|

市場調查報告書

商品編碼

1444888

智慧廢棄物管理 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Smart Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

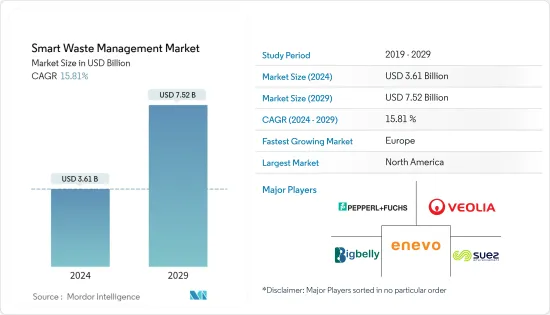

智慧廢棄物管理市場規模預計到 2024 年為 36.1 億美元,預計到 2029 年將達到 75.2 億美元,在預測期內(2024-2029 年)CAGR為 15.81%。

根據世界銀行的數據,全球每年產生約 13 億噸廢棄物。這一成長可歸因於各地區快速的城市化和工業化。

主要亮點

- 智慧廢棄物管理市場正變得越來越有吸引力,支持市場擴張。智慧廢棄物管理市場的發展得到了包括即時廢棄物管理系統的一次性標籤、容器和吸塵器等產品的幫助。廢棄物管理系統的使用不斷增加也是環境問題日益嚴重的結果。

- 智慧廢棄物管理是發展智慧城市(以及水管理、能源管理、交通管理等)以改善城市地區生活方式的關鍵面向。各地區擴大採用智慧城市舉措,支持了智慧廢棄物管理市場的成長。

- 廢棄物管理行業涉及各種活動,例如收集、運輸、處置和回收。該行業在廢棄物管理的不同階段一直面臨效率問題。準確地說,營運成本與廢棄物的收集和運輸相對應,從而導致擴大採用智慧廢棄物管理。

- 廢棄物收集物流的日益複雜性以及遵守廢棄物處理相關法規的需要需要更好的廢棄物管理解決方案,而這些解決方案可以透過使用物聯網感測器、RFID、GPS 等技術來實現。目前正處於起步階段,由於商業上可行的技術和營運效益的存在,預計將實現健康成長。

- 由於阻止病毒傳播所需的嚴格封鎖和社會隔離,COVID-19 對智慧廢棄物管理市場產生了不利影響。對與智慧廢棄物管理技術結合使用的設備和儀器的需求受到不確定的經濟環境、部分企業關閉和消費者信心不佳的影響。疫情期間,供應鏈和物流運作都受到阻礙。然而,由於政府持續採取的措施和監管的放鬆,預計智慧垃圾管理產業將在疫情後的環境中加速發展。

智慧廢棄物管理市場趨勢

透過物聯網進行智慧垃圾收集,促進市場成長

- 推動智慧廢棄物管理市場的關鍵因素之一是,由於智慧城市的創建,為城市地區提供了更好的生活品質,因此對智慧廢棄物管理的需求不斷成長——此外,市場受益於跨地區採用智慧城市舉措。

- 在智慧收集領域,物聯網的出現徹底改變了廢棄物處理公司的營運成本,並解決了這些問題。提供垃圾收集智慧解決方案的公司主要專注於三種解決方案—智慧監控、路線最佳化和分析。透過部署感測器、網路基礎設施和資料視覺化平台,廢棄物管理公司已經能夠產生可行的見解,從而做出明智的決策。

- 透過在垃圾箱附近使用液位感測器(有時還有攝影機),公司能夠根據垃圾箱中的垃圾量來規劃車隊卡車,從而減少不必要的車隊燃料消耗,並有助於減少城市的碳排放。此外,使用物聯網,車隊營運可能比以往更有效率。例如,物聯網支援的車隊管理解決方案是 Evreka 的車隊管理軟體。此外,這種方法將為管理者和員工提供一個結構化的環境。

- 美國、阿拉伯聯合大公國、英國等一些城市的市政當局與智慧垃圾管理創新者(如 Enevo、Smartbin、Bigbelly 等)合作,節省了約 30% 的垃圾收整合本。由於商業技術提供者的存在,加上智慧城市計畫和物聯網感測器成本的下降,市場正在被推動強勁成長。

北美將佔據最大市場佔有率

- 美國智慧城市越來越頻繁地使用智慧廢棄物管理解決方案來解決廢棄物收集和處置問題,預計將促進市場銷售。此外,北美地區減少碳排放的嚴格規定預計將在未來幾年推動市場銷售。政府加大力度促進永續發展和實現淨零廢棄物,將繼續推動該地區的需求。

- 美國和加拿大約 22% 的城市已經實施了戰略計劃,而全球這一比例僅為 7%。光是美國就佔了每年產生的垃圾的大部分,大約有 2.3 億噸垃圾,其中很大一部分是由私人實體處理的。由於政府提倡永續發展、到 2020 年實現零廢棄物的舉措,以及智慧城市舉措在城市高度集中地區的滲透,預計北美將佔據智慧廢棄物管理市場的最大佔有率。

智慧廢棄物管理產業概述

由於少數參與者佔據主要市場佔有率,智慧廢棄物管理市場得到整合。此外,人們需要提高認知,這使得參與者進入市場變得具有課題性。市場上一些主要的參與者包括蘇伊士環境服務公司、威立雅環境服務公司、Enevo、倍加福有限公司、Smartbin (OnePlus Systems Inc.)、IBM公司、Bigbelly Inc.、Covanta Holding Corporation等。

- 2022 年 2 月 - 永續廢棄物和能源解決方案供應商卡萬塔 (Covanta) 與李縣固體廢棄物資源回收設施之間的公私關係將持續到 2031 年。

- 2022 年 9 月 - Smarter Sorting 新創公司與 Republic Services, Inc. 合作,進入廢棄物管理市場並提高其產品的永續性。使用資料庫對廢棄物進行正確分類並根據其類別進行分類。因此,進一步廢棄物管理所需的時間和金錢都減少了。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 市場定義和範圍

- 研究假設

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場洞察

- 市場概況

- 產業利害關係人分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者的議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭激烈程度

第 5 章:市場動態

- 市場促進因素

- 增加廢棄物量以提振市場

- 智慧城市的不斷採用促進市場繁榮

- 市場課題

- 實施成本高昂

- Covid-19 對全球智慧廢棄物管理整體市場的影響

第 6 章:技術概覽

- 技術概覽

- 智慧廢棄物管理階段

- 智慧收藏

- 智慧處理

- 智慧能源回收

- 智慧處置

第 7 章:市場區隔

- 依解決方案

- 車隊的管理

- 遠端監控

- 分析

- 依廢物類型

- 工業廢料

- 生活垃圾

- 地理

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 印度

- 中國

- 澳洲

- 日本

- 亞太其他地區

- 世界其他地區

- 北美洲

第 8 章:競爭格局

- 公司簡介

- Suez Environmental Services

- Veolia Environmental Services

- Enevo

- Smartbin (OnePlus Systems Inc.)

- Bigbelly Inc.

- Covanta Holding Corporation

- Evoeco

- Pepperl+Fuchs GmbH

- IBM Corporation

- BIN-e

第 9 章:投資分析

第 10 章:市場機會與未來趨勢

The Smart Waste Management Market size is estimated at USD 3.61 billion in 2024, and is expected to reach USD 7.52 billion by 2029, growing at a CAGR of 15.81% during the forecast period (2024-2029).

According to the World Bank, across the globe, about 1.3 billion metric tons of waste is generated every year. This increase can be attributed to rapid urbanization and industrialization across regions.

Key Highlights

- The Smart Waste Management Market is becoming more appealing, supporting market expansion. The development of the smart waste management market has been aided by products like disposable tags, containers, and vacuum cleaners that include real-time waste management systems. The rising use of waste management systems also results from growing environmental concerns.

- Smart waste management is a key aspect in developing smart cities (along with water management, energy management, traffic management, etc.) to provide improved lifestyles in urban areas. The increasing adoption of smart city initiatives across regions supports the growth of the smart waste management market.

- The waste management industry involves various activities, such as collection, transportation, disposal, and recycling. The industry has been facing efficiency issues at different stages of waste management. Precisely, the operational costs correspond to the collection and transport of the waste, thereby leading to the increasing adoption of smart waste management.

- The growing complexity in the logistics of waste collection and the need to comply with regulations pertaining to waste processing demand better waste management solutions, which are made possible by using technologies such as IoT sensors, RFID, GPS, etc. Although the smart waste management market is at a nascent phase, it is expected to witness healthy growth, owing to the availability of commercially viable technologies and operational benefits.

- Due to the tight lockdowns and social isolation necessary to stop the virus's transmission, COVID-19 had a detrimental effect on the market for smart waste management. The demand for equipment and instruments used in conjunction with smart waste management technologies was influenced by the uncertain economic climate, the partial corporate shutdown, and poor consumer confidence. During the epidemic, the supply chain was impeded along with logistics operations. However, due to the government's ongoing measures and relaxation of the regulations, the smart waste management industry is anticipated to pick up steam in the post-pandemic environment.

Smart Waste Management Market Trends

Smart Waste Collection Through IoT to Contribute to the Market Growth

- One of the key factors propelling the smart waste management market is the rise in demand for smart waste management due to the creation of smart cities that offer a better quality of life in urban areas-additionally, the market benefits from adopting smart city initiatives across regions.

- In the smart collection segment, the emergence of IoT has revolutionized and addressed operational costs for waste-handling companies. The companies that offer smart solutions for waste collection primarily focus on three solutions - intelligent monitoring, route optimization, and analytics. By deploying sensors, network infrastructure, and data visualization platforms, waste management companies have been able to generate actionable insights, to make informed decisions.

- By using fill-level sensors (sometimes also cameras) near the trash bins, companies have been able to plan the fleet trucks following the volume of trash in bins, thus reducing unnecessary fleet fuel consumption and contributing to reducing carbon emissions in cities. Also, fleet operations may be more productive than ever using IoT. For instance, a Fleet Management Solution backed by IoT is Evreka's Fleet Management Software. Additionally, this approach will give managers and workers a structured environment.

- The municipalities of a few cities across the United States, United Arab Emirates, United Kingdom, etc., in collaboration with smart waste management innovators (such as Enevo, Smartbin, Bigbelly, etc.), are saving around 30% of waste collection costs. Due to the presence of commercially available technology providers, coupled with smart city initiatives and decreasing cost of IoT sensors, the market is being pushed toward robust growth.

North America to Account for the Largest Market Share

- Smart waste management solutions are being used more frequently by smart cities in the U.S. to solve issues with waste collection and disposal, which is anticipated to boost market sales. Additionally, strict rules governing reducing carbon emissions across North America are expected to drive market sales in the following years. The government's increasing efforts to promote sustainability and achieve net-zero waste will keep driving up demand in the area.

- Approximately 22% of the cities in the United States and Canada have already been implementing strategic programs, compared to just 7% of cities worldwide. The United States alone contributes the majority of the annual waste produced, with approximately 230 million metric tons of trash, a significant chunk of which is handled by private entities. Owing to government initiatives that promote sustainability, to achieve zero waste by 2020, and the penetration of smart city initiatives across the high urban concentration region, North America is expected to account for the lion's share in the Smart Waste Management Market.

Smart Waste Management Industry Overview

The Smart Waste Management Market is consolidated due to a few players having a major market share. Moreover, the need for more awareness among the people is making it challenging for the players to enter the market. Some of the key players in the market are Suez Environmental Services, Veolia Environmental Services, Enevo, Pepperl+Fuchs GmbH, Smartbin (OnePlus Systems Inc.), IBM Corporation, Bigbelly Inc., Covanta Holding Corporation, among others.

- February 2022 - The public-private relationship between Covanta, a sustainable waste and energy solutions provider, and the Lee County Solid Waste Resource Recovery Facility will last until 2031.

- September 2022 - Smarter Sorting start-up teams up with Republic Services, Inc. to enter the waste management market and increase the sustainability of its products. The waste is sorted correctly and classified based on its category using a database. Consequently, the time and money required for further waste management are reduced.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Volumes Of Waste to boost the market

- 5.1.2 Rising Adoption of Smart Cities to flourish the market

- 5.2 Market Challenges

- 5.2.1 High Costs of Implementation

- 5.3 Impact of Covid-19 on overall global smart waste management market

6 Technology Snapshot

- 6.1 Technology Overview

- 6.2 Smart Waste Management Stages

- 6.2.1 Smart Collection

- 6.2.2 Smart Processing

- 6.2.3 Smart Energy Recovery

- 6.2.4 Smart Disposal

7 MARKET SEGMENTATION

- 7.1 By Solution

- 7.1.1 Fleet Management

- 7.1.2 Remote Monitoring

- 7.1.3 Analytics

- 7.2 By Waste Type

- 7.2.1 Industrial Waste

- 7.2.2 Residential Waste

- 7.3 Geography

- 7.3.1 North America

- 7.3.1.1 United States

- 7.3.1.2 Canada

- 7.3.2 Europe

- 7.3.2.1 Germany

- 7.3.2.2 UK

- 7.3.2.3 France

- 7.3.2.4 Spain

- 7.3.2.5 Italy

- 7.3.2.6 Rest of Europe

- 7.3.3 Asia Pacific

- 7.3.3.1 India

- 7.3.3.2 China

- 7.3.3.3 Australia

- 7.3.3.4 Japan

- 7.3.3.5 Rest of Asia-Pacific

- 7.3.4 Rest of the World

- 7.3.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Suez Environmental Services

- 8.1.2 Veolia Environmental Services

- 8.1.3 Enevo

- 8.1.4 Smartbin (OnePlus Systems Inc.)

- 8.1.5 Bigbelly Inc.

- 8.1.6 Covanta Holding Corporation

- 8.1.7 Evoeco

- 8.1.8 Pepperl+Fuchs GmbH

- 8.1.9 IBM Corporation

- 8.1.10 BIN-e

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

智慧廢棄物管理全球市場 2024-2028

智慧廢棄物管理全球市場 2024-2028 智慧廢棄物管理市場 - 全球產業規模、佔有率、趨勢、機會和預測細分方法,按處置方法、按地區、按競爭2018-2028。

智慧廢棄物管理市場 - 全球產業規模、佔有率、趨勢、機會和預測細分方法,按處置方法、按地區、按競爭2018-2028。 2023-2030 年全球智慧廢棄物管理市場規模研究與預測(依廢棄物類型、方法、來源和區域分析)

2023-2030 年全球智慧廢棄物管理市場規模研究與預測(依廢棄物類型、方法、來源和區域分析) 智慧廢物管理市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會及預測

智慧廢物管理市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會及預測 數位智慧廢棄物管理解決方案的全球市場:2023年

數位智慧廢棄物管理解決方案的全球市場:2023年 智慧廢棄物管理市場:按服務、解決方案和應用分類 - 2023-2030 年全球預測

智慧廢棄物管理市場:按服務、解決方案和應用分類 - 2023-2030 年全球預測 數位、智慧廢棄物管理解決方案的全球市場:考察與預測 (2029年)

數位、智慧廢棄物管理解決方案的全球市場:考察與預測 (2029年) 智能廢物管理 (SWM) 支持技術的進步

智能廢物管理 (SWM) 支持技術的進步 智慧廢棄物管理系統的全球市場

智慧廢棄物管理系統的全球市場