|

市場調查報告書

商品編碼

1923671

智慧建築新創公司(2026):併購與投資 | 貫穿 AEC/O 生命週期的數位孿生與人工智慧新創公司StartUps in Smart Buildings 2026: M&A & Investments | Digital Twin & AI Startups across the AEC/O Lifecycle |

||||||

智慧建築新創企業生態系已達到臨界點。儘管創投成長放緩,但併購活動卻激增,光是 2025 年就發生了 98 起初創企業收購案——較 2024 年成長 75%,創下近十年來的最高年度紀錄。這種整合顯示市場已趨於成熟,成熟的商業模式正吸引策略性收購者的目光。

本報告深入探討了智慧建築業,並提供了一份電子表格,列出了 2025 年涵蓋所有融資輪次、企業投資者、併購活動、技術類別以及整個 AEC/O 生命週期的 84 家數位孿生和人工智慧新創公司,以及兩個包含高解析度圖表的簡報文件。本報告包含在我們的 2026 年企業訂閱服務中。

為什麼這項研究在2026年仍然重要

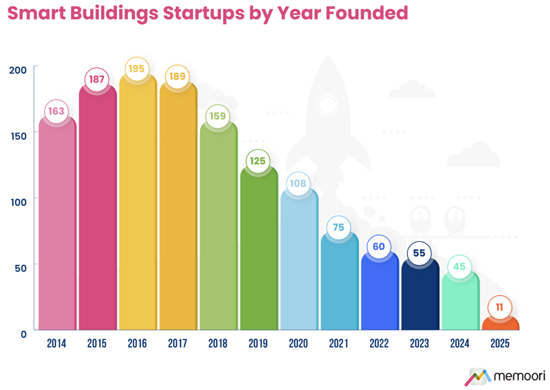

- 整個生態系已從成長階段根本性地轉向整合階段。 2025年僅有11家新創企業成立,較2016年195家的峰值穩定下降。

- 然而,智慧建築新創企業的融資活動並未顯著減少。 2025年,該領域共完成281輪融資,總額達65億美元,輪次減少5%,總價值減少14%。

- 此外,種子輪/A輪投資的平均規模正在增加。投資者變得更加挑剔,減少了投資項目的數量,但增加了每筆交易的規模。

- 當前新創企業面臨的環境充滿挑戰。投資難求,投資人更青睞那些根基穩固、收入來源清晰的公司。領先的房地產科技創投公司 Fifth Wall 近期裁員並暫停了積極的融資活動,理由是高利率和川普政府的氣候政策。

併購活躍趨勢

2025 年併購活動十分活躍,自 2014 年以來成立的新創公司共有 98 家被收購,比 2024 年同期成長了 75%。自 2014 年以來,智慧商業建築領域的新創公司收購案總數已達 554 起。

2025 年共發生 20 起物聯網平台收購案,其中包括 Vertiv 收購 Waylay NV。數位孿生相關交易包括 Oakglen Group 收購 Pupil(英國)和 Zutec 收購 Operance(英國)。

2026 年展望

智慧建築領域的新創企業格局預計將發生以下重大變化:

- 隨著市場日趨成熟,我們預期交易數量將減少,而融資輪次規模將擴大,策略參與將更加普遍。

- 隨著現有企業從少數股權投資轉向收購平台整合,產業整合將加速。

- 策略性收購者將持續圍繞人工智慧增強數位建築管理系統重組其投資組合。

This Report is the Definitive Resource for Evaluating Startups, Innovation, & Investment Trends in the Smart Building & PropTech Space 2026

The smart building startup ecosystem has reached an inflection point. While venture capital funding has moderated, M&A activity has exploded, with 98 startup acquisitions in 2025 alone, a 75% increase on 2024 and the highest annual total in the last decade. This consolidation signals a maturing market where proven business models are commanding attention from strategic buyers.

It is our 8th comprehensive evaluation of startups and scaleups in the operations and maintenance phase of the lifecycle of commercial real estate. It builds on our previous research into Grid-Interactive Buildings, HVAC Optimization, Artificial Intelligence, the Internet of Things, Video Surveillance, and Access Control.

The research includes a spreadsheet listing all 2025 funding rounds, corporate investors, M&A activity, technology categories, and 84 digital twin and AI startups across the AEC/O lifecycle, plus 2 presentation files with high-resolution charts. This report is included in our 2026 Enterprise Subscription Service.

Why This Research Matters in 2026?

- The ecosystem has fundamentally shifted from a growth phase to a consolidation phase. We identified only 11 new startups founded in 2025, and there has been a steady decline from the peak of 195 in 2016.

- BUT Funding Activity for smart building startups is not down that much. It reached $6.5 billion in 2025, spread across 281 funding rounds, a 5% decrease in the number of rounds, and a 14% decrease in total value.

- AND the average value of Seed and Series A investments has increased. Investors are being much more selective, making fewer but larger investments.

- What does this all mean? Currently, it is a tough environment for startups. Investment is harder to come by, and investors are prioritizing companies with solid fundamentals and clear revenue streams. Fifth Wall, a prominent PropTech VC, recently cut staff and stopped active fundraising, citing high interest rates and the Trump Administration's climate policies as factors in the decision.

Our definition of a startup is "a private company formed no earlier than 2014 that is focused on the commercial and industrial buildings market, is not a subsidiary or an acquisition of a larger company, and is generally financed by venture capital or private equity funding."

Intense M&A Activity

2025 saw an intense year of M&A activity, with 98 startups founded since 2014 acquired in 2025, representing a 75% increase compared to the same period in 2024. Since 2014, we have recorded 554 startup acquisitions in the smart commercial buildings sector.

There were 20 IoT platform acquisitions in 2025, including Vertiv's purchase of Waylay NV. Digital twin deals including Oakglen Group acquiring Pupil (UK) and Zutec purchasing Operance (UK).

NEW in 2026: Digital Twin & AI Startups Across the AEC/O Lifecycle

Part 2 of this report introduces expanded coverage of new companies applying digital twin and AI technologies across all stages of the building lifecycle, from architecture and design through engineering, construction, and operations.

84 companies are profiled in our comprehensive appendix, categorized by: Lifecycle stage (Architecture, Engineering, Construction, Operations), founding date and headquarters location, funding stage, and technology focus (52 AI-focused, 32 digital twin-focused). We profile 20 of these companies with an in-depth analysis of their offering, strategic focus, funding history, and market positioning.

2026 Outlook

We forecast significant shifts in the smart buildings startup landscape:

- Fewer deals, larger rounds, and heavier strategic participation as the market continues to mature.

- Consolidation will accelerate as incumbents move from minority investments to acquisitions and platform consolidation.

- Strategic buyers will continue repositioning portfolios around AI-enhanced digital building operations.

40 Startups Who Gained Traction in 2025

As part of this research, we also identified 40 startups that we believe gained market traction in 2025, selected based on organic growth, innovative business models, strategic investor interest, and headcount growth.

Who Should Buy This Report?

This research will be valuable to:

- Strategic acquirers seeking targets to expand technology portfolios.

- Building owners and operators assessing emerging technologies.

- Technology vendors who want to understand competitive positioning.

- Investors (VCs, PE firms, corporate VC arms) evaluating smart building opportunities.

智慧建築市場:按組件、連接方式、部署模式、建築類型、應用和最終用戶分類-2026-2032年全球市場預測

智慧建築市場:按組件、連接方式、部署模式、建築類型、應用和最終用戶分類-2026-2032年全球市場預測 2026年全球智慧建築(非住宅建築)市場報告2026年全球辦公大樓市場報告

2026年全球智慧建築(非住宅建築)市場報告2026年全球辦公大樓市場報告 建築能源模擬軟體市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署、最終用戶、功能、解決方案2026年全球建築能源模擬軟體市場報告2026年智慧建築與基礎設施人工智慧全球市場報告

建築能源模擬軟體市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署、最終用戶、功能、解決方案2026年全球建築能源模擬軟體市場報告2026年智慧建築與基礎設施人工智慧全球市場報告 2026年智慧建築領域五大成長機遇智慧建築市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、部署類型及最終用戶分類智慧建築市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

2026年智慧建築領域五大成長機遇智慧建築市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、部署類型及最終用戶分類智慧建築市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 智慧建築市場規模、佔有率和趨勢分析報告:按組件、解決方案、服務、最終用途、地區和細分市場預測(2026-2033 年)

智慧建築市場規模、佔有率和趨勢分析報告:按組件、解決方案、服務、最終用途、地區和細分市場預測(2026-2033 年)