磁感應,這是產生扭矩的主要方法。透過充分理解磁感應原理並最佳化各種設計元素,工程師可以開發出適合各種應用的高效能、高性能馬達。

- 由於資料中心投資的增加,對資料中心不斷電系統(UPS)系統的需求正在強勁成長。隨著各行業數位化業務和服務的拓展,對資料儲存、處理和管理的需求迅速成長。因此,為了滿足這些要求,人們在資料中心基礎設施方面進行了大量投資。根據Cloudscene統計,截至2023年9月,中國擁有448個資料中心,比亞太地區任何其他國家都多,蘊藏著巨大的市場機會。

中國正在經歷快速成長

- 由於中國家電、汽車和醫療設備產量的增加,預計在預測期內對被動電子產品的需求將保持強勁。

- Rayming PCB and Assembly表示,近年來,中國繼續在電子製造業中佔據主導地位。儘管最近與美國有貿易往來,但該國仍然是電子產品的重要製造地。作為大型製造業,中國約50%的筆記型電腦和行動電話出口到全球。

- 全球電子市場從2022年的35,549.4億美元成長到2023年的37,393.7億美元。在全球電子領域,中國佔收益的很大比例。該國躋身頂級電子產品生產國。我們生產各種電子產品,從消費性電子產品到工業零件。南方東莞、深圳等城市設有工廠。我們在上海和青雲也有工廠。

- 中國在筆記型電腦製造商的全球生產佔有率中佔有顯著的佔有率。儘管中國依賴進口半導體,但對於許多世界頂級筆記型電腦品牌來說,中國仍然是一個不錯的選擇。崑山和重慶是最大的兩個筆記型電腦製造叢集,此外還有東莞、深圳等熱門電子生產基地。這些中心以生產筆記型電腦、零件和配件而聞名。

- 中國約有160個人口超過100萬的城市,而美國祇有9個。因此,電子設備製造和消費的擴展預計將增加所有家用電器和消費性電子設備中對電流管理的各種被動元件的需求。

- 過去 15 年,中國針對電動車產業所做的努力是該國近代史上最成功的產業政策案例之一。包括補貼在內的大規模政府干涉使得國內工業和市場同步成長。該政策的推出時機至關重要,因為它恰逢電池技術的進步和消費者對電動車接受度的不斷提高。重要的是,許多老牌汽車公司直到最近才拒絕電動車技術。

- 同時,中國競爭對手迅速抓住機遇,在技術上超越了擁有數十年內燃機技術知識產權累積的跨國公司。中國也是全球領先的鋰電池生產國,鋰電池是電動車的關鍵零件。根據國際能源總署(IEA)的數據,中國生產了65%的電池和80%的正極,能源部的估計甚至更高。由此,呈現了該國汽車產業調查市場的成長前景。

磁性行業概況

磁性材料市場是分散的,由在其產品上投入大量資金的老牌廠商組成。新參與企業需要高額投資。這些公司透過強力的競爭策略生存,主要參與者是 TDK Corporation、Yageo Corporation、Meritek Electronics Corporation、AVX Corporation(Kyocera Group)和 Vishay Intertechnolo。

2024 年 1 月,TDK Corporations 旗下子公司 TDK Ventures Inc. 投資了新加坡一家致力於數位和能源轉型的高科技公司 Silicon Box。我們計劃透過矽盒加速半導體封裝創新市場。

2023 年 11 月,Bourns 推出了一系列空心線圈電感器,具有高自諧振頻率、高 Q 值和嚴格的電感容差。 AC4842 RAir 線圈電感器系列提供低損耗、高頻解決方案,為射頻應用設計人員提供廣泛的高 Q 值解決方案選擇。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 磁性裝置類別技術概述

- 市場宏觀趨勢評估

第5章市場動態

- 市場促進因素

- 可再生能源需求增加

- 電動和自動駕駛汽車需求的增加推動磁性元件市場

- 市場挑戰

- 金屬價格上漲影響零件製造成本

第6章 市場細分

- 按類型

- 繞線電感

- 多層電感器

- 薄膜電感

- 鐵氧體磁芯/EMC零件

- EMI濾波器

- 射頻/電源變壓器

- 電流檢測/其他變壓器

- 按最終用戶使用情況

- 太陽能/風能

- 電動車/混合動力車用

- 工業(馬達/UPS)

- 鐵路/交通

- 消費性電子產品

- 其他最終用戶用途

- 按地區

- 中國

- 日本

- 美國

- 台灣

- 東南亞

- 韓國

- 歐洲

- 拉丁美洲

- 中東/非洲

第7章 競爭格局

- 公司簡介

- TDK Corporation

- Yageo Corporation

- Meritek Electronics Corporation

- AVX Corporation(Kyocera Group)

- Vishay Intertechnology

- Panasonic Corporation

- Taiyo Yuden Co. Ltd

- Exxelia Technology

- Bourns Inc.

- Wurth Elektronik Group

- Coilcraft Inc.

第8章市場展望

The Magnetics Market size is estimated at USD 14.10 billion in 2024, and is expected to reach USD 18.52 billion by 2029, growing at a CAGR of 5.60% during the forecast period (2024-2029).

Magnetic components are widely adopted in both advanced industrial and common household appliances, ranging from refrigerators and televisions to telecommunication devices. Magnetics plays a crucial role in cars, monitoring voltage in power supplies for dashboard displays, interior and exterior lighting, climate control, and other systems. These components are used in cell phones, computers, communication systems, and other electronic products.

Key Highlights

- The global demand for HPC and AI is exploding. Similarly, the demand for smartphones, PCs, and infrastructures is stabilizing. Smartphone sales are expected to recover significantly in 2024, driving the demand for these magnetic components. High-frequency inductors are used in mobile phones, which help with fast and stable internet surfing. Furthermore, with the advancement in mobile communication networks, the number of inductors in smartphones is growing significantly. Inductors enhance various smartphones' functions, including improving color LCD and battery life.

- Smartphone OEMs are ramping up Artificial intelligence-enabled smartphones in 2024, with generative AI capabilities and an additional storage capacity, which creates demand for better battery life. Further, with the advancement in technology, consumers prefer advanced technology products compared to older devices, which drives the sales of smartphones.

- The need for inter-country power grid connections (super grid) and renewable energy sources based on direct currents, such as fuel cells, wind power, and solar power, is expanding globally, as is the demand for magnetic components.

- Traditionally, transformers were made of solid iron; however, with the development of materials, silicon steel, amorphous steel, and ferrite ceramics have been used as core materials for transformers due to their higher penetrability. Similarly, inductors and EMI filters use iron, ferrite, and other magnetic materials as core material, and coils are usually made of copper.

- With the current rapid evolution of autonomous driving technologies and ADAS, automobiles are prepared with numerous sensors such as radars, cameras, and LiDAR, resulting in dramatic growth in magnetic components. Owing to ongoing advancement in automotive sector, key vendors are continuously investing on product developments and advancement to meet consumer demand.

- For instance, in January 2024, TDK Corporation launched a new inductor KLZ2012-A series, designed for automotive audio bus (A2B) applications with high durability, a wide operation range, and greater inductance tolerance. The company announced that the mass production of these new product series started in January 2024. A2B technology was developed to decrease the weight of cable harnesses containing of a broad variety of telecommunication buses, pointing at its final goal of amplified fuel efficiency of automobiles.

Magnetics Market Trends

Industrial (Motors/UPS) to Witness the Growth

- Industrial motors are electrical devices that convert electrical energy into mechanical energy. They are commonly powered by alternating current (AC) sources like generators and power grids. Industrial motors are specifically engineered to supply power and movement to various equipment and machinery utilized in different industries. Due to their requirement to endure heavy loads and function in challenging environments, these motors are typically more durable and potent than those employed in residential or commercial settings. The growing need for magnetic inductance in industrial motor applications will drive the market.

- The Industrial Energy Accelerator reports that a significant portion of the global electrical energy consumed by companies is attributed to the millions of electrical motors in operation. These motors are crucial in powering essential industrial processes and auxiliary systems such as ventilation, compressed air generation, and water pumping across various sectors. Additionally, there has been a recent introduction of universal motors in the industrial motors market, designed to work with both AC and DC power sources. The increasing demand for these motors and growing developments by the various vendors will increase the applications of magnetic components.

- The design and functioning of industrial motors heavily rely on magnetic induction, which serves as the primary method for producing torque. Engineers can develop efficient and high-performing motors suitable for various applications by thoroughly comprehending magnetic induction principles and optimizing different design elements.

- The demand for data center uninterruptable power supply (UPS) systems is experiencing significant growth due to the increasing investments in data centers. As various industries expand their digital operations and services, there is a surge in demand for data storage, processing, and management. Consequently, substantial investments are being made in data center infrastructure to meet these requirements. According to Cloudscene, as of September 2023, there were 448 data centers in China, the most of any country or territory in the Asia-Pacific region, where market opportunities can be found significantly.

China to Witness Rapid Growth

- The demand for passive electronics is expected to remain strong in the forecast period due to increased consumer electronics, automotive, and medical equipment production in China.

- According to Rayming PCB and Assembly, China has continued dominating the electronics manufacturing industry for some years. This country is an integral manufacturing place for electronics despite its recent trade with the United States. As a large manufacturing company, China exports about 50% of laptops and cell phones globally.

- The global electronics market grew from USD 3554.94 billion in 2022 to USD 3739.37 billion in 2023. In the global electronics sector, China contributes a large percentage of revenue. This country is ranked among the top producers of electronic devices. It produces various electronics products, ranging from consumer electronics to industrial components. Cities such as Dongguan and Shenzhen in the South have factories. In addition, Shanghai and Choingun are home to factories.

- China produces a prominent share of laptop manufacturers globally. Despite China's dependence on imported semiconductors, this country remains a good option for many world-class laptop brands. Kunshan and Chongqing are the two biggest clusters for laptop manufacturing and other popular electronic production hubs, like Dongguan and Shenzhen. These hubs are known for producing laptops, components, and accessories.

- The country also holds a significant consumer market considering the country's large population, with about 160 Chinese cities having a population crossing one million people, compared to the US, having only nine cities that incorporate more than one million people. Thus, the growing electronics manufacturing and consumption are expected to drive the need for various passive components to address electric flow management in all consumer and household electronics.

- China's initiatives targeting the EV industry over the past 15 years are one of the most successful cases of industrial policy in the country's recent history. Extensive government interventions, including subsidies, enabled the domestic industry and the market to grow simultaneously. The timing of the policies was crucial because they coincided with and magnified technological advancements in battery technology and greater consumer acceptance of EVs. Importantly, many existing automotive companies dismissed EV technology until recently.

- Meanwhile, their Chinese competitors quickly grasped the opportunity to technologically leapfrog multinational corporations with decades of IP accumulated in internal combustion engine technology. China is also by far the main producer of lithium batteries globally, which are the main component in EVs. According to the International Energy Agency (IEA), the country accounts for 65% of battery and 80% of cathode production, and the Department of Energy's estimate is even higher. Thus, the growing prospect of the market studied in the country's automotive sector is shown.

Magnetics Industry Overview

The magnetics market is fragmented, comprising long-standing established players who have made significant investments in the product. The new players entering the market require high investments. The companies can sustain themselves through powerful competitive strategies, and key players are TDK Corporation, Yageo Corporation, Meritek Electronics Corporation, AVX Corporation (Kyocera Group), and Vishay Intertechnolo.

* In January 2024, TDK Corporations subsidiary TDK Ventures Inc. invested in Singaporean tech company Silicon Box for digital and energy transformation. It plans to accelerate the market for semiconductor packaging innovations through Silicon Box.

* In November 2023, The Bourns introduced an air coil inductor series with high self-resonant frequency, high Q, and tight inductance tolerance. The Model AC4842R Air Coil Inductor Series offers a low-loss, high-frequency solution that gives RF application designers a wider range of high-Q solution options.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Technological overview of Magnetic Device Categories

- 4.4 Assessment of Macro trends in the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand For Renewable Energy

- 5.1.2 Rising Demand For Electric and Autonomous Vehicles Drives Magnetic Components Market

- 5.2 Market Challenges

- 5.2.1 Rising Metal Prices Impacting Component Production Costs

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Wire Wound Inductor

- 6.1.2 Multi-layer Inductor

- 6.1.3 Thin Film Inductor

- 6.1.4 Ferrite Cores and EMC Components

- 6.1.5 EMI Filters

- 6.1.6 RF/Power Transformers

- 6.1.7 Current Sense and Other Transformers

- 6.2 By End-user Application

- 6.2.1 Photovoltaics and wind

- 6.2.2 EV/HEV

- 6.2.3 Industrial (Motors/UPS)

- 6.2.4 Rail/Transportation

- 6.2.5 Consumer Electronics

- 6.2.6 Other End-user Applications

- 6.3 By Geography

- 6.3.1 China

- 6.3.2 Japan

- 6.3.3 United States

- 6.3.4 Taiwan

- 6.3.5 South East Asia

- 6.3.6 South Korea

- 6.3.7 Europe

- 6.3.8 Latin America

- 6.3.9 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 TDK Corporation

- 7.1.2 Yageo Corporation

- 7.1.3 Meritek Electronics Corporation

- 7.1.4 AVX Corporation (Kyocera Group)

- 7.1.5 Vishay Intertechnology

- 7.1.6 Panasonic Corporation

- 7.1.7 Taiyo Yuden Co. Ltd

- 7.1.8 Exxelia Technology

- 7.1.9 Bourns Inc.

- 7.1.10 Wurth Elektronik Group

- 7.1.11 Coilcraft Inc.

8 MARKET OUTLOOK

鐵氧體磁粉市場報告:按應用和地區分類(2026-2034 年)

鐵氧體磁粉市場報告:按應用和地區分類(2026-2034 年) 軟磁粉市場:材料類型、製造技術、先進磁化技術和應用分類-2026-2032年全球市場預測

軟磁粉市場:材料類型、製造技術、先進磁化技術和應用分類-2026-2032年全球市場預測 金屬芯PCB市場分析及預測(至2035年):依類型、產品、技術、材料類型、應用、最終用戶、組件、安裝類型、製程及解決方案分類異向性磁粉市場:依材料種類、製造流程、磁取向及最終用途分類,全球預測(2026-2032年)鐵鎳鉬合金軟磁粉末磁芯市場(按磁芯類型、頻率範圍、額定功率、鎳含量、應用、終端用戶行業和銷售管道),全球預測,2026-2032年

金屬芯PCB市場分析及預測(至2035年):依類型、產品、技術、材料類型、應用、最終用戶、組件、安裝類型、製程及解決方案分類異向性磁粉市場:依材料種類、製造流程、磁取向及最終用途分類,全球預測(2026-2032年)鐵鎳鉬合金軟磁粉末磁芯市場(按磁芯類型、頻率範圍、額定功率、鎳含量、應用、終端用戶行業和銷售管道),全球預測,2026-2032年 矽鐵合金材料市場規模、佔有率和成長分析(按產品類型、應用、最終用戶、分銷管道和地區分類)- 產業預測(2026-2033 年)

矽鐵合金材料市場規模、佔有率和成長分析(按產品類型、應用、最終用戶、分銷管道和地區分類)- 產業預測(2026-2033 年) 粉末磁芯:全球市佔率及排名、總收入及需求預測(2025-2031年)鐵矽鋁合金磁粉芯:全球市佔率及排名、總收入及需求預測(2025-2031年)

粉末磁芯:全球市佔率及排名、總收入及需求預測(2025-2031年)鐵矽鋁合金磁粉芯:全球市佔率及排名、總收入及需求預測(2025-2031年) 全球金屬芯PCB市場

全球金屬芯PCB市場 全球Sendust粉磁芯市場分析及預測(至2030年)

全球Sendust粉磁芯市場分析及預測(至2030年)