|

市場調查報告書

商品編碼

1444675

3D 列印材料 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 年 - 2029 年)3D Printing Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

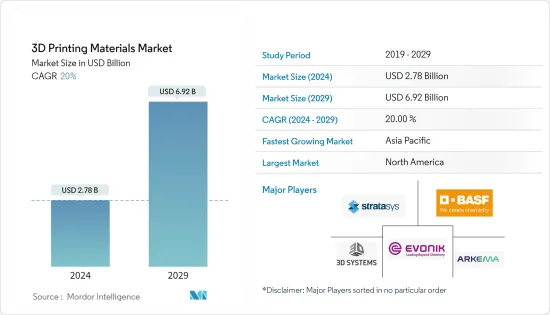

2024年3D列印材料市場規模預計為27.8億美元,預計到2029年將達到69.2億美元,在預測期內(2024-2029年)CAGR為20%。

隨著COVID-19大流行的爆發,3D列印材料市場因供應鏈中斷而遭受損失,導致多個專案延遲。此外,各國資金流動中斷和嚴格封鎖,導致生產線工人缺勤率上升,對市場產生了不利影響。然而,由於汽車產業需求增加,市場在2021年出現反彈。

主要亮點

- 推動市場成長的主要因素是製造應用需求的激增、與3D列印相關的大規模客製化以及汽車應用需求的激增。

- 另一方面,高昂的設備和材料成本以及有限的材料供應可能會阻礙市場的成長。

- 石墨烯等新材料的引入開啟了新的應用,而在家庭列印中採用3D列印技術有望為3D列印材料市場創造新的機會。

3D列印材料市場趨勢

增加在汽車產業的應用

- 3D列印材料廣泛應用於汽車產業來製造用於測試的比例模型。它們也用於製造波紋管、前保險桿、空調管道、懸吊叉骨、儀表板介面、交流發電機安裝支架、電池蓋等零件。汽車OEM製造商正在使用 3D 列印材料進行快速原型製作。

- 由於3D列印製程具有成本低、製造時間短、材料浪費少等優點,汽車製造商正在轉向這種製程。奧迪、勞斯萊斯、保時捷、Hackrod 等世界上一些最大的汽車製造商正在使用這些材料來製造備用零件和金屬原型。

- 中國汽車製造業規模全球第一。根據中國汽車工業協會統計,2023年3月,汽車產銷量分別為258.4萬輛和245.1萬輛,環比分別成長27.2%和24%,環比成長24%。年比分別成長15.3%和9.7%。

- 根據中國汽車工業協會統計,2023年1-3月,乘用車產銷分別完成526.2萬輛和513.8萬輛,年比分別成長4.3%和7.3% -依年計算。同樣,商用車產銷分別完成94.8萬輛和93.8萬輛,較去年同期成長3.9%和2.9%。

- 根據國際汽車製造商組織(OICA)的數據,2022年全球乘用車總產量為61,598,650輛; 2021 年為 57,054,295 套。由於多種因素,例如預測期內私人出行需求的增加以及電動車的指數成長,預計對車輛的需求將增加。

- 由於上述因素,汽車產業對3D列印材料的需求預計將成長。

亞太地區預計將以最快的速度成長

- 亞太地區是全球成長最快的經濟體之一,其中中國是全球成長最快的國家之一,由於人口、生活水準和人均收入的不斷成長,幾乎所有最終用戶產業都在成長。

- 該地區由多個汽車產業產量顯著的國家組成。此外,電動車的出現預計將進一步為3D列印材料市場提供實質成長機會。

- 到 2022 年,印度、印尼、馬來西亞和越南等幾個國家的汽車產量預計將大幅成長。例如,根據國際汽車製造商組織(OICA)的數據,2022年,印度和印尼的汽車總產量分別為5,456,857輛和1,470,146輛,較去年同期成長24%和31%。年。

- 2022年9月20日,財政部、工業及資訊化部、國稅局聯合宣布,2023年1月至12月新能源汽車購置2023年免徵車輛購置稅。這支持了中國新型電動車的需求和銷售。

- 此外,3D 列印中的逐層沉積製程可將感測器、天線和其他功能性電子產品直接列印到塑膠零件、金屬表面、玻璃面板和陶瓷材料上。

- 中國資訊通訊研究院的報告顯示,2022年前兩個月,電子製造業保持穩定成長。 2022年1-2月主要電子製造業增加價值年增12.7%;然而,同期整體工業成長率為7.5%。

- 中國是新技術和建築創新材料成長最快的市場之一。隨著中國作為全球建築中心的主導地位,3D列印在家庭列印領域的加速發展可能會徹底改變中國傳統的建築產業,其應用範圍從住宅建築到紀念碑。該國成功地 3D 列印房屋和其他大型結構,這使得其他每個國家都開始研究 3D 列印在建築中的可能性。

- 建築領域的 3D 列印存在一些限制,例如建築開發商缺乏信心以及缺乏使用該技術的適當法規。然而,隨著對新技術及其優勢的認知不斷增強,組織和個人擴大考慮節省成本的替代方案。這反過來又推動了該國3D列印材料市場的需求。

- 由於上述所有因素,亞太地區對 3D 列印材料的需求預計將推動所研究的市場。

3D列印材料行業概況

3D列印材料市場趨於整合,少數廠商佔據市場主要佔有率。 3D 列印材料市場的主要參與者(排名不分先後)包括 Stratasys、BASF SE、Evonik Industries AG、Arkema 和 3D Systems Inc. 等。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場動態

- 促進要素

- 在製造應用中的使用不斷成長

- 與 3D 列印相關的大規模客製化

- 汽車應用需求激增

- 限制

- 設備及材料成本高

- 有限類型材料的可用性

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者的議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第 5 章:市場區隔(市場價值規模)

- 材料種類

- 塑膠

- 丙烯腈丁二烯苯乙烯 (ABS)

- 聚乳酸 (PLA)

- 尼龍

- 聚醯胺

- 聚碳酸酯

- 其他塑膠

- 陶瓷

- 金屬

- 其他材料類型

- 塑膠

- 形式

- 粉末

- 燈絲

- 液體

- 最終用戶產業

- 汽車

- 醫療的

- 航太和國防

- 消費性電子產品

- 其他最終用戶產業

- 地理

- 亞太

- 中國

- 印度

- 日本

- 韓國

- 新加坡

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 亞太

第 6 章:競爭格局

- 併購、合資、合作與協議

- 市佔率(%)**/排名分析

- 領先企業採取的策略

- 公司簡介

- 3D Systems, Inc.

- Arkema

- BASF SE

- CRP TECHNOLOGY Srl

- CRS Holdings, LLC

- ENVISIONTEC US LLC

- EOS

- Evonik Industries AG

- General Electric

- Henkel AG & Co. KGaA

- Hoganas AB

- Materialise

- Sandvik AB

- Solvay

- Stratasys

第 7 章:市場機會與未來趨勢

- 石墨烯等新材料的引入開啟了新的應用

- 3D列印技術在家庭列印的應用

The 3D Printing Materials Market size is estimated at USD 2.78 billion in 2024, and is expected to reach USD 6.92 billion by 2029, growing at a CAGR of 20% during the forecast period (2024-2029).

With the outbreak of the COVID-19 pandemic, the 3D printing materials market suffered due to the disruption in the supply chain, resulting in delays in several projects. Moreover, disrupted financial flows and strict lockdowns in various countries, resulting in growing absenteeism among production line workers, affected the market adversely. However, the market rebounded in 2021 due to increased demand from the automotive industry.

Key Highlights

- The major factors driving the market growth are the surge in demand for manufacturing applications, mass customization associated with 3D printing, and the surge in demand for automotive applications.

- On the flip side, high equipment and material costs and limited materials availability will likely hinder the market's growth.

- Introducing new materials, like graphene, opens up new applications, and adopting 3D printing technology in home printing is expected to create new opportunities for the 3D printing materials market.

3D Printing Materials Market Trends

Increasing Applications in the Automotive Industry

- 3D printing materials are extensively used in the automotive industry to manufacture scaled models for testing. They are also used for components, such as bellows, front bumper, air conditioning ducting, suspension wishbone, dashboard interface, alternator mounting bracket, battery cover, etc. Automotive OEM manufacturers are using 3D printing materials for rapid prototyping.

- Due to the advantages of the 3D printing process, such as low cost, less manufacturing time, reduced material wastage, etc., automotive manufacturers are moving toward this process. Some of the largest automotive manufacturers in the world, such as AUDI, Rolls Royce, Porsche, Hackrod, and many others, are using these materials for manufacturing spare parts and metal prototypes.

- The Chinese automotive manufacturing industry is the largest in the world. According to the China Association of Automobile Manufacturers (CAAM), In March 2023, the production and sales of automobiles accounted for 2.584 million and 2.451 million units, respectively, with an increase of 27.2% and 24% respectively on the month every month and an increase of 15.3% and 9.7% respectively on a year-on-year basis.

- According to the China Association of Automobile Manufacturers (CAAM), from January to March of 2023, passenger cars production and sales accounted for 5.262 million and 5.138 million units, respectively, with an increase of 4.3% and 7.3%, respectively, on a year-on-year basis. Similarly, commercial vehicle production and sales accounted for 948000 and 938000 units, respectively, with an increase of 3.9% and 2.9% year-on-year.

- According to the International Organization of Motor Vehicle Manufacturers(OICA), the world's total passenger car production in 2022 was 61,598,650; in 2021, it was 57,054,295 units. The demand for vehicles is expected to rise due to several factors, such as increased demand for private mobility and exponential growth in electric vehicles during the forecast period.

- The demand for 3D printing materials in the automotive industry is expected to grow due to the above factors.

Asia-Pacific is Expected to Grow at a Fastest Rate

- Asia-Pacific is among the fastest-growing economies globally, comprising China as one of the fastest-growing countries globally, and almost all the end-user industries have been growing due to the rising population, living standards, and per capita income.

- The region comprises several countries with noteworthy production in the automotive sector. Moreover, the emergence of electric vehicles is expected to further provide substantial growth opportunities in the 3D printing materials market.

- In 2022, several countries, such as India, Indonesia, Malaysia, and Vietnam, were expected to grow tremendously in automotive production. For instance, according to the International Organization of Motor Vehicle Manufacturers (OICA), in 2022, the total production of motor vehicles in India and Indonesia stood at 5,456,857 and 1,470,146 units, respectively, showing growth of 24% and 31% compared to the previous year.

- On September 20, 2022, the Ministry of Finance (MOF), the Ministry of Industry and Information Technology (MIIT), and the State Taxation Administration (STA) jointly announced that the purchase of new energy vehicles (NEVs) from January 2023 to December 2023 would be exempt from the vehicle purchase tax. This supports the demand for and sales of new electric vehicles in China.

- Furthermore, the layer-by-layer deposition process in 3D printing allows sensors, antennas, and other functional electronics to be printed directly onto plastic components, metal surfaces, glass panels, and ceramic materials.

- According to a report by the China Academy of Information and Communications Technology, during the first two months of 2022, the electronics manufacturing industry maintained a steady expansion. The added value of major electronics manufacturers from January to February 2022 increased by 12.7% yearly; however, overall industrial growth stood at 7.5% during the same period.

- China is among the fastest-growing markets regarding new technologies and using innovative materials for construction. With China's dominating role as a global construction center, the accelerated development of 3D printing in the home printing sector is likely to revolutionize the traditional construction industry in the country, with applications ranging from residential buildings to monuments. The country managed to 3D print homes and other large-scale structures, making every other country look into the possibilities of 3D printing in construction.

- There are a few limitations to 3D printing in the construction sector, such as a lack of confidence from building developers and the absence of proper regulations for using this technology. However, with increasing awareness of new technologies and their advantages, organizations, and individuals are increasingly considering cost-saving alternatives. This, in turn, is driving demand in the 3D printing materials market in the country.

- Owing to all the abovementioned factors, the demand for 3D printing materials in Asia-Pacific is expected to drive the market studied.

3D Printing Materials Industry Overview

The 3D printing materials market is consolidated, with few players holding the major share in the market. Key players in the 3D printing materials market (not in any particular order) include Stratasys, BASF SE, Evonik Industries AG, Arkema, and 3D Systems Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage in Manufacturing Applications

- 4.1.2 Mass Customization Associated with 3D Printing

- 4.1.3 Surge in Demand in Automotive Application

- 4.2 Restraints

- 4.2.1 High Equipment and Material Cost

- 4.2.2 Availability of Limited Types of Materials

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Material Type

- 5.1.1 Plastics

- 5.1.1.1 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.1.2 Polylactic Acid (PLA)

- 5.1.1.3 Nylon

- 5.1.1.4 Polyamide

- 5.1.1.5 Polycarbonates

- 5.1.1.6 Other Plastics

- 5.1.2 Ceramics

- 5.1.3 Metals

- 5.1.4 Other Material Types

- 5.1.1 Plastics

- 5.2 Form

- 5.2.1 Powder

- 5.2.2 Filament

- 5.2.3 Liquid

- 5.3 End-user Industry

- 5.3.1 Automotive

- 5.3.2 Medical

- 5.3.3 Aerospace and Defense

- 5.3.4 Consumer Electronics

- 5.3.5 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Singapore

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3D Systems, Inc.

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 CRP TECHNOLOGY S.r.l.

- 6.4.5 CRS Holdings, LLC

- 6.4.6 ENVISIONTEC US LLC

- 6.4.7 EOS

- 6.4.8 Evonik Industries AG

- 6.4.9 General Electric

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Hoganas AB

- 6.4.12 Materialise

- 6.4.13 Sandvik AB

- 6.4.14 Solvay

- 6.4.15 Stratasys

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Introduction of New Materials, like Graphene Opens Up New Applications

- 7.2 Adoption of 3D Printing Technology in Home Printing

全球 3D 列印材料市場(按類型、幾何形狀、應用、技術、最終用途行業和地區分類)- 預測至 2030 年

全球 3D 列印材料市場(按類型、幾何形狀、應用、技術、最終用途行業和地區分類)- 預測至 2030 年 3D 列印材料市場(按材料成分、材料形式、材料等級、最終用途產業和應用)—全球預測,2025-2032 年3D列印陶瓷市場(按列印技術、材料類型、粉末形式、應用和最終用途行業)—2025-2032年全球預測

3D 列印材料市場(按材料成分、材料形式、材料等級、最終用途產業和應用)—全球預測,2025-2032 年3D列印陶瓷市場(按列印技術、材料類型、粉末形式、應用和最終用途行業)—2025-2032年全球預測 2025年生物相容性3D列印材料全球市場報告3D 列印塑膠市場(按塑膠類型、形狀、列印技術、應用、最終用戶產業和分銷管道)—2025-2030 年全球預測3D 列印高性能塑膠市場(按材料類型、外形規格、列印技術、應用和最終用途行業)—全球預測,2025-2030 年

2025年生物相容性3D列印材料全球市場報告3D 列印塑膠市場(按塑膠類型、形狀、列印技術、應用、最終用戶產業和分銷管道)—2025-2030 年全球預測3D 列印高性能塑膠市場(按材料類型、外形規格、列印技術、應用和最終用途行業)—全球預測,2025-2030 年 全球 3D 列印陶瓷市場(按陶瓷類型、形態、最終用途行業和地區分類)- 2030 年預測

全球 3D 列印陶瓷市場(按陶瓷類型、形態、最終用途行業和地區分類)- 2030 年預測 PET 長絲 3D 列印材料市場 - 預測至 2025 年至 2030 年3D列印塑膠市場:2025-2030年預測全球 3D 列印陶瓷市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測

PET 長絲 3D 列印材料市場 - 預測至 2025 年至 2030 年3D列印塑膠市場:2025-2030年預測全球 3D 列印陶瓷市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測