|

市場調查報告書

商品編碼

2064088

全球控制閥市場(至 2032 年):按類型(旋轉式(球閥、蝶閥、旋塞閥)、線性式(截止閥、夾管閥、閘閥、隔膜閥、止回閥、電磁閥、針閥、固定錐閥)、閥門尺寸(小於 1 英寸、1-6 英寸、6-25 英寸、25-50 英寸)Control Valve Market by Type [Rotary (Ball, Butterfly, Plug)], Linear (Globe, Pinch, Gate, Diaphragm, Check, Solenoid, Needle, Fixed Cone), Vale Size (Up to 1", >1-6", >6-25", >25-50", >50"), Media (Liquid, Gas, Slurry) - Global Forecast to 2032 |

||||||

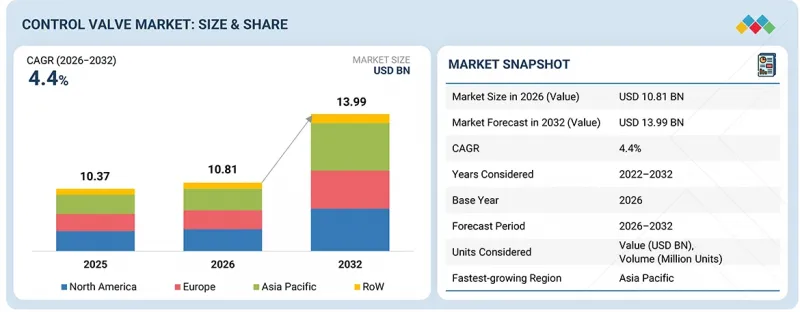

預計控制閥市場將從 2026 年的 108.1 億美元成長到 2032 年的 139.9 億美元,複合年成長率為 4.4%。

預計在預測期內,控制閥市場將經歷強勁成長,這主要得益於石油天然氣、發電、化學、水和用水和污水處理、製藥以及食品飲料等行業對工業自動化的日益重視。

| 調查範圍 | |

|---|---|

| 調查期 | 2021-2032 |

| 基準年 | 2025 |

| 預測期 | 2026-2032 |

| 單元 | 金額(美元) |

| 部分 | 按類型、按最終用戶、按地區 |

| 目標區域 | 北美、歐洲、亞太地區及其他地區 |

隨著各行業日益重視提升營運效率、製程可靠性和合規性,對先進控制閥解決方案的需求顯著成長。控制閥在調節流量、壓力、溫度和流體處理過程中發揮至關重要的作用,確保工業運作的安全和高效。製造商正不斷開發智慧控制閥,將數位閥門控制器、物聯網監控系統和基於人工智慧的預測性維護技術整合於一體,以增強流程自動化並減少運作。這些技術進步正在提升工業設施的製程可視性、資產可靠性和能源效率。此外,對工業基礎設施、煉油廠現代化、能源轉型專案和智慧製造舉措的投資不斷增加,也加速了市場對智慧控制閥的接受度。憑藉改進的運作控制、降低的維護成本、增強的安全性和更高的自動化效率等長期效益,控制閥已成為現代工業製程系統不可或缺的組成部分。

“按材料分類,預計不銹鋼細分市場將在預測期內佔據最大的市場佔有率。”

由於不銹鋼控制閥具有優異的耐腐蝕性、耐用性和對嚴苛工業運作環境的適應性,預計在預測期內將實現顯著成長。這些閥門廣泛應用於對可靠性和運作要求極高的行業,例如石油天然氣、化學、能源電力、水處理和用水和污水處理以及食品飲料行業。它們能夠承受高壓、溫度波動和腐蝕性流體,使其成為要求嚴苛的製程工業的理想之選。此外,工業自動化、基礎設施現代化以及對製程安全系統投資的增加也推動了不銹鋼控制閥的應用。對可靠、高效且低維護的流量控制解決方案日益成長的需求也進一步促進了不銹鋼控制閥市場的成長。

“按線性閥門類型分類,預計在預測期內,截止閥將獲得顯著的市場佔有率。”

球閥在整體工業應用中發揮著至關重要的作用,能夠提供精確的流量控制和可靠的節流性能,因此有望佔據線性控制閥市場的重要佔有率。這些閥門廣泛應用於石油天然氣、能源電力、化學、水處理和用水和污水處理以及製藥等行業,在這些行業中,對壓力、溫度和流體流量的精確控制至關重要。球閥具有控制精度高、截止能力強以及在各種工況下都能保持穩定性能等優點,從而提高了運作效率和製程安全性。此外,對工業自動化、製程最佳化和先進流量控制系統的需求不斷成長,也進一步推動了球閥在整體工業應用中的廣泛應用。

“預計在預測期內,亞太地區將成為控制閥市場成長最快的地區。”

預計亞太地區將在預測期內成為成長最快的地區,這主要得益於快速的工業化、基礎設施擴張以及關鍵終端用戶產業的強勁成長。中國、印度、日本和韓國等國家在石油天然氣、發電、化學、水處理和用水和污水處理以及製造業等領域的投資增加,顯著推動了對控制閥的需求。工業自動化、智慧製造技術和流程最佳化系統的日益普及,進一步加速了市場成長。政府對工業發展、能源基礎設施和水資源管理項目的支持,以及具有成本競爭力的製造地,也促進了市場滲透。對營運效率、流程安全和數位自動化的日益重視,也持續支撐著亞太地區控制閥市場的強勁成長動能。

本報告考察了全球控制閥市場,提供了市場概述、影響市場成長的各種因素分析、技術和專利趨勢、法律制度、案例研究、歷史和預測市場規模、按各個細分市場和地區/主要國家進行的詳細分析、競爭格局以及主要公司的概況。

目錄

第1章:引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 與相關市場和不同產業相關的跨領域機遇

- 一級/二級/三級公司的策略性舉措

第5章 產業趨勢

- 波特五力分析

- 宏觀經濟展望

- GDP趨勢與預測

- 全球石油和天然氣產業的趨勢

- 全球化學工業的發展趨勢

- 供應鏈分析

- 生態系分析

- 價格分析

- 貿易分析

- 2026-2027 年主要會議和活動

- 影響客戶業務的趨勢/顛覆性因素

- 投資和資金籌措場景

- 案例研究分析

- 美國關稅對控制閥市場的影響

第6章:技術進步、人工智慧的影響、專利與創新

- 主要技術

- 智慧閥門定位器

- 先進密封

- 互補技術

- 工業感測器

- 工業連接平台

- 鄰近技術

- 工業IoT

- 工業自動化

- 智慧型控制器

- 技術藍圖

- 專利分析

- 人工智慧對控制閥市場的影響

- 成功案例和實際應用

第7章 監理情勢

- 當地法規和合規性

第8章:顧客趨勢與購買行為

- 決策流程

- 採購過程中涉及的關鍵相關利益者和評估標準

- 實施障礙和內部挑戰

- 來自各個終端使用者產業的未滿足需求

第9章:控制閥的介質類型

- 泥

- 氣體

- 液體

第10章 控制閥的壓力範圍

- 小於 50 巴

- 50-350 巴

- 351~700 BAR

- 701–1,000 巴

- 超過1000巴

第11章 控制閥市場:按類型分類

- 旋轉閥

- 球閥

- 蝶閥

- 塞閥

- 線性閥

- 球閥

- 隔膜閥

- 其他

第12章 控制閥市場:依組件分類

- 執行器

- 氣壓

- 電

- 油壓

- 閥體

- 其他

第13章 控制閥市場:依材料分類

- 不銹鋼

- 奧氏體和馬氏體

- 碳和鉻鉬

- 合金

- 鑄鐵

- 極低溫度

- 其他

第14章 控制閥市場:依尺寸分類

- 最大 1 英寸

- 1-6英寸

- 6-25英寸

- 25-50英寸

- 超過50英寸

第15章 控制閥市場:依行業分類

- 石油和天然氣

- 井口、鑽井系統、海底生產

- 管道、壓縮站、儲罐

- 煉油廠、石化廠、反應器

- 能源與電力

- 蒸氣渦輪流量控制

- 鍋爐壓力管理

- 冷凝水流量調節

- 渦輪機安全壓力釋放

- 水處理和污水處理

- 水分配和儲存

- 抽水站流量控制

- 水處理過程控制

- 儲存流量管理

- 壓力調節

- 食品/飲料

- 衛生處理系統

- 飲料生產線

- 乳製品加工廠

- CIP清洗系統

- 金屬和採礦

- 漿料輸送管

- 礦物加工廠

- 藥物注射系統

- 尾礦管道管理系統

- 化學品

- 反應器流量控制

- 化學轉移

- 蒸餾塔流量調節

- 腐蝕性液體的處理

- 緊急壓力保護

- 製藥

- 無菌液體的處理

- 生物製程

- 反應器和發酵槽的控制

- 潔淨室流體分佈

- 建築/施工

- 暖通空調系統

- 消防系統

- 供水和管道系統

- 紙漿和造紙

- 紙漿原料流量與濃度控制

- 化學注入和漂白過程控制

- 蒸氣和壓力控制

- 鍋爐供水和公用設施流量調整

- 污水處理和排水管理

- 其他行業

第16章 控制閥市場:依地區分類

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他

- 其他地區

- GCC

- 非洲及其他中東地區

- 南美洲

第17章 競爭格局

- 概述

- 主要公司/主要企業的競爭策略

- 收入分析

- 市佔率分析

- 企業估值和財務指標

- 品牌對比

- 企業估值矩陣:主要公司

- 公司估值矩陣:新創企業/中小企業

- 競爭格局

第18章:公司簡介

- 大公司

- EMERSON ELECTRIC CO.

- FLOWSERVE CORPORATION

- SLB

- IMI

- CRANE HOLDINGS, CO.

- KITZ CORPORATION

- CURTISS-WRIGHT CORPORATION

- VALMET

- BAKER HUGHES COMPANY

- KSB SE & CO. KGAA

- BRAY INTERNATIONAL

- AVK HOLDING A/S

- CIRCOR INTERNATIONAL, INC.

- 其他公司

- SAMSON AG

- HONEYWELL INTERNATIONAL INC.

- NEWAY VALVE

- ALFA LAVAL

- SPIRAX GROUP PLC

- WATTS.

- PARKER HANNIFIN CORP

- THE WEIR GROUP PLC

- HAM-LET GROUP

- AVCON CONTROLS PVT LTD.

- VELAN ABV SRL

- TRILLIUM FLOW TECHNOLOGIES

第19章:調查方法

第20章附錄

According to MarketsandMarkets, the control valve market is projected to reach USD 13.99 billion by 2032 from USD 10.81 billion in 2026, at a CAGR of 4.4%. The control valve market is projected to witness strong growth during the forecast period, driven by the increasing adoption of industrial automation across industries such as oil & gas, power generation, chemicals, water & wastewater treatment, pharmaceuticals, and food & beverages.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Type, End User and Region |

| Regions covered | North America, Europe, APAC, RoW |

As industries focus on improving operational efficiency, process reliability, and regulatory compliance, the demand for advanced control valve solutions is rising significantly. Control valves play a critical role in regulating flow, pressure, temperature, and fluid handling processes, enabling safe and efficient industrial operations. Manufacturers are increasingly developing smart control valves integrated with digital valve controllers, IoT-enabled monitoring systems, and AI-based predictive maintenance technologies to enhance process automation and reduce operational downtime. These advancements improve process visibility, asset reliability, and energy efficiency across industrial facilities. Additionally, growing investments in industrial infrastructure, refinery modernization, energy transition projects, and smart manufacturing initiatives are accelerating market adoption. The long-term benefits of improved operational control, reduced maintenance costs, enhanced safety, and automation efficiency make control valves a critical component across modern industrial process systems.

"By material, stainless steel segment to capture largest market share throughout forecast period"

Stainless steel control valves are expected to witness significant growth during the forecast period due to their high corrosion resistance, durability, and suitability for harsh industrial operating environments. These valves are widely used in applications such as oil & gas, chemicals, energy & power, water & wastewater treatment, and food & beverages, where reliability and long operational life are critical. Their ability to withstand high pressure, temperature variations, and corrosive fluids makes them highly suitable for demanding process industries. Additionally, increasing investments in industrial automation, infrastructure modernization, and process safety systems are driving the adoption of stainless steel control valves. Growing demand for reliable, efficient, and low-maintenance flow control solutions is further supporting the growth of the stainless steel segment in the control valve market.

"By linear valves, globe valves to capture significant market share throughout forecast period"

Globe valves are expected to capture a significant share of the linear control valve market due to their critical role in providing precise flow regulation and reliable throttling performance across industrial applications. These valves are widely used in industries such as oil & gas, energy & power, chemicals, water & wastewater treatment, and pharmaceuticals, where accurate control of pressure, temperature, and fluid flow is essential. Their ability to deliver high control accuracy, strong shutoff capability, and stable performance under varying operating conditions enhances operational efficiency and process safety. Increasing demand for industrial automation, process optimization, and advanced flow control systems is further driving the adoption of globe valves across industrial applications.

"Asia Pacific to be fastest-growing region in control valve market during forecast period"

Asia Pacific is likely to be the fastest-growing region in the control valve market during the forecast period due to rapid industrialization, infrastructure expansion, and strong growth across key end-use industries. Increasing investments in oil & gas, power generation, chemicals, water & wastewater treatment, and manufacturing sectors in countries such as China, India, Japan, and South Korea are significantly driving demand for control valves. Rising adoption of industrial automation, smart manufacturing technologies, and process optimization systems is further accelerating market growth. Additionally, supportive government initiatives for industrial development, energy infrastructure, and water management projects, along with the presence of cost-competitive manufacturing hubs, are enhancing market penetration. Increasing emphasis on operational efficiency, process safety, and digital automation continues to support the strong growth trajectory of the Asia Pacific control valve market.

Breakdown of Primaries

A variety of executives from key organizations operating in the hydrogen sensor market were interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

- By Company Type: Tier 1 - 38%, Tier 2 - 28%, and Tier 3 - 34%

- By Designation: C-level Executives - 40%, Directors - 30%, and Others - 30%

- By Region: North America - 35%, Europe - 35, Asia Pacific - 20%, and RoW - 10%

Note: The RoW region includes the Middle East, Africa, and South America. Other designations include product, sales, and marketing managers. Three tiers of companies have been defined based on their total revenues as of 2025: Tier 3: revenue less than USD 100 million; Tier 2: revenue between USD 100 million and USD 1 billion; and Tier 1: revenue more than USD 1 billion.

Major players profiled in this report are as follows: Emerson Electric Co. (US), Flowserve Corporation (US), SLB (US), KITZ Corporation (Japan), Valmet (Finland), IMI plc (UK), Crane Holdings Co. (US), Spirax Sarco Limited (UK), Curtiss-Wright Corporation (US), and KSB SE & Co. KGaA (Germany), among others.

These companies compete by continuously enhancing control valve performance, focusing on improved flow control accuracy, operational reliability, durability, and automation capabilities across diverse industrial applications. Strategic emphasis is placed on developing advanced control valve technologies, including smart valves, digital valve controllers, intelligent actuators, and IoT-enabled monitoring systems integrated with AI-based predictive maintenance platforms. Market participants prioritize scalable and efficient solutions tailored for industries such as oil & gas, energy & power, chemicals, water & wastewater treatment, and pulp & paper. Strong focus is also placed on ensuring process safety, regulatory compliance, energy efficiency, and seamless integration with industrial automation systems. Continued investments in smart manufacturing technologies, advanced materials, digitalization, and automation solutions, along with collaborations with industrial operators and technology providers, are expected to sustain competition and accelerate adoption across the global control valve market.

The study provides a detailed competitive analysis of these key players in the control valve market, presenting their company profiles, most recent developments, and key market strategies.

Research Coverage

This report on the control valve market presents a detailed analysis based on component, material, type, valve size, end-use industry, and region. By component, the market is segmented into actuator, valve body, and other components. By material, it is segmented into stainless steel, cast iron, cryogenic, alloy-based, and other materials. By type, the market includes rotary and linear. By valve size, it is classified into up to 1", >1-6", >6-25", >25-50", and >50". By end-use industry, the market covers oil & gas, energy & power, water & wastewater treatment, food & beverages, metals & mining, chemicals, pharmaceuticals, building & construction, pulp & paper, and other industries. Based on media, the market covers slurry, gas, and liquid. The market based on pressure range is segmented into <50 bar, 50-350 bar, >350-700 bar, >700-1,000 bar, and >1,000 bar. The regional analysis includes North America, Europe, Asia Pacific, and RoW, enabling evaluation of demand patterns, growth drivers, and industry trends.

Reasons to Buy the Report

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the control valve market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

- Analysis of key drivers (rapid industrial automation and energy infrastructure expansion, increasing investment in oil and gas infrastructure in Middle East), restraints (lack of standardized certifications and government policies, complications associated with installation and maintenance), opportunities (rising integration of advanced technologies into smart valves, increasing green hydrogen production for industrial use), and challenges (risks associated with safety and operational efficiency due to leakage, high maintenance and integration costs associated with smart control valve systems) influencing the growth of the control valve market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the control valve market

- Market Development: Comprehensive information about lucrative markets by analyzing the control valve market across varied regions

- Market Diversification: Exhaustive information about new products/services, untapped geographies, recent developments, and investments in the control valve market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Emerson Electric Co. (US), Flowserve Corporation (US), SLB (US), KITZ Corporation (Japan), Valmet (Finland), IMI plc (UK), Crane Holdings Co. (US), Curtiss-Wright Corporation (US), KSB SE & Co. KGaA (Germany), and Baker Hughes Company (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING CONTROL VALVE MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CONTROL VALVE MARKET

- 3.2 CONTROL VALVE MARKET, BY COMPONENT

- 3.3 CONTROL VALVE MARKET, BY MATERIAL

- 3.4 CONTROL VALVE MARKET, BY TYPE

- 3.5 CONTROL VALVE MARKET, BY SIZE

- 3.6 CONTROL VALVE MARKET, BY INDUSTRY

- 3.7 CONTROL VALVE MARKET, BY REGION

- 3.8 CONTROL VALVE MARKET, BY GEOGRAPHY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rapid industrial automation and energy infrastructure expansion

- 4.2.1.2 Increasing investment in oil and gas infrastructure in Middle East

- 4.2.1.3 Mounting electricity demand amid rapid urbanization and industrialization in Southeast Asia

- 4.2.1.4 High investment in LNG and natural gas processing infrastructure

- 4.2.2 RESTRAINTS

- 4.2.2.1 Lack of standardized certifications and government policies

- 4.2.2.2 Installation and maintenance complications

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising integration of advanced technologies into smart valves

- 4.2.3.2 Increasing green hydrogen production for industrial use

- 4.2.4 CHALLENGES

- 4.2.4.1 Safety risks and operational inefficiency due to leakage

- 4.2.4.2 High maintenance and integration costs of smart control valves

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL OIL & GAS INDUSTRY

- 5.2.4 TRENDS IN GLOBAL CHEMICALS INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING RANGE OF CONTROL VALVES OFFERED BY KEY PLAYERS, BY VALVE TYPE, 2025

- 5.5.2 PRICING TREND OF CONTROL VALVES, BY REGION, 2021-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 848110)

- 5.6.2 EXPORT SCENARIO (HS CODE 848110)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 FLOWSERVE SUPPORTS LNG FACILITY WITH ADVANCED CRYOGENIC CONTROL VALVE SOLUTIONS

- 5.10.2 FLOWSERVE HELPS INDUSTRIAL OPERATORS WITH REDRAVEN INDUSTRIAL IOT PLATFORM POWERED BY INTELLIGENT VALVE MONITORING TECHNOLOGY

- 5.10.3 EMERSON AIDS LARAMIE ENERGY WITH ASCO ELECTRIC DUMP VALVES

- 5.11 IMPACT OF US TARIFFS - CONTROL VALVE MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, AND INNOVATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 SMART VALVE POSITIONERS

- 6.1.2 ADVANCE SEALING

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 INDUSTRIAL SENSORS

- 6.2.2 INDUSTRIAL CONNECTIVITY PLATFORMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 INDUSTRIAL INTERNET OF THINGS

- 6.3.2 INDUSTRIAL AUTOMATION

- 6.3.3 SMART CONTROLLERS

- 6.4 TECHNOLOGY ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI ON CONTROL VALVE MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY OEMS IN CONTROL VALVE MARKET

- 6.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN CONTROL VALVE MARKET

- 6.6.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED CONTROL VALVES

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS INDUSTRIES

9 MEDIA TYPES FOR CONTROL VALVES

- 9.1 INTRODUCTION

- 9.2 SLURRY

- 9.3 GAS

- 9.4 LIQUID

10 PRESSURE RANGE OF CONTROL VALVES

- 10.1 INTRODUCTION

- 10.2 <50 BAR

- 10.3 50-350 BAR

- 10.4 351-700 BAR

- 10.5 701-1,000 BAR

- 10.6 >1,000 BAR

11 CONTROL VALVE MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.2 ROTARY VALVES

- 11.2.1 BALL VALVES

- 11.2.1.1 Reliable, bubble-tight sealing attributes to contribute to segmental growth

- 11.2.2 BUTTERFLY VALVES

- 11.2.2.1 Precise control, compact, and lightweight features to foster segmental growth

- 11.2.3 PLUG VALVES

- 11.2.3.1 Ease of cleaning and effective leakage-prevention mechanism to augment segmental growth

- 11.2.1 BALL VALVES

- 11.3 LINEAR VALVES

- 11.3.1 GLOBE VALVES

- 11.3.1.1 Integration with predictive maintenance diagnostics and digital communication protocols for Industry 4.0 environments to spur demand

- 11.3.2 DIAPHRAGM VALVES

- 11.3.2.1 Use to control flow of corrosive and radioactive fluids to accelerate segmental growth

- 11.3.3 OTHER LINEAR VALVES

- 11.3.1 GLOBE VALVES

12 CONTROL VALVE MARKET, BY COMPONENT

- 12.1 INTRODUCTION

- 12.2 ACTUATORS

- 12.2.1 PNEUMATIC

- 12.2.1.1 Cost-effectiveness, fast response time, and suitability for hazardous industrial environments to fuel segmental growth

- 12.2.2 ELECTRIC

- 12.2.2.1 Industrial automation and energy-efficient process control requirements to augment segmental growth

- 12.2.3 HYDRAULIC

- 12.2.3.1 Superior torque output and operational durability to expedite segmental growth

- 12.2.1 PNEUMATIC

- 12.3 VALVE BODIES

- 12.3.1 HIGH EMPHASIS ON RELIABILITY, EFFICIENCY, AND SAFETY IN INDUSTRIAL OPERATIONS TO BOLSTER SEGMENTAL GROWTH

- 12.4 OTHER COMPONENTS

13 CONTROL VALVE MARKET, BY MATERIAL

- 13.1 INTRODUCTION

- 13.2 STAINLESS STEEL

- 13.2.1 SUPERIOR CORROSION RESISTANCE, DURABILITY, AND TEMPERATURE HANDLING CAPABILITIES TO BOOST SEGMENTAL GROWTH

- 13.2.2 AUSTENITIC & MARTENSITIC

- 13.2.3 CARBON & CHROME MOLY

- 13.3 ALLOY

- 13.3.1 STRONG FOCUS ON TACKLING PRESSURES AND TEMPERATURES IN STEAM POWER PLANTS TO SPUR DEMAND

- 13.4 CAST IRON

- 13.4.1 ABILITY TO WITHSTAND SEVERE VIBRATIONS AND DURABILITY TO FOSTER SEGMENTAL GROWTH

- 13.5 CRYOGENIC

- 13.5.1 NEED FOR SAFE PRODUCTION AND STORAGE OF LIQUEFIED GASES TO ACCELERATE SEGMENTAL GROWTH

- 13.6 OTHER MATERIALS

14 CONTROL VALVE MARKET, BY SIZE

- 14.1 INTRODUCTION

- 14.2 UP TO 1"

- 14.2.1 RISING NEED FOR LOW PRESSURE AND TEMPERATURE IN PROCESS INDUSTRIES TO BOLSTER SEGMENTAL GROWTH

- 14.3 >1-6"

- 14.3.1 GROWING DEMAND FROM OIL & GAS AND CHEMICALS INDUSTRIES TO EXPEDITE SEGMENTAL GROWTH

- 14.4 >6-25"

- 14.4.1 INCREASING USE FOR HIGH-PRESSURE APPLICATIONS TO BOOST SEGMENTAL GROWTH

- 14.5 >25-50"

- 14.5.1 GROWING EMPHASIS ON HANDLING HIGH TEMPERATURES AND PRESSURES IN INDUSTRIES TO FUEL SEGMENTAL GROWTH

- 14.6 >50"

- 14.6.1 INCREASING USE IN THERMAL POWER AND PETROCHEMICAL REFINERIES TO AUGMENT SEGMENTAL GROWTH

15 CONTROL VALVE MARKET, BY INDUSTRY

- 15.1 INTRODUCTION

- 15.2 OIL & GAS

- 15.2.1 REQUIREMENT FOR ADVANCED EQUIPMENT AND TECHNOLOGIES IN PRODUCTION AND TRANSPORTATION PROCESSES TO DRIVE MARKET

- 15.2.2 WELLHEADS, DRILLING SYSTEMS & SUBSEA PRODUCTION

- 15.2.3 PIPELINES, COMPRESSOR STATIONS & STORAGE TERMINALS

- 15.2.4 REFINERIES, PETROCHEMICAL PLANTS & REACTORS

- 15.3 ENERGY & POWER

- 15.3.1 NEED TO INCREASE ELECTRICITY PRODUCTION AND MINIMIZE ENVIRONMENTAL IMPACT TO BOOST SEGMENTAL GROWTH

- 15.3.2 STEAM TURBINE FLOW CONTROL

- 15.3.3 BOILER PRESSURE MANAGEMENT

- 15.3.4 CONDENSATE FLOW REGULATION

- 15.3.5 TURBINE SAFETY PRESSURE RELIEF

- 15.4 WATER & WASTEWATER TREATMENT

- 15.4.1 INCREASED POLLUTION DUE TO POPULATION GROWTH AND INDUSTRIALIZATION TO EXPEDITE SEGMENTAL GROWTH

- 15.4.2 WATER DISTRIBUTION & STORAGE

- 15.4.3 PUMP STATION FLOW CONTROL

- 15.4.4 WATER TREATMENT PROCESS REGULATION

- 15.4.5 STORAGE FLOW MANAGEMENT

- 15.4.6 PRESSURE REGULATION

- 15.5 FOOD & BEVERAGES

- 15.5.1 HIGH EMPHASIS ON ENHANCING SAFETY AND NUTRITIONAL VALUES TO ACCELERATE SEGMENTAL GROWTH

- 15.5.2 HYGIENIC PROCESSING SYSTEMS

- 15.5.3 BEVERAGE PRODUCTION LINES

- 15.5.4 DAIRY PROCESSING PLANTS

- 15.5.5 CLEANING-IN-PLACE SYSTEMS

- 15.6 METALS & MINING

- 15.6.1 STRONG FOCUS ON REDUCING SCRAP AND DOWNTIME WHILE INCREASING OVERALL YIELD TO FOSTER SEGMENTAL GROWTH

- 15.6.2 SLURRY TRANSPORTATION PIPELINES

- 15.6.3 MINERAL PROCESSING PLANTS

- 15.6.4 CHEMICAL DOSING SYSTEMS

- 15.6.5 TAILINGS PIPELINE MANAGEMENT SYSTEMS

- 15.7 CHEMICALS

- 15.7.1 HIGH EMPHASIS ON REDUCING EMISSIONS AND INCREASING PLANT SAFETY TO BOLSTER SEGMENTAL GROWTH

- 15.7.2 REACTOR FLOW CONTROL

- 15.7.3 CHEMICAL TRANSFER

- 15.7.4 DISTILLATION COLUMN FLOW REGULATION

- 15.7.5 CORROSIVE FLUID HANDLING

- 15.7.6 EMERGENCY PRESSURE PROTECTION

- 15.8 PHARMACEUTICALS

- 15.8.1 RAPID DIGITALIZATION AND AUTOMATION FOR BETTER CONTROL OVER OPERATIONS TO FACILITATE SEGMENTAL GROWTH

- 15.8.2 STERILE FLUID HANDLING

- 15.8.3 BIOPROCESSING

- 15.8.4 REACTOR & FERMENTER CONTROL

- 15.8.5 CLEANROOM FLUID DISTRIBUTION

- 15.9 BUILDING & CONSTRUCTION

- 15.9.1 NEED TO REGULATE FLOW OF FLUIDS AND GASES TO CONTRIBUTE TO SEGMENTAL GROWTH

- 15.9.2 HVAC SYSTEMS

- 15.9.3 FIRE PROTECTION SYSTEMS

- 15.9.4 WATER SUPPLY & PLUMBING SYSTEMS

- 15.10 PULP & PAPER

- 15.10.1 STRONG FOCUS ON MONITORING AND MANAGING WORKFLOW AND OPTIMIZING PROCESSES TO DRIVE MARKET

- 15.10.2 PULP STOCK FLOW & CONSISTENCY CONTROL

- 15.10.3 CHEMICAL DOSING & BLEACHING PROCESS CONTROL

- 15.10.4 STEAM & PRESSURE CONTROL

- 15.10.5 BOILER FEEDWATER & UTILITY FLOW REGULATING

- 15.10.6 WASTEWATER TREATMENT & EFFLUENT MANAGEMENT

- 15.11 OTHER INDUSTRIES

16 CONTROL VALVE MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 NORTH AMERICA

- 16.2.1 US

- 16.2.1.1 Rising shale gas exploration and wastewater infrastructure modernization to augment market growth

- 16.2.2 CANADA

- 16.2.2.1 Increasing geothermal, HVAC, and industrial automation projects to expedite market growth

- 16.2.3 MEXICO

- 16.2.3.1 Growing demand for energy and water sanitation solutions to fuel market growth

- 16.2.1 US

- 16.3 EUROPE

- 16.3.1 UK

- 16.3.1.1 Increasing valve automation and stringent environmental regulations to foster market growth

- 16.3.2 GERMANY

- 16.3.2.1 Rapid industrial automation and decarbonization initiatives to accelerate market growth

- 16.3.3 FRANCE

- 16.3.3.1 Increasing nuclear energy development and renewable energy investment to create lucrative growth opportunities

- 16.3.4 ITALY

- 16.3.4.1 Growing emphasis on reducing water wastage to contribute to market growth

- 16.3.5 REST OF EUROPE

- 16.3.1 UK

- 16.4 ASIA PACIFIC

- 16.4.1 CHINA

- 16.4.1.1 Rapid industrialization and infrastructure projects to augment market growth

- 16.4.2 JAPAN

- 16.4.2.1 Increasing reliance on nuclear energy to generate electricity and semiconductor investments to drive market

- 16.4.3 INDIA

- 16.4.3.1 Rising offshore explorations and development of oil and gas pipeline infrastructure to bolster market growth

- 16.4.4 SOUTH KOREA

- 16.4.4.1 Expanding hydrogen export infrastructure and semiconductor manufacturing to expedite market growth

- 16.4.5 REST OF ASIA PACIFIC

- 16.4.1 CHINA

- 16.5 ROW

- 16.5.1 GCC

- 16.5.2 AFRICA & REST OF MIDDLE EAST

- 16.5.3 SOUTH AMERICA

- 16.5.3.1 Growing demand for automation and process optimization to accelerate market growth

17 COMPETITIVE LANDSCAPE

- 17.1 OVERVIEW

- 17.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2026

- 17.3 REVENUE ANALYSIS, 2021-2025

- 17.4 MARKET SHARE ANALYSIS, 2025

- 17.5 COMPANY VALUATION AND FINANCIAL METRICS

- 17.6 BRAND COMPARISON

- 17.6.1 EMERSON ELECTRIC CO. (US)

- 17.6.2 FLOWSERVE CORPORATION (US)

- 17.6.3 SLB (US)

- 17.6.4 IMI PLC (UK)

- 17.6.5 CRANE COMPANY (US)

- 17.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 17.7.1 STARS

- 17.7.2 EMERGING LEADERS

- 17.7.3 PERVASIVE PLAYERS

- 17.7.4 PARTICIPANTS

- 17.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 17.7.5.1 Company footprint

- 17.7.5.2 Region footprint

- 17.7.5.3 Type footprint

- 17.7.5.4 Component footprint

- 17.7.5.5 Industry footprint

- 17.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 17.8.1 PROGRESSIVE COMPANIES

- 17.8.2 RESPONSIVE COMPANIES

- 17.8.3 DYNAMIC COMPANIES

- 17.8.4 STARTING BLOCKS

- 17.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 17.8.5.1 Detailed list of key startups/SMEs

- 17.8.5.2 Competitive benchmarking of key startups/SMEs

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES/EXPANSIONS

- 17.9.2 DEALS

- 17.9.3 EXPANSIONS

18 COMPANY PROFILES

- 18.1 KEY PLAYERS

- 18.1.1 EMERSON ELECTRIC CO.

- 18.1.1.1 Business overview

- 18.1.1.2 Products/Solutions/Services offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Product launches/expansions

- 18.1.1.4 MnM view

- 18.1.1.4.1 Key strengths/Right to win

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses/Competitive threats

- 18.1.2 FLOWSERVE CORPORATION

- 18.1.2.1 Business overview

- 18.1.2.2 Products/Solutions/Services offered

- 18.1.2.3 Recent developments

- 18.1.2.3.1 Product launches/expansions

- 18.1.2.3.2 Deals

- 18.1.2.4 MnM view

- 18.1.2.4.1 Key strengths/Right to win

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses/Competitive threats

- 18.1.3 SLB

- 18.1.3.1 Business overview

- 18.1.3.2 Products/Solutions/Services offered

- 18.1.3.3 Recent developments

- 18.1.3.3.1 Expansions

- 18.1.3.4 MnM view

- 18.1.3.4.1 Key strengths/Right to win

- 18.1.3.4.2 Strategic choices

- 18.1.3.4.3 Weaknesses/Competitive threats

- 18.1.4 IMI

- 18.1.4.1 Business overview

- 18.1.4.2 Products/Solutions/Services offered

- 18.1.4.3 Recent developments

- 18.1.4.3.1 Product launches/expansions

- 18.1.4.4 MnM view

- 18.1.4.4.1 Key strengths/Right to win

- 18.1.4.4.2 Strategic choices

- 18.1.4.4.3 Weaknesses/Competitive threats

- 18.1.5 CRANE HOLDINGS, CO.

- 18.1.5.1 Business overview

- 18.1.5.2 Products/Solutions/Services offered

- 18.1.5.3 Recent developments

- 18.1.5.3.1 Deals

- 18.1.5.4 MnM view

- 18.1.5.4.1 Key strengths/Right to win

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses/Competitive threats

- 18.1.6 KITZ CORPORATION

- 18.1.6.1 Business overview

- 18.1.6.2 Products/Solutions/Services offered

- 18.1.6.3 Recent developments

- 18.1.6.3.1 Product launches/expansions

- 18.1.6.3.2 Deals

- 18.1.6.3.3 Expansions

- 18.1.7 CURTISS-WRIGHT CORPORATION

- 18.1.7.1 Business overview

- 18.1.7.2 Products/Solutions/Services offered

- 18.1.8 VALMET

- 18.1.8.1 Business overview

- 18.1.8.2 Products/Solutions/Services offered

- 18.1.8.3 Recent developments

- 18.1.8.3.1 Product launches/expansions

- 18.1.8.3.2 Deals

- 18.1.9 BAKER HUGHES COMPANY

- 18.1.9.1 Business overview

- 18.1.9.2 Products/Solutions/Services offered

- 18.1.9.3 Recent developments

- 18.1.9.3.1 Product launches/expansions

- 18.1.9.3.2 Deals

- 18.1.10 KSB SE & CO. KGAA

- 18.1.10.1 Business overview

- 18.1.10.2 Products/Solutions/Services offered

- 18.1.10.3 Recent developments

- 18.1.10.3.1 Product launches/expansions

- 18.1.11 BRAY INTERNATIONAL

- 18.1.11.1 Business overview

- 18.1.11.2 Products/Solutions/Services offered

- 18.1.11.3 Recent developments

- 18.1.11.3.1 Deals

- 18.1.12 AVK HOLDING A/S

- 18.1.12.1 Business overview

- 18.1.12.2 Products/Solutions/Services offered

- 18.1.12.3 Recent developments

- 18.1.12.3.1 Deals

- 18.1.13 CIRCOR INTERNATIONAL, INC.

- 18.1.13.1 Business overview

- 18.1.13.2 Products/Solutions/Services offered

- 18.1.13.3 Recent developments

- 18.1.13.3.1 Deals

- 18.1.1 EMERSON ELECTRIC CO.

- 18.2 OTHER PLAYERS

- 18.2.1 SAMSON AG

- 18.2.2 HONEYWELL INTERNATIONAL INC.

- 18.2.3 NEWAY VALVE

- 18.2.4 ALFA LAVAL

- 18.2.5 SPIRAX GROUP PLC

- 18.2.6 WATTS.

- 18.2.7 PARKER HANNIFIN CORP

- 18.2.8 THE WEIR GROUP PLC

- 18.2.9 HAM-LET GROUP

- 18.2.10 AVCON CONTROLS PVT LTD.

- 18.2.11 VELAN ABV S.R.L.

- 18.2.12 TRILLIUM FLOW TECHNOLOGIES

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH DATA

- 19.1.1 SECONDARY DATA

- 19.1.1.1 Key data from secondary sources

- 19.1.1.2 List of key secondary sources

- 19.1.2 PRIMARY DATA

- 19.1.2.1 Key data from primary sources

- 19.1.2.2 List of primary interview participants

- 19.1.2.3 Breakdown of primary interviews

- 19.1.2.4 Key industry insights

- 19.1.3 SECONDARY AND PRIMARY RESEARCH

- 19.1.1 SECONDARY DATA

- 19.2 MARKET SIZE ESTIMATION

- 19.2.1 BOTTOM-UP APPROACH

- 19.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 19.2.2 TOP-DOWN APPROACH

- 19.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 19.2.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 19.2.1 BOTTOM-UP APPROACH

- 19.3 MARKET FORECAST APPROACH

- 19.3.1 SUPPLY-SIDE

- 19.3.2 DEMAND-SIDE

- 19.4 DATA TRIANGULATION

- 19.5 RESEARCH ASSUMPTIONS

- 19.6 RESEARCH LIMITATIONS

- 19.7 RISK ANALYSIS

20 APPENDIX

- 20.1 DISCUSSION GUIDE

- 20.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.3 CUSTOMIZATION OPTIONS

- 20.4 RELATED REPORTS

- 20.5 AUTHOR DETAILS

List of Tables

- TABLE 1 CONTROL VALVE MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 2 INTERCONNECTED MARKETS AND OPPORTUNITIES

- TABLE 3 STRATEGIC FOCUS OF TIER-1/2/3 PLAYERS

- TABLE 4 IMPACT OF PORTER'S FIVE FORCES

- TABLE 5 GDP GROWTH RATES, BY KEY COUNTRY, 2022-2030 (%)

- TABLE 6 ROLE OF COMPANIES IN CONTROL VALVE ECOSYSTEM

- TABLE 7 PRICING RANGE OF CONTROL VALVES OFFERED BY KEY PLAYERS, BY TYPE, 2025 (USD)

- TABLE 8 PRICING TREND OF CONTROL VALVES, BY REGION, 2021-2025 (USD)

- TABLE 9 IMPORT DATA FOR HS CODE 848110-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 10 EXPORT DATA FOR HS CODE 848110-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 11 LIST OF KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 12 FLOWSERVE SUPPLIES SEVERE-SERVICE CRYOGENIC CONTROL VALVES TO IMPROVE PROCESS RELIABILITY AND OPERATIONAL SAFETY IN FLOATING LNG FACILITY

- TABLE 13 FLOWSERVE OFFERS RAVEN INDUSTRIAL IOT PLATFORM INTEGRATED WITH VALVE MONITORING TECHNOLOGY TO HELP OIL & GAS AND LNG OPERATORS OPTIMIZE ASSET MONITORING

- TABLE 14 EMERSON PROVIDES ASCO ELECTRIC DUMP VALVES TO HELP LARAMIE ENERGY IMPROVE PRESSURE CONTROL AND REDUCE ENERGY CONSUMPTION

- TABLE 15 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 16 KEY PRODUCT-RELATED TARIFF EFFECTIVE FOR CONTROL VALVE MARKET

- TABLE 17 TECHNOLOGY FOCUS, KEY DEVELOPMENTS, AND IMPACTS

- TABLE 18 LIST OF KEY PATENTS, 2023-2025

- TABLE 19 MAJOR USE CASES OF CONTROL VALVES AND MARKET POTENTIAL

- TABLE 20 BEST PRACTICES FOLLOWED BY COMPANIES IN CONTROL VALVE MARKET

- TABLE 21 CASE STUDIES RELATED TO IMPLEMENTATION OF AI IN CONTROL VALVE MARKET

- TABLE 22 INTERCONNECTED ECOSYSTEM AND IMPACT ON CONTROL VALVE MARKET PLAYERS

- TABLE 23 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 24 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 25 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 26 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 27 STANDARDS FOLLOWED BY INDUSTRIAL VALVE MANUFACTURERS

- TABLE 28 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE INDUSTRIES (%)

- TABLE 29 BUYING CRITERIA FOR TOP INDUSTRIES

- TABLE 30 UNMET NEEDS, BY INDUSTRY

- TABLE 31 CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 32 CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 33 CONTROL VALVE MARKET, BY TYPE, 2022-2025 (MILLION UNITS)

- TABLE 34 CONTROL VALVE MARKET, BY TYPE, 2026-2032 (MILLION UNITS)

- TABLE 35 ROTARY VALVES: CONTROL VALVE MARKET, BY SIZE, 2022-2025 (USD MILLION)

- TABLE 36 ROTARY VALVES: CONTROL VALVE MARKET, BY SIZE, 2026-2032 (USD MILLION)

- TABLE 37 ROTARY VALVES: CONTROL VALVE MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 38 ROTARY VALVES: CONTROL VALVE MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 39 ROTARY VALVES: CONTROL VALVE MARKET, BY VALVE TYPE, 2022-2025 (USD MILLION)

- TABLE 40 ROTARY VALVES: CONTROL VALVE MARKET, BY VALVE TYPE, 2026-2032 (USD MILLION)

- TABLE 41 LINEAR VALVES: CONTROL VALVE MARKET, BY SIZE, 2022-2025 (USD MILLION)

- TABLE 42 LINEAR VALVES: CONTROL VALVE MARKET, BY SIZE, 2026-2032 (USD MILLION)

- TABLE 43 LINEAR VALVES: CONTROL VALVE MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 44 LINEAR VALVES: CONTROL VALVE MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 45 LINEAR VALVES: CONTROL VALVE MARKET, BY VALVE TYPE, 2022-2025 (USD MILLION)

- TABLE 46 LINEAR VALVES: CONTROL VALVE MARKET, BY VALVE TYPE, 2026-2032 (USD MILLION)

- TABLE 47 CONTROL VALVE MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 48 CONTROL VALVE MARKET, BY COMPONENT, 2026-2032 (USD MILLION)

- TABLE 49 ACTUATORS: CONTROL VALVE MARKET, BY ACTUATOR TYPE, 2022-2025 (USD MILLION)

- TABLE 50 ACTUATORS: CONTROL VALVE MARKET, BY ACTUATOR TYPE, 2026-2032 (USD MILLION)

- TABLE 51 CONTROL VALVE MARKET, BY MATERIAL, 2022-2025 (USD MILLION)

- TABLE 52 CONTROL VALVE MARKET, BY MATERIAL, 2026-2032 (USD MILLION)

- TABLE 53 CONTROL VALVE MARKET, BY SIZE, 2022-2025 (USD MILLION)

- TABLE 54 CONTROL VALVE MARKET, BY SIZE, 2026-2032 (USD MILLION)

- TABLE 55 UP TO 1": CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 56 UP TO 1": CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 57 >1-6": CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 58 >1-6": CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 59 >6-25": CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 60 >6-25": CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 61 >25-50": CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 62 >25-50": CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 63 >50": CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 64 >50": CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 65 CONTROL VALVE MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 66 CONTROL VALVE MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 67 OIL & GAS: CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 68 OIL & GAS: CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 69 OIL & GAS: CONTROL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 70 OIL & GAS: CONTROL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 71 OIL & GAS: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 72 OIL & GAS: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 73 OIL & GAS: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 74 OIL & GAS: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 75 OIL & GAS: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 76 OIL & GAS: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 77 OIL & GAS: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2022-2025 (USD MILLION)

- TABLE 78 OIL & GAS: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2026-2032 (USD MILLION)

- TABLE 79 ENERGY & POWER: CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 80 ENERGY & POWER: CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 81 ENERGY & POWER: CONTROL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 82 ENERGY & POWER: CONTROL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 83 ENERGY & POWER: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 84 ENERGY & POWER: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 85 ENERGY & POWER: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 86 ENERGY & POWER: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 87 ENERGY & POWER: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 88 ENERGY & POWER: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 89 ENERGY & POWER: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2022-2025 (USD MILLION)

- TABLE 90 ENERGY & POWER: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2026-2032 (USD MILLION)

- TABLE 91 WATER & WASTEWATER TREATMENT: CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 92 WATER & WASTEWATER TREATMENT: CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 93 WATER & WASTEWATER TREATMENT: CONTROL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 94 WATER & WASTEWATER TREATMENT: CONTROL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 95 WATER & WASTEWATER TREATMENT: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 96 WATER & WASTEWATER TREATMENT: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 97 WATER & WASTEWATER TREATMENT: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 98 WATER & WASTEWATER TREATMENT: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 99 WATER & WASTEWATER TREATMENT: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 100 WATER & WASTEWATER TREATMENT: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 101 WATER & WASTEWATER TREATMENT: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2022-2025 (USD MILLION)

- TABLE 102 WATER & WASTEWATER TREATMENT: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2026-2032 (USD MILLION)

- TABLE 103 FOOD & BEVERAGES: CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 104 FOOD & BEVERAGES: CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 105 FOOD & BEVERAGES: CONTROL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 106 FOOD & BEVERAGES: CONTROL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 107 FOOD & BEVERAGES: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 108 FOOD & BEVERAGES: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 109 FOOD & BEVERAGES: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 110 FOOD & BEVERAGES: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 111 FOOD & BEVERAGES: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 112 FOOD & BEVERAGES: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 113 FOOD & BEVERAGES: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2022-2025 (USD MILLION)

- TABLE 114 FOOD & BEVERAGES: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2026-2032 (USD MILLION)

- TABLE 115 METALS & MINING: CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 116 METALS & MINING: CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 117 METALS & MINING: CONTROL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 118 METALS & MINING: CONTROL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 119 METALS & MINING: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 120 METALS & MINING: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 121 METALS & MINING: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2022-2025 USD MILLION)

- TABLE 122 METALS & MINING: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 123 METALS & MINING: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 124 METALS & MINING: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 125 METALS & MINING: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2022-2025 (USD MILLION)

- TABLE 126 METALS & MINING: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2026-2032 (USD MILLION)

- TABLE 127 CHEMICALS: CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 128 CHEMICALS: CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 129 CHEMICALS: CONTROL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 130 CHEMICALS: CONTROL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 131 CHEMICALS: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 132 CHEMICALS: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 133 CHEMICALS: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 134 CHEMICALS: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 135 CHEMICALS: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 136 CHEMICALS: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 137 CHEMICALS: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2022-2025 (USD MILLION)

- TABLE 138 CHEMICALS: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2026-2032 (USD MILLION)

- TABLE 139 PHARMACEUTICALS: CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 140 PHARMACEUTICALS: CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 141 PHARMACEUTICALS: CONTROL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 142 PHARMACEUTICALS: CONTROL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 143 PHARMACEUTICALS: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 144 PHARMACEUTICALS: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 145 PHARMACEUTICALS: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 146 PHARMACEUTICALS: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 147 PHARMACEUTICALS: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 148 PHARMACEUTICALS: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 149 PHARMACEUTICALS: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2022-2025 (USD MILLION)

- TABLE 150 PHARMACEUTICALS: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2026-2032 (USD MILLION)

- TABLE 151 BUILDING & CONSTRUCTION: CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 152 BUILDING & CONSTRUCTION: CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 153 BUILDING & CONSTRUCTION: CONTROL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 154 BUILDING & CONSTRUCTION: CONTROL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 155 BUILDING & CONSTRUCTION: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 156 BUILDING & CONSTRUCTION: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 157 BUILDING & CONSTRUCTION: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 158 BUILDING & CONSTRUCTION: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 159 BUILDING & CONSTRUCTION: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 160 BUILDING & CONSTRUCTION: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 161 BUILDING & CONSTRUCTION: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2022-2025 (USD MILLION)

- TABLE 162 BUILDING & CONSTRUCTION: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2026-2032 (USD MILLION)

- TABLE 163 PULP & PAPER: CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 164 PULP & PAPER: CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 165 PULP & PAPER: CONTROL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 166 PULP & PAPER: CONTROL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 167 PULP & PAPER: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 168 PULP & PAPER: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 169 PULP & PAPER: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 170 PULP & PAPER: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 171 PULP & PAPER: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 172 PULP & PAPER: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 173 PULP & PAPER: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2022-2025 (USD MILLION)

- TABLE 174 PULP & PAPER: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2026-2032 (USD MILLION)

- TABLE 175 OTHER INDUSTRIES: CONTROL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 176 OTHER INDUSTRIES: CONTROL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 177 OTHER INDUSTRIES: CONTROL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 178 OTHER INDUSTRIES: CONTROL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 179 OTHER INDUSTRIES: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 180 OTHER INDUSTRIES: CONTROL VALVE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 181 OTHER INDUSTRIES: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 182 OTHER INDUSTRIES: CONTROL VALVE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 183 OTHER INDUSTRIES: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 184 OTHER INDUSTRIES: CONTROL VALVE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 185 OTHER INDUSTRIES: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2022-2025 (USD MILLION)

- TABLE 186 OTHER INDUSTRIES: CONTROL VALVE MARKET IN ROW, BY GEOGRAPHY, 2026-2032 (USD MILLION)

- TABLE 187 CONTROL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 188 CONTROL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 189 NORTH AMERICA: CONTROL VALVE MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 190 NORTH AMERICA: CONTROL VALVE MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 191 NORTH AMERICA: CONTROL VALVE MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 192 NORTH AMERICA: CONTROL VALVE MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 193 EUROPE: CONTROL VALVE MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 194 EUROPE: CONTROL VALVE MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 195 EUROPE: CONTROL VALVE MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 196 EUROPE: CONTROL VALVE MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 197 ASIA PACIFIC: CONTROL VALVE MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 198 ASIA PACIFIC: CONTROL VALVE MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 199 ASIA PACIFIC: CONTROL VALVE MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 200 ASIA PACIFIC: CONTROL VALVE MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 201 ROW: CONTROL VALVE MARKET, BY GEOGRAPHY, 2022-2025 (USD MILLION)

- TABLE 202 ROW: CONTROL VALVE MARKET, BY GEOGRAPHY, 2026-2032 (USD MILLION)

- TABLE 203 ROW: CONTROL VALVE MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 204 ROW: CONTROL VALVE MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 205 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN CONTROL VALVE MARKET, JANUARY 2022-MAY 2026

- TABLE 206 CONTROL VALVE MARKET: DEGREE OF COMPETITION, 2025

- TABLE 207 CONTROL VALVE MARKET: REGION FOOTPRINT

- TABLE 208 CONTROL VALVE MARKET: TYPE FOOTPRINT

- TABLE 209 CONTROL VALVE MARKET: COMPONENT FOOTPRINT

- TABLE 210 CONTROL VALVE MARKET: INDUSTRY FOOTPRINT

- TABLE 211 CONTROL VALVE MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 212 CONTROL VALVE MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 213 CONTROL VALVE MARKET: PRODUCT LAUNCHES/EXPANSIONS, JANUARY 2022-MAY 2026

- TABLE 214 CONTROL VALVE MARKET: DEALS, JANUARY 2022-MAY 2026

- TABLE 215 CONTROL VALVE MARKET: EXPANSIONS, JANUARY 2022-MAY 2026

- TABLE 216 EMERSON ELECTRIC CO.: COMPANY OVERVIEW

- TABLE 217 EMERSON ELECTRIC CO.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 218 EMERSON ELECTRIC CO.: PRODUCT LAUNCHES/EXPANSIONS

- TABLE 219 FLOWSERVE CORPORATION: COMPANY OVERVIEW

- TABLE 220 FLOWSERVE CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 221 FLOWSERVE CORPORATION: PRODUCT LAUNCHES/EXPANSIONS

- TABLE 222 FLOWSERVE CORPORATION: DEALS

- TABLE 223 SLB: COMPANY OVERVIEW

- TABLE 224 SLB: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 225 SLB: EXPANSIONS

- TABLE 226 IMI: COMPANY OVERVIEW

- TABLE 227 IMI: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 228 IMI: PRODUCT LAUNCHES/EXPANSIONS

- TABLE 229 CRANE HOLDINGS, CO.: COMPANY OVERVIEW

- TABLE 230 CRANE HOLDINGS, CO.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 231 CRANE HOLDINGS, CO.: DEALS

- TABLE 232 KITZ CORPORATION: COMPANY OVERVIEW

- TABLE 233 KITZ CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 234 KITZ CORPORATION: PRODUCT LAUNCHES/EXPANSIONS

- TABLE 235 KITZ CORPORATION: DEALS

- TABLE 236 KITZ CORPORATION: EXPANSIONS

- TABLE 237 CURTISS-WRIGHT CORPORATION: COMPANY OVERVIEW

- TABLE 238 CURTISS-WRIGHT CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 239 VALMET: COMPANY OVERVIEW

- TABLE 240 VALMET: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 241 VALMET: PRODUCT LAUNCHES/EXPANSIONS

- TABLE 242 VALMET: DEALS

- TABLE 243 BAKER HUGHES COMPANY: COMPANY OVERVIEW

- TABLE 244 BAKER HUGHES COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 245 BAKER HUGHES COMPANY: PRODUCT LAUNCHES/EXPANSIONS

- TABLE 246 BAKER HUGHES COMPANY: DEALS

- TABLE 247 KSB SE & CO. KGAA: COMPANY OVERVIEW

- TABLE 248 KSB SE & CO. KGAA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 249 KSB SE & CO. KGAA: PRODUCT LAUNCHES/EXPANSIONS

- TABLE 250 BRAY INTERNATIONAL: COMPANY OVERVIEW

- TABLE 251 BRAY INTERNATIONAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 252 BRAY INTERNATIONAL: DEALS

- TABLE 253 AVK HOLDING A/S: COMPANY OVERVIEW

- TABLE 254 AVK HOLDING A/S: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 255 AVK HOLDING A/S: DEALS

- TABLE 256 CIRCOR INTERNATIONAL, INC.: COMPANY OVERVIEW

- TABLE 257 CIRCOR INTERNATIONAL, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 258 CIRCOR INTERNATIONAL, INC.: DEALS

- TABLE 259 SAMSON AG: COMPANY OVERVIEW

- TABLE 260 HONEYWELL INTERNATIONAL INC.: COMPANY OVERVIEW

- TABLE 261 NEWAY VALVE: COMPANY OVERVIEW

- TABLE 262 ALFA LAVAL: COMPANY OVERVIEW

- TABLE 263 SPIRAX GROUP PLC: COMPANY OVERVIEW

- TABLE 264 WATTS.: COMPANY OVERVIEW

- TABLE 265 PARKER HANNIFIN CORP: COMPANY OVERVIEW

- TABLE 266 THE WEIR GROUP PLC: COMPANY OVERVIEW

- TABLE 267 HAM-LET GROUP: COMPANY OVERVIEW

- TABLE 268 AVCON CONTROLS PVT LTD.: COMPANY OVERVIEW

- TABLE 269 VELAN ABV S.R.L.: COMPANY OVERVIEW

- TABLE 270 TRILLIUM FLOW TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 271 MAJOR SECONDARY SOURCES

- TABLE 272 PRIMARY INTERVIEW PARTICIPANTS

- TABLE 273 CONTROL VALVE MARKET: RISK ANALYSIS

List of Figures

- FIGURE 1 CONTROL VALVE MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 CONTROL VALVE MARKET: DURATION CONSIDERED

- FIGURE 3 CONTROL VALVE MARKET SCENARIO

- FIGURE 4 GLOBAL CONTROL VALVE MARKET SIZE, 2022-2032

- FIGURE 5 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN CONTROL VALVE MARKET, 2022-2026

- FIGURE 6 DISRUPTIONS INFLUENCING GROWTH OF CONTROL VALVE MARKET

- FIGURE 7 HIGH-GROWTH SEGMENTS IN CONTROL VALVE MARKET, 2026-2032

- FIGURE 8 ASIA PACIFIC TO REGISTER HIGHEST CAGR IN CONTROL VALVE MARKET, IN TERMS OF VALUE, DURING FORECAST PERIOD

- FIGURE 9 RISING AUTOMATION AND RENEWABLE ENERGY INFRASTRUCTURE DEVELOPMENT TO DRIVE CONTROL VALVE MARKET

- FIGURE 10 ACTUATORS SEGMENT TO HOLD LARGEST SHARE OF CONTROL VALVE MARKET IN 2026

- FIGURE 11 ALLOY SEGMENT TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 12 ROTARY VALVES SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE IN 2032

- FIGURE 13 UP TO 1" SEGMENT TO EXHIBIT HIGHEST CAGR BETWEEN 2026 AND 2032

- FIGURE 14 OIL & GAS SEGMENT TO CAPTURE LARGEST MARKET SHARE IN 2026

- FIGURE 15 ASIA PACIFIC TO HOLD LARGEST SHARE OF CONTROL VALVE MARKET IN 2032

- FIGURE 16 SOUTH KOREA TO RECORD HIGHEST CAGR IN GLOBAL CONTROL VALVE MARKET DURING FORECAST PERIOD

- FIGURE 17 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 18 IMPACT ANALYSIS: DRIVERS

- FIGURE 19 IMPACT ANALYSIS: RESTRAINTS

- FIGURE 20 IMPACT ANALYSIS: OPPORTUNITIES

- FIGURE 21 IMPACT ANALYSIS: CHALLENGES

- FIGURE 22 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 23 CONTROL VALVE MARKET : SUPPLY CHAIN ANALYSIS

- FIGURE 24 CONTROL VALVE ECOSYSTEM

- FIGURE 25 IMPORT DATA FOR HS CODE 848110-COMPLIANT PRODUCTS FOR TOP FIVE COUNTRIES, 2021-2025

- FIGURE 26 EXPORT DATA FOR HS CODE 848110-COMPLIANT PRODUCTS FOR TOP FIVE COUNTRIES, 2021-2025

- FIGURE 27 TRENDS/DISRUPTIONS INFLUENCING CUSTOMER BUSINESS

- FIGURE 28 INVESTMENT AND FUNDING SCENARIO, 2021-2025

- FIGURE 29 PATENTS APPLIED AND GRANTED, 2016-2025

- FIGURE 30 DECISION-MAKING FACTORS CONSIDERED WHILE SELECTING CONTROL VALVES

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE INDUSTRIES

- FIGURE 32 KEY BUYING CRITERIA FOR TOP THREE INDUSTRIES

- FIGURE 33 CONTROL VALVE ADOPTION BARRIERS AND INTERNAL CHALLENGES

- FIGURE 34 CONTROL VALVE MEDIA TYPES

- FIGURE 35 CONTROL VALVE MARKET, BY PRESSURE RANGE

- FIGURE 36 CONTROL VALVE MARKET, BY TYPE

- FIGURE 37 ROTARY VALVES SEGMENT TO RECORD HIGHER CAGR BETWEEN 2026 AND 2032

- FIGURE 38 CONTROL VALVE MARKET, BY COMPONENT

- FIGURE 39 ACTUATORS SEGMENT TO DOMINATE CONTROL VALVE MARKET BETWEEN 2026 AND 2032

- FIGURE 40 CONTROL VALVE MARKET, BY MATERIAL

- FIGURE 41 STAINLESS STEEL SEGMENT TO HOLD LARGEST MARKET SHARE IN 2032

- FIGURE 42 CONTROL VALVE MARKET, BY SIZE

- FIGURE 43 >6-25" SEGMENT TO HOLD LARGEST SHARE OF CONTROL VALVE MARKET IN 2032

- FIGURE 44 CONTROL VALVE MARKET, BY INDUSTRY

- FIGURE 45 OIL & GAS SEGMENT TO DOMINATE CONTROL VALVE MARKET FROM 2026 TO 2032

- FIGURE 46 CONTROL VALVE MARKET, BY REGION

- FIGURE 47 ASIA PACIFIC TO REGISTER HIGHEST CAGR IN CONTROL VALVE MARKET DURING FORECAST PERIOD

- FIGURE 48 NORTH AMERICA: CONTROL VALVE MARKET SNAPSHOT

- FIGURE 49 EUROPE: CONTROL VALVE MARKET SNAPSHOT

- FIGURE 50 ASIA PACIFIC: CONTROL VALVE MARKET SNAPSHOT

- FIGURE 51 CONTROL VALVE MARKET: REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2021-2025

- FIGURE 52 MARKET SHARE ANALYSIS OF COMPANIES OFFERING CONTROL VALVES, 2025

- FIGURE 53 COMPANY VALUATION

- FIGURE 54 FINANCIAL METRICS (EV/EBITDA)

- FIGURE 55 BRAND COMPARISON

- FIGURE 56 CONTROL VALVE MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 57 CONTROL VALVE MARKET: COMPANY FOOTPRINT

- FIGURE 58 CONTROL VALVE MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2025

- FIGURE 59 EMERSON ELECTRIC CO.: COMPANY SNAPSHOT

- FIGURE 60 FLOWSERVE CORPORATION: COMPANY SNAPSHOT

- FIGURE 61 SLB: COMPANY SNAPSHOT

- FIGURE 62 IMI: COMPANY SNAPSHOT

- FIGURE 63 CRANE HOLDINGS, CO.: COMPANY SNAPSHOT

- FIGURE 64 KITZ CORPORATION: COMPANY SNAPSHOT

- FIGURE 65 CURTISS-WRIGHT CORPORATION: COMPANY SNAPSHOT

- FIGURE 66 VALMET: COMPANY SNAPSHOT

- FIGURE 67 BAKER HUGHES COMPANY: COMPANY SNAPSHOT

- FIGURE 68 KSB SE & CO. KGAA: COMPANY SNAPSHOT

- FIGURE 69 CONTROL VALVE MARKET: RESEARCH DESIGN

- FIGURE 70 DATA CAPTURED FROM SECONDARY SOURCES

- FIGURE 71 DATA CAPTURED FROM PRIMARY SOURCES

- FIGURE 72 BREAKDOWN OF PRIMARY INTERVIEWS, BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 73 CORE FINDINGS FROM INDUSTRY EXPERTS

- FIGURE 74 CONTROL VALVE MARKET: RESEARCH APPROACH

- FIGURE 75 CONTROL VALVE MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- FIGURE 76 CONTROL VALVE MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 77 CONTROL VALVE MARKET SIZE ESTIMATION (SUPPLY SIDE)

- FIGURE 78 CONTROL VALVE MARKET: DATA TRIANGULATION

- FIGURE 79 CONTROL VALVE MARKET: RESEARCH ASSUMPTIONS

夾管閥市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、材料、應用、地區和競爭格局分類,2021-2031年

夾管閥市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、材料、應用、地區和競爭格局分類,2021-2031年 控制閥市場報告:按類型、技術、組件、材質、最終用途行業和地區分類(2026-2034 年)

控制閥市場報告:按類型、技術、組件、材質、最終用途行業和地區分類(2026-2034 年) 工業控制閥市場規模及預測(2021-2034),全球及區域佔有率、趨勢及成長機會分析報告:按類型、尺寸、等級及產業分類

工業控制閥市場規模及預測(2021-2034),全球及區域佔有率、趨勢及成長機會分析報告:按類型、尺寸、等級及產業分類 控制閥市場:2026-2032年全球市場預測(依閥類型、材質、驅動技術、組件、閥門尺寸、驅動方式、應用、終端用戶產業及銷售管道)

控制閥市場:2026-2032年全球市場預測(依閥類型、材質、驅動技術、組件、閥門尺寸、驅動方式、應用、終端用戶產業及銷售管道) 夾管閥市場機會、成長要素、產業趨勢分析及2026-2035年預測

夾管閥市場機會、成長要素、產業趨勢分析及2026-2035年預測 2026年移動式機械主控閥全球市場報告模組化流量控制閥市場:按類型、操作方式、材料、連接方式、尺寸和最終用途行業分類,全球預測,2026-2032年選擇閥市場:按操作方式、類型、尺寸、材料和產業分類,全球預測(2026-2032年)手動槓桿閥市場按材質、連接類型、驅動類型、壓力等級和應用分類-全球預測,2026-2032年

2026年移動式機械主控閥全球市場報告模組化流量控制閥市場:按類型、操作方式、材料、連接方式、尺寸和最終用途行業分類,全球預測,2026-2032年選擇閥市場:按操作方式、類型、尺寸、材料和產業分類,全球預測(2026-2032年)手動槓桿閥市場按材質、連接類型、驅動類型、壓力等級和應用分類-全球預測,2026-2032年 控制閥市場:策略性洞察與預測(2026-2031 年)

控制閥市場:策略性洞察與預測(2026-2031 年)