|

市場調查報告書

商品編碼

1404100

汽車零件鋁壓鑄件-市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測Automotive Parts Aluminum Die Casting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

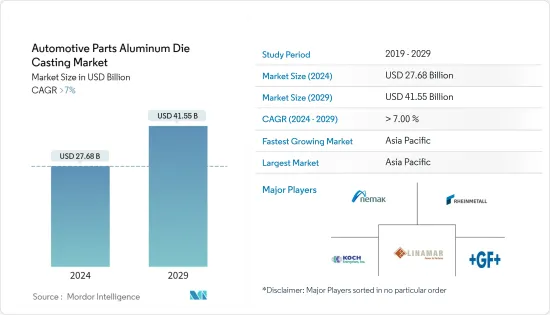

預計2024年汽車零件鋁壓鑄市場規模為276.8億美元,2029年達到415.5億美元,預計在預測期內(2024-2029年)複合年成長率將超過7%。

對輕型車輛的需求增加以及壓鑄汽車零件中鋁的使用增加等因素預計將在預測期內推動市場成長。各個地區都實施了嚴格的環境法規和 CAFE 標準,推動了壓鑄製程的採用。

對電動車和混合動力汽車不斷成長的需求也使汽車製造商開始關注在所有類型的車輛中使用鋁等輕量材料來替代較重的鋼和鐵。此外,石化燃料成本的上升和電動車普及的提高是主要的市場促進因素。在這個市場上經營的公司正致力於提高產能,以滿足不斷成長的需求。例如

主要亮點

- 2022年8月,文燦集團在中國投資10億元人民幣(1.4億美元),在安徽省六安經濟技術開發區興建新能源汽車(NEV)鋁壓鑄件生產基地。

- 2022年5月,泰米爾納德邦小型工業發展公司投資5,800萬印度盧比(約70萬美元)建立鋁高壓鑄通用設備中心。

由於各國之間的製裁和貿易爭端,以及汽車業擴大使用新鑄造技術(如3D列印),預計市場將受到鋁價波動的限制。

汽車零件鋁壓鑄件市場趨勢

鋁在汽車中的廣泛普及可能會刺激需求

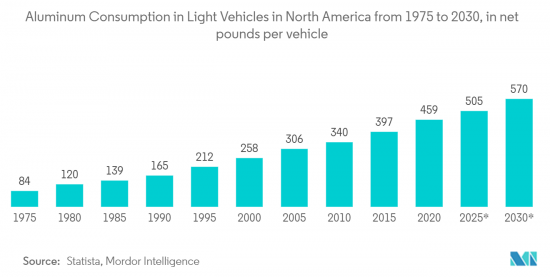

鋁是壓鑄最優選的金屬。在汽車應用中,混合動力汽車和電動車技術正在興起。例如,在北美,自 2016 年以來,每輛車的鋁含量增加了 62 磅(28 公斤),到 2020 年將達到 459 磅(208 公斤)。預計到 20230 年將達到 570 磅(258 公斤)。這主要是由轉向輕型卡車和電池電動車推動的。

此外,到 2026 年,每輛輕型卡車預計將使用 550 磅(250 公斤)的鋁。這種成長主要體現在三個主要材料應用領域:鋁車身板、鑄件和擠壓件。特斯拉的 Model S BEV 就是一個很好的例子,它在結構部件、鑄件、擠壓件和整個車身中使用了超過 800 磅(360 公斤)的鋁。

另一方面,價格上漲和與原料採購相關的風險預計將在長期預測期內阻礙市場成長。由於美國與中東和非洲其他地區之間迫在眉睫的貿易戰,近幾週基本金屬價格一直面臨壓力。候任總統對來自美國盟友(包括歐盟、墨西哥和加拿大)的鋁(10%)和鋼(25%)徵收進口關稅,預計將提高國內鋁價。

此外,印度、泰國、印尼、埃及以及其他中東和非洲國家等新興國家小客車產銷量的增加預計將在預測期內推動汽車零件鋁壓鑄件市場的發展。

亞太地區預計將出現顯著成長

預計亞太地區在預測期內將呈現最快的成長率。在亞太地區,印度、中國和日本等主要國家預計將在預測期內為市場開拓做出重大貢獻。中國是壓鑄件的主要生產國之一,小客車在該地區不斷成長的普及可能會對市場產生樂觀的影響。

例如,根據中國工業協會的數據,2022年中國汽車產量達到2702萬輛,與前一年同期比較成長3.4%,銷售汽車數量成長2.1%,達到2686萬輛。

由於亞太地區是世界主要汽車生產國之一,因此往往吸引主要市場製造商。許多製造商正在採取地理擴張和產能擴張等成長策略,以保持在該市場的競爭。例如,

- 2022年1月,一家中國零件供應商向特斯拉合作夥伴訂購了一台超級壓鑄機,顯示蔚來和小鵬汽車可能會採用它。該機器可實現整合製造,減少生產時間和成本,並滿足特斯拉的供應鏈效率目標。

在推動市場的因素以及導致市場混亂的因素中,客戶對鋁產品的強烈偏好以及鋁使用量持續增加的趨勢預計將為市場提供顯著的成長機會。

汽車零件鋁壓鑄產業概況

汽車零件鋁壓鑄市場由全球和地區知名參與企業進行整合和主導。這些公司採用新產品開拓、聯盟、合約和協議等策略來維持其市場地位。例如

- 2023 年 3 月,瑞典鋁供應商 Granges 與中國山東創新集團合作,開始生產永續鋁。此次合作旨在利用 Granges 的永續材料專業知識和山東創新集團的回收和清潔能源能力。兩家公司共同致力於滿足對環保鋁鑄造產品日益成長的需求。

該市場的主要參與者包括萊茵金屬公司、Nemak、Linmar Corporation、Koch Enterprises 和 George Fischer Limited。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 越來越重視輕量材料

- 其他

- 市場抑制因素

- 價格波動對報酬率構成持續威脅

- 其他

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 生產流程

- 壓力鑄造

- 真空壓鑄

- 擠壓鑄造

- 重力鑄造

- 應用程式類型

- 身體部位

- 引擎零件

- 傳動部件

- 電池及相關零件

- 其他使用類型

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 英國

- 法國

- 德國

- 義大利

- 俄羅斯

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太地區

- 其他中東/非洲

- 巴西

- 南非

- 阿根廷

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他國家

- 北美洲

第6章競爭形勢

- 供應商市場佔有率

- 公司簡介

- Form Technologies Inc.(Dynacast)

- Nemak

- Endurance Technologies Ltd(CN)

- Sundaram Clayton Ltd

- Shiloh Industries Inc.

- Georg Fischer Limited

- Kochi Enterprises(Gibbs Die Casting Corporation)

- Bocar Group

- Engtek Group

- Rheinmetall AG

- Rockman Industries

- Ryobi Die Casting Ltd

- Linmar Corporation

- Meridian Light weight Technologies UK Limited

- Sandhar Group

第 7 章 7. 市場機會與未來趨勢

- 提高流程自動化程度

- 電動車的普及

The Automotive Parts Aluminum Die Casting Market size is estimated at USD 27.68 billion in 2024, and is expected to reach USD 41.55 billion by 2029, growing at a CAGR of greater than 7% during the forecast period (2024-2029).

Factors such as the rising demand for lightweight vehicles and the growing utilization of aluminum in diecasting auto parts are expected to fuel the market's growth during the forecast period. Stringent environmental regulations and CAFE standards were imposed across various regions to support the adoption of the diecasting process.

In addition, increased demand for electric and hybrid vehicles turned automakers' focus to using lightweight materials like aluminum as a substitute for heavier steel and iron in all types of vehicles. Furthermore, the rising cost of fossil fuels and rising electric vehicle adoption are significant market drivers. Players operating in the market are focused on raising their production capacities to meet this rising demand. For instance,

Key Highlights

- In August 2022, WencanGroup Co., Ltd. Invested CNY 1 billion (USD 0.14 billion) in China to build a production base of aluminum diecast parts for New Energy Vehicles (NEVs) in Lu'anEconomic and Technological Development Zone, Anhui Province.

- In May 2022, Tamil Nadu Small Industries Development Corporation invested an amount of INR 5.8 crore (around USD 0.70 million) to establish a common facility center for aluminum high-pressure die casting.

The market is anticipated to be constrained by the volatility of aluminum pricing due to sanctions and trade disputes between nations and the growing use of novel casting technologies (such as 3D printing) in the automotive industry.

Automotive Parts Aluminum Die Casting Market Trends

Increasing Aluminum Penetration in Automobiles is Likely to Bolster Demand

Aluminum is the most preferred metal for die casting. Within the automotive application, hybrid and electric vehicle technologies are on the rise. Taking North America as an example, since 2016, there was an increase in terms of aluminum content of 62 lbs (28 kg) per vehicle, with 2020 reaching a total vehicle content figure of 459 lbs (208 kg). It is expected to reach 570 lbs (258 kg) by the year 20230. The shift toward the light truck and battery electric vehicles primarily drives it.

Further, it is expected that by 2026, 550 lbs (250 kg) of aluminum content per vehicle for light-duty trucks. This increase is seen primarily in three main areas of material usage: aluminum auto body sheets, castings, and extrusions. A good example of this is Tesla's Model-S BEV, which uses over 800 lbs (360 kg) of aluminum for structural components, castings, extrusions, and the whole body of the vehicle.

On the other side, rising prices and risks associated with raw material sourcing are expected to hinder market growth during the longer-term forecast period. Base metal prices are under pressure in recent weeks due to the looming trade war between the United States and the rest of the world. The imposition of tariffs on imports from the US allies (including the European Union, Mexico, and Canada) on aluminum (10%) and steel (25%) by the President-elect is expected to increase the domestic aluminum prices.

Moreover, the increasing production and sales of passenger cars in several emerging economies, such as India, Thailand, Indonesia, Egypt, and other Middle East & African countries, are anticipated to drive the automotive parts aluminum die casting market during the forecast period.

Asia-Pacific Region Anticipated to Witness Significant Growth

Asia-Pacific is expected to witness the fastest growth rate during the forecast period. In the Asia-Pacific region, major countries like India, China, and Japan are expected to contribute significantly to the development of the market over the forecast period. China is one of the major producers of die-casting parts, and the growing adoption of passenger cars in the region is likely to provide an optimistic impact on the market.

For instance, according to the China Association of Automobile Manufacturers, China's car production reached 27.02 million units in 2022, an increase of 3.4% year-on-year, while sales increased by 2.1% to 26.86 million units.

The Asia-Pacific region, being one of the world's largest manufacturers of vehicles, tends to attract major market manufacturers. Many players adopt growth strategies, such as geographic expansion and production capacity expansion, to stay competitive in this market. For instance,

- In January 2022, a Chinese part supplier ordered super die-casting machines from a Tesla partner, hinting at potential adoption by NIO and XPeng. The machines enable one-piece manufacturing, reducing production time and costs, and align with Tesla's goal of improving efficiency in its supply chain.

Amidst all the factors promoting the market and the factors that can lead to disruption in the market, the strong preference of the customers toward aluminum products and the ongoing trend of increased usage of aluminum is expected to provide a significant growth opportunity in the market.

Automotive Parts Aluminum Die Casting Industry Overview

The automotive parts aluminum die casting market is consolidated and led by globally and regionally established players. These companies adopt strategies such as new product developments, collaborations, and contracts and agreements to sustain their market positions. For instance,

- In March 2023, Granges, a Swedish aluminum supplier, joined forces with China's Shandong Innovation Group to produce sustainable aluminum. The partnership aims to leverage Granges' expertise in sustainable materials and Shandong Innovation Group's capabilities in recycling and clean energy. Together, they aim to meet the increasing demand for environmentally friendly aluminum casting products.

Some of the major players in the market include Rheinmetall AG, Nemak, Linmar Corporation, Koch Enterprises, and George Fischer Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Emphasis towards Lightweight Material

- 4.1.2 Others

- 4.2 Market Restraints

- 4.2.1 Volatility in Prices is a Constant Threat for Profit Margin

- 4.2.2 Others

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Production Process

- 5.1.1 Pressure Die Casting

- 5.1.2 Vacuum Die Casting

- 5.1.3 Squeeze Die Casting

- 5.1.4 Gravity Die Casting

- 5.2 Application Type

- 5.2.1 Body Parts

- 5.2.2 Engine Parts

- 5.2.3 Transmission Parts

- 5.2.4 Battery and Related Components

- 5.2.5 Other Application Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Italy

- 5.3.2.5 Russia

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 Brazil

- 5.3.4.2 South Africa

- 5.3.4.3 Argentina

- 5.3.4.4 Saudi Arabia

- 5.3.4.5 United Arab Emirates

- 5.3.4.6 Other Countries

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Form Technologies Inc.(Dynacast)

- 6.2.2 Nemak

- 6.2.3 Endurance Technologies Ltd (CN)

- 6.2.4 Sundaram Clayton Ltd

- 6.2.5 Shiloh Industries Inc.

- 6.2.6 Georg Fischer Limited

- 6.2.7 Kochi Enterprises (Gibbs Die Casting Corporation)

- 6.2.8 Bocar Group

- 6.2.9 Engtek Group

- 6.2.10 Rheinmetall AG

- 6.2.11 Rockman Industries

- 6.2.12 Ryobi Die Casting Ltd

- 6.2.13 Linmar Corporation

- 6.2.14 Meridian Light weight Technologies UK Limited

- 6.2.15 Sandhar Group

7 7. Market Opportunities and Future Trends

- 7.1 Increasing Process Automation

- 7.2 Growing Electric Vehicle Adoption

全球汽車金屬衝壓沖壓市場 - 規模、佔有率、趨勢分析、機會、預測(2019-2030)

全球汽車金屬衝壓沖壓市場 - 規模、佔有率、趨勢分析、機會、預測(2019-2030) 2024-2032年按生產流程(壓力壓鑄、真空壓鑄、重力壓鑄、擠壓壓鑄)、應用(車身零件、引擎零件、變速箱零件等)和地區分類的汽車零件鎂壓鑄市場報告

2024-2032年按生產流程(壓力壓鑄、真空壓鑄、重力壓鑄、擠壓壓鑄)、應用(車身零件、引擎零件、變速箱零件等)和地區分類的汽車零件鎂壓鑄市場報告 汽車金屬沖壓 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)

汽車金屬沖壓 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029) 汽車零件鎂壓鑄件:市場佔有率分析、產業趨勢、成長預測(2024-2029)

汽車零件鎂壓鑄件:市場佔有率分析、產業趨勢、成長預測(2024-2029) 汽車沖壓件市場:按技術、工藝和最終用戶分類 - 2024-2030 年全球預測

汽車沖壓件市場:按技術、工藝和最終用戶分類 - 2024-2030 年全球預測 全球汽車金屬沖壓市場 2023-2030

全球汽車金屬沖壓市場 2023-2030 2018-2028年全球汽車零件鎂壓鑄市場依生產流程、按應用、地區、競爭預測及機會細分

2018-2028年全球汽車零件鎂壓鑄市場依生產流程、按應用、地區、競爭預測及機會細分 全球汽車零件鋁壓鑄市場按生產流程、按應用類型、地區、競爭預測和機會細分,2018-2028 年

全球汽車零件鋁壓鑄市場按生產流程、按應用類型、地區、競爭預測和機會細分,2018-2028 年 汽車模具沖壓設備市場:按沖壓(冷沖壓、熱沖壓)、材料(鋁、鋼)、工藝、車輛分類 - 全球預測 2023-2030

汽車模具沖壓設備市場:按沖壓(冷沖壓、熱沖壓)、材料(鋁、鋼)、工藝、車輛分類 - 全球預測 2023-2030 汽車零部件壓鑄市場:按產品類型、按應用、按原材料、按國家、按地區 - 行業分析、市場規模、市場份額、2023-2030 年預測

汽車零部件壓鑄市場:按產品類型、按應用、按原材料、按國家、按地區 - 行業分析、市場規模、市場份額、2023-2030 年預測