|

市場調查報告書

商品編碼

2083326

活性藥物成分 (API) CDMO 的市場機會、成長要素、產業趨勢和 2026-2035 年預測。Active Pharmaceutical Ingredient CDMO Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

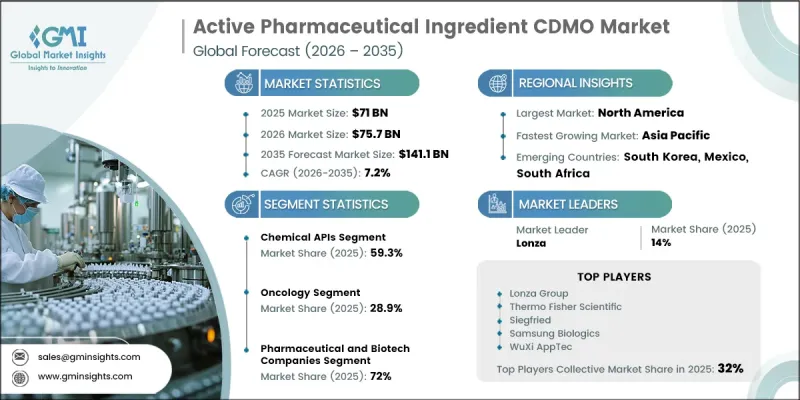

全球活性藥物成分 (API) CDMO 市場預計到 2025 年將價值 710 億美元,預計到 2035 年將以 7.2% 的複合年成長率成長至 1,411 億美元。

這一擴張是由醫藥價值鏈的結構性重組所驅動的。研發投入的增加、藥物研發管線的日益複雜以及持續的資本效率最佳化壓力,正促使創新公司更加依賴合約研發生產機構(CDMO)。同時,慢性病和感染疾病在全球日益加重,持續擴大著各個治療領域對活性藥物成分的需求。藥物治療模式的快速發展,特別是生技藥品、胜肽、寡核苷酸和抗體藥物複合體(ADC)的快速發展,推動了對先進合成能力和高度專業化生產技術的需求。目前,中小型生物技術公司在法規核准中佔據了相當大的佔有率,但它們通常缺乏內部生產基礎設施,因此與外部生產機構建立合作關係至關重要。隨著監管要求日益嚴格,研發管線的複雜性不斷增加,整個產業都在加速向靈活的委託製造網路轉型。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 710億美元 |

| 預計金額 | 1411億美元 |

| 複合年成長率 | 7.2% |

到2025年,化學原料藥領域將佔59.3%的市佔率。這一主導地位得益於全球對小分子療法的持續依賴,小分子療法將繼續構成大多數處方治療的基礎,包括心血管疾病、感染疾病和慢性病的治療。

2025年,製藥和生技產業將佔據72%的市場佔有率,成為原料藥CDMO市場的主要終端用戶群。這其中包括一些大型跨國製藥公司,它們在保留自身生產能力的同時,選擇性地將生產外包;也包括一些新興生物技術公司,它們幾乎完全依賴外部生產合作夥伴來滿足其臨床和商業化生產需求。

預計到2025年,北美活性藥物成分(API)合約研發生產(CDMO)市佔率將達到41.2%,主要得益於活躍的藥物核准環境和廣泛的生產外包。絕大多數獲準藥物都依賴外部生產的API,這反映了醫藥生態系統對契約製造的強烈依賴。基於既定GMP和品質合規標準的法律規範,正在強化一個高度結構化的商業環境,該環境有利於經驗豐富且經過嚴格審查的CDMO供應商。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 慢性病盛行率增加

- 製藥業研發活動活性化

- 對學名藥的需求不斷成長

- 外包服務的擴展

- 產業潛在風險與挑戰

- 嚴格遵守規章制度

- 價格壓力和利潤率限制

- 市場機遇

- 擴大高活躍度和複雜度 API 的生產。

- 長期策略外包夥伴關係

- 促進因素

- 成長潛力分析

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 價格趨勢分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 投資與資金籌措分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 化學原料藥

- 生物來源藥物成分

- 高活動 API

第6章 市場估計與預測:依適應症分類,2022-2035年

- 腫瘤學

- 心血管疾病

- 糖尿病

- 內分泌疾病

- 感染疾病

- 其他改編

第7章 市場估計與預測:依藥物分類,2022-2035年

- 品牌

- 非專利的

第8章 市場估算與預測:依工作流程分類,2022-2035年

- 臨床階段

- 商業的

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 人類應用

- 獸用

第10章 市場估價與預測:依最終用途分類,2022-2035年

- 製藥和生物技術公司

- 學術研究機構

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- UAE

第12章:公司簡介

- Lonza Group

- Thermo Fisher Scientific

- Catalent

- Recipharm

- Cambrex

- CordenPharma International

- Siegfried

- Boehringer Ingelheim

- Ajinomoto Biopharma Services

- Teva API(TAPI)

- Piramal Pharma Solutions

- WuXi AppTec

- Divi's Laboratories

- Aurobindo Pharma

- Dr. Reddy's Laboratories

The Global Active Pharmaceutical Ingredient CDMO Market was valued at USD 71 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 141.1 billion by 2035.

The expansion is shaped by a structural reconfiguration of the pharmaceutical value chain, where rising R&D expenditure, increasingly complex drug pipelines, and sustained pressure to optimize capital efficiency are pushing innovators to rely more heavily on contract development and manufacturing organizations. At the same time, the increasing global burden of chronic and infectious diseases continues to expand demand for active pharmaceutical ingredients across a wide range of therapies. The rapid evolution of drug modalities, particularly biologics, peptides, oligonucleotides, and antibody-drug conjugates, has intensified the need for advanced synthesis capabilities and highly specialized manufacturing expertise. Smaller biotechnology firms, which now represent a significant portion of regulatory approvals, typically lack in-house production infrastructure, making external manufacturing partnerships essential. Across the industry, pharmaceutical companies are increasingly shifting toward flexible, outsourced manufacturing networks as regulatory expectations tighten and pipeline complexity continues to rise.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $71 Billion |

| Forecast Value | $141.1 Billion |

| CAGR | 7.2% |

The chemical-based APIs segment held a 59.3% share in 2025. This dominance is supported by the continued global reliance on small-molecule therapeutics, which remain the foundation of most prescribed treatments, including cardiovascular, metabolic, infectious, and chronic disease medications.

The pharmaceutical and biotechnology segment held a 72% share in 2025, positioning them as the primary end-user group in the API CDMO landscape. This includes large multinational pharmaceutical organizations that selectively outsource production while maintaining internal capabilities, as well as emerging biotech firms that depend almost entirely on external manufacturing partners to support clinical and commercial production requirements.

North America Active Pharmaceutical Ingredient CDMO Market held a 41.2% share in 2025, supported by a highly active drug approval environment and widespread outsourcing of manufacturing activities. A significant majority of approved medicines rely on externally manufactured APIs, reflecting the strong dependence of the pharmaceutical ecosystem on contract manufacturing. Regulatory frameworks under established GMP and quality compliance standards reinforce a highly structured operating environment that favors experienced and inspection-ready CDMO providers.

Major players operating in the global active pharmaceutical ingredient CDMO industry include WuXi AppTec, Thermo Fisher Scientific, Lonza AG, Dr. Reddy's Laboratories, Catalent, Inc., Piramal Pharma Solutions, Recipharm AB, Cambrex Corporation, Siegfried Holding AG, Teva API (TAPI), Boehringer Ingelheim, Aurobindo Pharma, Divi's Laboratories, Ajinomoto Biopharma Services, and CordenPharma International. The Active Pharmaceutical Ingredient CDMO Market is being shaped by several strategic priorities adopted by leading companies to strengthen competitive positioning. Firms are heavily investing in expanding high-potency API and complex molecule manufacturing capacity to align with evolving drug pipelines. Many players are strengthening geographic footprints through facility expansions and acquisitions across North America, Europe, and Asia to ensure supply chain resilience and proximity to key clients. Long-term supply agreements with pharmaceutical innovators are increasingly used to secure predictable revenue streams and deepen client relationships. Companies are also prioritizing digital manufacturing technologies, process automation, and continuous manufacturing systems to improve efficiency and regulatory compliance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Indication trends

- 2.1.4 Drug trends

- 2.1.5 Workflow trends

- 2.1.6 Application trends

- 2.1.7 End use trends

- 2.1.8 Regional trends

- 2.2 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic disease

- 3.2.1.2 Rising R&D activities in the pharmaceutical industry

- 3.2.1.3 Rising demand for generic drugs

- 3.2.1.4 Rising adoption of outsourcing services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory compliance

- 3.2.2.2 Pricing pressure and margin constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of high-potency and complex API manufacturing

- 3.2.3.2 Long-term strategic outsourcing partnerships

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing trend analysis (Driven by primary research)

- 3.6 Regulatory landscape (Driven by primary research)

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.11 Investment & funding analysis (Driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Chemical APIs

- 5.3 Biological APIs

- 5.4 High Potent APIs

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Oncology

- 6.3 Cardiovascular diseases

- 6.4 Diabetes

- 6.5 Hormonal disorders

- 6.6 Infectious diseases

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By Drug, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Branded

- 7.3 Generic

Chapter 8 Market Estimates and Forecast, By Workflow, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Clinical

- 8.3 Commercial

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Human application

- 9.3 Veterinary application

Chapter 10 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Pharmaceutical and biotechnology companies

- 10.3 Academic and research institutes

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 France

- 11.3.3 UK

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East & Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Lonza Group

- 12.2 Thermo Fisher Scientific

- 12.3 Catalent

- 12.4 Recipharm

- 12.5 Cambrex

- 12.6 CordenPharma International

- 12.7 Siegfried

- 12.8 Boehringer Ingelheim

- 12.9 Ajinomoto Biopharma Services

- 12.10 Teva API (TAPI)

- 12.11 Piramal Pharma Solutions

- 12.12 WuXi AppTec

- 12.13 Divi’s Laboratories

- 12.14 Aurobindo Pharma

- 12.15 Dr. Reddy’s Laboratories

醫藥CDMO市場機會、成長要素、產業趨勢分析及2026-2035年預測

醫藥CDMO市場機會、成長要素、產業趨勢分析及2026-2035年預測 醫藥CDMO市場規模、佔有率和成長分析:按服務、分子類型、產品類型、劑型、最終用戶、治療領域和地區分類-2026-2033年產業預測

醫藥CDMO市場規模、佔有率和成長分析:按服務、分子類型、產品類型、劑型、最終用戶、治療領域和地區分類-2026-2033年產業預測 臨床實驗新藥(IND)CDMO市場規模、佔有率和成長分析:按服務類型、藥物類型、臨床階段、治療領域和地區分類-2026-2033年產業預測

臨床實驗新藥(IND)CDMO市場規模、佔有率和成長分析:按服務類型、藥物類型、臨床階段、治療領域和地區分類-2026-2033年產業預測 藥品研發受託製造廠商(CDMO)外包市場規模、佔有率和成長分析:按服務類型、應用和地區分類-2026-2033年產業預測

藥品研發受託製造廠商(CDMO)外包市場規模、佔有率和成長分析:按服務類型、應用和地區分類-2026-2033年產業預測 生物製品合約開發與生產組織(CDMO)的成長機會:全球,2026-2031年

生物製品合約開發與生產組織(CDMO)的成長機會:全球,2026-2031年 生物製藥CDMO市場規模、佔有率和趨勢分析報告:按產品、服務、原料、工作流程、治療領域、最終用途、地區和細分市場預測(2026-2033年)

生物製藥CDMO市場規模、佔有率和趨勢分析報告:按產品、服務、原料、工作流程、治療領域、最終用途、地區和細分市場預測(2026-2033年) 生物製藥合約開發和生產組織 (CDMO) 市場:2026-2032 年全球市場預測(按服務類型、表現系統、治療領域、開發階段和最終用戶分類)

生物製藥合約開發和生產組織 (CDMO) 市場:2026-2032 年全球市場預測(按服務類型、表現系統、治療領域、開發階段和最終用戶分類) 合約研發生產組織(CDMO)-2026-2032年全球市佔率及排名、總收入及需求預測

合約研發生產組織(CDMO)-2026-2032年全球市佔率及排名、總收入及需求預測 醫藥CDMO市場:按服務類型、技術、治療方式、最終用途、國家和地區分類-全球產業分析、市場規模、市場佔有率和預測(2025-2032年)全球小分子藥物研發原料藥、合約研發生產機構和開發機構市場:市場規模、佔有率和趨勢分析(按藥物研發階段、客戶類型、治療領域和地區分類)以及基於細分市場的預測(2026-2033 年)

醫藥CDMO市場:按服務類型、技術、治療方式、最終用途、國家和地區分類-全球產業分析、市場規模、市場佔有率和預測(2025-2032年)全球小分子藥物研發原料藥、合約研發生產機構和開發機構市場:市場規模、佔有率和趨勢分析(按藥物研發階段、客戶類型、治療領域和地區分類)以及基於細分市場的預測(2026-2033 年)