|

市場調查報告書

商品編碼

2083366

冷凍食品加工機械市場:商機、成長要素、產業趨勢分析及2026-2035年預測Frozen Food Processing Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

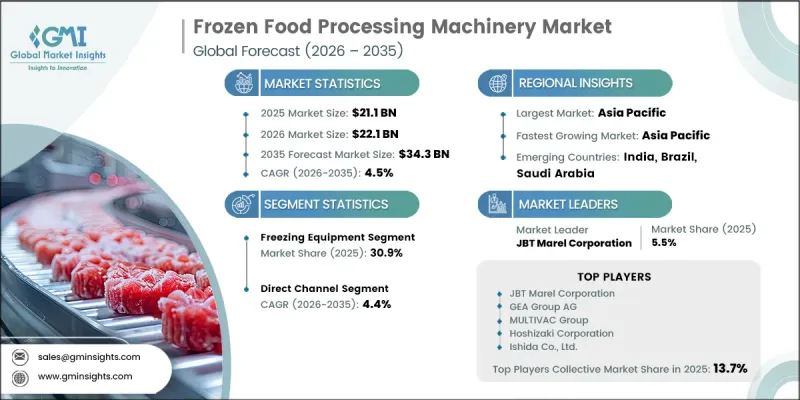

預計到 2025 年,全球冷凍食品加工機械市場價值將達到 211 億美元,並預計以 4.5% 的複合年成長率成長,到 2035 年達到 343 億美元。

冷凍食品加工機械市場的成長得益於全球冷凍食品和簡便食品食品消費量的持續成長,而這又受到生活方式改變、都市化加快、可支配收入增加以及低溫運輸基礎設施持續投資的推動。食品製造商正在擴大產能以滿足不斷成長的消費者需求,從而增加了對先進加工設備的投資。此外,不斷變化的食品安全法規和環境要求也推動了機械設備的現代化和加工設施中節能技術的應用。該行業正逐步向更環保的製冷系統轉型,並擴大自動化技術的應用,旨在提高營運效率、減少對勞動力的依賴並確保產品品質的穩定性。有組織的零售網路的擴張以及對已烹調食品和即食食品需求的成長,持續為設備製造商創造有利條件。此外,對生產現代化和加工流程最佳化的投資,正在增強已開發市場和新興市場對先進冷凍食品加工機械的長期需求,從而支撐該行業持續成長至2035年。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 211億美元 |

| 預計金額 | 343億美元 |

| 複合年成長率 | 4.5% |

預計到2025年,冷凍設備市佔率將達到30.9%,並在2035年之前以5.9%的複合年成長率成長。該細分市場佔據主導地位的主要原因是,與其他加工設備類別相比,冷凍系統需要大量的資本投資,且技術更為先進。除了冷凍技術的不斷進步外,市場對高效食品保鮮解決方案日益成長的需求也推動了該細分市場的成長。製造商正在加大對先進製冷系統的投資,以提高產品品質、提升營運效率並最佳化生產效率,從而進一步鞏固了該細分市場在市場上的主導地位。

預計到2025年,直銷通路將佔61.5%的市場佔有率,並預計在2026年至2035年間以4.4%的複合年成長率成長。這一主導地位源自於食品加工機械的技術複雜性和巨額投資。製造商與終端用戶之間的直接互動,使得製造商能夠提供客製化的設備規格、安裝支援、試運行服務和長期維護計劃。此外,直銷模式有助於建立長期的客戶關係,並透過提供備件、系統升級、校準服務和持續的技術支持,創造持續的收入,使其成為整個行業首選的分銷方式。

預計到2025年,北美冷凍食品加工機械市場佔有率將達到27.8%,並在2035年之前以4.1%的複合年成長率成長。該地區憑藉其成熟的食品加工業、持續投資提升產能以及對自動化和營運效率日益成長的重視,保持著強勁的市場地位。對先進加工機械的需求持續受到設備更新換代、現代化改造以及遵守不斷變化的食品安全法規的推動。該地區強大的冷凍食品製造基礎設施和對技術進步的投入,持續為機械供應商和設備製造商創造巨大的商機。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 全球對冷凍食品和簡便食品的需求不斷成長

- 新興市場低溫運輸基礎設施的快速擴張

- 引入自動化技術以解決食品加工行業的人手不足

- 更嚴格的食品安全法規正在推動設備的現代化。

- 產業潛在風險與挑戰

- 關鍵零件(壓縮機、冷媒)供應鏈中斷

- 先進自動化系統操作和維護熟練人員短缺

- 機會

- 高階水產品和蛋白質出口商對速凍和低溫設備的需求

- 對老舊食品加工廠維修和現代化升級

- 促進因素

- 成長潛力分析

- 監理框架

- 標準和合規要求

- 區域監理框架

- 認證標準

- 關鍵市場趨勢與顛覆性因素

- 技術與創新展望

- 當前趨勢

- 新進展

- 價格分析

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 未來市場趨勢

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 波特的分析

- PESTLE分析

- 生產能力和生產情況

- 按地區和主要設備製造商分類的裝置容量

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依機械類型分類,2022-2035年

- 預處理裝置

- 刀具

- 切片機

- 破碎機

- 攪拌機和混合機

- 漂燙機

- 擠出機和均質機

- 其他(去皮機、分裝機等)

- 冷凍設備

- 快速冷凍庫

- 螺旋式冷凍機

- 平板冷凍機

- 單體速凍(IQF)設備

- 低溫冷凍機(液態氮和二氧化碳系統)

- 其他類型(隧道式冷水機、流體化床冷水機等)

- 包裝設備

- 包裝機

- 裝袋機

- 裝盒機

- 托盤裝載機和封口機

- 其他(真空包裝機、收縮包裝機等)

- 冷氣和冷卻系統

- 快速冷卻機

- 工業製冷裝置(低全球暖化潛值冷媒系統)

- 儲藏室冷凍設備

- 其他

第6章 市場估算與預測:依冷凍技術分類,2022-2035年

- 機械冷凍

- 超低溫冷凍

第7章 市場估計與預測:依營運模式分類,2022-2035年

- 半自動

- 自動的

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 水果和蔬菜

- 乳製品

- 肉類、家禽和水產品

- 即食食品

- 烘焙產品

- 小吃

- 其他(湯、醬汁等)

第9章 市場估計與預測:依最終用途分類,2022-2035年

- 食品加工公司

- 餐廳及餐飲服務業

- 零售和超級市場

- 其他(例如,物流中心)

第10章 市場估價與預測:依通路分類,2022-2035年

- 直接的

- 間接

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第12章:公司簡介

- 世界公司

- Air Products and Chemicals, Inc.

- Business Overview

- Financial Data

- Product Landscape

- Strategic Outlook

- SWOT Analysis

- Alfa Laval AB

- Buhler Group

- GEA Group AG

- Ishida Co., Ltd.

- JBT Marel Corporation

- Linde plc

- MULTIVAC Group

- Tetra Pak International SA

- The Middleby Corporation

- Air Products and Chemicals, Inc.

- 本地公司

- Hoshizaki Corporation

- Intralox

- Nantong Sinrofreeze Equipment Co., Ltd.

- NTSquare

- OctoFrost Group

- SPX FLOW, Inc.

- Starfrost(UK)Ltd.

- 新興企業

- AMF Tech

- Nantong Icesource Coldchain Technology Co., Ltd.

- Nantong Worldbase Refrigeration Equipment Co., Ltd.

- Yurnfreeze

The Global Frozen Food Processing Machinery Market was valued at USD 21.1 billion in 2025 and is estimated to grow at a CAGR of 4.5% to reach USD 34.3 billion by 2035.

Growth in the frozen food processing machinery market is supported by the continued rise in frozen and convenience food consumption worldwide, driven by changing lifestyles, urban expansion, increasing disposable incomes, and ongoing investments in cold-chain infrastructure. Food manufacturers are expanding production capacities to meet growing consumer demand, resulting in greater investments in advanced processing equipment. In addition, evolving food safety regulations and environmental requirements are encouraging processing facilities to modernize their machinery and adopt energy-efficient technologies. The industry is also witnessing a gradual transition toward refrigeration systems with lower environmental impact, alongside increasing deployment of automation technologies designed to improve operational efficiency, reduce labor dependency, and ensure consistent product quality. Expanding organized retail networks and rising demand for ready-to-cook and ready-to-eat food products continue to create favorable conditions for equipment manufacturers. Furthermore, investments in production modernization and processing optimization are strengthening long-term demand for advanced frozen food processing machinery across both developed and emerging markets, supporting sustained industry expansion through 2035.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.1 Billion |

| Forecast Value | $34.3 Billion |

| CAGR | 4.5% |

The freezing equipment segment accounted for 30.9% share in 2025 and is projected to grow at a CAGR of 5.9% through 2035. The segment's leading position is primarily attributed to the high capital investment requirements and technological sophistication associated with freezing systems compared to other processing equipment categories. Continuous advancements in freezing technologies, coupled with increasing demand for efficient food preservation solutions, are supporting segment growth. Manufacturers are increasingly investing in advanced freezing systems that enhance product quality, improve operational efficiency, and optimize production throughput, further strengthening the segment's market leadership.

The direct sales channel represented 61.5% share in 2025 and is expected to grow at a CAGR of 4.4% during 2026-2035. The dominance of this channel is linked to the technical complexity and substantial investment associated with food processing machinery. Direct engagement between manufacturers and end users allows for customized equipment specifications, installation support, commissioning services, and long-term maintenance programs. The direct sales model also facilitates extended customer relationships and generates recurring revenue through spare parts supply, system upgrades, calibration services, and ongoing technical support, making it the preferred distribution approach across the industry.

North America Frozen Food Processing Machinery Market captured 27.8% share in 2025 and is anticipated to grow at a CAGR of 4.1% through 2035. The region continues to maintain a strong market position due to its established food processing sector, continuous investments in production capacity upgrades, and increasing focus on automation and operational efficiency. Demand for advanced processing machinery remains supported by replacement cycles, modernization initiatives, and compliance with evolving food safety regulations. The region's robust frozen food manufacturing infrastructure and commitment to technological advancement continue to create substantial opportunities for machinery suppliers and equipment manufacturers.

Major companies operating in the global frozen food processing machinery market include Air Products and Chemicals, Inc., GEA Group AG, Alfa Laval AB, Buhler Group, and AMF Tech. Companies operating in the frozen food processing machinery market are focusing on several strategic initiatives to strengthen their market position and expand their customer base. A major priority is investment in automation technologies that improve productivity, reduce labor requirements, and enhance operational efficiency. Manufacturers are also developing energy-efficient equipment and environmentally sustainable refrigeration systems to align with evolving regulatory requirements and customer sustainability goals. Strategic partnerships, acquisitions, and collaborations are being pursued to expand technological capabilities and geographic reach. In addition, companies are increasing investments in research and development to introduce innovative processing solutions with improved performance and lower operating costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 By Machinery type

- 2.2.3 By Freezing Technology

- 2.2.4 By Mode of operation

- 2.2.5 By Application

- 2.2.6 By End use

- 2.2.7 By Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global demand for frozen & convenience food products

- 3.2.1.2 Rapid cold chain infrastructure expansion in emerging markets

- 3.2.1.3 Automation adoption to address labor shortages in food processing

- 3.2.1.4 Stricter food safety regulations driving equipment upgradation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Supply chain disruptions for critical components (compressors, refrigerants)

- 3.2.2.2 Skilled workforce gaps for operating & maintaining advanced automation

- 3.2.3 Opportunities

- 3.2.3.1 IQF & cryogenic equipment demand from premium seafood & protein exporters

- 3.2.3.2 Retrofitting & modernization of legacy food processing plants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.4.1 Standards & compliance requirements

- 3.4.2 Regional regulatory frameworks

- 3.4.3 Certification standards

- 3.5 Major market trends and disruptions

- 3.6 Technology/innovation landscape

- 3.6.1 Current trends

- 3.6.2 Emerging trends

- 3.7 Pricing Analysis (driven by primary research)

- 3.7.1 Historical price trend analysis (driven by primary research)

- 3.7.2 Pricing strategy by player type (premium / value / cost- plus) (driven by primary research)

- 3.8 Future market trends

- 3.9 Trade data analysis (driven by paid database) (HS Code- 8438)

- 3.9.1 Import/export volume & value trends (driven by primary research)

- 3.9.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI- driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Equipment Producer (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Middle East and Africa

- 4.2.1.5 Latin America

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Machinery Type, 2022 - 2035 (USD Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Preparation equipment

- 5.2.1 Cutters

- 5.2.2 Slicers

- 5.2.3 Grinders

- 5.2.4 Blenders & mixers

- 5.2.5 Blanchers

- 5.2.6 Extruders & homogenizers

- 5.2.7 Others (peelers, portioning machines, etc.)

- 5.3 Freezing equipment

- 5.3.1 Blast freezers

- 5.3.2 Spiral freezers

- 5.3.3 Plate freezers

- 5.3.4 Individual quick freezing (IQF) equipment

- 5.3.5 Cryogenic Freezers (LN2 & CO2 Systems)

- 5.3.6 Others (tunnel freezers, fluidized bed freezers, etc.)

- 5.4 Packaging equipment

- 5.4.1 Wrapping machines

- 5.4.2 Bagging machines

- 5.4.3 Cartoning machines

- 5.4.4 Tray loaders & sealers

- 5.4.5 Others (vacuum packaging machines, shrink wrappers, etc.)

- 5.5 Refrigeration & cooling systems

- 5.5.1 Blast chillers

- 5.5.2 Industrial refrigeration units (low-GWP refrigerant systems)

- 5.5.3 Holding room refrigeration

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Freezing Technology, 2022 - 2035 (USD Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Mechanical freezing

- 6.3 Cryogenic freezing

Chapter 7 Market Estimates & Forecast, By Mode of Operation, 2022 - 2035 (USD Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Semi-Automatic

- 7.3 Automatic

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Fruits & vegetables

- 8.3 Dairy products

- 8.4 Meat, poultry, & seafood

- 8.5 Ready-to-eat (RTE) meals

- 8.6 Bakery products

- 8.7 Snacks

- 8.8 Others (soups, sauces, etc)

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 (USD Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Food processing companies

- 9.3 Restaurants and foodservice

- 9.4 Retail & supermarkets

- 9.5 Others (distribution centers, etc)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Companies

- 12.1.1 Air Products and Chemicals, Inc.

- 12.1.1.1 Business Overview

- 12.1.1.2 Financial Data

- 12.1.1.3 Product Landscape

- 12.1.1.4 Strategic Outlook

- 12.1.1.5 SWOT Analysis

- 12.1.2 Alfa Laval AB

- 12.1.3 Buhler Group

- 12.1.4 GEA Group AG

- 12.1.5 Ishida Co., Ltd.

- 12.1.6 JBT Marel Corporation

- 12.1.7 Linde plc

- 12.1.8 MULTIVAC Group

- 12.1.9 Tetra Pak International S.A.

- 12.1.10 The Middleby Corporation

- 12.1.1 Air Products and Chemicals, Inc.

- 12.2 Regional Companies

- 12.2.1 Hoshizaki Corporation

- 12.2.2 Intralox

- 12.2.3 Nantong Sinrofreeze Equipment Co., Ltd.

- 12.2.4 NTSquare

- 12.2.5 OctoFrost Group

- 12.2.6 SPX FLOW, Inc.

- 12.2.7 Starfrost (UK) Ltd.

- 12.3 Emerging Companies

- 12.3.1 AMF Tech

- 12.3.2 Nantong Icesource Coldchain Technology Co., Ltd.

- 12.3.3 Nantong Worldbase Refrigeration Equipment Co., Ltd.

- 12.3.4 Yurnfreeze

食品飲料加工設備市場:2026-2032年全球市場預測(依設備類型、運作模式、技術、自動化程度及最終用途分類)

食品飲料加工設備市場:2026-2032年全球市場預測(依設備類型、運作模式、技術、自動化程度及最終用途分類) 2026-2030年全球食品加工機械市場

2026-2030年全球食品加工機械市場 腰果烘焙機市場規模、佔有率及成長分析:按產品類型、加熱方式、加工能力、應用、自動化程度、分銷管道和地區分類-2026-2033年產業預測

腰果烘焙機市場規模、佔有率及成長分析:按產品類型、加熱方式、加工能力、應用、自動化程度、分銷管道和地區分類-2026-2033年產業預測 蛋清分離器市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。食品加工設備市場:2026-2032年全球市場預測(按設備類型、運作模式、加工能力、技術、應用和最終用戶分類)

蛋清分離器市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。食品加工設備市場:2026-2032年全球市場預測(按設備類型、運作模式、加工能力、技術、應用和最終用戶分類) 雞蛋加工機械市場規模、佔有率和成長分析:按產品類型、運作模式、應用、最終用戶、加工能力、分銷管道和地區分類-2026-2033年產業預測

雞蛋加工機械市場規模、佔有率和成長分析:按產品類型、運作模式、應用、最終用戶、加工能力、分銷管道和地區分類-2026-2033年產業預測 食品飲料加工設備市場規模、佔有率及成長分析:依設備功能、應用及地區分類-產業預測,2026-2033年

食品飲料加工設備市場規模、佔有率及成長分析:依設備功能、應用及地區分類-產業預測,2026-2033年 2026年全球害蟲防治設備市場報告2026年全球甜瓜加工設備市場報告2026年全球莎莎醬加工設備市場報告

2026年全球害蟲防治設備市場報告2026年全球甜瓜加工設備市場報告2026年全球莎莎醬加工設備市場報告