|

市場調查報告書

商品編碼

2027002

全球醫用黏合劑市場:按技術、樹脂類型、應用和地區分類-預測(至2031年)Medical Adhesives Market by Technology (Water-Based, Solvent-Based, Solid & Hot Melt Based), Resin Type (Natural Resin, Synthetic & Semi-Synthetic Resin), Application (Dental, Surgery, Medical Device & Equipment), And Region - Global Forecast To 2031 |

||||||

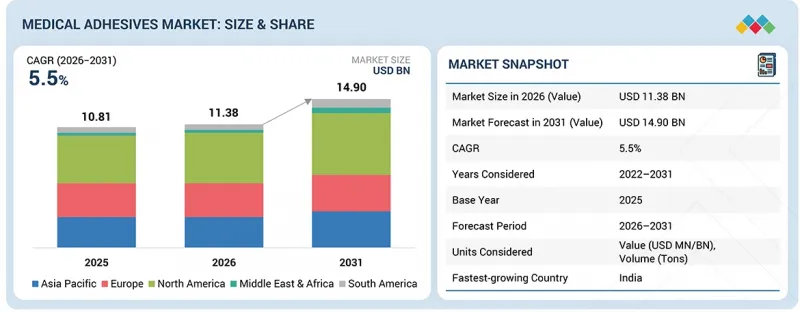

全球醫用黏合劑市場預計將從 2026 年的 113.8 億美元成長到 2031 年的 149 億美元,預測期內複合年成長率為 5.5%。

| 調查範圍 | |

|---|---|

| 調查期 | 2022-2031 |

| 基準年 | 2025 |

| 預測期 | 2026-2031 |

| 單元 | 100萬美元,噸 |

| 部分 | 技術、樹脂類型、應用、區域 |

| 目標區域 | 歐洲、北美、亞太地區、中東和非洲、南美 |

隨著醫療機構對更強效、更佳生物相容性和更耐用的黏合材料的需求不斷成長,醫用黏合劑市場也持續發展。除了外科手術數量的增加,微創手術的日益普及也推動了醫用黏合劑在醫院傷口縫合、組織封裝和止血方面的應用。

穿戴式醫療設備和經皮給藥系統的日益普及推動了對可長時間穿戴的軟性親和性黏合劑的需求。人口老化和慢性傷口患者數量的增加也提高了對先進創傷護理產品(包括敷料和密封劑)的需求。醫療設備製造業需要高性能黏合劑,這對於器械的組裝和固定至關重要。新興市場醫療設施的快速發展創造了新的機會。持續的供應端產品改進、矽丙烯酸酯黏合劑系統的開發以及對法規遵從性和永續材料使用的日益重視,正在推動產品性能的提升和市場的成長。

依技術分類,醫用黏合劑市場可分為三大類:水性黏合劑、溶劑型黏合劑和固態/熱熔型黏合劑。水性黏合劑因其優異的生物相容性、低毒性和極低的揮發性有機化合物排放而佔據市場主導地位,使其適用於皮膚接觸和創傷護理應用。這些黏合劑用於醫用膠帶、敷料和穿戴式設備,以確保患者的安全和舒適。雖然溶劑型黏合劑保持了較高的黏合強度和耐久性,但由於環境法規對溶劑排放的限制,其市場成長持續放緩。固態/熱熔型黏合劑因其固化時間短、易於加工且能有效黏合多種材料,在醫療設備組裝和衛生應用中越來越廣泛的應用。隨著對不含毒性成分的環保產品的法規日益嚴格,以及醫療領域對安全有效解決方案的需求不斷成長,水性黏合劑在市場中佔據主導地位。

從樹脂類型來看,醫用黏合劑市場可分為三大類:纖維蛋白基黏合劑、膠原蛋白基黏合劑和其他醫用黏合劑產品。纖維蛋白基黏合劑因其優異的生物相容性以及在人體自然癒合過程中作為天然成分發揮作用而佔據最大的市場佔有率。纖維蛋白基黏合劑源自人類或動物血漿成分,可形成完整的血液凝固系統,外科醫生將其用於止血、組織封裝和傷口縫合。在醫療領域,這些產品用於心血管外科、整形外科和普通外科手術,以控制出血、加速患者癒合,同時降低不良健康反應的風險。膠原蛋白蛋白基黏合劑因其優異的組織相容性(可促進細胞增殖)而日益普及,尤其是在創傷護理和再生醫學領域。合成黏合劑用於需要強黏合力和可控分解的特殊應用,其中氰基丙烯酸酯和聚乙二醇 (PEG) 基配方是首選的樹脂類型。由於纖維蛋白基黏合劑使用安全、在緊急醫療環境中效果顯著,以及現代醫學對生物基醫療解決方案的需求不斷成長,因此它仍然是首選。

從區域來看,亞太地區是醫用黏合劑市場成長最快的地區。這主要得益於中國、印度和東南亞醫療設施的快速發展,以及人口成長和醫療保健支出模式的持續改善。慢性病患者數量的增加和人口老化推動了對先進創傷護理解決方案和外科治療的需求成長,進而帶動了醫用黏合劑消費量的成長。在亞太地區,由於成本低廉、政府監管支持以及外商投資增加,醫療設備製造業呈現強勁成長動能。隨著醫院、診所和門診手術中心不斷擴大業務規模,產品的使用量也不斷增加。人們對微創手術技術和最新治療方案的了解不斷加深,也催生了對優質黏合劑產品的市場需求。亞太地區醫用黏合劑市場的快速成長得益於本地製造資源的改善以及外國公司在該地區建立生產基地,從而提升了供應、分銷和營運效率。

本報告對全球醫用黏合劑市場進行了深入分析,深入探討了關鍵促進因素和限制因素、產品開發和創新以及競爭格局。

目錄

第1章:引言

第2章執行摘要

第3章 主要發現

- 醫療黏合劑市場對企業而言極具吸引力的機會

- 醫用黏合劑市場:按技術和地區分類

- 醫用黏合劑市場:依樹脂類型分類

- 醫用黏合劑市場:按應用領域分類

- 醫用黏合劑市場:按國家/地區分類

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 未滿足的需求和閒置頻段

- 醫用黏合劑市場尚未滿足的需求

- 閒置頻段的機遇

- 相互關聯的市場與跨產業機遇

- 互聯市場

- 跨部門機會

- 一級/二級/三級公司的策略性舉措

- 波特五力分析

- 價值鏈分析

- 生態系統

- 定價分析

- 平均售價:依地區分類

- 平均售價:依技術分類

- 平均售價:按申請

- 總體經濟指標

- 2025年美國關稅對醫用黏合劑市場的影響

- 主要關稅稅率

- 價格影響分析

- 國家/地區

- 對終端用戶產業的影響

- 貿易分析

- 進口方案(HS編碼300590)

- 出口方案(HS編碼300590)

- 影響客戶業務的趨勢/干擾因素

- 投資和資金籌措場景

- 案例研究

- 醫療設備製造中的生物相容性環氧樹脂封裝

- 用於長期佩戴設備的矽膠黏合劑

- 用於外科性創傷閉合的氰基丙烯酸黏合劑

- 主要會議和活動

第5章:技術進步、人工智慧的影響、專利、創新與未來應用

- 技術分析

- 主要技術

- 互補技術

- 鄰近技術

- 技術/產品藍圖

- 短期 | 基礎建設與初步商業化(2025-2027 年)

- 中期計畫 | 擴張與標準化(2027-2030 年)

- 長期 |大規模商業化與顛覆性變革(2030 年至 2030 年及以後)

- 專利分析

- 專利的法律地位

- 管轄權分析

- 未來用途

- 穿戴式和遠端監控設備

- 微創手術/機器人輔助手術

- 植入式醫療設備

- 先進的傷口護理和再生醫學

- 經皮給藥系統

- 人工智慧/生成式人工智慧對醫用黏合劑市場的影響

- 主要應用案例和市場展望

- 醫用黏合劑加工的最佳實踐

- 人工智慧在醫用黏合劑市場應用案例研究研究

- 相互關聯的鄰近生態系及其對市場參與企業的影響

- 醫療黏合劑市場中客戶對採用人工智慧生成解決方案的準備。

第6章 監理情勢與永續性舉措

- 當地法規和合規性

- 監管機構、政府機構和其他組織

- 業界標準

- 監理政策和永續性措施的影響

- 認證、標籤檢視、環境標準

第7章:顧客趨勢與購買行為

- 決策流程

- 主要相關利益者和採購標準

- 招募障礙和內部挑戰

- 各個終端用戶產業中尚未滿足的需求

- 市場盈利

- 潛在收入

- 成本動態

- 提高主要終端用戶產業利潤率的機會

第8章 醫用黏合劑市場:依樹脂類型分類

- 天然樹脂

- 合成樹脂和半合成樹脂

第9章 醫用黏合劑市場:依技術分類

- 水溶液

- 溶劑型

- 固體/熱熔型

第10章 醫用黏合劑市場:依應用領域分類

- 牙科

- 外科手術

- 醫療器材與設備

- 其他用途

第11章 醫用黏合劑市場:按地區分類

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 其他歐洲國家

- 中東和非洲

- 海灣合作理事會國家

- 南非

- 其他中東和非洲

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

第12章 競爭格局

- 概述

- 主要參與企業的策略/優勢

- 收入分析

- 市佔率分析(2025 年)

- 企業評估與財務指標

- 品牌/產品比較分析

- 企業評估矩陣:主要公司(2025 年)

- 公司評估矩陣:新創企業/中小企業(2025 年)

- 競爭格局

第13章:公司簡介

- 大公司

- SOLVENTUM(3M)

- HENKEL AG & CO, KGAA

- HB FULLER COMPANY

- SCAPA HEALTHCARE

- JOHNSON & JOHNSON(MEDTECH COMPANY)

- PERMABOND

- B. BRAUN SE

- CHEMENCE MEDICAL, INC.

- ARTIVION, INC.

- DYMAX

- BOSTIK

- 其他公司

- MEDTRONIC

- DENTSPLY SIRONA

- MASTERBOND INC.

- ASHLAND

- ADVANCED MEDICAL SOLUTIONS GROUP PLC

- HOENLE AG

- BECTON, DICKINSON AND COMPANY(BD)

- VIVOSTAT A/S

- OCULAR THERAPEUTIX, INC.

- GLAXOSMITHKLINE PLC

- NITTO DENKO CORPORATION

- BAXTER INTERNATIONAL

- CARTELL CHEMICAL CO., LTD.

- BIOSEAL INC.

第14章調查方法

第15章附錄

The medical adhesives market is projected to grow from USD 11.38 billion in 2026 to USD 14.90 billion by 2031, at a CAGR of 5.5% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million), Volume (Tons) |

| Segments | By Technology, Resin Type, Application, and Region |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and South America |

The medical adhesives market is growing as healthcare facilities need stronger, biocompatible, and durable bonding materials. The rising number of surgical procedures, together with the growing acceptance of minimally invasive procedures, is driving hospitals to use medical adhesives for wound closure, tissue sealing, and hemostasis.

The increasing use of wearable medical devices, together with transdermal drug delivery systems, creates a higher demand for skin-compatible flexible adhesives that can be worn for extended periods. The combination of growing elderly populations and rising chronic wound cases drives higher demand for advanced wound care products, including adhesive dressings and sealants. The medical device manufacturing industry requires high-performance adhesives, which are essential for assembling and fixing devices. The rapid development of healthcare facilities in emerging markets opens new business opportunities. Product performance and market growth receive boosts from ongoing supply-side product advances, the development of silicone and acrylic adhesive systems, and increased dedication to meeting regulatory requirements and using sustainable materials.

Based on technology, the medical adhesives market is divided into three segments: water-based adhesives, solvent-based adhesives, and solid & hot melt adhesives. Water-based adhesives lead the market because they provide excellent biocompatibility and low toxicity and produce minimal volatile organic compound emissions, making them suitable for skin-contact and wound care applications. Medical tapes, dressings, and wearable devices use these adhesives to ensure patient safety and comfort. The bonding strength and durability of solvent-based adhesives remain strong, yet their market growth continues to decline because of environmental regulations that restrict solvent emissions. Solid and hot-melt adhesives are now seeing increased use in medical device assembly and hygiene applications because they provide fast curing times, simple processing, and effective adhesion to multiple materials. The water-based adhesive market is the dominant force because rising regulations mandate environmentally friendly products without toxic components and because healthcare demands require both safe and effective solutions.

Based on resin type, the medical adhesives market is divided into three categories: fibrin, collagen, and other medical adhesive products. Fibrin-based adhesives maintain the largest market share because they provide better biocompatibility and function as natural components of the body healing process. Fibrin adhesives, which derive from human or animal plasma components, create a complete blood coagulation system that surgeons use for hemostasis, tissue sealing, and wound closure. The medical community uses these products because they help patients heal faster while controlling blood loss and reducing the risk of adverse health effects during cardiovascular, orthopedic, and general surgical operations. Collagen-based adhesives are becoming more popular because they provide excellent tissue compatibility, which helps cells grow, especially in wound care and regenerative medicine. Specialized applications that need strong bonding and controlled degradation use synthetic adhesives, which include cyanoacrylates and polyethylene glycol (PEG)-based formulations as their preferred resin types. Fibrin adhesives represent the preferred choice because they provide safe usage, effective results in emergency medical situations, and growing demand for biologically based medical solutions in contemporary healthcare.

Based on region, Asia Pacific represents the fastest expanding market for medical adhesives because healthcare facilities in China, India, and Southeast Asia experience rapid development while their population numbers and healthcare spending patterns continue to rise. The increasing number of chronic disease cases, together with the expanding elderly population, creates a greater need for advanced wound care solutions and surgical treatments, which results in higher consumption of medical adhesives. The region experiences strong growth in medical device manufacturing due to lower costs, supportive government regulations, and rising foreign investment. Product usage increases as hospitals, clinics, and ambulatory care centers continue to expand their operations. Rising knowledge of minimally invasive surgical methods, together with modern treatment solutions, creates a market need for superior adhesive products. The medical adhesives market in Asia Pacific experiences rapid growth because local manufacturing resources and foreign companies establishing production centers in the area enhance supply distribution and operational efficiency.

Major players operating in the market include Solventum (US), Henkel AG & Co. KGaA (Germany), H.B. Fuller Company (US), Scapa Healthcare (US), Johnson & Johnson (US), Permabond (UK), Chemence Medical, Inc (US), Artivion, Inc (US), Dymax (Ireland), and Bostik (France). These companies have dependable manufacturing facilities across the Asia Pacific region, as well as robust distribution networks. They have a well-established portfolio that includes reliable goods and services, a strong market presence, and effective business plans. These businesses also hold a sizable portion of the market, offer a broader range of products with more applications, and use cases spanning more geographic regions.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MEDICAL ADHESIVES MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MEDICAL ADHESIVES MARKET

- 3.2 MEDICAL ADHESIVES MARKET, BY TECHNOLOGY AND REGION

- 3.3 MEDICAL ADHESIVES MARKET, BY RESIN TYPE

- 3.4 MEDICAL ADHESIVES MARKET, BY APPLICATION

- 3.5 MEDICAL ADHESIVES MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising demand for minimally invasive surgeries

- 4.2.1.2 Growth in wearable and portable medical devices

- 4.2.1.3 Advancements in biocompatible and light-curable technologies

- 4.2.2 RESTRAINTS

- 4.2.2.1 Stringent regulatory requirement

- 4.2.2.2 Risk of skin irritation and biocompatibility issues

- 4.2.2.3 Availability of alternative wound closure methods

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growth in home healthcare and remote diagnostics

- 4.2.3.2 Innovations in advanced adhesive technologies

- 4.2.3.3 Integration with smart and minimally invasive surgical solutions

- 4.2.4 CHALLENGES

- 4.2.4.1 Compatibility with new medical devices

- 4.2.4.2 Technological complexity in product development

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN MEDICAL ADHESIVES MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

- 4.6 PORTER'S FIVE FORCES ANALYSIS

- 4.6.1 THREAT OF NEW ENTRANTS

- 4.6.2 THREAT OF SUBSTITUTES

- 4.6.3 BARGAINING POWER OF SUPPLIERS

- 4.6.4 BARGAINING POWER OF BUYERS

- 4.6.5 INTENSITY OF COMPETITIVE RIVALRY

- 4.7 VALUE CHAIN ANALYSIS

- 4.8 ECOSYSTEM

- 4.9 PRICING ANALYSIS

- 4.9.1 AVERAGE SELLING PRICE, BY REGION

- 4.9.2 AVERAGE SELLING PRICE, BY TECHNOLOGY

- 4.9.3 AVERAGE SELLING PRICE, BY APPLICATION

- 4.10 MACROECONOMIC INDICATORS

- 4.10.1 GLOBAL GDP TRENDS

- 4.11 IMPACT OF 2025 US TARIFFS ON MEDICAL ADHESIVES MARKET

- 4.11.1 INTRODUCTION

- 4.11.2 KEY TARIFF RATES

- 4.11.3 PRICE IMPACT ANALYSIS

- 4.11.4 IMPACT ON COUNTRIES/REGIONS

- 4.11.4.1 US

- 4.11.4.2 Europe

- 4.11.4.3 Asia Pacific

- 4.11.5 IMPACT ON END-USE INDUSTRIES

- 4.12 TRADE ANALYSIS

- 4.12.1 IMPORT SCENARIO (HS CODE 300590)

- 4.12.2 EXPORT SCENARIO (HS CODE 300590)

- 4.13 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 4.14 INVESTMENT AND FUNDING SCENARIO

- 4.15 CASE STUDIES

- 4.15.1 BIOCOMPATIBLE EPOXY ENCAPSULANTS IN MEDICAL DEVICE MANUFACTURING

- 4.15.2 SILICONE ADHESIVES FOR LONG-WEAR WEARABLE DEVICES

- 4.15.3 CYANOACRYLATE ADHESIVES FOR SURGICAL WOUND CLOSURE

- 4.16 KEY CONFERENCES & EVENTS

5 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 5.1 TECHNOLOGY ANALYSIS

- 5.1.1 KEY TECHNOLOGIES

- 5.1.1.1 Solids hot melt adhesives

- 5.1.1.2 UV curable adhesives

- 5.1.2 COMPLEMENTARY TECHNOLOGIES

- 5.1.2.1 Water-based (emulsion) adhesives

- 5.1.2.2 Silicone-based adhesives

- 5.1.3 ADJACENT TECHNOLOGIES

- 5.1.3.1 Medical sealants & hemostats

- 5.1.1 KEY TECHNOLOGIES

- 5.2 TECHNOLOGY/PRODUCT ROADMAP

- 5.2.1 SHORT TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 5.2.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 5.2.3 LONG TERM (2030-2030+) | MASS COMMERCIALIZATION & DISRUPTION

- 5.3 PATENT ANALYSIS

- 5.3.1 LEGAL STATUS OF PATENTS

- 5.3.2 JURISDICTION ANALYSIS

- 5.4 FUTURE APPLICATIONS

- 5.4.1 WEARABLE & REMOTE MONITORING DEVICES

- 5.4.2 MINIMALLY INVASIVE & ROBOTIC SURGERIES

- 5.4.3 IMPLANTABLE MEDICAL DEVICES

- 5.4.4 ADVANCED WOUND CARE & REGENERATIVE MEDICINE

- 5.4.5 TRANSDERMAL DRUG DELIVERY SYSTEMS

- 5.5 IMPACT OF AI/GEN AI ON MEDICAL ADHESIVES MARKET

- 5.5.1 TOP USE CASES AND MARKET POTENTIAL

- 5.5.2 BEST PRACTICES IN MEDICAL ADHESIVES PROCESSING

- 5.5.3 CASE STUDIES OF AI IMPLEMENTATION IN MEDICAL ADHESIVES MARKET

- 5.5.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 5.5.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN MEDICAL ADHESIVES MARKET

6 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 6.1 REGIONAL REGULATIONS AND COMPLIANCE

- 6.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.1.2 INDUSTRY STANDARDS

- 6.2 IMPACT OF REGULATORY POLICIES AND SUSTAINABILITY INITIATIVES

- 6.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

7 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.1 INTRODUCTION

- 7.2 DECISION-MAKING PROCESS

- 7.3 KEY STAKEHOLDERS AND BUYING CRITERIA

- 7.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.3.2 BUYING CRITERIA

- 7.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 7.5 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 7.6 MARKET PROFITABILITY

- 7.6.1 REVENUE POTENTIAL

- 7.6.2 COST DYNAMICS

- 7.6.3 MARGIN OPPORTUNITIES IN KEY END-USE INDUSTRIES

8 MEDICAL ADHESIVES MARKET, BY RESIN TYPE

- 8.1 INTRODUCTION

- 8.2 NATURAL RESIN

- 8.2.1 GROWING PREFERENCE FOR BIOCOMPATIBLE AND BIO-BASED SOLUTIONS DRIVING ADOPTION

- 8.2.2 FIBRIN

- 8.2.2.1 Rising surgical procedures boosting adoption of fibrin-based medical adhesives

- 8.2.3 COLLAGEN

- 8.2.3.1 Expanding advanced wound care applications driving demand

- 8.2.4 OTHER NATURAL RESINS

- 8.3 SYNTHETIC & SEMI-SYNTHETIC RESIN

- 8.3.1 RISING DEMAND FOR HIGH-PERFORMANCE AND DURABLE BONDING SOLUTIONS DRIVING MARKET GROWTH

- 8.3.2 ACRYLIC

- 8.3.2.1 Growing adoption of wearable medical devices driving demand

- 8.3.3 SILICONE

- 8.3.3.1 Increasing demand for gentle, skin-friendly adhesion driving adoption

- 8.3.4 CYANOACRYLATE

- 8.3.4.1 Rising preference for sutureless wound closure to support market growth

- 8.3.5 EPOXY

- 8.3.5.1 Demand for high-strength bonding in medical device assembly to drive growth

- 8.3.6 POLYURETHANE

- 8.3.6.1 Need for flexible and durable medical materials fueling demand

- 8.3.7 OTHER SYNTHETIC & SEMI-SYNTHETIC RESINS

9 MEDICAL ADHESIVES MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 WATER-BASED

- 9.2.1 RISING DEMAND FOR BIOCOMPATIBLE AND SKIN-FRIENDLY SOLUTIONS DRIVING ADOPTION

- 9.3 SOLVENT-BASED

- 9.3.1 HIGH BOND STRENGTH AND DURABILITY DRIVING DEMAND FOR SOLVENT-BASED MEDICAL ADHESIVES

- 9.4 SOLID & HOT MELT-BASED

- 9.4.1 FAST PROCESSING AND SOLVENT-FREE FORMULATION DRIVING ADOPTION OF HOT MELT MEDICAL ADHESIVES

10 MEDICAL ADHESIVES MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 DENTAL

- 10.2.1 RISING DEMAND FOR COSMETIC AND RESTORATIVE DENTISTRY DRIVING MARKET GROWTH

- 10.3 SURGERY

- 10.3.1 GROWING SHIFT TOWARD MINIMALLY INVASIVE PROCEDURES DRIVING ADOPTION

- 10.3.2 INTERNAL

- 10.3.2.1 Increasing complex surgical procedures driving demand for internal medical adhesives

- 10.3.3 EXTERNAL

- 10.3.3.1 Rising preference for sutureless skin closure driving external adhesives demand

- 10.4 MEDICAL DEVICE & EQUIPMENT

- 10.4.1 RAPID GROWTH OF WEARABLE AND MINIATURIZED DEVICES DRIVING DEMAND

- 10.5 OTHER APPLICATIONS

11 MEDICAL ADHESIVES MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Rising surgical volumes and advanced healthcare infrastructure driving demand

- 11.2.2 CANADA

- 11.2.2.1 Growing surgical procedures and aging population fueling demand

- 11.2.3 MEXICO

- 11.2.3.1 Expanding medical device manufacturing and healthcare infrastructure driving market growth

- 11.2.1 US

- 11.3 ASIA PACIFIC

- 11.3.1 CHINA

- 11.3.1.1 Massive healthcare expansion and government support driving demand

- 11.3.2 INDIA

- 11.3.2.1 Expanding healthcare coverage and rising surgical volumes fueling market growth

- 11.3.3 JAPAN

- 11.3.3.1 Rapidly aging population driving demand for advanced medical adhesives

- 11.3.4 SOUTH KOREA

- 11.3.4.1 Presence of advanced medical device industry driving medical adhesives demand

- 11.3.5 REST OF ASIA PACIFIC

- 11.3.1 CHINA

- 11.4 EUROPE

- 11.4.1 GERMANY

- 11.4.1.1 Strong healthcare infrastructure and high surgical volumes driving demand

- 11.4.2 FRANCE

- 11.4.2.1 Advanced healthcare systems and rising surgical procedures fueling market growth

- 11.4.3 UK

- 11.4.3.1 E-commerce sales to drive market expansion

- 11.4.4 ITALY

- 11.4.4.1 Rapidly aging population fueling demand for advanced wound care and surgical adhesives

- 11.4.5 SPAIN

- 11.4.5.1 Growing aging population and chronic disease burden driving demand

- 11.4.6 REST OF EUROPE

- 11.4.1 GERMANY

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.5.1.1 Saudi Arabia

- 11.5.1.1.1 Vision 2030 healthcare investments accelerating market growth

- 11.5.1.2 Rest of GCC

- 11.5.1.1 Saudi Arabia

- 11.5.2 SOUTH AFRICA

- 11.5.2.1 Rising chronic disease burden and healthcare expansion supporting market growth

- 11.5.3 REST OF MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.6 SOUTH AMERICA

- 11.6.1 BRAZIL

- 11.6.1.1 Expanding public healthcare system driving medical adhesives demand

- 11.6.2 ARGENTINA

- 11.6.2.1 Rising chronic disease burden accelerating demand

- 11.6.3 REST OF SOUTH AMERICA

- 11.6.1 BRAZIL

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS, 2025

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.6 BRAND/PRODUCT COMPARISON ANALYSIS

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Overall company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Technology footprint

- 12.7.5.4 Resin type footprint

- 12.7.5.5 Application footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2025

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

- 12.9.4 OTHERS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 SOLVENTUM (3M)

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Others

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 HENKEL AG & CO, KGAA

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 H.B. FULLER COMPANY

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 SCAPA HEALTHCARE

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 JOHNSON & JOHNSON (MEDTECH COMPANY)

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 MnM view

- 13.1.5.3.1 Key strengths

- 13.1.5.3.2 Strategic choices

- 13.1.5.3.3 Weaknesses and competitive threats

- 13.1.6 PERMABOND

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 MnM view

- 13.1.7 B. BRAUN SE

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 MnM view

- 13.1.8 CHEMENCE MEDICAL, INC.

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Others

- 13.1.8.4 MnM view

- 13.1.9 ARTIVION, INC.

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 MnM view

- 13.1.10 DYMAX

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 MnM view

- 13.1.11 BOSTIK

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Solutions/Services offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Deals

- 13.1.11.4 MnM view

- 13.1.1 SOLVENTUM (3M)

- 13.2 OTHER PLAYERS

- 13.2.1 MEDTRONIC

- 13.2.2 DENTSPLY SIRONA

- 13.2.3 MASTERBOND INC.

- 13.2.4 ASHLAND

- 13.2.5 ADVANCED MEDICAL SOLUTIONS GROUP PLC

- 13.2.6 HOENLE AG

- 13.2.7 BECTON, DICKINSON AND COMPANY (BD)

- 13.2.8 VIVOSTAT A/S

- 13.2.9 OCULAR THERAPEUTIX, INC.

- 13.2.10 GLAXOSMITHKLINE PLC

- 13.2.11 NITTO DENKO CORPORATION

- 13.2.12 BAXTER INTERNATIONAL

- 13.2.13 CARTELL CHEMICAL CO., LTD.

- 13.2.14 BIOSEAL INC.

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 List of key secondary sources

- 14.1.1.2 Key data from secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 Key data from primary sources

- 14.1.2.2 List of primary interview participants-demand and supply side

- 14.1.2.3 Key industry insights

- 14.1.2.4 Breakdown of interviews with experts

- 14.1.1 SECONDARY DATA

- 14.2 MARKET SIZE ESTIMATION

- 14.2.1 BOTTOM-UP APPROACH

- 14.2.2 TOP-DOWN APPROACH

- 14.3 FORECAST NUMBER CALCULATION

- 14.4 DATA TRIANGULATION

- 14.5 FACTOR ANALYSIS

- 14.6 ASSUMPTIONS

- 14.7 LIMITATIONS & RISKS

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS

List of Tables

- TABLE 1 MEDICAL ADHESIVES MARKET: IMPACT OF PORTER'S FIVE FORCES

- TABLE 2 MEDICAL ADHESIVES MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 3 PROJECTED REAL GDP GROWTH (ANNUAL PERCENT CHANGE) OF KEY COUNTRIES, 2021-2030

- TABLE 4 HEALTH EXPENDITURE AS PERCENTAGE OF GDP, 2019-2020

- TABLE 5 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 6 IMPORT DATA FOR HS CODE 300590-COMPLIANT PRODUCTS, 2021-2024 (USD THOUSAND)

- TABLE 7 EXPORT DATA FOR HS CODE 300590-COMPLIANT PRODUCTS, 2021-2024 (USD THOUSAND)

- TABLE 8 MEDICAL ADHESIVES MARKET: CONFERENCES & EVENTS, 2026-2027

- TABLE 9 TOP USE CASES AND MARKET POTENTIAL

- TABLE 10 BEST PRACTICES: NOTABLE INDUSTRY PRACTICES BY LEADING COMPANIES

- TABLE 11 MEDICAL ADHESIVES MARKET: CASE STUDIES RELATED TO AI IMPLEMENTATION

- TABLE 12 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- TABLE 13 MEDICAL ADHESIVES MARKET: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 GLOBAL STANDARDS IN MEDICAL ADHESIVES MARKET

- TABLE 15 CERTIFICATIONS, LABELING, AND ECO-STANDARDS IN MEDICAL ADHESIVES MARKET

- TABLE 16 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR KEY APPLICATIONS (%)

- TABLE 17 KEY BUYING CRITERIA FOR KEY APPLICATIONS

- TABLE 18 MEDICAL ADHESIVES MARKET: UNMET NEEDS IN KEY END-USE INDUSTRIES

- TABLE 19 MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2022-2025 (USD MILLION)

- TABLE 20 MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2026-2031 (USD MILLION)

- TABLE 21 MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2022-2025 (TON)

- TABLE 22 MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2026-2031 (TON)

- TABLE 23 MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 24 MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2026-2031 (USD MILLION)

- TABLE 25 MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2022-2025 (TON)

- TABLE 26 MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2026-2031 (TON)

- TABLE 27 MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 28 MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 29 MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 30 MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 31 MEDICAL ADHESIVES MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 32 MEDICAL ADHESIVES MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 33 MEDICAL ADHESIVES MARKET, BY REGION, 2022-2025 (TON)

- TABLE 34 MEDICAL ADHESIVES MARKET, BY REGION, 2026-2031 (TON)

- TABLE 35 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 36 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 37 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2022-2025 (TON)

- TABLE 38 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2026-2031 (TON)

- TABLE 39 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 40 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2026-2031 (USD MILLION)

- TABLE 41 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2022-2025 (TON)

- TABLE 42 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2026-2031 (TON)

- TABLE 43 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2022-2025 (USD MILLION)

- TABLE 44 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2026-2031 (USD MILLION)

- TABLE 45 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2022-2025 (TON)

- TABLE 46 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2026-2031 (TON)

- TABLE 47 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 48 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 49 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 50 NORTH AMERICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 51 US: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 52 US: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 53 US: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 54 US: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 55 CANADA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 56 CANADA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 57 CANADA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 58 CANADA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 59 MEXICO: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 60 MEXICO: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 61 MEXICO: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 62 MEXICO: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 63 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 64 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 65 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2022-2025 (TON)

- TABLE 66 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2026-2031 (TON)

- TABLE 67 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 68 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2026-2031 (USD MILLION)

- TABLE 69 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2022-2025 (TON)

- TABLE 70 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2026-2031 (TON)

- TABLE 71 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2022-2025 (USD MILLION)

- TABLE 72 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2026-2031 (USD MILLION)

- TABLE 73 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2022-2025 (TON)

- TABLE 74 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2026-2031 (TON)

- TABLE 75 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 76 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 77 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 78 ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 79 CHINA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 80 CHINA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 81 CHINA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 82 CHINA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 83 INDIA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 84 INDIA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 85 INDIA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 86 INDIA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 87 JAPAN: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 88 JAPAN: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 89 JAPAN: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 90 JAPAN: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 91 SOUTH KOREA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 92 SOUTH KOREA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 93 SOUTH KOREA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 94 SOUTH KOREA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 95 REST OF ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 96 REST OF ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 97 REST OF ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 98 REST OF ASIA PACIFIC: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 99 EUROPE: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 100 EUROPE: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 101 EUROPE: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2022-2025 (TON)

- TABLE 102 EUROPE: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2026-2031 (TON)

- TABLE 103 EUROPE: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 104 EUROPE: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2026-2031 (USD MILLION)

- TABLE 105 EUROPE: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2022-2025 (TON)

- TABLE 106 EUROPE: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2026-2031 (TON)

- TABLE 107 EUROPE: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2022-2025 (USD MILLION)

- TABLE 108 EUROPE: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2026-2031 (USD MILLION)

- TABLE 109 EUROPE: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2022-2025 (TON)

- TABLE 110 EUROPE: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2026-2031 (TON)

- TABLE 111 EUROPE: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 112 EUROPE: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 113 EUROPE: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 114 EUROPE: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 115 GERMANY: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 116 GERMANY: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 117 GERMANY: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 118 GERMANY: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 119 FRANCE: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 120 FRANCE: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 121 FRANCE: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 122 FRANCE: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 123 UK: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 124 UK: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 125 UK: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 126 UK: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 127 ITALY: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 128 ITALY: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 129 ITALY: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 130 ITALY: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 131 SPAIN: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 132 SPAIN: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 133 SPAIN: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 134 SPAIN: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 135 REST OF EUROPE: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 136 REST OF EUROPE: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 137 REST OF EUROPE: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 138 REST OF EUROPE: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 139 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 140 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 141 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2022-2025 (TON)

- TABLE 142 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2026-2031 (TON)

- TABLE 143 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 144 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2026-2031 (USD MILLION)

- TABLE 145 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2022-2025 (TON)

- TABLE 146 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2026-2031 (TON)

- TABLE 147 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2022-2025 (USD MILLION)

- TABLE 148 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2026-2031 (USD MILLION)

- TABLE 149 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2022-2025 (TON)

- TABLE 150 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2026-2031 (TON)

- TABLE 151 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 152 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 153 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 154 MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 155 SAUDI ARABIA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 156 SAUDI ARABIA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 157 SAUDI ARABIA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 158 SAUDI ARABIA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 159 REST OF GCC: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 160 REST OF GCC: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 161 REST OF GCC: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 162 REST OF GCC: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 163 SOUTH AFRICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 164 SOUTH AFRICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 165 SOUTH AFRICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 166 SOUTH AFRICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 167 REST OF MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 168 REST OF MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 169 REST OF MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 170 REST OF MIDDLE EAST & AFRICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 171 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 172 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 173 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2022-2025 (TON)

- TABLE 174 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY COUNTRY, 2026-2031 (TON)

- TABLE 175 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 176 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2026-2031 (USD MILLION)

- TABLE 177 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2022-2025 (TON)

- TABLE 178 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY TECHNOLOGY, 2026-2031 (TON)

- TABLE 179 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2022-2025 (USD MILLION)

- TABLE 180 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2026-2031 (USD MILLION)

- TABLE 181 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2022-2025 (TON)

- TABLE 182 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY RESIN TYPE, 2026-2031 (TON)

- TABLE 183 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 184 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 185 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 186 SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 187 BRAZIL: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 188 BRAZIL: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 189 BRAZIL: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 190 BRAZIL: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 191 ARGENTINA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 192 ARGENTINA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 193 ARGENTINA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 194 ARGENTINA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 195 REST OF SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 196 REST OF SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 197 REST OF SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2022-2025 (TON)

- TABLE 198 REST OF SOUTH AMERICA: MEDICAL ADHESIVES MARKET, BY APPLICATION, 2026-2031 (TON)

- TABLE 199 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN MEDICAL ADHESIVES MARKET BETWEEN JANUARY 2020 AND MARCH 2026

- TABLE 200 MEDICAL ADHESIVES MARKET: DEGREE OF COMPETITION

- TABLE 201 MEDICAL ADHESIVES MARKET: REGION FOOTPRINT

- TABLE 202 MEDICAL ADHESIVES MARKET: TECHNOLOGY FOOTPRINT

- TABLE 203 MEDICAL ADHESIVES MARKET: RESIN TYPE FOOTPRINT

- TABLE 204 MEDICAL ADHESIVES MARKET: APPLICATION FOOTPRINT

- TABLE 205 MEDICAL ADHESIVES MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 206 MEDICAL ADHESIVES MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- TABLE 207 MEDICAL ADHESIVES MARKET: PRODUCT LAUNCHES, JANUARY 2020-MARCH 2026

- TABLE 208 MEDICAL ADHESIVES MARKET: DEALS, JANUARY 2020-MARCH 2026

- TABLE 209 MEDICAL ADHESIVES MARKET: EXPANSIONS, JANUARY 2020-MARCH 2026

- TABLE 210 MEDICAL ADHESIVES MARKET: OTHERS, JANUARY 2020-MARCH 2026

- TABLE 211 SOLVENTUM (3M): COMPANY OVERVIEW

- TABLE 212 SOLVENTUM (3M): PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 213 SOLVENTUM (3M): PRODUCT LAUNCHES

- TABLE 214 SOLVENTUM (3M): DEALS

- TABLE 215 SOLVENTUM (3M): OTHERS

- TABLE 216 HENKEL AG & CO. KGAA: COMPANY OVERVIEW

- TABLE 217 HENKEL AG & CO. KGAA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 218 HENKEL AG & CO. KGAA: PRODUCT LAUNCHES

- TABLE 219 H.B. FULLER COMPANY: COMPANY OVERVIEW

- TABLE 220 H. B. FULLER COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 221 H.B. FULLER COMPANY: PRODUCT LAUNCHES

- TABLE 222 H.B. FULLER COMPANY: DEALS

- TABLE 223 SCAPA HEALTHCARE: COMPANY OVERVIEW

- TABLE 224 SCAPA HEALTHCARE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 225 SCAPA HEALTHCARE: EXPANSIONS

- TABLE 226 JOHNSON & JOHNSON (MEDTECH COMPANY): COMPANY OVERVIEW

- TABLE 227 JOHNSON & JOHNSON (MEDTECH COMPANY): PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 228 PERMABOND: COMPANY OVERVIEW

- TABLE 229 PERMABOND: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 230 B. BRAUN SE: COMPANY OVERVIEW

- TABLE 231 B. BRAUN SE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 232 CHEMENCE MEDICAL, INC.: COMPANY OVERVIEW

- TABLE 233 CHEMENCE MEDICAL, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 234 CHEMENCE MEDICAL, INC.: OTHERS

- TABLE 235 ARTIVION, INC.: COMPANY OVERVIEW

- TABLE 236 ARTIVION, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 237 DYMAX: COMPANY OVERVIEW

- TABLE 238 DYMAX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 239 BOSTIK: COMPANY OVERVIEW

- TABLE 240 BOSTIK: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 241 BOSTIK: DEALS

- TABLE 242 MEDTRONIC: COMPANY OVERVIEW

- TABLE 243 DENTSPLY SIRONA: COMPANY OVERVIEW

- TABLE 244 MASTERBOND INC.: COMPANY OVERVIEW

- TABLE 245 ASHLAND: COMPANY OVERVIEW

- TABLE 246 ADVANCED MEDICAL SOLUTIONS GROUP PLC: COMPANY OVERVIEW

- TABLE 247 HOENLE AG: COMPANY OVERVIEW

- TABLE 248 BECTON, DICKINSON AND COMPANY (BD): COMPANY OVERVIEW

- TABLE 249 VIVOSTAT A/S: COMPANY OVERVIEW

- TABLE 250 OCULAR THERAPEUTIX, INC.: COMPANY OVERVIEW

- TABLE 251 GLAXOSMITHKLINE PLC: COMPANY OVERVIEW

- TABLE 252 NITTO DENKO CORPORATION: COMPANY OVERVIEW

- TABLE 253 BAXTER INTERNATIONAL: COMPANY OVERVIEW

- TABLE 254 CARTELL CHEMICAL CO., LTD.: COMPANY OVERVIEW

- TABLE 255 BIOSEAL INC.: COMPANY OVERVIEW

List of Figures

- FIGURE 1 MEDICAL ADHESIVES MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 KEY INSIGHTS AND MARKET HIGHLIGHTS

- FIGURE 3 MEDICAL ADHESIVES MARKET, 2026-2031

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN MEDICAL ADHESIVES MARKET, 2020-2025

- FIGURE 5 DISRUPTIONS INFLUENCING GROWTH OF MEDICAL ADHESIVES MARKET

- FIGURE 6 HIGH-GROWTH SEGMENTS IN MEDICAL ADHESIVES MARKET, 2026-2031

- FIGURE 7 ASIA PACIFIC TO REGISTER HIGHEST CAGR IN MEDICAL ADHESIVES MARKET DURING FORECAST PERIOD

- FIGURE 8 ASIA PACIFIC TO OFFER LUCRATIVE OPPORTUNITIES IN MEDICAL ADHESIVES MARKET DURING FORECAST PERIOD

- FIGURE 9 WATER-BASED ACCOUNTED FOR LARGEST MARKET SHARE IN 2025

- FIGURE 10 SYNTHETIC & SEMI-SYNTHETIC RESIN SEGMENT DOMINATED MEDICAL ADHESIVES MARKET IN 2025

- FIGURE 11 ELECTRICAL & ELECTRONICS APPLICATION ACCOUNTED FOR LARGEST MARKET SHARE IN 2025

- FIGURE 12 INDIA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 13 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN MEDICAL ADHESIVES MARKET

- FIGURE 14 MEDICAL ADHESIVES MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 15 MEDICAL ADHESIVES MARKET: VALUE CHAIN ANALYSIS

- FIGURE 16 MEDICAL ADHESIVES MARKET: ECOSYSTEM ANALYSIS

- FIGURE 17 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2025

- FIGURE 18 AVERAGE SELLING PRICE TREND, BY TECHNOLOGY, 2022-2025

- FIGURE 19 AVERAGE SELLING PRICE TREND, BY APPLICATION, 2022-2025

- FIGURE 20 IMPORT SCENARIO FOR HS CODE 300590-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2024

- FIGURE 21 EXPORT SCENARIO FOR HS CODE 300590-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2024

- FIGURE 22 DISRUPTIONS/TRENDS SHAPING MEDICAL ADHESIVES MARKET

- FIGURE 23 MEDICAL ADHESIVES MARKET: INVESTMENT AND FUNDING SCENARIO, 2023-2025

- FIGURE 24 PATENTS APPLIED AND GRANTED, 2015-2025

- FIGURE 25 PATENT ANALYSIS, BY LEGAL STATUS

- FIGURE 26 TOP JURISDICTION, BY DOCUMENT

- FIGURE 27 MEDICAL ADHESIVES MARKET: DECISION-MAKING FACTORS

- FIGURE 28 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR KEY APPLICATIONS

- FIGURE 29 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

- FIGURE 30 ADOPTION BARRIERS & INTERNAL CHALLENGES

- FIGURE 31 SYNTHETIC & SEMI-SYNTHETIC RESIN SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE DURING FORECAST PERIOD

- FIGURE 32 SOLIDS & HOT MELT-BASED SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 33 SURGERY TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 34 INDIA TO REGISTER HIGHEST CAGR IN MEDICAL ADHESIVES MARKET DURING FORECAST PERIOD

- FIGURE 35 NORTH AMERICA: MEDICAL ADHESIVES MARKET SNAPSHOT

- FIGURE 36 ASIA PACIFIC: MEDICAL ADHESIVES MARKET SNAPSHOT

- FIGURE 37 EUROPE: MEDICAL ADHESIVES MARKET SNAPSHOT

- FIGURE 38 REVENUE ANALYSIS OF KEY COMPANIES IN MEDICAL ADHESIVES MARKET, 2023-2025

- FIGURE 39 SHARES OF LEADING COMPANIES IN MEDICAL ADHESIVES MARKET, 2025

- FIGURE 40 COMPANY VALUATION OF LEADING COMPANIES IN MEDICAL ADHESIVES MARKET, 2025

- FIGURE 41 EV/EBITDA OF LEADING COMPANIES IN MEDICAL ADHESIVES MARKET, 2024

- FIGURE 42 MEDICAL ADHESIVES MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 43 MEDICAL ADHESIVES MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 44 MEDICAL ADHESIVES MARKET: OVERALL COMPANY FOOTPRINT

- FIGURE 45 MEDICAL ADHESIVES MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2025

- FIGURE 46 SOLVENTUM (3M): COMPANY SNAPSHOT

- FIGURE 47 HENKEL AG & CO. KGAA: COMPANY SNAPSHOT

- FIGURE 48 H. B. FULLER COMPANY: COMPANY SNAPSHOT

- FIGURE 49 JOHNSON & JOHNSON (MEDTECH COMPANY): COMPANY SNAPSHOT

- FIGURE 50 ARTIVION, INC.: COMPANY SNAPSHOT

- FIGURE 51 MEDICAL ADHESIVES MARKET: RESEARCH DESIGN

- FIGURE 52 MEDICAL ADHESIVES MARKET: BOTTOM-UP APPROACH

- FIGURE 53 MEDICAL ADHESIVES MARKET: TOP-DOWN APPROACH - 1

- FIGURE 54 MEDICAL ADHESIVES MARKET: TOP-DOWN APPROACH - 2

- FIGURE 55 MEDICAL ADHESIVES MARKET: DEMAND-SIDE FORECAST

- FIGURE 56 MEDICAL ADHESIVES MARKET: DATA TRIANGULATION

醫用黏合劑市場:按產品類型、原料、應用和最終用戶分類-2026-2032年全球市場預測醫用黏合劑和密封劑市場:按類型、應用、劑型、包裝和技術分類-2026-2032年全球市場預測

醫用黏合劑市場:按產品類型、原料、應用和最終用戶分類-2026-2032年全球市場預測醫用黏合劑和密封劑市場:按類型、應用、劑型、包裝和技術分類-2026-2032年全球市場預測 醫用黏合劑市場:產業趨勢與全球市場預測(至2035年)眼科黏合劑和密封劑市場:2026-2032年全球市場預測(按產品類型、配方、給藥途徑、分銷管道、應用和最終用戶分類)外科黏合劑市場:2026-2032年全球市場預測(按產品、成分、手術方法、應用和最終用戶分類)醫用皮膚科黏合劑市場:按產品類型、黏合劑類型、應用和最終用戶分類-2026-2032年全球市場預測

醫用黏合劑市場:產業趨勢與全球市場預測(至2035年)眼科黏合劑和密封劑市場:2026-2032年全球市場預測(按產品類型、配方、給藥途徑、分銷管道、應用和最終用戶分類)外科黏合劑市場:2026-2032年全球市場預測(按產品、成分、手術方法、應用和最終用戶分類)醫用皮膚科黏合劑市場:按產品類型、黏合劑類型、應用和最終用戶分類-2026-2032年全球市場預測 醫用黏合劑市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年)液態醫用黏合劑市場:依產品類型、應用、最終用戶、通路分類,全球預測(2026-2032年)

醫用黏合劑市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年)液態醫用黏合劑市場:依產品類型、應用、最終用戶、通路分類,全球預測(2026-2032年) 2026年全球醫用皮膚黏附感測器市場報告2026年全球醫用黏合劑市場報告

2026年全球醫用皮膚黏附感測器市場報告2026年全球醫用黏合劑市場報告