|

市場調查報告書

商品編碼

1434481

圖形薄膜:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Graphic Film - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

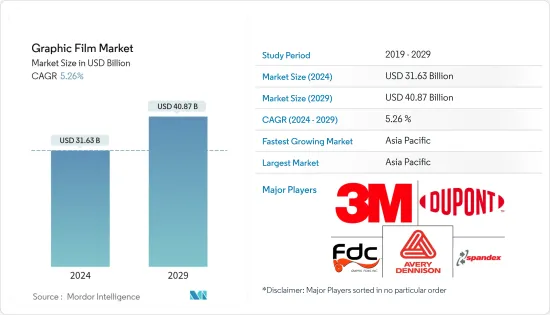

圖形薄膜市場規模預計到 2024 年為 316.3 億美元,預計到 2029 年將達到 408.7 億美元,預測期內(2024-2029 年)複合年成長率為 5.26%。

COVID-19感染疾病對所研究市場的影響阻礙了預期的整體成長率。然而,應急策略和關鍵最終用戶產業正在逐漸獲得動力,長期需求預測顯示銷售額將大幅成長。隨著需求穩步成長以及企業從疫情造成的損失中恢復過來,對受訪市場的短期預測預計,汽車行業對圖形薄膜包裝的配套需求將呈線性成長。此外,根據印度評級和研究私人有限公司 (IND-RA) 的數據,2020 年塑膠薄膜的需求增加了近 9%,但預計到 2023 年將下降至 6-6.5%。

主要亮點

- 現有的幾家市場公司生產穿孔窗膜,設計用於玻璃窗和門等平坦、透明的表面。這些薄膜通常具有穿過薄膜的連續孔圖案,以提供從一側可見的圖形。

- 窗膜基本上是一種薄層壓板,帶有粘合劑內襯,可塗在窗戶的內部或外部。它們幾乎可以切割成任何設計,並應用於門窗,用於各種用途,從企業徽標印刷和行銷到完全客製化的牆壁設計。窗膜不僅可以保護隱私和免受紫外線傷害,還有助於調節室內溫度,例如公司工作空間。窗膜可以改裝到現有窗戶上,使其成為經濟且快速的選擇。

- 牆壁和窗戶圖形透過室內週邊設備計改變消費者體驗。一些辦公室使用它來最大化公司品牌、促進新產品和銷售、提高職場生產力和士氣、娛樂和通知客戶以及改善企業環境。我們正在引入圖形薄膜。

- 隨著大多數企業建築正在使用這些產品重新設計其工作空間,室內牆飾在市場上越來越受歡迎。這些牆布使用各種圖形薄膜將光滑的室內表面轉變為藝術品。此外,市場相關人員正在利用這一利潤豐厚的機會,提供可印刷薄膜、彩色膠片飾面和其他輔助產品,以提高整體收益。

- 圖文膜也用作漆面保護膜,保護車輛外飾件,降低維修成本。已開發經濟體和新興經濟體對用於車輛保護和廣告的圖形薄膜的需求不斷成長,可能會加速汽車行業的圖形薄膜成長。例如,總部位於美國的 Mactac 為想要在卡車、巴士、貨車和其他車輛上宣傳其產品和品牌的供應商推出了一種新型黏性車輛包裝。

- 該公司表示,一種新的專有黏劑使包裝更容易黏貼。這款易剝離黏合劑的背面是一層光亮的白色軟質壓延 PVC 薄膜,非常適合色彩再現,還有一層聚乙烯塗層襯裡,可增加印刷過程中的穩定性。

圖形膜市場趨勢

汽車產業預計將大幅成長

- 在汽車產業,圖形薄膜應用包括車輛包裝、圖形切割和切割。相比之下,在切割乙烯基時,車輛貼膜是一大張黏合乙烯基,本身沒有特定的形狀。這些包裹物覆蓋了車輛的整個面板。出於保護、廣告目的以及使車輛看起來更好的需要,汽車上大規模採用圖形薄膜和包裝材料。根據美國戶外廣告協會 (OAAA) 的數據,單一車輛包裝每天可產生 30,000 到 80,000廣告曝光率。此外,根據豐業銀行的數據,全球汽車銷售量從 2020 年的約 6,380 萬輛增至 2021 年的約 6,670 萬輛。

- 將圖形薄膜貼在汽車上是比其他形式的廣告更便宜的廣告方式。根據美國戶外廣告協會的數據,車輛包裝的成本為每 1,000 次廣告曝光率(CPM) 0.15 美元。相比之下,廣告看板每 PCM 的成本為 1.78 美元,廣播每 CPM 的成本為 5.92 美元,Prime TV Spot 的每 CPM 的成本為 20.54 美元。因此,廣告成本的降低將推動整個汽車產業研究市場的成長。

- 3M、Avery Dennison 和 Lintec 等許多公司正在創新並為市場上的主要汽車製造商供貨。例如,Spandex推出了3M Wrap Film Series 2080,這是一種改進的變色車輛包裹材料。一旦應用,薄膜可以輕鬆去除,留下光滑的表面,並確保保護層上的刮痕不會轉移到薄膜本身。

- 反光膜的進一步發展可提供額外的安全性、可見度和特殊效果標記,從而提高了相關車隊的夜間能見度。因此,此類電影必須符合聯邦道路安全準則。同樣,反光帶作為壓感形式被引入市場,採用高品質微棱鏡反光材料,增強夜間辨識能力。

- 就車窗貼膜和貼膜而言,它們本質上具有廣泛的用途,從個人隱私/安全到車輛廣告。例如,3M 汽車窗膜有多種色調可供選擇,可限制 95% 的可見光,以確保乘客的隱私。該公司的 Obsidian 系列、FX-Hp 和陶瓷 IR 膜是其為汽車應用提供的一些窗膜。

亞太地區預計將佔據最大市場佔有率

- 汽車、工業和電子商務等終端用戶行業對圖形薄膜的需求不斷成長,正在積極推動該地區的市場成長。預計中國將在亞太地區佔據重要佔有率。這種成長可歸因於先進的技術發展、高可支配收入、卓越的架構和汽車產業場景。

- 中國汽車工業快速發展,中國在全球汽車市場中扮演越來越重要的角色。政府認為汽車工業,包括汽車零件產業,是主導產業之一。

- 此外,中國政府預計2025年汽車產量將達3,500萬輛。 IBEF預計,到2026年,印度汽車工業產值預計將達到2,514億美元至2,828億美元。因此,由於汽車工業的成長,該地區的市場範圍不斷擴大。此外,消費者對改變車輛顏色的興趣日益濃厚,預計將推動該地區對汽車保鮮膜的需求。

- 中國廣告業在過去幾十年經歷了快速發展。外國品牌和廣告在當今中國人的生活中司空見慣。此外,中國企業迅速採用國際廣告技術和做法,對國內廣告市場產生了重大影響。

- 此外,印度是該地區成長最快的建築市場之一,預計到 2030 年建築業支出將達到約 13 兆美元。該國人口正在迅速成長,一次性住宅的增加正在創造對重大住宅計劃的需求。收入和都市化。在預測期內,上述所有最終用戶產業的成長預計將為市場創造機會。

圖形膠片產業概述

圖形薄膜市場分散,同時競爭激烈。市場主要企業採取的主要策略是產品創新、併購,以擴大影響力並維持市場競爭力。市場主要企業包括3M公司、EI杜邦公司、FDC Graphic Films Inc.、艾利丹尼森公司、Spandex AG等。

- 2021 年 2 月 - Schweitzer Mauduit International, Inc. 宣布計劃收購英國Scapa Group Plc,這是一家面向醫療保健和工業市場的一流創新、設計和製造解決方案供應商。該公司透過提供用於建築、運輸、消費和工業終端市場的強大且盈利的工業圖形薄膜膠帶來補充其現有業務。

- 2021 年 1 月 - Drytac 推出全新 Polar Choice 系列單體 PVC 薄膜。其中包括 Polar Choice White 下的 6 種產品,包括 Gloss PB(一種永久灰色黏劑)、Matte RB(一種可移除灰色黏劑)和 Gloss P(一種永久透明黏劑)。 Polar Choice Clear 提供 Gloss P(永久透明黏劑)和 Gloss R(可移除透明黏劑),以及 Polar Choice Air White Gloss PB(永久灰色黏劑)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- COVID-19 市場影響評估

第5章市場動態

- 市場促進因素

- 建築業的發展與生活水準的提高

- 包裝廣告的需求成長

- 市場限制因素

- 原物料價格波動

第 6 章 技術概覽

- 薄膜類型

- 不透明薄膜

- 透明膜

- 半透明薄膜

- 反光膜

- 印刷技術

- 彈性凸版印刷

- 平版膠印

- 凹版印刷

- 數位的

第7章市場區隔

- 聚合物

- 聚丙烯(PP)

- 聚乙烯(PE)

- 聚氯乙烯(PVC)

- 其他聚合物

- 最終用戶產業

- 車

- 促銷/廣告

- 公共公共設施

- 其他最終用戶產業(航空業和電子商務)

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

第8章 競爭形勢

- 公司簡介

- 3M Company

- EI Du Pont De Nemours and Company

- FDC Graphic Films Inc.

- Avery Dennison Corporation

- Spandex AG

- Graphic Image Films Ltd

- Hexis SA

- Drytac Corporation

- Orafol Europe GMBH

- Arlon Graphics LLC(FLEXcon Company Inc.)

- Lintec Corporation

- LG Hausys

- Cosmos Films Ltd

- Taghleef Industries Inc.

- Ritrama SpA

- ACCO Brands Corporation

- Innovia Films(CCL Industries Inc.)

- Contravision

- Schweitzer-Mauduit International Inc.

- Ultraflex Systems Inc.

第9章投資分析

第10章市場的未來

The Graphic Film Market size is estimated at USD 31.63 billion in 2024, and is expected to reach USD 40.87 billion by 2029, growing at a CAGR of 5.26% during the forecast period (2024-2029).

The impact of the COVID-19 pandemic on the market studied is hindering the overall anticipated growth rates. However, with contingency strategies and major end-user industries gaining gradual momentum, the long-term demand forecast demonstrates a significant surge in sales. With demand steadily growing and companies recuperating from the losses incurred due to the pandemic, the ancillary demand for graphic film wraps used in the automobile sector is anticipated to rise linearly in the short-term forecast of the market studied. Furthermore, according to Indian Rating and Research Private Limited (IND-RA), the plastic film demand rose close to 9% in 2020 and is expected to fall to 6-6.5% by 2023.

Key Highlights

- Several market incumbents are manufacturing perforated window films that are designed for use on flat, transparent surfaces, such as glass windows or doors. These films are usually equipped with a continuous hole pattern perforated into the film to provide graphics visible from one side.

- Window film is essentially a thin laminate with an adhesive backing that is added to either the inside or outside of a window. It can be cut into almost any design and applied to windows or doors for various purposes - from printing corporate logos and marketing to designing fully customized walls. Window films offer privacy and protection against UV rays and even help manage thermoregulation of interiors, like corporate workspaces. Window films can be retrofitted to existing windows, which makes them an economical and speedy option.

- Wall and window graphics transform consumer experiences with interior and exterior designs. Several offices are incorporating graphic films to maximize their branding, promote new products and sales, improve workplace productivity and morale, entertain and inform customers, and enhance the corporate environment.

- Indoor wall wraps are gaining market traction, as most corporate buildings are redesigning their workspaces with these products. These wall wraps turn smooth indoor surfaces into artworks with a wide array of graphic films. Further, market players are capitalizing on this lucrative opportunity by offering printable films and finishes to colored films and other ancillary products, thus boosting their overall revenues.

- Graphic films are also used as paint protection films to protect the exterior components of vehicles for lowering the maintenance cost. The rising demand for graphic films to safeguard vehicles and for advertising in developed and developing economies may augment graphic films' growth in the automotive sector. For instance, US-based Mactac launched a new adhesive vehicle wrap for vendors looking to advertise their products and brands on trucks, buses, vans, and other vehicles.

- As per the company, the new proprietary adhesive enhances the ease of application of wraps. This easily-removable adhesive backs a gloss white soft calendered PVC film, which is highly suitable for color reproduction, and a poly-coated liner for stability during printing.

Graphic Film Market Trends

Automotive Sector is Expected to Witness Significant Growth

- In the automotive industry, graphic film applications include vehicle wraps, cut graphics, and cut deals. In contrast, to cut vinyl, vehicle wraps are large sheets of self-adhesive vinyl without a particular shape of their own. These wraps cover across entire panels of the vehicle. The large-scale adoption of graphic films or wraps in vehicles has been driven by the need for protective and advertisement purposes and to provide a better look at the vehicles. Also, per the Outdoor Advertising Association of America (OAAA), one vehicle wrap can generate between 30,000 and 80,000 impressions daily. Moreover, according to Scotiabank, worldwide car sales grew to around 66.7 million automobiles in 2021, up from approximately 63.8 million units in 2020.

- Putting graphic film wraps on an automobile is a cheaper means of advertising than other forms of advertisement. According to the Outdoor Advertising Association of America, the vehicle wraps cost USD 0.15 per cost of thousand impressions (CPM). In contrast, the billboards cost USD 1.78 per PCM, radios cost USD 5.92 per CPM, and prime TV spots cost USD 20.54 per CPM. Thus, the lower cost of advertisement drives the growth of the market studied across the automotive sector.

- Many companies, such as 3M, Avery Dennison, and Lintec, among others, are innovating and offering products to the major automotive players in the market. For instance, Spandex launched the 3M Wrap Film Series 2080, an improved color-change vehicle wrap material. The film can be easily removed after the application to reveal a smooth finish, and any scratch on the protective layer will not be transferred to the film itself.

- Further developments in the form of Reflective Films, which provide added safety or visibility and special effect markings, are enhancing the night visibility of the concerned fleet. Such films are therefore required to meet the federal guidelines for road safety. Likewise, Reflective Tapes as pressure-sensitive formats have been launched in the market featuring high-quality, micro-prismatic retroreflective materials for additional night-time recognition.

- As far as window tints or films are concerned, these basically serve a wide range of purposes, from personal privacy/security to fleet advertisements. For instance, 3M Automotive Window Films are available in different tint levels to restrict 95% of visible light for privacy among passengers. Its Obsidian Series, FX-Hp, and Ceramic IR Film are some of the window films offered for automotive applications.

Asia Pacific is Expected to Account for the Largest Market Share

- Growing demand for graphic films across the end-user industries, such as automotive, industrial, and e-commerce, is driving the market growth positively in the region. China is expected to hold a prominent share in Asia-Pacific. The increase may be attributed to high technological development, high disposable income, and good architecture and automotive industrial scenarios.

- The Chinese automotive industry has been growing rapidly, and the country plays an increasingly important role in the global automotive market. The government views its automotive industry, including the auto parts sector, as one of the prominent industries.

- Moreover, the Chinese government predicts that its automobile output may reach 35 million units by 2025. According to the IBEF, the Indian automotive industry is anticipated to reach USD 251.4-282.8 billion by 2026. Hence, growth in the automotive industry is expected to create scope for the market studied in the region. Moreover, rising interest in vehicle color change among consumers is anticipated to propel the demand for automotive wrap films in the region.

- The advertising industry in China has witnessed exponential development over the past few decades. Foreign brands and advertisements have become commonplace in the lives of the Chinese population today. Moreover, Chinese companies have been quick to adopt international advertising techniques and practices to create a huge impact on the domestic advertising market.

- Further, India is one of the fastest-growing construction markets in the region, and it is expected to spend around USD 13 trillion on the construction industry by 2030. The country's rapidly expanding population is generating significant housing project demand due to the increase in disposable income and urbanization. Over the forecast period, the growth of all the above end-user industries is expected to create opportunities for the market.

Graphic Film Industry Overview

The Graphic Film Market is fragmented and, at the same time, highly competitive. Key strategies that the major players in the market adopt are product innovation, mergers, and acquisitions to extend their reach and stay competitive in the market. Some of the key players in the market include 3M Company, E.I. Du Pont De Nemours and Company, FDC Graphic Films Inc., Avery Dennison Corporation, and Spandex AG, among others.

- February 2021 - Schweitzer-Mauduit International, Inc. announced its plans to acquire UK-based Scapa Group Plc, best-in-class innovation, design, & manufacturing solutions provider for healthcare & industrial markets. The company will bring a robust and profitable set of industrial, graphic film tapes used in construction, transportation, consumer, and industrial end-markets, complementing existing business.

- January 2021 - Drytac launched a new Polar Choice range of monomeric PVC films. It includes 6 products such as Gloss PB (permanent grey adhesive), Matte RB (removable grey adhesive), and Gloss P (permanent clear adhesive) under Polar Choice White. While under Polar Choice Clear, it offers Gloss P (permanent clear adhesive) and Gloss R (removable clear adhesive), and Polar Choice Air White Gloss PB (permanent grey adhesive).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in the Construction Industry and Improvements in the Standard of Living

- 5.1.2 Growth in Demand for Wrap Advertisement

- 5.2 Market Restraints

- 5.2.1 Fluctuations in Raw Material Prices

6 TECHNOLOGY SNAPSHOT

- 6.1 Film Type

- 6.1.1 Opaque Film

- 6.1.2 Transparent Film

- 6.1.3 Translucent Film

- 6.1.4 Reflective Film

- 6.2 Printing Technology

- 6.2.1 Flexography

- 6.2.2 Offset Lithography

- 6.2.3 Rotogravure

- 6.2.4 Digital

7 MARKET SEGMENTATION

- 7.1 Polymer

- 7.1.1 Polypropylene (PP)

- 7.1.2 Polyethylene (PE)

- 7.1.3 Polyvinyl Chloride (PVC)

- 7.1.4 Other Polymers

- 7.2 End-User Industry

- 7.2.1 Automotive

- 7.2.2 Promotional & Advertisement

- 7.2.3 Institutional

- 7.2.4 Other End-User Industries (Aircraft Industry and E-commerce)

- 7.3 Geography

- 7.3.1 North America

- 7.3.2 Europe

- 7.3.3 Asia Pacific

- 7.3.4 Rest of the World

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 3M Company

- 8.1.2 E.I. Du Pont De Nemours and Company

- 8.1.3 FDC Graphic Films Inc.

- 8.1.4 Avery Dennison Corporation

- 8.1.5 Spandex AG

- 8.1.6 Graphic Image Films Ltd

- 8.1.7 Hexis S.A.

- 8.1.8 Drytac Corporation

- 8.1.9 Orafol Europe GMBH

- 8.1.10 Arlon Graphics LLC (FLEXcon Company Inc.)

- 8.1.11 Lintec Corporation

- 8.1.12 LG Hausys

- 8.1.13 Cosmos Films Ltd

- 8.1.14 Taghleef Industries Inc.

- 8.1.15 Ritrama SpA

- 8.1.16 ACCO Brands Corporation

- 8.1.17 Innovia Films (CCL Industries Inc.)

- 8.1.18 Contravision

- 8.1.19 Schweitzer-Mauduit International Inc.

- 8.1.20 Ultraflex Systems Inc.

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

背光膜市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區及競爭狀況,2020-2030 年)

背光膜市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區及競爭狀況,2020-2030 年) 2032 年圖形薄膜市場預測:按薄膜類型、聚合物類型、印刷技術、基材類型、應用、最終用戶和地區進行的全球分析2032 年圖形薄膜市場預測:按薄膜類型、特性、印刷技術、應用、最終用戶和地區進行的全球分析圖形薄膜市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品類型、薄膜類型、印刷技術、最終用戶、地區和競爭細分,2020-2030 年

2032 年圖形薄膜市場預測:按薄膜類型、聚合物類型、印刷技術、基材類型、應用、最終用戶和地區進行的全球分析2032 年圖形薄膜市場預測:按薄膜類型、特性、印刷技術、應用、最終用戶和地區進行的全球分析圖形薄膜市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品類型、薄膜類型、印刷技術、最終用戶、地區和競爭細分,2020-2030 年 圖形薄膜市場:按薄膜類型、聚合物類型和最終用戶分類 - 全球預測 2025-2030

圖形薄膜市場:按薄膜類型、聚合物類型和最終用戶分類 - 全球預測 2025-2030 全球圖形薄膜市場(2024-2028)

全球圖形薄膜市場(2024-2028) 2024-2032 年按聚合物(聚氯乙烯、聚丙烯、聚乙烯等)、薄膜類型、印刷技術、最終用途和地區分類的圖形薄膜市場報告

2024-2032 年按聚合物(聚氯乙烯、聚丙烯、聚乙烯等)、薄膜類型、印刷技術、最終用途和地區分類的圖形薄膜市場報告 2022-2032 年全球圖形薄膜市場規模研究(按聚合物、印刷技術、薄膜類型、最終用戶和區域預測)

2022-2032 年全球圖形薄膜市場規模研究(按聚合物、印刷技術、薄膜類型、最終用戶和區域預測) 圖形薄膜市場規模、佔有率和趨勢分析報告:按產品、按薄膜、按製造程序、按印刷技術、按最終用途、按地區和細分趨勢:2024-2030

圖形薄膜市場規模、佔有率和趨勢分析報告:按產品、按薄膜、按製造程序、按印刷技術、按最終用途、按地區和細分趨勢:2024-2030 亞太圖形薄膜市場:按最終用戶、按產品類型、按技術、按國家:分析和預測(2023-2033)

亞太圖形薄膜市場:按最終用戶、按產品類型、按技術、按國家:分析和預測(2023-2033)