|

市場調查報告書

商品編碼

2064086

全球商用電動車市場:按車輛類型、推進系統、電池類型、功率輸出、續航里程、最終用途、組件、電池容量和地區分類-預測至2033年Electric Commercial Vehicle Market by Vehicle Type (LCVs, Trucks, Buses), Propulsion (BEV, PHEV), Battery Type (NMC, LFP), End Use (Last Mile Delivery, Refuse, Others), Battery Capacity, Power Output, Component, and Region - Global Forecast to 2033 |

||||||

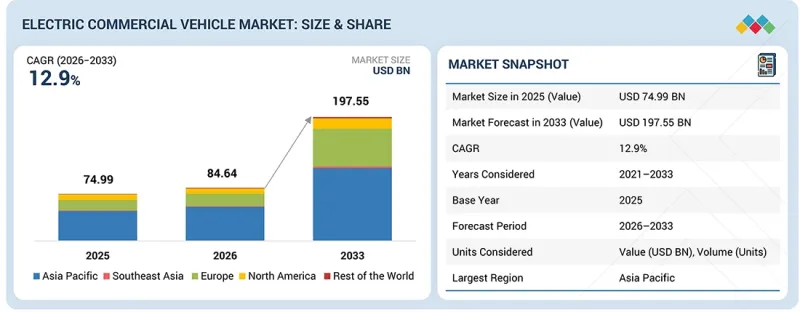

預計商用電動車市場將從 2026 年的 846.4 億美元成長到 2033 年的 1,975.5 億美元,複合年成長率為 12.9%。

這一成長是由電子商務配送網路的快速擴張、對節能型貨運需求的增加以及對商用車輛充電基礎設施投資的增加所推動的。

| 調查範圍 | |

|---|---|

| 調查期 | 2026-2033 |

| 基準年 | 2025 |

| 預測期 | 2026-2033 |

| 目標單元 | 10億美元 |

| 部分 | 按車輛類型、推進系統、電池類型、功率輸出、續航里程、最終用途、組件、電池容量和地區分類。 |

| 目標區域 | 亞太地區、東南亞、北美、歐洲及世界其他地區 |

政府對淨零排放、零排放貨運目標以及政策主導的車輛電氣化計畫的承諾,正在進一步加速全部區域市場的普及。車輛營運商優先考慮降低燃料成本、減少排放氣體和提高長期營運效率,這推動了電動卡車、巴士和輕型商用車的廣泛應用。高能量密度電池系統、再生煞車技術和智慧溫度控管技術的進步,正在提高車輛在高利用率運作工況下的續航里程和性能。此外,車庫充電基礎設施和兆瓦級充電系統的擴展,正在減少運作,並加速大規模車隊轉型為電氣化。

“磷酸鐵鋰電池因其熱穩定性高、電池壽命長、成本低廉等優點,將推動市場需求。”

由於磷酸鐵鋰電池系統具有熱穩定性高、循環壽命長、成本低等優勢,在高運轉率車隊營運中正迅速獲得商用電動車市場的青睞。電動巴士、卡車和輕型商用車對能夠應對頻繁充電循環、重負載容量和長時間日常使用的電池系統的需求日益成長,這使得磷酸鋰電池的化學成分成為商務傳輸應用的理想選擇。這種電池結構增強了熱安全性,降低了熱失控風險,即使在嚴苛的運作條件下也能確保穩定的性能,從而推動了其在物流、礦業和公共交通車隊中的應用。與快速充電系統、能量回收煞車和高壓驅動系統的兼容性進一步提高了效率和車輛運轉率。包括寧德時代在內的電池供應商正與汽車製造商簽訂長期契約,供應具成本效益的磷酸鐵鋰電池系統,進一步推進商用車隊的電氣化,並有助於降低總體擁有成本 (TCO)。例如,寧德時代正在拓展與宇通、一汽集團等商用車製造商的戰略電池供應夥伴關係,並推進高容量磷酸鐵鋰電池平台在電動客車和重型卡車領域的應用。比亞迪和宇通也在各自的高容量磷酸鐵鋰電池平台上整合先進的電池管理系統和預測性維護功能,以提高營運效率。例如,宇通和比亞迪已簽署契約,向義大利巴里和塔蘭托兩座城市供應電動客車。

「60-120千瓦時的電池正在推動市場發展,這主要得益於市場對電動輕型商用車(LCV)的高需求。”

隨著電動輕型商用車 (LCV) 在城市物流、最後一公里配送和本地運輸等領域的日益普及,60 kWh 至 120 kWh 的電池容量區間佔據了相當大的市場佔有率。此容量範圍在續航里程、有效載荷、充電時間和車輛成本之間實現了最佳平衡,使其成為高運轉率商用輕型車輛車隊營運的理想選擇。車隊營運商正擴大採用配備 60 kWh 至 120 kWh 電池組的電動輕型商用車 (LCV),以降低營運和維護成本,同時滿足日常配送、倉儲和本地貨運的需求。磷酸鐵鋰電池化學、再生煞車系統和智慧電池溫度控管技術的進步正在提升該容量區間的營運效率、電池壽命和能源利用效率。隨著電動車電池價格逐年下降,各公司紛紛推出配備此容量範圍電池的 LCV。例如,比亞迪和一汽正在擴大部署這一容量範圍內的輕型商用車,以支援互聯車隊運營,並將遠端資訊處理、預測性維護和路線最佳化技術整合到物流和都市區配送應用中。

“電池製造的擴張和智慧城市交通項目的推進將加速亞太地區商用電動車的普及。”

亞太地區商用電動車市場正蓬勃發展,這主要得益於電池製造的快速成長、智慧城市交通項目的增加以及工業和物流運輸網路的電氣化。該地區各國政府正透過本地生產政策、車隊電氣化計畫以及對換電和超快充電基礎設施的投資,大力支持電動車的普及。隨著營運商致力於降低營運成本和提高能源效率,對電動公車和城市配送車隊的需求也在不斷成長。比亞迪、徐工集團、宇通和塔塔汽車等公司正在加強在亞太地區生產和部署整合先進電池系統和智慧車輛管理技術的電動卡車和公車。例如,比亞迪已擴大在東南亞的合作夥伴關係,以部署用於城市交通和物流電氣化的電動公車和卡車。宇通已與哈薩克斯坦和烏茲別克斯坦簽署電動公車供應契約,以支持公共交通電氣化舉措。

商用電動車市場由徐工集團(中國)、三一集團(中國)、一汽集團(中國)、中國重汽(中國)及宇通客車(中國)等中國企業主導。這些企業採取多種策略來維持其市場地位,主要策略包括推出新產品、建立合作夥伴關係和拓展業務。我們分析了這些策略,以了解每家企業的市場定位。製造商致力於透過提供先進且多元化的解決方案來滿足不斷變化的法規和消費者需求,從而保持其在市場中的戰略地位。

調查範圍:

本報告按車輛類型(輕型商用車、卡車、巴士)、驅動系統(純電動車、插電式混合動力車)、電池類型(鎳鎘電池、磷酸鐵鋰電池)、電池容量(低於60千瓦時、60-120度、電池類型(鎳鎘電池、磷酸鐵鋰電池)、電池容量(低於60千瓦時、60-120千瓦時、121-200度、功率輸出(低於100千瓦、100-250千瓦、高於250千瓦)、續航里程(150英里、151-300英里、高於300英里)、應用領域(末端配送、現場服務、送貨服務、長途運輸、垃圾車)、零部件以及地區(亞太地區、東南亞地區分析。報告還涵蓋了商用電動車市場生態系統中的競爭格局和主要參與者的公司概況。

除了對市場主要參與者進行詳細的競爭分析外,本研究還涵蓋了每家公司的企業概況、有關其產品和服務的關鍵觀察、近期趨勢和主要市場策略。

- 本報告透過提供者用電動車市場生態系統及其細分市場最準確的收入估算,幫助商用電動車市場的市場領導和新參與企業。

- 本報告幫助相關人員了解競爭格局,獲得更深入的見解,最佳化業務定位,並制定合適的打入市場策略。

- 此外,該報告有助於相關人員了解市場趨勢,並獲取有關關鍵市場促進因素、限制因素、挑戰和機會的資訊。

本報告深入分析了以下幾點:

- 關鍵促進因素(電池技術的進步、電子商務和物流的成長)、阻礙因素(負載容量限制和低利用率、對電池在嚴苛運作循環、快速充電和極端底盤條件下劣化的擔憂)、機遇(為高運轉率商用車隊運營開發電池更換、超快速充電和能源管理生態系統)、挑戰(在重型商用應用中實現高能量密度而不影響負載容量、底盤整合、車輛耐久性和動力傳動系統效率)。

- 產品開發與創新:深入了解商用電動車市場的未來技術、研發活動與新產品發表。

- 市場發展:盈利市場的全面資訊-本報告分析了各個地區的商用電動車市場。

- 市場多元化:提供有關商用電動車市場的新產品、未開發市場、最新趨勢和投資的全面資訊。

- 競爭評估:對商用電動車市場主要參與者的市場排名、成長策略和服務產品進行詳細評估,包括徐工集團(中國)、三一集團(中國)、一汽集團(中國)、中國重汽(中國)和宇通客車(中國)。

目錄

第1章:引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 未滿足的需求和未開發的領域

第5章 產業趨勢

- 總體經濟指標

- 供應鏈分析

- 生態系測繪

- 價格分析

- 貿易分析

- 2026-2027 年主要會議和活動

- 影響客戶業務的趨勢與干擾因素

- 投資情境

- 案例研究分析

- 對經營模式機會的洞察

- 以色列-伊朗戰爭的影響

- 歐盟-印度貿易協定的影響分析

第6章:OEM和供應商分析

- 電動巴士

- 電動卡車

- 電動輕型商用車

第7章 商用電動車市場的技術進步、人工智慧影響、專利、創新與未來應用

- 技術分析

- 技術/產品藍圖

- 專利分析

- 未來應用

- 人工智慧/生成式人工智慧對商用電動車市場的影響

第8章永續性和監管情勢

- 監理情勢

- 對永續性的承諾

- 對永續性和監管政策舉措的影響

- 認證、標籤檢視和環境標準

第9章:顧客趨勢與購買行為

- 決策流程

- 主要相關人員和採購標準

- 實施障礙和內部挑戰

- 終端用戶的各種未滿足需求

第10章:商用電動車市場(依車輛類型分類)

- 輕型商用車

- 追蹤

- 公車

- 主要行業趨勢

第11章:商用電動車市場(依動力系統分類)

- 電池式電動車(BEV)

- 插電式混合動力車(PHEV)

- 主要行業趨勢

第12章:商用電動車市場(依電池類型分類)

- NMC

- LFP

- 主要行業趨勢

第13章:商用電動車市場(依功率輸出)

- 小於100千瓦

- 100~250kW

- 250度或以上

- 主要行業趨勢

第14章:商用電動車市場(以續航里程分類)

- 不到150英里

- 151-300英里

- 超過300英里

- 主要行業趨勢

第15章:商用電動車市場(依最終用途分類)

- 最後一公里配送

- 現場服務

- 送貨服務

- 長途

- 垃圾車

- 主要行業趨勢

第16章:商用電動車市場(按零件分類)

- 電池組

- 車用充電器

- 電動機

- 逆變器

- 直流-直流轉換器

第17章:商用電動車市場(以電池容量分類)

- 少於60千瓦時

- 60~120kWh

- 121~200kWh

- 201~300kWh

- 301~500kWh

- 500度或以上

- 主要行業趨勢

第18章:商用電動車市場(依地區分類)

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 泰國

- 印尼

- 菲律賓

- 馬來西亞

- 越南

- 新加坡

- 澳洲

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 法國

- 德國

- 西班牙

- 奧地利

- 挪威

- 瑞典

- 荷蘭

- 英國

- 義大利

- 比利時

- 丹麥

- 瑞士

- 其他地區

- 俄羅斯

- 巴西

- 土耳其

第19章 競爭情勢

- 概述

- 主要參與企業的策略/優勢

- 2025年市佔率分析

- 2021-2025年收入分析

- 企業估值和財務指標

- 品牌/產品對比

- 企業估值矩陣:主要公司,2025 年

- 公司估值矩陣:新創企業/中小企業,2025 年

- 競爭格局

第20章:公司簡介

- 中國主要參與企業

- XCMG GLOBAL

- SANY GROUP

- FAW GROUP

- CNHTC

- YUTONG BUS CO., LTD.

- BEIJING AUTOMOTIVE GROUP CO., LTD.

- DONGFENG MOTOR CORPORATION

- BYD

- 中國以外的主要參與企業

- DAIMLER GROUP AG

- AB VOLVO

- FORD MOTOR COMPANY

- TESLA, INC.

- HYUNDAI MOTOR COMPANY

- NFI GROUP

- 其他公司

- TATA MOTORS LIMITED

- WORKHORSE GROUP

- VDL GROEP

- ASHOK LEYLAND

- ISUZU MOTORS LTD.

- IRIZAR GROUP

- IVECO

- XOS TRUCKS INC.

- MAN SE

- GOLDEN DRAGON

- ZENITH MOTORS

- FIRST BUS(WRIGHTBUS)

第21章調查方法

第22章附錄

The electric commercial vehicle market is projected to grow from USD 84.64 billion in 2026 to USD 197.55 billion by 2033, at a CAGR of 12.9%. Growth is being supported by the rapid expansion of e-commerce delivery networks, increasing demand for energy-efficient freight transportation, and rising investments in charging infrastructure for commercial fleets.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Billion |

| Segments | by Vehicle Type, Propulsion, Battery Type, End Use, Range, Battery Capacity, Power Output, Component, and Region |

| Regions covered | Asia Pacific, Southeast Asia, North America, Europe, Rest of the World |

Government net-zero commitments, zero-emission freight targets, and policy-driven fleet electrification programs are further accelerating market adoption across key regions. Fleet operators are prioritizing reduced fuel costs, lower emissions, and improved long-term operational efficiency, supporting wider deployment of electric trucks, buses, and light commercial vehicles. Advancements in high-energy-density battery systems, regenerative braking technologies, and intelligent thermal management are enhancing vehicle range and performance across high-utilization duty cycles. Expansion of depot charging infrastructure, megawatt charging systems, is also reducing operational downtime and enabling faster transition to large-scale fleet electrification.

"LFP batteries to lead market demand due to high thermal stability, long battery life cycle, and availability at lower cost"

LFP battery systems are witnessing strong adoption in the electric commercial vehicle market due to their high thermal stability, longer cycle life, and lower cost advantages for high-utilization fleet operations. Electric buses, trucks, and light commercial vehicles increasingly require battery systems capable of supporting frequent charging cycles, heavy payload operations, and extended daily vehicle usage, making LFP chemistry highly suitable for commercial transportation applications. The battery architecture improves thermal safety, reduces risk of thermal runaway, and ensures stable performance under demanding operating conditions, supporting deployment across logistics, mining, and public transit fleets. Compatibility with fast-charging systems, regenerative braking, and high-voltage drivetrains is further enhancing efficiency and fleet uptime. Companies such as CATL, along with other battery suppliers, are securing long-term contracts with automakers to supply cost-effective LFP battery systems, supporting wider commercial fleet electrification and lowering the total cost of ownership. For instance, CATL expanded strategic battery supply partnerships with commercial vehicle manufacturers, including Yutong and FAW GROUP, for deployment of high-capacity LFP battery platforms in electric buses and heavy-duty trucks. BYD and Yutong are also integrating high-capacity LFP platforms with advanced battery management systems and predictive diagnostics to improve operational efficiency. For instance, Yutong and BYD signed a contract to supply electric buses to the Italian cities of Bari and Taranto.

"60-120 kWh batteries to lead market with high demand in electric LCVs"

The 60 kWh to 120 kWh battery capacity segment accounts for a major share due to the increasing deployment of electric light commercial vehicles in urban logistics, last-mile delivery, and regional transportation applications. This battery capacity range provides an optimal balance between driving range, payload capability, charging time, and vehicle cost, making it highly suitable for high-utilization commercial light-duty fleet operations. Fleet operators are increasingly adopting electric LCVs equipped with 60 kWh to 120 kWh battery packs to support daily delivery cycles, warehouse distribution, and intra-city freight movement while reducing operating costs and maintenance costs. Advancements in LFP battery chemistry, regenerative braking systems, and intelligent battery thermal management are improving operational efficiency, battery lifecycle, and energy utilization in this segment. Companies are providing LCVs with this battery range, as prices of EV batteries decrease year on year. For instance, BYD and FAW are increasingly deploying LCV vehicles within this capacity range to support connected fleet operations integrated with telematics, predictive maintenance, and route optimization technologies for logistics and urban delivery applications.

"Battery Manufacturing Expansion and Smart Urban Mobility Projects Accelerating Electric Commercial Vehicle Adoption in Asia Pacific"

The Asia Pacific electric commercial vehicle market is expanding due to rapid battery manufacturing expansion, increasing smart urban mobility projects, and rising electrification of industrial and logistics transportation networks. Governments across the region are supporting electric commercial vehicle deployment through localization policies, fleet electrification programs, and investments in battery swapping and ultra-fast charging infrastructure. Demand is increasing for electric buses and urban delivery fleets as operators focus on reducing operating costs and improving energy efficiency. Companies such as BYD, XCMG GLOBAL, Yutong, and Tata Motors are strengthening regional production and deployment of electric trucks and buses integrated with advanced battery systems and intelligent fleet technologies. For instance, BYD expanded electric bus and truck deployment partnerships across Southeast Asia for urban transit and logistics electrification projects. Yutong secured electric bus supply agreements in Kazakhstan and Uzbekistan to support public transportation electrification initiatives.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: Tier 1- 50%, OEMs - 40%, Others - 10%

- By Designation: CXOs - 20%, Directors - 30%, Others - 50%

- By Country: Asia Pacific - 35%, Southeast Asia 25%, North America - 15%, Europe - 20% and Rest of the World - 5%

The electric commercial vehicle market is dominated by Chinese players, such as XCMG GLOBAL (China), SANY GROUP (China), FAW Group (China), CNHTC (China), and Yutong Bus Co., Ltd. (China). These players have been adopting various strategies to sustain their positions in the market. Major strategies adopted are product launches, deals, and expansions. These strategies have been analyzed to understand the positions of these companies in the market. Manufacturers focus on maintaining their strategic position in the market by offering advanced, various solutions to meet evolving regulatory and consumer demands.

Research Coverage:

The report covers the electric commercial vehicle market by Vehicle Type (LCVs, Trucks, Buses), Propulsion (BEV, PHEV), Battery Type (NMC, LFP), Battery Capacity (less than 60, 60-120 kwh, 121-200 kWh, 201-300 kWh, 301-500 kWh, 501-1,000 kWh), Power Output (less than 100 kw, 100-250 kw, above 250 kw), Range (150 miles, 151-300 miles, above 300), End Use (Last-mile Delivery, Field Services, Distribution Services, Long-haul Transportation, Refuse Trucks), Component, and Region (Asia Pacific, Southeast Asia, Europe, North America, and Rest of the World). It covers the competitive landscape and company profiles of the major players in the electric commercial vehicle market ecosystem.

The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- This report will help market leaders/new entrants in this market with information on the closest approximations of revenue numbers for the electric commercial vehicle market ecosystem and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies.

- This report will also help stakeholders understand the market's pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (Advancements in battery technology, Growth in e-commerce and logistics), restraints (Payload limitations and inadequate utilization, Battery degradation concerns under intensive duty cycles, fast-charging, and extreme temperature conditions), opportunities (Development of battery swapping, ultra-fast charging, and energy management ecosystems for high-utilization commercial fleet operations), and challenges (Achieving high energy density without compromising payload capacity, chassis integration, vehicle durability, and drivetrain efficiency in heavy commercial applications)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the electric commercial vehicle market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the electric commercial vehicle market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the electric commercial vehicle market.

- Competitive Assessment: In-depth assessment of market ranking, growth strategies, and service offerings of leading players like XCMG GLOBAL (China), SANY GROUP (China), FAW Group (China), CNHTC (China), and Yutong Bus Co. Ltd. (China) in the electric commercial vehicle market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING ELECTRIC COMMERCIAL VEHICLE MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ELECTRIC COMMERCIAL VEHICLE MARKET

- 3.2 ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE

- 3.3 ELECTRIC COMMERCIAL VEHICLE MARKET, BY PROPULSION

- 3.4 ELECTRIC COMMERCIAL VEHICLE MARKET, BY BATTERY TYPE

- 3.5 ELECTRIC COMMERCIAL VEHICLE MARKET, BY RANGE

- 3.6 ELECTRIC COMMERCIAL VEHICLE MARKET, BY BATTERY CAPACITY

- 3.7 ELECTRIC COMMERCIAL VEHICLE MARKET, BY POWER OUTPUT

- 3.8 ELECTRIC COMMERCIAL VEHICLE MARKET, BY END USE

- 3.9 ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Advancements in battery technology

- 4.2.1.2 Growth in e-commerce and logistics

- 4.2.2 RESTRAINTS

- 4.2.2.1 Payload limitations and inadequate utilization

- 4.2.2.2 Short battery life

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Development of battery swapping and ultra-fast charging

- 4.2.3.2 Energy management ecosystems for high-utilization commercial fleet operations

- 4.2.4 CHALLENGES

- 4.2.4.1 Achieving high energy density without compromising payload capacity

- 4.2.4.2 Chassis integration, vehicle durability, and drivetrain efficiency in heavy commercial applications

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 RELIABLE PERFORMANCE UNDER REAL WORLD CONDITIONS

- 4.3.2 SIMPLIFIED CHARGING AND ENERGY MANAGEMENT IN DEPOTS

- 4.3.3 LIMITED ECOSYSTEM INTEGRATION AND DATA USAGE

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN ELECTRIC COMMERCIAL VEHICLE MARKET

- 5.1.4 TRENDS IN GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.2 SUPPLY CHAIN ANALYSIS

- 5.3 ECOSYSTEM MAPPING

- 5.3.1 CHARGING INFRASTRUCTURE PROVIDERS

- 5.3.2 TIER II SUPPLIERS

- 5.3.3 TIER I SUPPLIERS

- 5.3.4 RAW MATERIAL PROVIDERS

- 5.3.5 BATTERY MANUFACTURERS

- 5.3.6 OEMS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING TREND (ASP) OF KEY PLAYERS, BY ELECTRIC TRUCK VEHICLE TYPE, 2025

- 5.4.2 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT SCENARIO (HS CODE 8704)

- 5.5.2 EXPORT SCENARIO (HS CODE 8704)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 ASSESSMENT OF INVESTMENT IN ELECTRIC BUSES

- 5.9.2 USER EXPERIENCE OF BATTERY ELECTRIC TRUCKS IN NORWAY

- 5.9.3 ELECTRIC VEHICLE FLEETS FOR PUBLIC SECTOR IN VERMONT

- 5.9.4 ASSESSMENT OF ELECTRIC BUS DEPLOYMENT IN PUBLIC TRANSPORTATION

- 5.9.5 ASSESSMENT OF ELECTRIC PICKUP TRUCK DEPLOYMENT FOR LOGISTICS OPERATIONS

- 5.10 INSIGHTS INTO BUSINESS MODEL OPPORTUNITIES

- 5.10.1 FLEET OPERATORS

- 5.10.2 INSURANCE COMPANIES

- 5.10.3 MOBILITY PLATFORMS

- 5.11 IMPACT OF ISRAEL-IRAN WAR

- 5.11.1 INTRODUCTION

- 5.11.2 ENERGY MARKET DISRUPTION

- 5.11.3 OPERATING COST IMPACT

- 5.11.4 MARKET DEMAND SHIFT

- 5.11.5 SUPPLY CHAIN AND LOCALIZATION IMPACT

- 5.11.6 STRATEGIC MARKET OUTLOOK

- 5.12 EU-INDIA TRADE DEAL IMPACT ANALYSIS

- 5.12.1 INTRODUCTION

- 5.12.2 EU TARIFFS

6 OEM AND SUPPLIER ANALYSIS

- 6.1 INTRODUCTION

- 6.2 ELECTRIC BUS

- 6.2.1 TOTAL COST OF OWNERSHIP (TCO) ANALYSIS: ICE VS. ELECTRIC BUS

- 6.2.2 ELECTRIC BUS DRIVE MOTOR SUPPLIERS, BY OEM AND REGION

- 6.2.2.1 Asia Pacific: Drive motor suppliers

- 6.2.2.2 Europe: Drive motor suppliers

- 6.2.2.3 North America: Drive motor suppliers

- 6.2.3 ELECTRIC BUS BATTERY CELL SUPPLIERS, BY OEM AND REGION

- 6.2.3.1 Asia Pacific: Battery cell suppliers

- 6.2.3.2 Europe: Battery cell suppliers

- 6.2.3.3 North America: Battery cell suppliers

- 6.3 ELECTRIC TRUCK

- 6.3.1 TCO ANALYSIS: ICE VS. ELECTRIC

- 6.3.2 ELECTRIC TRUCK DRIVE MOTOR SUPPLIERS, BY OEM AND REGION

- 6.3.2.1 Asia Pacific: Drive motor suppliers

- 6.3.2.2 Europe: Drive motor suppliers

- 6.3.2.3 North America: Drive motor suppliers

- 6.3.3 ELECTRIC TRUCK BATTERY CELL SUPPLIERS, BY OEM AND REGION

- 6.3.3.1 Asia Pacific: Battery cell suppliers

- 6.3.3.2 Europe: Battery cell suppliers

- 6.3.3.3 North America: Battery cell suppliers

- 6.4 ELECTRIC LCV

- 6.4.1 TCO ANALYSIS: ICE VS. ELECTRIC

- 6.4.2 ELECTRIC LCV BATTERY CELL SUPPLIERS, BY OEM AND REGION

- 6.4.2.1 Asia Pacific: Battery cell suppliers

- 6.4.2.2 Europe: Battery cell suppliers

- 6.4.2.3 North America: Battery cell suppliers

7 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS IN ELECTRIC COMMERCIAL VEHICLE MARKET

- 7.1 TECHNOLOGY ANALYSIS

- 7.1.1 INTRODUCTION

- 7.1.2 KEY EMERGING TECHNOLOGIES

- 7.1.2.1 AI-based fleet analytics and predictive operations

- 7.1.2.2 Edge computing for on vehicle processing

- 7.1.2.3 High-performance battery systems and fast charging technologies

- 7.1.2.4 Depot energy economics

- 7.1.2.5 Battery swapping and fleet charging infrastructure

- 7.1.3 COMPLEMENTARY TECHNOLOGIES

- 7.1.3.1 Charging ownership models

- 7.1.3.2 Real-time fleet connectivity and low-latency data communication

- 7.1.3.3 GNSS-based vehicle tracking and route optimization

- 7.1.3.4 Over-the-air (OTA) software update framework

- 7.1.4 ADJACENT TECHNOLOGIES

- 7.1.4.1 Fleet telematics and remote vehicle monitoring

- 7.1.4.2 Battery lifecycle monetization

- 7.1.4.3 Software-defined fleet operations

- 7.1.4.4 Battery residual value benchmarks

- 7.1.4.5 Battery lifecycle monetization

- 7.1.4.6 Second-life stationary storage markets

- 7.1.4.7 Usage-based insurance and driver behavior analytics

- 7.1.4.8 Circular economy economics

- 7.1.4.9 Smart city traffic monitoring systems

- 7.2 TECHNOLOGY/PRODUCT ROADMAP

- 7.3 PATENT ANALYSIS

- 7.3.1 LIST OF PATENTS

- 7.4 FUTURE APPLICATIONS

- 7.4.1 PREDICTIVE RISK AND ACCIDENT PREVENTION

- 7.4.2 INTEGRATION WITH SMART CITY AND TRAFFIC ECOSYSTEMS

- 7.4.3 IN-VEHICLE INTELLIGENCE AND HUMAN MACHINE INTERACTION

- 7.5 IMPACT OF AI/GENERATIVE AI ON ELECTRIC COMMERCIAL VEHICLE MARKET

- 7.5.1 TOP USE CASES AND MARKET POTENTIAL

- 7.5.1.1 Key AI/Generative AI electric commercial vehicle use cases

- 7.5.1.2 Market potential

- 7.5.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN ELECTRIC COMMERCIAL VEHICLE MARKET

- 7.5.2.1 AI-driven integration patterns

- 7.5.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN ELECTRIC COMMERCIAL VEHICLE MARKET

- 7.5.3.1 Tesla AI-driven fleet and battery optimization

- 7.5.3.2 Volvo Trucks' connected electric fleet intelligence

- 7.5.3.3 Samsara AI-powered fleet management for electric vehicles

- 7.5.3.4 Geotab predictive EV analytics platform

- 7.5.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 7.5.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED ELECTRIC COMMERCIAL VEHICLES

- 7.5.1 TOP USE CASES AND MARKET POTENTIAL

8 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 8.1 REGULATORY LANDSCAPE

- 8.1.1 COUNTRY-WISE REGULATIONS

- 8.1.1.1 Netherlands

- 8.1.1.2 Germany

- 8.1.1.3 France

- 8.1.1.4 UK

- 8.1.1.5 China

- 8.1.1.6 US

- 8.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.3 INDUSTRY STANDARDS

- 8.1.1 COUNTRY-WISE REGULATIONS

- 8.2 SUSTAINABILITY INITIATIVES

- 8.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 8.4 CERTIFICATION, LABELING, AND ECO-STANDARDS

- 8.4.1 CERTIFICATION, LABELING, AND ENVIRONMENTAL STANDARDS RELEVANT TO ELECTRIC COMMERCIAL VEHICLE MARKET

9 CUSTOMER LANDSCAPE AND BUYING BEHAVIOR

- 9.1 DECISION-MAKING PROCESS

- 9.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 9.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 9.2.2 BUYING CRITERIA

- 9.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 9.4 UNMEET NEED TO VARIOUS END USERS

10 ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE

- 10.1 INTRODUCTION

- 10.2 LIGHT COMMERCIAL VEHICLE

- 10.2.1 INCREASING LAST-MILE DELIVERY ELECTRIFICATION TO DRIVE GROWTH

- 10.3 TRUCKS

- 10.3.1 MEDIUM-DUTY TRUCK

- 10.3.1.1 Increasing regional distribution electrification to drive adoption

- 10.3.2 HEAVY-DUTY TRUCK

- 10.3.2.1 Rising freight decarbonization targets to accelerate market growth

- 10.3.1 MEDIUM-DUTY TRUCK

- 10.4 BUS

- 10.4.1 INCREASING GOVERNMENT INVESTMENTS IN CLEAN PUBLIC TRANSPORTATION TO SUPPORT MARKET EXPANSION

- 10.5 KEY INDUSTRY INSIGHTS

11 ELECTRIC COMMERCIAL VEHICLE MARKET, BY PROPULSION

- 11.1 INTRODUCTION

- 11.2 BATTERY ELECTRIC VEHICLE (BEV)

- 11.2.1 STRONG GOVERNMENT SUPPORT AND REDUCTION IN BATTERY PRICES TO SUPPORT DEMAND

- 11.3 PLUG-IN HYBRID ELECTRIC VEHICLE (PHEV)

- 11.3.1 PLUG IN HYBRID TECHNOLOGY SUPPORTING COMMERCIAL FLEET ELECTRIFICATION

- 11.4 KEY INDUSTRY INSIGHTS

12 ELECTRIC COMMERCIAL VEHICLE MARKET, BY BATTERY TYPE

- 12.1 INTRODUCTION

- 12.2 NMC

- 12.2.1 HIGH DENSITY AND COMPACT SIZE TO DRIVE MARKET

- 12.3 LFP

- 12.3.1 AFFORDABILITY AND SUPERIOR SAFETY TO DRIVE MARKET

- 12.4 KEY INDUSTRY INSIGHTS

13 ELECTRIC COMMERCIAL VEHICLE MARKET, BY POWER OUTPUT

- 13.1 INTRODUCTION

- 13.2 LESS THAN 100 KW

- 13.2.1 GROWING ADOPTION OF ELECTRIC LIGHT COMMERCIAL VEHICLES FOR URBAN DELIVERIES TO DRIVE MARKET

- 13.3 100-250 KW

- 13.3.1 GROWING ELECTRIFICATION OF MEDIUM-DUTY COMMERCIAL FLEETS TO DRIVE MARKET

- 13.4 ABOVE 250 KW

- 13.4.1 EXPANSION OF HEAVY-DUTY ELECTRIC FREIGHT OPERATIONS & INTRACITY LOGISTICS TO DRIVE MARKET

- 13.5 KEY INDUSTRY INSIGHTS

14 ELECTRIC COMMERCIAL VEHICLE MARKET, BY RANGE

- 14.1 INTRODUCTION

- 14.2 LESS THAN 150 MILES

- 14.2.1 E-COMMERCE EXPANSION DRIVING DEMAND FOR SHORT RANGE ELECTRIC COMMERCIAL VEHICLES

- 14.3 151-300 MILES

- 14.3.1 RISING DEMAND FOR ELECTRIC TRUCKS AND BUSES FROM TRANSPORTATION INDUSTRY TO DRIVE MARKET

- 14.4 ABOVE 300 MILES

- 14.4.1 RISING ADOPTION OF LONG-RANGE HEAVY-DUTY ELECTRIC TRUCKS TO DRIVE MARKET

- 14.5 KEY INDUSTRY INSIGHTS

15 ELECTRIC COMMERCIAL VEHICLE MARKET, BY END USE

- 15.1 INTRODUCTION

- 15.2 LAST-MILE DELIVERY

- 15.2.1 GROWTH IN LAST MILE DELIVERY DRIVING ELECTRIC VAN ADOPTION

- 15.3 FIELD SERVICES

- 15.3.1 EXPANSION OF FIELD SERVICE OPERATIONS DRIVING ELECTRIC SERVICE VAN ADOPTION

- 15.4 DISTRIBUTION SERVICES

- 15.4.1 EXPANSION OF DISTRIBUTION NETWORKS DRIVING ELECTRIC VAN AND TRUCK ADOPTION

- 15.5 LONG-HAUL TRANSPORTATION

- 15.5.1 PUSH FOR SUSTAINABLE TRANSPORTATION TO DRIVE MARKET

- 15.6 REFUSE TRUCKS

- 15.6.1 GROWING PUBLIC AWARENESS ABOUT RESPONSIBLE WASTE COLLECTION TO DRIVE MARKET

- 15.7 KEY INDUSTRY INSIGHTS

16 ELECTRIC COMMERCIAL VEHICLE MARKET, BY COMPONENT

- 16.1 INTRODUCTION

- 16.2 BATTERY PACKS

- 16.3 ONBOARD CHARGERS

- 16.4 ELECTRIC MOTORS

- 16.5 INVERTERS

- 16.6 DC-DC CONVERTERS

17 ELECTRIC COMMERCIAL VEHICLE MARKET, BY BATTERY CAPACITY

- 17.1 INTRODUCTION

- 17.2 LESS THAN 60 KWH

- 17.2.1 INCREASING ADOPTION OF COMPACT ELECTRIC VANS FOR LOCAL TRANSPORTATION TO DRIVE MARKET

- 17.3 60-120 KWH

- 17.3.1 GOVERNMENT POLICIES FOR PREMIUM VANS AND PICKUP TRUCKS TO DRIVE MARKET

- 17.4 121-200 KWH

- 17.4.1 RISING ADOPTION OF ELECTRIFICATION IN PREMIUM PICKUP TRUCKS AND BUSES TO DRIVE MARKET

- 17.5 201-300 KWH

- 17.5.1 IMPROVED DRIVING RANGE TO FUEL MARKET GROWTH

- 17.6 301-500 KWH

- 17.6.1 INCREASING PREFERENCE FOR LONG-HAUL ELECTRIC COMMERCIAL VEHICLES TO DRIVE MARKET

- 17.7 ABOVE 500 KWH

- 17.7.1 RISING E-COMMERCE AND RETAIL SECTORS TO DRIVE MARKET

- 17.8 KEY INDUSTRY INSIGHTS

18 ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION

- 18.1 INTRODUCTION

- 18.2 ASIA PACIFIC

- 18.2.1 CHINA

- 18.2.1.1 Growing E-Commerce and Logistics Activities Driving Electric Commercial Vehicle Demand

- 18.2.2 JAPAN

- 18.2.2.1 Advancements in Electric and Fuel Cell Technologies Driving Market Growth

- 18.2.3 INDIA

- 18.2.3.1 Expansion of major OEMs to support market growth

- 18.2.4 SOUTH KOREA

- 18.2.4.1 Rising demand for electric pickup trucks to drive market

- 18.2.1 CHINA

- 18.3 SOUTHEAST ASIA

- 18.3.1 THAILAND

- 18.3.1.1 Setup of Government 2030 decarbonization plan to drive demand

- 18.3.2 INDONESIA

- 18.3.2.1 Growth in Urban Logistics Driving Electric Commercial Vehicle Adoption

- 18.3.3 PHILIPPINES

- 18.3.3.1 Shift to electrification of LCVs to drive demand

- 18.3.4 MALAYSIA

- 18.3.4.1 Public Transport Modernization Accelerating Electric Commercial Vehicle Adoption

- 18.3.5 VIETNAM

- 18.3.5.1 Government plans for E-bus shift to drive market

- 18.3.6 SINGAPORE

- 18.3.6.1 Advancement in EV charging infrastructure to drive market

- 18.3.7 AUSTRALIA

- 18.3.7.1 Commercial Fleet Modernization Accelerating Vehicle Electrification

- 18.3.1 THAILAND

- 18.4 NORTH AMERICA

- 18.4.1 US

- 18.4.1.1 Rising adoption of electric vans to drive market

- 18.4.2 CANADA

- 18.4.2.1 Government plans to electrify transit to drive market

- 18.4.3 MEXICO

- 18.4.3.1 Rising electrification of last-mile delivery fleets to drive market

- 18.4.1 US

- 18.5 EUROPE

- 18.5.1 FRANCE

- 18.5.1.1 Increased adoption of electric vans for delivery purposes to drive market

- 18.5.2 GERMANY

- 18.5.2.1 Expansion of Charging Corridors Supporting Electric Freight Transportation

- 18.5.3 SPAIN

- 18.5.3.1 Government focus on replacing existing bus and van fleets to drive market

- 18.5.4 AUSTRIA

- 18.5.4.1 Strong government incentives and renewable energy integration to drive market

- 18.5.5 NORWAY

- 18.5.5.1 Early commercialization of electric transport and rapid charging network development to drive market

- 18.5.6 SWEDEN

- 18.5.6.1 Presence of market-leading OEMs and startups to drive market

- 18.5.7 NETHERLANDS

- 18.5.7.1 Advancement in EV charging infrastructure to drive market

- 18.5.8 UK

- 18.5.8.1 Government electrification roadmap to drive market

- 18.5.9 ITALY

- 18.5.9.1 Urban Emission Regulations Accelerating Electric Commercial Vehicle Adoption

- 18.5.10 BELGIUM

- 18.5.10.1 Expansion of freight electrification and urban delivery van deployment to drive market

- 18.5.11 DENMARK

- 18.5.11.1 Expansion of green transportation policies and regional logistics electrification to drive market

- 18.5.12 SWITZERLAND

- 18.5.12.1 Strong urban emission reduction targets and rising electric freight deployment to drive market

- 18.5.1 FRANCE

- 18.6 REST OF THE WORLD

- 18.6.1 RUSSIA

- 18.6.1.1 Expansion of electric bus procurement programs to drive market

- 18.6.2 BRAZIL

- 18.6.2.1 Expansion of electric bus deployment and urban logistics electrification to drive market

- 18.6.3 TURKEY

- 18.6.3.1 Expansion of urban logistics fleets to drive market

- 18.6.1 RUSSIA

19 COMPETITIVE LANDSCAPE

- 19.1 OVERVIEW

- 19.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 19.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN ELECTRIC COMMERCIAL VEHICLE MARKET

- 19.3 MARKET SHARE ANALYSIS, 2025

- 19.3.1 ELECTRIC BUSES & TRUCKS

- 19.3.2 ELECTRIC LIGHT COMMERCIAL VEHICLES

- 19.4 REVENUE ANALYSIS, 2021-2025

- 19.5 COMPANY VALUATION AND FINANCIAL METRICS

- 19.5.1 COMPANY VALUATION

- 19.5.2 FINANCIAL METRICS

- 19.6 BRAND/PRODUCT COMPARISON

- 19.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 19.7.1 STARS

- 19.7.2 EMERGING LEADERS

- 19.7.3 PERVASIVE PLAYERS

- 19.7.4 PARTICIPANTS

- 19.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 19.7.5.1 Company footprint

- 19.7.5.2 Regional footprint

- 19.7.5.3 Vehicle type footprint

- 19.7.5.4 Propulsion footprint

- 19.7.5.5 Battery type footprint

- 19.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 19.8.1 PROGRESSIVE COMPANIES

- 19.8.2 RESPONSIVE COMPANIES

- 19.8.3 DYNAMIC COMPANIES

- 19.8.4 STARTING BLOCKS

- 19.8.5 COMPETITIVE BENCHMARKING, STARTUPS/SMES, 2025

- 19.8.5.1 List of key startups/SMEs

- 19.8.5.2 Competitive benchmarking of startups/SMEs

- 19.9 COMPETITIVE SCENARIO

- 19.9.1 PRODUCT LAUNCHES

- 19.9.2 DEALS

- 19.9.3 EXPANSIONS

- 19.9.4 OTHER DEVELOPMENTS

20 COMPANY PROFILES

- 20.1 CHINESE KEY PLAYERS

- 20.1.1 XCMG GLOBAL

- 20.1.1.1 Business overview

- 20.1.1.2 Electric commercial vehicle sales, 2022-2025 (Units)

- 20.1.1.3 Products offered

- 20.1.1.4 Recent developments

- 20.1.1.4.1 Product launches

- 20.1.1.4.2 Deals

- 20.1.1.4.3 Expansions

- 20.1.1.4.4 Other developments

- 20.1.1.5 MnM view

- 20.1.1.5.1 Key strengths

- 20.1.1.5.2 Strategic choices

- 20.1.1.5.3 Weaknesses and competitive threats

- 20.1.2 SANY GROUP

- 20.1.2.1 Business overview

- 20.1.2.2 Electric commercial vehicle sales, 2022-2025

- 20.1.2.3 Products offered

- 20.1.2.4 Recent development

- 20.1.2.4.1 Product launches

- 20.1.2.4.2 Deals

- 20.1.2.4.3 Expansions

- 20.1.2.4.4 Other developments

- 20.1.2.5 MnM view

- 20.1.2.5.1 Key strengths

- 20.1.2.5.2 Strategic choices

- 20.1.2.5.3 Weaknesses and competitive threats

- 20.1.3 FAW GROUP

- 20.1.3.1 Business overview

- 20.1.3.2 Electric commercial vehicle sales, 2022-2025 (Units)

- 20.1.3.3 Products offered

- 20.1.3.4 Recent developments

- 20.1.3.4.1 Product launches/enhancements

- 20.1.3.4.2 Deals

- 20.1.3.4.3 Expansions

- 20.1.3.4.4 Other developments

- 20.1.3.5 MnM view

- 20.1.3.5.1 Key strengths

- 20.1.3.5.2 Strategic choices

- 20.1.3.5.3 Weaknesses and competitive threats

- 20.1.4 CNHTC

- 20.1.4.1 Business overview

- 20.1.4.2 Electric commercial vehicle sales, 2022-2025 (Units)

- 20.1.4.3 Products offered

- 20.1.4.4 Recent developments

- 20.1.4.4.1 Product launches

- 20.1.4.4.2 Deals

- 20.1.4.4.3 Expansions

- 20.1.4.4.4 Other developments

- 20.1.4.5 MnM view

- 20.1.4.5.1 Key strengths

- 20.1.4.5.2 Strategic choices

- 20.1.4.5.3 Weaknesses and competitive threats

- 20.1.5 YUTONG BUS CO., LTD.

- 20.1.5.1 Business overview

- 20.1.5.2 Electric commercial vehicle sales, 2022-2025 (Units)

- 20.1.5.3 Products offered

- 20.1.5.4 Recent developments

- 20.1.5.4.1 Product launches/upgrades/developments

- 20.1.5.4.2 Deals

- 20.1.5.4.3 Expansions

- 20.1.5.4.4 Other developments

- 20.1.5.5 MnM view

- 20.1.5.5.1 Key strengths

- 20.1.5.5.2 Strategic choices

- 20.1.5.5.3 Weaknesses and competitive threats

- 20.1.6 BEIJING AUTOMOTIVE GROUP CO., LTD.

- 20.1.6.1 Business overview

- 20.1.6.2 Electric commercial vehicle sales, 2022-2025 (Units)

- 20.1.6.3 Products offered

- 20.1.6.4 Recent developments

- 20.1.6.4.1 Product launches

- 20.1.6.4.2 Deals

- 20.1.6.4.3 Expansions

- 20.1.6.4.4 Other developments

- 20.1.7 DONGFENG MOTOR CORPORATION

- 20.1.7.1 Business overview

- 20.1.7.2 Electric commercial vehicle sales, 2022-2025 (Units)

- 20.1.7.3 Products offered

- 20.1.7.4 Recent developments

- 20.1.7.4.1 Product launches/enhancements

- 20.1.7.4.2 Deals

- 20.1.7.4.3 Expansions

- 20.1.7.4.4 Other developments

- 20.1.8 BYD

- 20.1.8.1 Business overview

- 20.1.8.2 Electric commercial vehicle sales, 2022-2025 (Units)

- 20.1.8.3 Products offered

- 20.1.8.4 Recent developments

- 20.1.8.4.1 Product launches

- 20.1.8.4.2 Deals

- 20.1.8.4.3 Expansions

- 20.1.8.4.4 Other developments

- 20.1.1 XCMG GLOBAL

- 20.2 NON-CHINESE KEY PLAYERS

- 20.2.1 DAIMLER GROUP AG

- 20.2.1.1 Business overview

- 20.2.1.2 Electric commercial vehicle sales, 2022-2025 (Units)

- 20.2.1.3 Products offered

- 20.2.1.4 Recent developments

- 20.2.1.4.1 Product launches

- 20.2.1.4.2 Deals

- 20.2.1.4.3 Expansions

- 20.2.1.4.4 Other developments

- 20.2.2 AB VOLVO

- 20.2.2.1 Business overview

- 20.2.2.2 Electric commercial vehicle sales, 2022-2025 (Units)

- 20.2.2.3 Products offered

- 20.2.2.4 Recent developments

- 20.2.2.4.1 Product launches/developments

- 20.2.2.4.2 Deals

- 20.2.2.4.3 Expansions

- 20.2.3 FORD MOTOR COMPANY

- 20.2.3.1 Business overview

- 20.2.3.2 Electric commercial vehicle sales, 2022-2025 (Units)

- 20.2.3.3 Products offered

- 20.2.3.4 Recent developments

- 20.2.3.4.1 Product launches/developments

- 20.2.3.4.2 Deals

- 20.2.3.4.3 Expansions

- 20.2.3.4.4 Other developments

- 20.2.4 TESLA, INC.

- 20.2.4.1 Business overview

- 20.2.4.2 Products offered

- 20.2.4.3 Recent developments

- 20.2.4.3.1 Product launches

- 20.2.4.3.2 Deals

- 20.2.4.3.3 Expansions

- 20.2.5 HYUNDAI MOTOR COMPANY

- 20.2.5.1 Business overview

- 20.2.5.2 Products offered

- 20.2.5.3 Recent developments

- 20.2.5.3.1 Product launches/developments

- 20.2.5.3.2 Deals

- 20.2.5.3.3 Expansions

- 20.2.5.3.4 Other developments

- 20.2.6 NFI GROUP

- 20.2.6.1 Business overview

- 20.2.6.2 Products offered

- 20.2.6.3 Recent developments

- 20.2.6.3.1 Product launches

- 20.2.6.3.2 Deals

- 20.2.6.3.3 Expansions

- 20.2.6.3.4 Other developments

- 20.2.1 DAIMLER GROUP AG

- 20.3 OTHER PLAYERS

- 20.3.1 TATA MOTORS LIMITED

- 20.3.2 WORKHORSE GROUP

- 20.3.3 VDL GROEP

- 20.3.4 ASHOK LEYLAND

- 20.3.5 ISUZU MOTORS LTD.

- 20.3.6 IRIZAR GROUP

- 20.3.7 IVECO

- 20.3.8 XOS TRUCKS INC.

- 20.3.9 MAN SE

- 20.3.10 GOLDEN DRAGON

- 20.3.11 ZENITH MOTORS

- 20.3.12 FIRST BUS (WRIGHTBUS)

21 RESEARCH METHODOLOGY

- 21.1 RESEARCH DATA

- 21.1.1 SECONDARY DATA

- 21.1.1.1 Key secondary sources

- 21.1.1.2 Key data from secondary sources

- 21.1.2 PRIMARY DATA

- 21.1.2.1 Primary interviewees from demand and supply sides

- 21.1.2.2 Key industry insights and breakdown of primary interviews

- 21.1.2.3 List of primary interview participants

- 21.1.1 SECONDARY DATA

- 21.2 MARKET SIZE ESTIMATION

- 21.2.1 BOTTOM-UP APPROACH

- 21.2.2 TOP-DOWN APPROACH

- 21.3 DATA TRIANGULATION

- 21.4 FACTOR ANALYSIS

- 21.4.1 DEMAND AND SUPPLY-SIDE FACTOR ANALYSIS

- 21.5 RESEARCH ASSUMPTIONS

- 21.6 RESEARCH LIMITATIONS

- 21.7 RISK ASSESSMENT

22 APPENDIX

- 22.1 KEY INSIGHTS FROM INDUSTRY EXPERTS

- 22.2 DISCUSSION GUIDE

- 22.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 22.4 CUSTOMIZATION OPTIONS

- 22.4.1 PROFILING OF ADDITIONAL MARKET PLAYERS (UP TO 5)

- 22.4.2 ELECTRIC COMMERCIAL VEHICLE MARKET, BY BUS LENGTH AT REGIONAL LEVEL

- 22.4.3 ELECTRIC COMMERCIAL VEHICLE MARKET, BY PROPULSION AT COUNTRY LEVEL

- 22.5 RELATED REPORTS

- 22.6 AUTHOR DETAILS

List of Tables

- TABLE 1 MARKET DEFINITION, BY PROPULSION

- TABLE 2 MARKET DEFINITION, BY END USE

- TABLE 3 MARKET DEFINITION, BY BATTERY TYPE

- TABLE 4 MARKET DEFINITION, BY VEHICLE TYPE

- TABLE 5 MARKET DEFINITION, BY COMPONENT

- TABLE 6 INCLUSIONS AND EXCLUSIONS

- TABLE 7 CURRENCY EXCHANGE RATES (PER USD), 2021-2025

- TABLE 8 ADVANCEMENTS IN BATTERY TECHNOLOGY AND STRATEGIC IMPACT

- TABLE 9 EXPANSION PLANS AND OPERATIONAL FOCUS

- TABLE 10 BATTERY DEGRADATION AND IMPLICATION

- TABLE 11 ENERGY MANAGEMENT APPROACH AND SYSTEM IMPLEMENTATION

- TABLE 12 STRATEGY IMPLICATION BY OEMS

- TABLE 13 ELECTRIC COMMERCIAL VEHICLE MARKET: IMPACT OF MARKET DYNAMICS

- TABLE 14 GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021-2030

- TABLE 15 ROLE OF COMPANIES IN ELECTRIC COMMERCIAL VEHICLE MARKET ECOSYSTEM

- TABLE 16 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY ELECTRIC TRUCK VEHICLE TYPE, 2025 (USD THOUSAND)

- TABLE 17 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD THOUSAND)

- TABLE 18 IMPORT DATA FOR HS CODE 8704-COMPLIANT PRODUCTS, BY COUNTRY, 2022-2025 (USD BILLION)

- TABLE 19 EXPORT DATA FOR HS CODE 8704-COMPLIANT PRODUCTS, BY COUNTRY, 2022-2025 (USD BILLION)

- TABLE 20 KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 21 ELECTRIC BUS SALES BY LEADING OEMS, 2021-2025 (UNIT)

- TABLE 22 TCO ANALYSIS: ICE VS. ELECTRIC BUS

- TABLE 23 ELECTRIC BUS: OEM-WISE INSTALLED BATTERY CAPACITIES, 2021-2025

- TABLE 24 ELECTRIC TRUCK SALES BY LEADING OEMS, 2021-2025 (UNITS)

- TABLE 25 ELECTRIC TRUCK: TCO ANALYSIS: ICE VS. ELECTRIC

- TABLE 26 ELECTRIC TRUCK: OEM-WISE INSTALLED BATTERY CAPACITIES, 2021-2025

- TABLE 27 ELECTRIC LCV SALES BY LEADING OEMS, 2021-2025 (UNITS)

- TABLE 28 ELECTRIC LCV: TCO ANALYSIS: ICE VS. ELECTRIC

- TABLE 29 ELECTRIC LCV: OEM-WISE INSTALLED BATTERY CAPACITIES, 2021-2025 (MWH)

- TABLE 30 INSIGHTS INTO EDGE COMPUTING FOR ON-DEVICE PROCESSING

- TABLE 31 FUTURE OUTLOOK: ELECTRIC COMMERCIAL VEHICLE MARKET ECOSYSTEM

- TABLE 32 PATENT REGISTRATIONS IN ELECTRIC COMMERCIAL VEHICLE MARKET, SEPTEMBER 2024-MARCH 2026

- TABLE 33 KEY AI/GENERATIVE AI ELECTRIC COMMERCIAL VEHICLE USE CASES

- TABLE 34 MARKET POTENTIAL

- TABLE 35 ROLE AND IMPACT OF AI IN ELECTRIC COMMERCIAL VEHICLE MARKET

- TABLE 36 NETHERLANDS: EV INCENTIVES

- TABLE 37 NETHERLANDS: EV CHARGING STATION INCENTIVES

- TABLE 38 GERMANY: EV INCENTIVES

- TABLE 39 GERMANY: EV CHARGING STATION INCENTIVES

- TABLE 40 FRANCE: EV INCENTIVES

- TABLE 41 FRANCE: EV CHARGING STATION INCENTIVES

- TABLE 42 UK: EV INCENTIVES

- TABLE 43 UK: EV CHARGING STATION INCENTIVES

- TABLE 44 CHINA: EV INCENTIVES

- TABLE 45 CHINA: EV CHARGING STATION INCENTIVES

- TABLE 46 US: EV INCENTIVES

- TABLE 47 US: EV CHARGING STATION INCENTIVES

- TABLE 48 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 49 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 50 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 51 GLOBAL INDUSTRY STANDARDS

- TABLE 52 POLICY INITIATIVES AFFECTING SUSTAINABILITY, SAFETY, PRIVACY, AND TECHNOLOGY COMPLIANCE FOR ELECTRIC COMMERCIAL VEHICLES

- TABLE 53 CERTIFICATION, LABELING, AND ENVIRONMENTAL STANDARDS

- TABLE 54 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS IN ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE

- TABLE 55 KEY BUYING CRITERIA IN ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE

- TABLE 56 ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 57 ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 58 ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 59 ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 60 LIGHT COMMERCIAL VEHICLE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 61 LIGHT COMMERCIAL VEHICLES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 62 LIGHT COMMERCIAL VEHICLES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 63 LIGHT COMMERCIAL VEHICLES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 64 TRUCK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 65 TRUCK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 66 TRUCK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 67 TRUCK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 68 MEDIUM-DUTY TRUCK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 69 MEDIUM-DUTY TRUCK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 70 MEDIUM-DUTY TRUCK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 71 MEDIUM-DUTY TRUCK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 72 HEAVY-DUTY TRUCK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 73 HEAVY-DUTY TRUCK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 74 HEAVY-DUTY TRUCK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 75 HEAVY-DUTY TRUCK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 76 BUS: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 77 BUS: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 78 BUS: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 79 BUS: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033(USD MILLION)

- TABLE 80 ELECTRIC COMMERCIAL VEHICLE MARKET, BY PROPULSION, 2021-2025 (UNITS)

- TABLE 81 ELECTRIC COMMERCIAL VEHICLE MARKET, BY PROPULSION, 2026-2033 (UNITS)

- TABLE 82 BATTERY ELECTRIC VEHICLE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 83 BATTERY ELECTRIC VEHICLE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 84 PLUG-IN HYBRID ELECTRIC VEHICLE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 85 PLUG-IN HYBRID ELECTRIC VEHICLE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 86 ELECTRIC COMMERCIAL VEHICLE MARKET, BY BATTERY TYPE, 2021-2025 (UNITS)

- TABLE 87 ELECTRIC COMMERCIAL VEHICLE MARKET, BY BATTERY TYPE, 2026-2033 (UNITS)

- TABLE 88 NMC BATTERIES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 89 NMC BATTERIES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 90 LFP BATTERIES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 91 LFP BATTERIES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 92 ELECTRIC COMMERCIAL VEHICLE MARKET, BY POWER OUTPUT, 2021-2025 (UNITS)

- TABLE 93 ELECTRIC COMMERCIAL VEHICLE MARKET, BY POWER OUTPUT, 2026-2033(UNITS)

- TABLE 94 LESS THAN 100 KW: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION 2021-2025 (UNITS)

- TABLE 95 LESS THAN 100 KW: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION 2026-2033(UNITS)

- TABLE 96 100-250 KW: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025(UNITS)

- TABLE 97 100-250 KW: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 98 ABOVE 250 KW: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 99 ABOVE 250 KW: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 100 ELECTRIC COMMERCIAL VEHICLE MARKET, BY RANGE, 2021-2025 (UNITS)

- TABLE 101 ELECTRIC COMMERCIAL VEHICLE MARKET, BY RANGE, 2026-2033(UNITS)

- TABLE 102 LESS THAN 150 MILES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 103 LESS THAN 150 MILES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 104 151-300 MILES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 105 151-300 MILES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 106 ABOVE 300 MILES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 107 ABOVE 300 MILES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 108 ELECTRIC COMMERCIAL VEHICLE MARKET, BY END USE, 2021-2025 (UNITS)

- TABLE 109 ELECTRIC COMMERCIAL VEHICLE MARKET, BY END USE, 2026-2033 (UNITS)

- TABLE 110 PRODUCTS OFFERED BY BATTERY MANUFACTURERS

- TABLE 111 ONBOARD CHARGER MANUFACTURERS FOR ELECTRIC COMMERCIAL VEHICLES

- TABLE 112 ELECTRIC TRUCK MODELS, BY ELECTRIC MOTOR TYPE

- TABLE 113 INVERTERS, BY OEMS

- TABLE 114 ELECTRIC COMMERCIAL VEHICLE MARKET, BY BATTERY CAPACITY, 2021-2025(UNITS)

- TABLE 115 ELECTRIC COMMERCIAL VEHICLE MARKET, BY BATTERY CAPACITY, 2026-2033 (UNITS)

- TABLE 116 LESS THAN 60 KWH: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 117 LESS THAN 60 KWH: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 118 60-120 KWH: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 119 60-120 KWH: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 120 121-200 KWH: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 121 121-200 KWH: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 122 201-300 KWH: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 123 201-300 KWH: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033(UNITS)

- TABLE 124 301-500 KWH: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 125 301-500 KWH: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 126 ABOVE 500 KWH: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025(UNITS)

- TABLE 127 ABOVE 500 KWH: ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 128 ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (UNITS)

- TABLE 129 ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 130 ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 131 ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 132 ASIA PACIFIC: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2021-2025 (UNITS)

- TABLE 133 ASIA PACIFIC: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2026-2033 (UNITS)

- TABLE 134 ASIA PACIFIC: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 135 ASIA PACIFIC: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 136 CHINA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 137 CHINA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 138 CHINA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 139 CHINA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 140 JAPAN: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 141 JAPAN ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 142 JAPAN: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 143 JAPAN ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 144 INDIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 145 INDIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 146 INDIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 147 INDIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 148 SOUTH KOREA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 149 SOUTH KOREA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 150 SOUTH KOREA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 151 SOUTH KOREA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 152 SOUTHEAST ASIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2021-2025 (UNITS)

- TABLE 153 SOUTHEAST ASIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2026-2033 (UNITS)

- TABLE 154 SOUTHEAST ASIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 155 SOUTHEAST ASIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 156 THAILAND: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 157 THAILAND: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 158 THAILAND: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 159 THAILAND: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 160 INDONESIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 161 INDONESIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 162 INDONESIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 163 INDONESIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 164 PHILIPPINES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 165 PHILIPPINES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 166 PHILIPPINES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 167 PHILIPPINES: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 168 MALAYSIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 169 MALAYSIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 170 MALAYSIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 171 MALAYSIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 172 VIETNAM: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 173 VIETNAM: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 174 VIETNAM: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 175 VIETNAM: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 176 SINGAPORE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 177 SINGAPORE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 178 SINGAPORE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 179 SINGAPORE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 180 AUSTRALIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 181 AUSTRALIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 182 AUSTRALIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 183 AUSTRALIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 184 NORTH AMERICA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2021-2025 (UNITS)

- TABLE 185 NORTH AMERICA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2026-2033 (UNITS)

- TABLE 186 NORTH AMERICA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 187 NORTH AMERICA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 188 US: ELECTRIC VEHICLE INCENTIVES

- TABLE 189 US: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 190 US: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 191 US: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 192 US: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 193 CANADA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 194 CANADA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 195 CANADA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 196 CANADA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 197 MEXICO: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 198 MEXICO: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 199 MEXICO: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 200 MEXICO: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 201 EUROPE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2021-2025 (UNITS)

- TABLE 202 EUROPE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2026-2033 (UNITS)

- TABLE 203 EUROPE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 204 EUROPE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 205 FRANCE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 206 FRANCE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 207 FRANCE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 208 FRANCE: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 209 GERMANY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 210 GERMANY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 211 GERMANY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 212 GERMANY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 213 SPAIN: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 214 SPAIN: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 215 SPAIN: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 216 SPAIN: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 217 AUSTRIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 218 AUSTRIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 219 AUSTRIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 220 AUSTRIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 221 NORWAY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 222 NORWAY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 223 NORWAY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 224 NORWAY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 225 SWEDEN: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 226 SWEDEN: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 227 SWEDEN: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 228 SWEDEN: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 229 NETHERLANDS: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 230 NETHERLANDS: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 231 NETHERLANDS: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 232 NETHERLANDS: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 233 UK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 234 UK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 235 UK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 236 UK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 237 ITALY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 238 ITALY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 239 ITALY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 240 ITALY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 241 BELGIUM: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 242 BELGIUM: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 243 BELGIUM: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 244 BELGIUM: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 245 DENMARK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 246 DENMARK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 247 DENMARK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 248 DENMARK: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 249 SWITZERLAND: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 250 SWITZERLAND: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 251 SWITZERLAND: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 252 SWITZERLAND: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 253 REST OF THE WORLD: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2021-2025 (UNITS)

- TABLE 254 REST OF THE WORLD: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2026-2033 (UNITS)

- TABLE 255 REST OF THE WORLD: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 256 REST OF THE WORLD: ELECTRIC COMMERCIAL VEHICLE MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 257 RUSSIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 258 RUSSIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 259 RUSSIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 260 RUSSIA: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 261 BRAZIL: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 262 BRAZIL: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 263 BRAZIL: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 264 BRAZIL: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 265 TURKEY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (UNITS)

- TABLE 266 TURKEY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (UNITS)

- TABLE 267 TURKEY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2021-2025 (USD MILLION)

- TABLE 268 TURKEY: ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 269 OVERVIEW OF STRATEGIES DEPLOYED BY KEY COMPANIES

- TABLE 270 ELECTRIC COMMERCIAL VEHICLE MARKET SHARE OF TOP 5 PLAYERS (BUS & TRUCK MANUFACTURERS), 2025

- TABLE 271 ELECTRIC COMMERCIAL VEHICLE MARKET SHARE OF TOP 5 PLAYERS (LCV MANUFACTURERS), 2025

- TABLE 272 ELECTRIC COMMERCIAL VEHICLE MARKET: REGIONAL FOOTPRINT, 2025

- TABLE 273 ELECTRIC COMMERCIAL VEHICLE MARKET: VEHICLE TYPE FOOTPRINT, 2025

- TABLE 274 ELECTRIC COMMERCIAL VEHICLE MARKET: PROPULSION FOOTPRINT, 2025

- TABLE 275 ELECTRIC COMMERCIAL VEHICLE MARKET: BATTERY TYPE FOOTPRINT, 2025

- TABLE 276 ELECTRIC COMMERCIAL VEHICLE MARKET: KEY STARTUPS/SMES

- TABLE 277 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 278 ELECTRIC COMMERCIAL VEHICLE MARKET: PRODUCT LAUNCHES, JANUARY 2022-MAY 2026

- TABLE 279 ELECTRIC COMMERCIAL VEHICLE MARKET: DEALS, JANUARY 2022-MAY 2026

- TABLE 280 ELECTRIC COMMERCIAL VEHICLE MARKET: EXPANSIONS, JANUARY 2022-MAY 2026

- TABLE 281 ELECTRIC COMMERCIAL VEHICLE MARKET: OTHER DEVELOPMENTS, JANUARY 2022-MAY 2026

- TABLE 282 XCMG GLOBAL: COMPANY OVERVIEW

- TABLE 283 XCMG GLOBAL: PRODUCTS OFFERED

- TABLE 284 XCMG GLOBAL: PRODUCT LAUNCHES

- TABLE 285 XCMG GLOBAL: DEALS

- TABLE 286 XCMG GLOBAL: EXPANSIONS

- TABLE 287 XCMG GLOBAL: OTHER DEVELOPMENTS

- TABLE 288 SANY GROUP: COMPANY OVERVIEW

- TABLE 289 SANY GROUP: PRODUCTS OFFERED

- TABLE 290 SANY GROUP: PRODUCT LAUNCHES

- TABLE 291 SANY GROUP: DEALS

- TABLE 292 SANY GROUP: EXPANSIONS

- TABLE 293 SANY GROUP: OTHER DEVELOPMENTS

- TABLE 294 FAW GROUP: COMPANY OVERVIEW

- TABLE 295 FAW GROUP: PRODUCTS OFFERED

- TABLE 296 FAW GROUP: PRODUCT LAUNCHES/ENHANCEMENTS

- TABLE 297 FAW GROUP: DEALS

- TABLE 298 FAW GROUP: EXPANSIONS

- TABLE 299 FAW GROUP: OTHER DEVELOPMENTS

- TABLE 300 CNHTC: COMPANY OVERVIEW

- TABLE 301 CNHTC: PRODUCTS OFFERED

- TABLE 302 CNHTC: PRODUCT LAUNCHES

- TABLE 303 CNHTC: DEALS

- TABLE 304 CNHTC: EXPANSIONS

- TABLE 305 CNHTC: OTHER DEVELOPMENTS

- TABLE 306 YUTONG BUS CO., LTD.: COMPANY OVERVIEW

- TABLE 307 YUTONG BUS CO., LTD.: PRODUCTS OFFERED

- TABLE 308 YUTONG BUS CO., LTD.: PRODUCT LAUNCHES/UPGRADES/DEVELOPMENTS

- TABLE 309 YUTONG BUS CO., LTD.: DEALS

- TABLE 310 YUTONG BUS CO., LTD.: EXPANSIONS

- TABLE 311 YUTONG BUS CO., LTD.: OTHER DEVELOPMENTS

- TABLE 312 BEIJING AUTOMOTIVE GROUP CO., LTD.: COMPANY OVERVIEW

- TABLE 313 BEIJING AUTOMOTIVE GROUP CO., LTD.: PRODUCTS OFFERED

- TABLE 314 BEIJING AUTOMOTIVE GROUP CO., LTD.: PRODUCT LAUNCHES

- TABLE 315 BEIJING AUTOMOTIVE GROUP CO., LTD.: DEALS

- TABLE 316 BEIJING AUTOMOTIVE GROUP CO., LTD.: EXPANSIONS

- TABLE 317 BEIJING AUTOMOTIVE GROUP CO., LTD.: OTHER DEVELOPMENTS

- TABLE 318 DONGFENG MOTOR CORPORATION: COMPANY OVERVIEW

- TABLE 319 DONGFENG MOTOR CORPORATION: PRODUCTS OFFERED

- TABLE 320 DONGFENG MOTOR CORPORATION: PRODUCT LAUNCHES/ENHANCEMENTS

- TABLE 321 DONGFENG MOTOR CORPORATION: DEALS

- TABLE 322 DONGFENG MOTOR CORPORATION: EXPANSIONS

- TABLE 323 DONGFENG MOTOR CORPORATION: OTHER DEVELOPMENTS

- TABLE 324 BYD: COMPANY OVERVIEW

- TABLE 325 BYD: PRODUCTS OFFERED

- TABLE 326 BYD: PRODUCT LAUNCHES

- TABLE 327 BYD: DEALS

- TABLE 328 BYD: EXPANSIONS

- TABLE 329 BYD: OTHER DEVELOPMENTS

- TABLE 330 DAIMLER GROUP AG: COMPANY OVERVIEW

- TABLE 331 DAIMLER GROUP AG: PRODUCTS OFFERED

- TABLE 332 DAIMLER GROUP AG: PRODUCT LAUNCHES

- TABLE 333 DAIMLER GROUP AG: DEALS

- TABLE 334 DAIMLER GROUP AG: EXPANSIONS

- TABLE 335 DAIMLER GROUP AG: OTHER DEVELOPMENTS

- TABLE 336 AB VOLVO: COMPANY OVERVIEW

- TABLE 337 AB VOLVO: PRODUCTS OFFERED

- TABLE 338 AB VOLVO: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 339 AB VOLVO: DEALS

- TABLE 340 AB VOLVO: EXPANSIONS

- TABLE 341 FORD MOTOR COMPANY: COMPANY OVERVIEW

- TABLE 342 FORD MOTOR COMPANY: PRODUCTS OFFERED

- TABLE 343 FORD MOTOR COMPANY: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 344 FORD MOTOR COMPANY: DEALS

- TABLE 345 FORD MOTOR COMPANY: EXPANSIONS

- TABLE 346 FORD MOTORS COMPANY: OTHER DEVELOPMENTS

- TABLE 347 TESLA, INC.: COMPANY OVERVIEW

- TABLE 348 TESLA, INC.: PRODUCTS OFFERED

- TABLE 349 TESLA, INC.: PRODUCT LAUNCHES

- TABLE 350 TESLA, INC.: DEALS

- TABLE 351 TESLA, INC.: EXPANSIONS

- TABLE 352 HYUNDAI MOTOR COMPANY: COMPANY OVERVIEW

- TABLE 353 HYUNDAI MOTOR COMPANY: PRODUCTS OFFERED

- TABLE 354 HYUNDAI MOTOR COMPANY: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 355 HYUNDAI MOTOR COMPANY: DEALS

- TABLE 356 HYUNDAI MOTOR COMPANY: EXPANSIONS

- TABLE 357 HYUNDAI MOTOR COMPANY: OTHER DEVELOPMENTS

- TABLE 358 NFI GROUP: COMPANY OVERVIEW

- TABLE 359 NFI GROUP: PRODUCTS OFFERED

- TABLE 360 NFI GROUP: PRODUCT LAUNCHES

- TABLE 361 NFI GROUP: DEALS

- TABLE 362 NFI GROUP: EXPANSIONS

- TABLE 363 NFI GROUP: OTHER DEVELOPMENTS

List of Figures

- FIGURE 1 MARKET SEGMENTATION AND REGIONAL SNAPSHOT

- FIGURE 2 MARKET SCENARIO

- FIGURE 3 GLOBAL ELECTRIC COMMERCIAL VEHICLE MARKET, 2021-2033

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN ELECTRIC COMMERCIAL VEHICLE MARKET, JANUARY 2022-MAY 2026

- FIGURE 5 DISRUPTIONS INFLUENCING GROWTH OF ELECTRIC COMMERCIAL VEHICLE MARKET

- FIGURE 6 HIGH-GROWTH SEGMENTS IN ELECTRIC COMMERCIAL VEHICLE MARKET, 2026-2033

- FIGURE 7 ASIA PACIFIC TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 8 INCREASING ADOPTION OF ZERO-EMISSION VEHICLES TO DRIVE MARKET

- FIGURE 9 LCV SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 10 BEV SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 11 NMC BATTERIES SEGMENT TO HAVE FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 12 150-300 MILES RANGE SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 13 ABOVE 501 KWH BATTERY CAPACITY SEGMENT TO REGISTER FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 14 100- 250 KW POWER OUTPUT SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 15 LONG-HAUL TRANSPORTATION END USE SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 16 ASIA PACIFIC TO LEAD MARKET IN 2026

- FIGURE 17 ELECTRIC COMMERCIAL VEHICLE MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 18 TOYOTA BATTERY TECHNOLOGY DEVELOPMENT ROADMAP

- FIGURE 19 BATTERY TECHNOLOGY EVOLUTION: CYCLE LIFE AND COST TRENDS

- FIGURE 20 BATTERY STATE HEALTH, BY CHARGE CYCLE

- FIGURE 21 SUPPLY CHAIN ANALYSIS

- FIGURE 22 ELECTRIC COMMERCIAL VEHICLE MARKET ECOSYSTEM

- FIGURE 23 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD THOUSAND)

- FIGURE 24 IMPORT DATA FOR HS CODE 8704-COMPLIANT PRODUCTS, BY COUNTRY, 2022-2025 (USD BILLION)

- FIGURE 25 EXPORT DATA FOR HS CODE 8704-COMPLIANT PRODUCTS, BY COUNTRY, 2022-2025 (USD BILLION)

- FIGURE 26 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 27 INVESTMENT SCENARIO, 2022-2025

- FIGURE 28 CRUDE OIL PRICE SURGE FOLLOWING ISRAEL-IRAN CONFLICT, 2026

- FIGURE 29 INCREASE IN PETROL PRICES ACROSS KEY COUNTRIES, 2026

- FIGURE 30 DIRECT IMPACT OF ISRAEL-IRAN CONFLICT ON AUTOMOTIVE SECTOR

- FIGURE 31 INDIRECT IMPACT OF ISRAEL-IRAN CONFLICT ON AUTOMOTIVE SECTOR

- FIGURE 32 SECTORS IMPACTED BY EU-INDIA FTA DEAL

- FIGURE 33 IMPACT ON IMPORT DUTY FOR EUROPEAN VEHICLES DUE TO EU-INDIA FTA

- FIGURE 34 IMPACT ON OEMS AND SUPPLIERS IN INDIA DUE TO EU-INDIA FTA

- FIGURE 35 IMPACT ON AUTOMOTIVE COMPONENT TRADE DUE TO EU-INDIA FTA

- FIGURE 36 LORA-ENABLED INTELLIGENT ECOSYSTEM FOR ELECTRIC COMMERCIAL VEHICLES

- FIGURE 37 ELECTRIC COMMERCIAL VEHICLE MARKET: TECHNOLOGY DEVELOPMENT ROADMAP

- FIGURE 38 PATENT ANALYSIS, 2015-2026

- FIGURE 39 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS IN ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE

- FIGURE 40 KEY BUYING CRITERIA IN ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE

- FIGURE 41 ELECTRIC COMMERCIAL VEHICLE MARKET, BY VEHICLE TYPE, 2026 VS. 2033 (USD MILLION)

- FIGURE 42 ELECTRIC COMMERCIAL VEHICLE MARKET, BY PROPULSION, 2026 VS. 2033 (THOUSAND UNITS)

- FIGURE 43 ELECTRIC COMMERCIAL VEHICLE MARKET, BY BATTERY TYPE, 2026-2033 (UNITS)

- FIGURE 44 ELECTRIC COMMERCIAL VEHICLE MARKET, BY POWER OUTPUT, 2026 VS. 2033 (UNITS)

- FIGURE 45 ELECTRIC COMMERCIAL VEHICLE MARKET, BY RANGE, 2026 VS. 2033 (UNITS)

- FIGURE 46 ELECTRIC COMMERCIAL VEHICLE MARKET, BY END USE, 2026 VS. 2033 (UNITS)

- FIGURE 47 DC-DC CONVERTER

- FIGURE 48 ELECTRIC COMMERCIAL VEHICLE MARKET, BY BATTERY CAPACITY, 2026 VS. 2033 (UNITS)

- FIGURE 49 ELECTRIC COMMERCIAL VEHICLE MARKET, BY REGION, 2026 VS. 2033 (USD MILLION)

- FIGURE 50 ASIA PACIFIC: ELECTRIC COMMERCIAL VEHICLE MARKET SNAPSHOT

- FIGURE 51 SOUTHEAST ASIA: ELECTRIC COMMERCIAL VEHICLE MARKET SNAPSHOT

- FIGURE 52 NORTH AMERICA: EV BATTERY INITIATIVES

- FIGURE 53 NORTH AMERICA: ELECTRIC COMMERCIAL VEHICLE MARKET SNAPSHOT

- FIGURE 54 ELECTRIC COMMERCIAL VEHICLE DEMAND, BY COMPANY TYPE

- FIGURE 55 EUROPE: ELECTRIC COMMERCIAL VEHICLE MARKET SNAPSHOT

- FIGURE 56 REST OF THE WORLD: ELECTRIC COMMERCIAL VEHICLE MARKET SNAPSHOT

- FIGURE 57 ELECTRIC COMMERCIAL VEHICLE MARKET SHARE ANALYSIS (BUS & TRUCK MANUFACTURERS), 2025

- FIGURE 58 ELECTRIC COMMERCIAL VEHICLE MARKET SHARE ANALYSIS (LCV MANUFACTURERS), 2025

- FIGURE 59 ELECTRIC COMMERCIAL VEHICLE MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2021-2025

- FIGURE 60 COMPANY VALUATION OF KEY PLAYERS, 2025 (USD BILLION)

- FIGURE 61 FINANCIAL METRICS OF KEY PLAYERS (EV/EBITDA), 2025

- FIGURE 62 ELECTRIC COMMERCIAL VEHICLE MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 63 ELECTRIC COMMERCIAL VEHICLE MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 64 ELECTRIC COMMERCIAL VEHICLE MARKET: COMPANY FOOTPRINT, 2025

- FIGURE 65 ELECTRIC COMMERCIAL VEHICLE MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2025

- FIGURE 66 XCMG GLOBAL: COMPANY SNAPSHOT

- FIGURE 67 FAW GROUP: COMPANY SNAPSHOT

- FIGURE 68 CNHTC: COMPANY SNAPSHOT

- FIGURE 69 YUTONG BUS CO., LTD.: COMPANY SNAPSHOT

- FIGURE 70 BEIJING AUTOMOTIVE GROUP CO., LTD.: COMPANY SNAPSHOT

- FIGURE 71 DONGFENG MOTOR CORPORATION: COMPANY SNAPSHOT

- FIGURE 72 BYD: COMPANY SNAPSHOT

- FIGURE 73 DAIMLER GROUP AG: COMPANY SNAPSHOT

- FIGURE 74 DAIMLER GROUP AG

- FIGURE 75 AB VOLVO: COMPANY SNAPSHOT

- FIGURE 76 FORD MOTOR COMPANY: COMPANY SNAPSHOT

- FIGURE 77 FORD MOTOR COMPANY: ROAD TO CARBON NEUTRALITY

- FIGURE 78 TESLA, INC.: COMPANY SNAPSHOT

- FIGURE 79 TESLA, INC.: ROADMAP

- FIGURE 80 HYUNDAI MOTOR COMPANY: COMPANY SNAPSHOT

- FIGURE 81 NFI GROUP: COMPANY SNAPSHOT

- FIGURE 82 RESEARCH DESIGN

- FIGURE 83 RESEARCH PROCESS FLOW

- FIGURE 84 KEY INSIGHTS FROM INDUSTRY EXPERTS

- FIGURE 85 BREAKDOWN OF PRIMARY INTERVIEWS

- FIGURE 86 MARKET ESTIMATION METHODOLOGY

- FIGURE 87 BOTTOM-UP APPROACH

- FIGURE 88 TOP-DOWN APPROACH

- FIGURE 89 DATA TRIANGULATION

- FIGURE 90 MARKET GROWTH PROJECTIONS FROM DEMAND-SIDE DRIVERS AND OPPORTUNITIES

商用電動車市場預測至2034年-全球分析(按車輛類型、驅動系統、電池類型、電池容量、續航里程、充電方式、最終用戶和地區分類)

商用電動車市場預測至2034年-全球分析(按車輛類型、驅動系統、電池類型、電池容量、續航里程、充電方式、最終用戶和地區分類) 電動商用車市場規模、佔有率和趨勢分析報告:按車輛類型、推進系統、驅動系統、車速、地區和細分市場預測(2026-2033 年)

電動商用車市場規模、佔有率和趨勢分析報告:按車輛類型、推進系統、驅動系統、車速、地區和細分市場預測(2026-2033 年) 2026-2030年全球電動商用車(ECV)市場

2026-2030年全球電動商用車(ECV)市場 2026年全球中重型商用電動車市場報告2026年全球商用電動車市場報告

2026年全球中重型商用電動車市場報告2026年全球商用電動車市場報告 電動商用車市場:2026-2032年全球市場預測(按車輛類型、充電基礎設施、推進系統、驅動系統、車速、應用和最終用途產業分類)

電動商用車市場:2026-2032年全球市場預測(按車輛類型、充電基礎設施、推進系統、驅動系統、車速、應用和最終用途產業分類) 全球電動商用車MRO市場規模、佔有率、趨勢與成長分析報告(2026-2034年)

全球電動商用車MRO市場規模、佔有率、趨勢與成長分析報告(2026-2034年) 2026 年至 2035 年電動商用車的市場機會、成長要素、產業趨勢分析與預測。電動商用車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球工業電動車市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026 年至 2035 年電動商用車的市場機會、成長要素、產業趨勢分析與預測。電動商用車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球工業電動車市場規模、佔有率、趨勢和成長分析報告(2026-2034年)