|

市場調查報告書

商品編碼

2083249

蛋清分離器市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。Egg Separator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

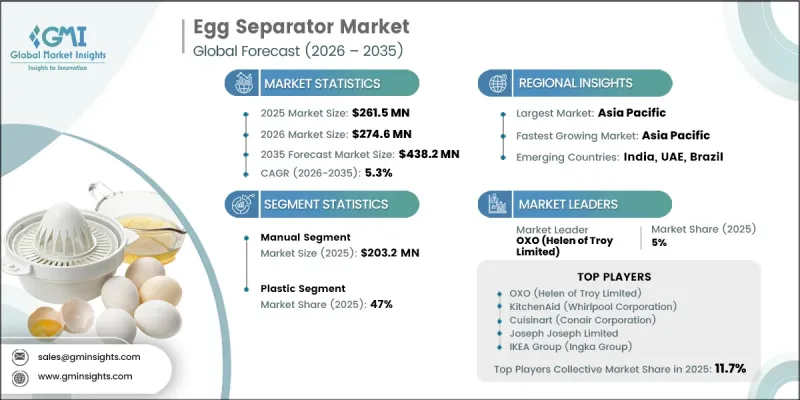

全球蛋清分離器市場預計到 2025 年將達到 2.615 億美元,並以 5.3% 的複合年成長率成長,到 2035 年將達到 4.382 億美元。

蛋黃分離器是一種專門用於高效分離蛋黃和蛋白的廚房用具,是烘焙、糕點製作、烹飪和食品加工等行業不可或缺的工具。全球雞蛋消費量的成長、現代廚房小工具的日益普及、家用廚具的日益精細化以及線上零售生態系統的快速發展,共同推動了蛋黃分離器市場的擴張。全球蛋黃分離器產業也正在經歷結構性變革,包括產品創新、材料偏好、使用模式和分銷網路等方面的變化。儘管蛋黃分離器仍被歸類為基本廚房用具,但隨著消費者對便利性、耐用性和設計效率的期望不斷提高,市場格局正在重塑。都市化進程的加速、中產階級的壯大以及家庭烹飪習慣的改變,都為此成長提供了強而有力的支撐。亞太地區在市場規模和成長動能方面均處於領先地位,這得益於該地區較高的雞蛋產量和消費量、快速的都市化以及東亞家庭對廚具的強勁需求。同時,數位化零售通路正在改變消費者的購買行為,線上平台也逐漸取代傳統的實體零售店。隨著品牌不斷強化自身銷售管道,直接面對消費者的線上商店的擴張速度超過了第三方電商平台。相較之下,在已開發市場,由於購物中心客流量下降和消費者購買偏好的改變,線下零售通路正面臨壓力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 2.615億美元 |

| 預測金額 | 4.382億美元 |

| 複合年成長率 | 5.3% |

預計到2025年,手動蛋黃分離器市場規模將達到2.032億美元。該細分市場持續佔據主導地位,主要得益於其低成本、易用性以及在家庭和小規模餐飲企業中日益普及。手動蛋黃分離器無需用電、維護成本低,且功能實用,能夠滿足日常烹飪和烘焙需求,因此仍然廣受歡迎。

預計到2025年,塑膠製品將佔蛋清分離器市場佔有率的47%。由於價格實惠且易於大規模生產,塑膠仍然是蛋白分離器製造中最常用的材料。然而,由於消費者對不銹鋼和矽膠等更耐用替代品的需求不斷成長,以及多個地區對塑膠使用的監管日益嚴格,塑膠製品市場正面臨越來越大的挑戰。此外,消費者環保意識的增強也影響他們的偏好,他們正逐漸轉向更永續性、更耐用、使用壽命更長的可重複使用廚房用具。

預計到2025年,美國蛋白分離器市場將佔據89.9%的佔有率,銷售額將達到6,240萬美元。該市場已顯露出成熟跡象,尤其是在低價位區間,入門級產品的普及率已接近飽和。這促使競爭對手將重心轉向高級產品,從塑膠材質轉向更高品質的替代材料,並更依賴線上銷售管道。蛋類烹飪的廣泛消費趨勢將繼續支撐廚房蛋白分離器的長期穩定需求。

目錄

第1章:調查方法

第2章執行摘要

第3章 行業洞察

- 產業生態系分析與價值鏈分析

- 原料和零件供應商

- 製造商和組裝

- 銷售代理商和批發商

- 零售商和最終用戶

- 對整個價值鏈的利潤率進行分析

- 影響產業的因素

- 市場促進因素

- 市場挑戰與陷阱

- 市場機遇

- 成長潛力分析

- 產業生態系分析

- 監理框架

- 食品接觸材料安全標準(FDA、歐盟法規 10/2011)

- 區域性雙酚A和化學品法規

- 產品安全和標籤合規性(CPSC、CE標誌)

- 影響廚具的永續性和可回收性法規

- 價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 技術與創新展望

- 新興過濾技術

- 智慧過濾器和具有狀態監控功能的過濾器

- 高壓高效過濾技術的創新

- 波特的分析

- PESTLE分析

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅對廚具經銷的影響

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧驅動的產品設計與消費者個人化轉型。

- GenAI 的應用案例和按細分市場(DTC 品牌、零售商)分類的實施藍圖

- 風險、限制和監管考量

- 目前分銷基礎設施和通路滲透情況

- 按地區與業態(現代零售與傳統零售)分類的通路覆蓋率

- 最後一公里基礎設施差異和不斷演變的管道(準商務、社交商務)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 手動的

- 電的

第6章 市場估計與預測:依材料分類,2022-2035年

- 塑膠

- 不銹鋼

- 矽酮

- 其他

第7章 市場估計與預測:依價格區間分類,2022-2035年

- 低價(低於 10 美元)

- 中價位(10-30美元)

- 高價(超過 30 美元)

第8章 市場估計與預測:依產能分類,2022-2035年

- 1個雞蛋

- 多枚卵

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 住宅

- 商業的

- 商用麵包店

- 餐廳餐飲服務

- 適用於機構用途(飯店、烹飪學校、醫院廚房)

- 其他(食品加工廠、食材自煮包製造商)

第10章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務平台

- 品牌/企業網站(D2C)

- 離線

- 廚具專賣店

- 大型零售/大賣場

- 其他(百貨公司、家居建材商店)

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第12章:公司簡介

- 世界頂尖公司

- KitchenAid

- Cuisinart

- OXO

- Joseph Joseph

- IKEA Group

- Kuhn Rikon

- Chef'n Corporation

- 本地公司

- Good Cook(Bradshaw Home)

- Norpro

- Prepworks by Progressive International

- Trudeau Corporation

- Tovolo

- MSC International(Joie)

- RSVP International

- 小眾及專業公司

- Fox Run Brands

- Hutzler Manufacturing Company

- Westmark GmbH

- Chef Craft

- Pampered Chef

- Wilton Brands

- Lakeland

The Global Egg Separator Market was valued at USD 261.5 million in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 438.2 million by 2035.

Egg separators are specialized kitchen tools designed to efficiently divide egg yolks from egg whites, serving as an essential utility in baking, confectionery preparation, culinary applications, and food processing workflows. The market is expanding due to a combination of rising egg consumption globally, increasing adoption of modern kitchen gadgets, premiumization of household cooking tools, and the rapid expansion of online retail ecosystems. The global egg separator industry is also undergoing structural changes across product innovation, material preferences, usage patterns, and distribution networks. Although still categorized as a basic kitchen accessory, the market is being reshaped by shifting consumer expectations toward convenience, durability, and design efficiency. Growth is strongly supported by increasing urbanization, expanding middle-class populations, and evolving home cooking habits. The Asia Pacific region leads both in market size and growth momentum, supported by high egg production and consumption levels, rapid urban expansion, and strong demand for kitchen utility products across East Asian households. At the same time, digital retail channels are transforming purchasing behavior, with online platforms increasingly replacing traditional retail outlets. Direct-to-consumer digital storefronts are expanding faster than third-party marketplaces as brands strengthen their owned sales channels. In contrast, offline retail channels are facing pressure due to reduced mall traffic and shifting consumer buying preferences in developed markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $261.5 Million |

| Forecast Value | $438.2 Million |

| CAGR | 5.3% |

The manual egg separator segment accounted for USD 203.2 million in 2025. This segment continues to lead the market due to its low cost, ease of use, and widespread adoption across households and small-scale food service operations. Manual separators remain popular because they do not require electricity, involve minimal maintenance, and offer practical functionality for everyday cooking and baking needs.

The plastic-based segment held 47% share in 2025. Plastic remains the most widely used material in egg separator manufacturing due to its affordability and mass production efficiency. However, the segment is increasingly challenged by growing demand for more durable alternatives such as stainless steel and silicone, along with tightening regulatory actions targeting plastic usage in multiple regions. Rising environmental awareness is also influencing consumer preferences, encouraging a gradual shift toward reusable, long-lasting kitchen tools that offer better sustainability performance and extended product lifecycles.

U.S. Egg Separator Market held 89.9% share, generating USD 62.4 million in 2025. The market is experiencing signs of maturity as household penetration levels for entry-level products approach saturation, particularly in the lower price range. This has shifted competitive focus toward premium product upgrades and material transitions from plastic to higher-end alternatives, alongside growing reliance on online distribution channels. Broader consumption trends in egg-based food preparation continue to support steady long-term demand for kitchen separation tools.

Major companies operating in the global egg separator market include OXO, KitchenAid, Joseph Joseph, Cuisinart, IKEA Group, Kuhn Rikon, Chef'n Corporation, Norpro, Good Cook (Bradshaw Home), Prepworks by Progressive International, Trudeau Corporation, Tovolo, MSC International (Joie), RSVP International, Fox Run Brands, Hutzler Manufacturing Company, Westmark GmbH, Chef Craft, Pampered Chef, Wilton Brands, and Lakeland. Companies in the egg separator market are focusing on product innovation, premium material upgrades, and ergonomic design improvements to strengthen market positioning. Manufacturers are increasingly shifting from basic plastic designs toward stainless steel and silicone-based products to meet rising sustainability expectations and durability demands. Expansion of e-commerce channels, particularly direct-to-consumer platforms, is enabling brands to improve visibility and customer engagement while reducing dependence on traditional retail networks. Firms are also investing in branding, packaging innovation, and kitchenware ecosystem integration to enhance product differentiation. Strategic collaborations with online retailers and culinary influencers are supporting stronger product promotion.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Business trends

- 2.3 Type trends

- 2.4 Material trends

- 2.5 Price range trends

- 2.6 Capacity trends

- 2.7 End use trends

- 2.8 Distribution channel trends

- 2.9 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem and value chain analysis

- 3.1.1 Raw material & component suppliers

- 3.1.2 Manufacturers & assemblers

- 3.1.3 Distributors & wholesalers

- 3.1.4 Retailers & end-users

- 3.1.5 Profit margin analysis across value chain

- 3.2 Industry impact forces

- 3.2.1 Market Driver

- 3.2.2 Market challenges/pitfalls

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Industry ecosystem analysis

- 3.5 Regulatory framework

- 3.5.1 Food contact material safety standards (FDA, EU Regulation 10/2011)

- 3.5.2 BPA & chemical restriction regulations by region

- 3.5.3 Product safety & labeling compliance (CPSC, CE marking)

- 3.5.4 Sustainability & recyclability regulations impacting kitchenware

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (driven by primary research)

- 3.6.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.7 Technology and innovation landscape

- 3.7.1 Emerging filter media technologies

- 3.7.2 Smart & condition-monitoring enabled filters

- 3.7.3 High-pressure & high-efficiency filtration innovations

- 3.8 Porter's Analysis

- 3.9 PESTEL Analysis

- 3.10 Trade data analysis (driven by primary research)

- 3.10.1 Import & export volume & value trends (HS code 8210)

- 3.10.2 Key trade corridors & tariff impact on kitchen tool flows

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption of product design & consumer personalization

- 3.11.2 GenAI use cases & adoption roadmap by segment (DTC brands, retailers)

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.12.1 Channel coverage by region & format (modern vs. traditional trade) (driven by primary research)

- 3.12.2 Last-mile infrastructure gaps & emerging channel shifts (Q-commerce, social commerce) (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 APAC

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Electric

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Stainless Steel

- 6.4 Silicone

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Price Range, 2022 - 2035 ($ Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low (< $10)

- 7.3 Medium ($10-$30)

- 7.4 High (> $30)

Chapter 8 Market Estimates and Forecast, By Capacity, 2022 - 2035 ($ Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Single Egg

- 8.3 Multi-Egg

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.3.1 Professional Bakeries

- 9.3.2 Restaurants & Catering

- 9.3.3 Institutional (Hotels, Culinary Schools, Hospital Kitchens)

- 9.3.4 Others (Food Processing Units, Meal-Kit Manufacturers)

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce Platforms

- 10.2.2 Brand/Company Websites (D2C)

- 10.3 Offline

- 10.3.1 Specialty Kitchen Stores

- 10.3.2 Mega Retail / Hypermarkets

- 10.3.3 Others (Department Stores, Home Improvement Stores)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 KitchenAid

- 12.1.2 Cuisinart

- 12.1.3 OXO

- 12.1.4 Joseph Joseph

- 12.1.5 IKEA Group

- 12.1.6 Kuhn Rikon

- 12.1.7 Chef'n Corporation

- 12.2 Regional Players

- 12.2.1 Good Cook (Bradshaw Home)

- 12.2.2 Norpro

- 12.2.3 Prepworks by Progressive International

- 12.2.4 Trudeau Corporation

- 12.2.5 Tovolo

- 12.2.6 MSC International (Joie)

- 12.2.7 RSVP International

- 12.3 Niche & Specialist Players

- 12.3.1 Fox Run Brands

- 12.3.2 Hutzler Manufacturing Company

- 12.3.3 Westmark GmbH

- 12.3.4 Chef Craft

- 12.3.5 Pampered Chef

- 12.3.6 Wilton Brands

- 12.3.7 Lakeland

食品飲料加工設備市場:2026-2032年全球市場預測(依設備類型、運作模式、技術、自動化程度及最終用途分類)

食品飲料加工設備市場:2026-2032年全球市場預測(依設備類型、運作模式、技術、自動化程度及最終用途分類) 2026-2030年全球食品加工機械市場

2026-2030年全球食品加工機械市場 腰果烘焙機市場規模、佔有率及成長分析:按產品類型、加熱方式、加工能力、應用、自動化程度、分銷管道和地區分類-2026-2033年產業預測

腰果烘焙機市場規模、佔有率及成長分析:按產品類型、加熱方式、加工能力、應用、自動化程度、分銷管道和地區分類-2026-2033年產業預測 冷凍食品加工機械市場:商機、成長要素、產業趨勢分析及2026-2035年預測食品加工設備市場:2026-2032年全球市場預測(按設備類型、運作模式、加工能力、技術、應用和最終用戶分類)

冷凍食品加工機械市場:商機、成長要素、產業趨勢分析及2026-2035年預測食品加工設備市場:2026-2032年全球市場預測(按設備類型、運作模式、加工能力、技術、應用和最終用戶分類) 雞蛋加工機械市場規模、佔有率和成長分析:按產品類型、運作模式、應用、最終用戶、加工能力、分銷管道和地區分類-2026-2033年產業預測

雞蛋加工機械市場規模、佔有率和成長分析:按產品類型、運作模式、應用、最終用戶、加工能力、分銷管道和地區分類-2026-2033年產業預測 食品飲料加工設備市場規模、佔有率及成長分析:依設備功能、應用及地區分類-產業預測,2026-2033年

食品飲料加工設備市場規模、佔有率及成長分析:依設備功能、應用及地區分類-產業預測,2026-2033年 2026年全球害蟲防治設備市場報告2026年全球甜瓜加工設備市場報告2026年全球莎莎醬加工設備市場報告

2026年全球害蟲防治設備市場報告2026年全球甜瓜加工設備市場報告2026年全球莎莎醬加工設備市場報告