|

市場調查報告書

商品編碼

1437881

包裝黏劑:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Packaging Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

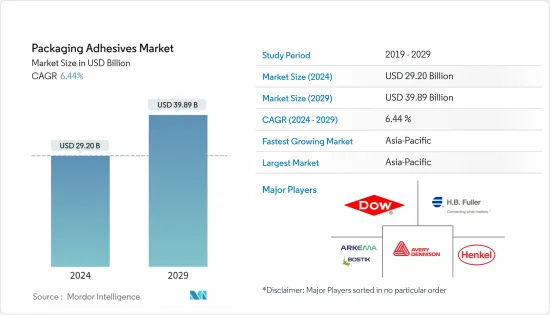

包裝黏劑市場規模預計到 2024 年為 292 億美元,預計到 2029 年將達到 398.9 億美元,預測期內(2024-2029 年)複合年成長率為 6.44%。

2020年市場受到COVID-19感染疾病的輕微影響。 COVID-19感染疾病限制了外食,促使家庭做飯的數量增加。結果,果汁、水、無酒精飲品和酒精飲料產值的大幅下降幾乎被麵粉、乳製品、保健食品、即食食品和即食食品的增加所抵消。

主要亮點

- 推動所研究市場成長的因素包括食品和飲料產業需求的增加、食品安全意識的提高以及污染風險的避免。

- 另一方面,法規對製造黏劑的各種原料的影響可能會阻礙市場成長。

- 然而,電子商務的快速成長將為市場進一步成長提供機會。

- 亞太地區在市場中佔據最高佔有率,並且可能在預測期內繼續主導市場。

包裝黏劑市場趨勢

軟包裝應用實現最高成長率

- 在消費者偏好轉向新的有吸引力的包裝、易用性、永續性和認真的環保理念的推動下,軟質包裝正在以驚人的速度成長。

- 用於軟包裝的貼合黏劑有多種技術、黏度和固態濃度可供選擇。常用的貼合黏劑有四種基本類別。這些是水基、溶劑基、反應性 100%固體(無溶劑)液體和熱熔膠。

- 軟包裝中使用的溶劑型黏劑一般為雙組份聚氨酯貼合黏劑。這些設計用於乾層壓工藝。

- 軟包裝也是VAE黏劑最重要的應用類型。另一個大類是層壓應用,因為它具有彈性、防潮性和出色的基材黏合力。

- 由於人口成長,美國、中國和印度等國家對食品的需求不斷增加,促使全球對軟包裝的需求增加。

- 根據軟包裝協會(FPA)統計,截至年終,整個美國軟包裝產業的年銷售額超過356億美元。軟包裝產業包括零售和商務用食品以及非食品、醫療和藥品包裝。 、工業材料、零售購物袋等美國食品工業是軟包裝的最大部分。

- 此外,包裝黏劑也用於蓋膜。蓋膜是一種軟包裝薄膜,通常由鋁箔、紙、聚酯、聚乙烯等製成,通常用於密封紙板品脫、塑膠容器和食品托盤。乳製品,如茅屋起司和優酪乳。

- 預計到 2022 年,全球食品業將產生 8.8 兆美元的收益。預計2022年至2027年該市場將以4.79%的複合年成長率成長。

- 因此,食品業需求增加和軟包裝成長等上述因素可能會增加預測期內包裝黏劑的市場需求。

亞太地區主導市場

- 目前,由於中國、日本和印度等國家的高需求,亞太地區在包裝黏劑市場中佔最高佔有率。

- 中國人均收入的不斷上升,加上國內電商巨頭的崛起,使其成為包裝黏劑消費量第一大國。

- 根據中國國家統計局統計,2020年社會消費品零售總額391,980.7億元(約2,216.6億元),黏劑的消耗來自消費品包裝和出貨活動。

- 此外,中國擁有世界上最大的食品工業。由於微波爐、零食和冷凍食品等食品行業客製化包裝的興起以及出口的增加,預計該國在預測期內將持續成長。包裝黏劑的使用預計將繼續增加。

- 此外,食品業是印度包裝黏劑的最大消費者之一。包裝黏劑的主要最終用戶產業包括藥品、個人保健產品和電器產品。這些最終用戶群體不斷成長的需求正在為市場創造巨大的成長潛力。

- 印度的包裝業也正在快速成長。它是印度經濟第五大部門,也是目前印度成長最快的部門之一。在電子商務蓬勃發展的背景下,印度包裝產業蓬勃發展,是成長最快的產業之一。

- 印度包裝研究所 (IIP) 的數據顯示,過去十年,印度的包裝消費量增加了 200%,從每人每年 4.3 公斤 (pppa) 增加到 8.6 公斤 pppa。

- 因此,由於上述因素,亞太地區很可能在預測期內主導調查市場。

包裝黏劑產業概況

包裝黏劑市場較為分散,因為沒有主要參與者佔據全球市場的重要佔有率。全球公司都專注於研發和協作開發新技術,以保持其在市場中的地位和立足點。該市場的主要企業包括漢高股份公司 (Henkel AG &Co. KGaA)、HB Fuller、陶氏化學 (Dow)、阿科瑪 (Bostik) 和艾利丹尼森公司 (Avery Dennison Corporation)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 食品和飲料行業需求不斷成長

- 提高食品安全意識

- 抑制因素

- 嚴格的政府法規

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔

- 依技術

- 水性的

- 溶劑型

- 熱熔膠

- 依用途

- 軟包裝

- 折疊盒和紙箱

- 密封

- 標籤和膠帶

- 其他用途

- 依地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場排名分析

- 主要企業採取的策略

- 公司簡介

- 3M

- Arkema Group(Bostik)

- AVERY DENNISON CORPORATION

- Ashland

- Dow

- Henkel AG &Co. KGaA

- HB Fuller Company

- Jowat SE

- Paramelt RMC BV

- Wacker Chemie AG

第7章市場機會與未來趨勢

- 電子商務產業快速成長

The Packaging Adhesives Market size is estimated at USD 29.20 billion in 2024, and is expected to reach USD 39.89 billion by 2029, growing at a CAGR of 6.44% during the forecast period (2024-2029).

The market was marginally impacted by COVID-19 in 2020. The COVID-19 pandemic limited dining out and led to increases in home cooking. With that, significant drops in the production values of juices, water, soft drinks, and alcoholic beverages were nearly offset by growth in wheat flour, dairy, health foods, and convenience or ready-to-eat foods.

Key Highlights

- The factors driving the growth of the market studied are the growing demand from the food and beverage industry, increasing awareness about food safety , and avoiding risks of contamination.

- On the flip side, the impact of regulations on various raw materials to be used for manufacturing adhesives may hinder the market's growth.

- However, the rapid growth in e-commerce will further provide opportunities for the market to grow.

- Asia-Pacific accounted for the highest share of the market, and it is likely to continue dominating the market during the forecast period.

Packaging Adhesives Market Trends

Flexible Packaging Application to Witness the Highest Growth Rate

- Flexible packaging is growing at an impressive rate, driven by consumer preferences shifting toward new attractive packages, ease of use, sustainability, and conscientious environmental ideals.

- Laminating adhesives for flexible packaging are available in various technologies, viscosities, and solids concentrations. There are four basic categories of laminating adhesives that are commonly used. These are waterborne, solvent-based, reactive 100% solid (solventless) liquid, and hot melt.

- Solvent-based adhesives used in flexible packaging are generally two-component polyurethane laminating adhesives. These are designed for use in the dry lamination process.

- Flexible packaging is also the most significant application type for VAE adhesives. Another large category is laminating applications due to their flexibility, moisture resistance, and superior substrate adhesion.

- With the growing population in countries such as the United States, China, and India, the requirement for food is increasing, thus resulting in increased demand for flexible packaging worldwide.

- According to the Flexible Packaging Association (FPA), the total US flexible packaging industry registered more than USD 35.6 billion in annual sales by the end of 2020. The flexible packaging industry includes packaging for retail and institutional food and non-food, medical and pharmaceutical, industrial materials, and retail shopping bags, among others. The US food industry is the largest segment for flexible packaging.

- Furthermore, packaging adhesives are also used in lidding films, which are a type of flexible packaging film commonly made by using foils, paper, polyester, polyethylene, and others generally used to seal paperboard pints, plastic containers, and trays for food items, including dairy products such as cottage cheese, sour cream, and others.

- The food industry worldwide is estimated to generate a revenue of USD 8.8 trillion in 2022. The market is expected to register a CAGR of 4.79% during 2022-2027.

- Hence, the factors above, such as increasing demand from the food industry and growing flexible packaging, will likely boost the market demand for packaging adhesives during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific currently accounts for the highest share of the packaging adhesives market, owing to the high demand from countries like China, Japan, India, etc.

- China is the leading country in the consumption of packaging adhesives due to growing per capita income, coupled with rising e-commerce giants in the country.

- According to the National Bureau of Statistics of China, the total retail sales revenue of consumer goods accounted for CNY 39,198.07 billion (~ USD 5532.31 billion) in 2020, which rose to CNY 44,082.34 billion (~ USD 6221.66 billion) in 2021, thereby enhancing the consumption of adhesives from consumer goods packaging and shipping activities.

- Additionally, China has one of the largest food industries globally. The country is expected to witness consistent growth during the forecast period due to the rise of customized packaging in the food segment, like microwave, snack, and frozen foods, and increasing exports. The use of packaging adhesives is expected to increase in the future.

- Furthermore, In India, the food industry is among the largest consumers of packaging adhesives. Some key end-user sectors of packaging adhesives include pharmaceuticals, personal care products, consumer electronics, etc. Increasing demand from these end-user segments is creating a huge market growth potential.

- In India, the packaging industry is also increasing at a rapid rate. It is the fifth-largest sector in India's economy and is currently one of the fastest and highest-growing sectors in the country. Amid the e-commerce surge, the Indian packaging industry is witnessing steep growth and is one of the strongest growing segments.

- According to the Indian Institute of Packaging (IIP), packaging consumption in India increased by 200% in the past decade, from 4.3 kgs per person per annum (pppa) to 8.6 kgs pppa.

- Hence, owing to the above-mentioned factors, Asia-Pacific is likely to dominate the market studied during the forecast period.

Packaging Adhesives Industry Overview

The packaging adhesives market is fragmented, as no major company holds a significant share of the global market. Global companies are significantly focusing on R&D and collaborations to develop new technologies to maintain their market presence and foothold. Some of the key players in the market include Henkel AG & Co. KGaA, H.B. Fuller, Dow, Arkema (Bostik), and Avery Dennison Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Food and Beverage Industry

- 4.1.2 Increasing Awareness for Food Safety

- 4.2 Restraints

- 4.2.1 Strict Government Regulations

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Technology

- 5.1.1 Water-based

- 5.1.2 Solvent-based

- 5.1.3 Hot-melt

- 5.2 By Application

- 5.2.1 Flexible Packaging

- 5.2.2 Folding Boxes and Cartons

- 5.2.3 Sealing

- 5.2.4 Labels and Tapes

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema Group (Bostik)

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 Ashland

- 6.4.5 Dow

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 H.B. Fuller Company

- 6.4.8 Jowat SE

- 6.4.9 Paramelt RMC B.V.

- 6.4.10 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rapid Growth of the E-commerce Industry

2024 年包裝黏劑全球市場報告

2024 年包裝黏劑全球市場報告 包裝黏劑市場至2030年預測:按產品類型、原料類型、包裝類型、黏劑化學、技術、應用、最終用戶和地區的全球分析

包裝黏劑市場至2030年預測:按產品類型、原料類型、包裝類型、黏劑化學、技術、應用、最終用戶和地區的全球分析 包裝黏劑市場:按技術、按應用分類 - 2024-2030 年全球預測

包裝黏劑市場:按技術、按應用分類 - 2024-2030 年全球預測 全球包裝黏合劑市場規模研究與預測,按技術(水基、溶劑基、熱熔膠等)、應用(軟包裝、折疊紙盒、盒子和箱子、標籤等)和區域分析,2023-2030年

全球包裝黏合劑市場規模研究與預測,按技術(水基、溶劑基、熱熔膠等)、應用(軟包裝、折疊紙盒、盒子和箱子、標籤等)和區域分析,2023-2030年 包裝黏合劑市場 - 按產品類型(水性黏合劑、溶劑型黏合劑、熱熔性黏合劑、反應性黏合劑、壓敏黏合劑)、按應用、按最終用途和預測, 2023年至2032年

包裝黏合劑市場 - 按產品類型(水性黏合劑、溶劑型黏合劑、熱熔性黏合劑、反應性黏合劑、壓敏黏合劑)、按應用、按最終用途和預測, 2023年至2032年 包裝黏合劑市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測

包裝黏合劑市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測 包裝黏劑市場報告:2030 年趨勢、預測與競爭分析

包裝黏劑市場報告:2030 年趨勢、預測與競爭分析 包裝黏合劑市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按技術、樹脂、按應用、地區和競爭細分

包裝黏合劑市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按技術、樹脂、按應用、地區和競爭細分 包裝黏劑市場-全球市場規模、佔有率、趨勢分析、機遇和預測報告,2019-2029

包裝黏劑市場-全球市場規模、佔有率、趨勢分析、機遇和預測報告,2019-2029 全球包裝粘合劑市場:按樹脂類型、技術、應用和地區劃分的未來預測(至 2028 年)

全球包裝粘合劑市場:按樹脂類型、技術、應用和地區劃分的未來預測(至 2028 年)