|

市場調查報告書

商品編碼

2083121

全球積層製造後後處理設備市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測Global Post Processing Equipment for Additive Manufacturing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球積層製造後處理設備市場預計到 2025 年將達到 4.55 億美元,到 2035 年將以 14.3% 的複合年成長率成長至 17.8 億美元。

然而,後處理設備在自動化技術和熱處理解決方案領域展現出強勁的發展勢頭,這使其與主流積層製造硬體的投資趨勢截然不同。設備成本降低、材料供應增加以及列印量提升,再加上已證實的投資回報,正推動後處理系統的應用群體不斷擴大。隨著積層製造進一步滲透到工業生產中,製造商面臨日益嚴格的品質保證、認證和合規要求,這需要標準化且可重複的後處理作業。這種轉變正推動著生產方式從勞力密集轉向設備主導型,從而提高單一零件的效益。此外,隨著自動化解決方案即使在較低產量下也具備經濟可行性,自動化應用的擴展正在擴大目標市場。同時,該市場也受益於有利的長期投資環境,該環境持續支持整個積層製造生態系統的資本投資。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 4.55億美元 |

| 預測金額 | 17.8億美元 |

| 複合年成長率 | 14.3% |

預計到2025年,熱處理系統市場銷售額將達到1.55億美元,市佔率為34.1%。這些系統的需求主要源於其在提升積層製造金屬零件的結構完整性、性能和可靠性方面發揮的關鍵作用,而這些零件廣泛應用於監管嚴格的行業。鑑於熱處理技術在生產流程中的核心地位,該領域持續吸引大量資本投資。隨著積層製造技術在工業應用中的普及,熱處理系統有望繼續保持主導地位,因為它們在滿足品質和性能要求方面發揮著至關重要的作用。

預計到2025年,金屬業的銷售額將達到2.18億美元,市佔率將達到47.9%。這一強勁成長主要得益於金屬積層製造技術在生產環境中的日益普及。多個終端應用領域對採用先進金屬材料製成的高性能零件的需求不斷成長,進一步推動了對旨在提升零件品質、一致性和性能的專業後處理技術的持續投資。

預計2025年,北美積層製造後處理設備市場銷售額將達1.59億美元,市佔率將達35%。美國仍然是該地區需求的主要驅動力,這得益於其積層製造活動的集中以及對先進製造技術的持續投資。成熟的工業基礎、關鍵產業對積層製造技術的日益普及以及對國內製造業創新的持續支持,都顯著推動了全部區域的市場成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應鏈分析

- 關鍵部件和關鍵材料的依賴關係

- 供應鏈脆弱性與風險映射

- 近岸外包和在地化趨勢

- 影響產業的因素

- 市場促進因素

- 積層製造作為一項產業化技術的發展,正在推動對高度擴充性的後處理解決方案的需求。

- 自動化勢在必行:人手不足正在加速新設備的引進。

- 金屬積層製造(AM)在航太和醫療領域的應用不斷擴展:需要熱處理和熱等靜壓(HIP)系統。

- 永續性和環境法規正在推動環保型後整理技術的應用。

- 市場限制因素

- 自動化後處理設備的高昂初始投資成本阻礙了中小企業採用該設備。

- 積層製造技術缺乏標準化是製程相容性的一大障礙。

- 由於危險化學品(異丙醇、活性金屬粉末)的處理要求,合規負擔加重。

- 市場機遇

- 將機器人技術和人工智慧結合,實現智慧封閉回路型後處理自動化

- 將多個後處理步驟整合到單一系統中的混合平台的出現。

- 亞太地區製造業的擴張正在創造高成長機會。

- 複合材料和陶瓷積層製造技術的發展帶來了新的設備設計要求

- 業務拓展

- 市場促進因素

- 成長潛力分析

- 技術與創新展望

- 新興的後處理技術(雷射拋光、電化學拋光、機器人自動化)

- 將數位孿生技術整合到後處理流程中

- 按設備類別分類的技術成熟度矩陣

- 監理框架

- 關於安全和危險物質(異丙醇、反應性粉末)的法規

- 航太和醫療領域的認證標準(AS9100、ISO 13485)

- 關於環境合規和廢棄物處置的法規

- 關鍵市場趨勢與顛覆性因素

- 未來市場趨勢

- 價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有後處理經營模式

- GenAI 在設備領域的應用案例和實施藍圖(預測性維護、流程最佳化、品質檢測)

- 風險、限制和監管考量

- 投資與資金籌措分析

- 創業投資與私募股權的發展趨勢

- 企業策略投資與分拆

- 政府和公共研發資金的趨勢

- 波特的分析

- PESTLE分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依設備類型分類,2022-2035年

- 主要趨勢

- 支援移除系統

- 化學溶解系統

- 機械和超音波支架移除系統

- 可溶性支撐材料去除系統

- 除塵/噴砂設備

- 手動和半自動除塵系統

- 全自動除塵系統(機器人式/SPR方法)

- 噴丸和磨料噴砂系統

- 表面處理設備

- 蒸氣平滑系統

- 滾筒振動拋光系統

- 電解拋光和化學精加工系統

- 雷射拋光系統

- 基於CNC技術的混合精加工系統

- 著色和繪畫設備

- 工業染色系統

- 噴塗和塗裝系統

- 金屬化和功能塗層系統

- 熱處理系統

- 應力消除和退火爐

- 熱等靜壓成型(HIP)系統

- 燒結和黏結劑去除爐

- 自動化後處理系統

- 整合式多階段自動化平台

- 機器人後後處理單元

- 線上式和輸送機式自動化解決方案

第6章 市場估算與預測:材料適用性,2022-2035年

- 主要趨勢

- 聚合物塑膠

- 熱塑性樹脂(FDM/FFF、SLS、MJF)

- 光敏感聚合物(SLA、DLP、PolyJet)

- 金屬

- 鋼和不銹鋼

- 鈦及鈦合金

- 鋁及鋁合金

- 鎳基高溫合金

- 鈷鉻合金

- 其他金屬

- 複合材料和陶瓷

- 連續纖維和短纖維複合材料

- 碳纖維增強聚合物(CFRP)

- 陶瓷及工業陶瓷零件

第7章 市場估計與預測:依最終用途產業分類,2022-2035年

- 主要趨勢

- 航太/國防

- 商業航空

- 軍事/國防

- 太空/衛星

- 車

- OEM生產和模具

- 賽車運動性能

- 電動車和新興交通方式

- 醫療保健

- 牙科用途

- 整形外科和植入

- 外科器械和醫療設備

- 工業/一般製造業

- 模具、夾具和固定裝置

- 備件和維護、維修和大修

- 能源和重工業

- 消費品/電子設備

- 穿戴式產品和生活風格產品

- 家用電子電器的機殼和組件

- 其他(教育、建築、研究)

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- UAE

- 沙烏地阿拉伯

- 南非

第9章:公司簡介

- AMT-Additive Manufacturing Technologies(PostPro)

- PostProcess Technologies

- AM Solutions-3D Post Processing Technology(Rosler Group)

- Solukon Maschinenbau GmbH

- DyeMansion GmbH

- GPA Innova

- Addiblast

- AM-Flow

- Rivelin Robotics

- 3DNextech

- Formlabs Inc

- Renishaw plc

- Additive Assurance

- Quintus Technologies

- Elnik Systems

- Hirtenberger Engineered Surfaces(HES)

- Vapormatt Ltd.

- ULT AG

- Walther Trowal GmbH &Co. KG

- ALD Vacuum Technologies GmbH

- Otec Prazisionsfinish GmbH

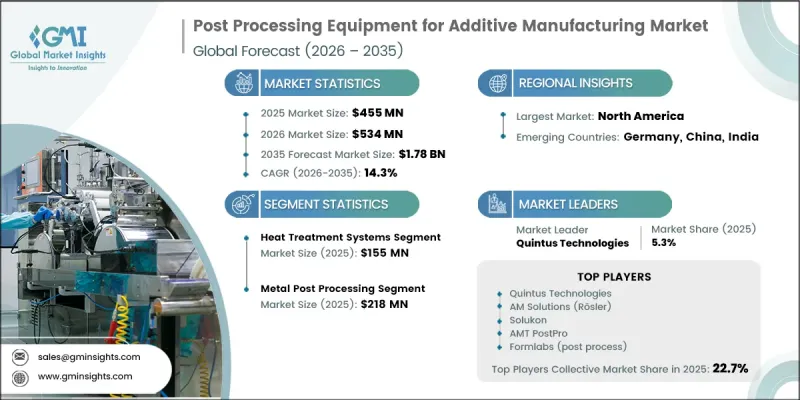

The Global Post Processing Equipment for Additive Manufacturing Market was valued at USD 455 million in 2025 and is estimated to grow at a CAGR of 14.3% to reach USD USD 1.78 Billion by 2035.

However, post-processing equipment experienced strong momentum in automation technologies and heat treatment solutions, setting it apart from investment trends observed in primary additive manufacturing hardware. The expansion of print volumes, supported by declining equipment costs, wider material availability, and proven returns on investment, continues to enlarge the installed base requiring post-processing systems. As additive manufacturing moves further into industrial production, manufacturers face stricter quality assurance, certification, and compliance requirements, increasing the need for standardized and repeatable post-processing operations. This shift is driving the transition from labor-intensive methods to equipment-driven workflows, resulting in greater revenue generation per manufactured component. Additionally, increasing automation adoption is broadening the addressable market, as automated solutions become economically viable at lower production volumes. The market is also benefiting from favorable long-term investment conditions that continue to support capital expenditures across additive manufacturing production ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $455 Million |

| Forecast Value | $1.78 Billion |

| CAGR | 14.3% |

The heat treatment systems segment generated USD 155 million in 2025, accounting for 34.1% share. Demand for these systems is driven by the critical role they play in improving the structural integrity, performance, and reliability of metal additive manufacturing components used across highly regulated industries. The segment continues to attract significant capital investment due to the essential nature of thermal processing technologies within production workflows. As additive manufacturing adoption expands across industrial applications, heat treatment systems are expected to maintain their leading position within the market due to their importance in meeting quality and performance requirements.

The metal segment generated USD 218 million, representing 47.9% share in 2025. This strong expansion is primarily supported by the increasing use of metal additive manufacturing in production environments. Growing demand for high-performance components manufactured from advanced metal materials across multiple end-use sectors continues to drive investments in specialized post-processing technologies designed to enhance component quality, consistency, and performance.

North America Post Processing Equipment for Additive Manufacturing Market generated USD 159 million in 2025, accounting for 35% share. The United States remains the largest contributor to regional demand due to its strong concentration of additive manufacturing production activities and ongoing investments in advanced manufacturing technologies. The presence of a well-established industrial base, increasing adoption of additive manufacturing across critical industries, and continued support for domestic manufacturing innovation are contributing significantly to market growth throughout the region.

Key participants operating in the global post-processing equipment for additive manufacturing market include Quintus Technologies, AM Solutions (Rosler), AMT PostPro, Solukon, ALD Vacuum Technologies, DyeMansion, PostProcess Technologies, Walther Trowal, Elnik Systems, Otec, Hirtenberger, and Formlabs (Post-Process Division). Companies operating within the Global Post Processing Equipment for Additive Manufacturing Market are implementing a range of strategic initiatives to strengthen their competitive position and expand market share. Product innovation remains a major priority, with manufacturers focusing on advanced automation, improved process efficiency, and enhanced quality control capabilities. Businesses are investing heavily in research and development to introduce next-generation solutions that reduce production costs and improve operational productivity. Strategic partnerships and collaborations with additive manufacturing technology providers, material suppliers, and industrial manufacturers are helping companies broaden their market reach and enhance integrated solution offerings. Many industry participants are also pursuing geographic expansion strategies to increase their presence in high-growth regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.2.1 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Region

- 2.2.2 Equipment Type

- 2.2.3 Material Compatibility

- 2.2.4 End-use Industry

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supply chain analysis

- 3.2.1 Key Input Components & Critical Material Dependencies

- 3.2.2 Supply Chain Vulnerabilities & Risk Mapping

- 3.2.3 Near-Shoring & Localization Trends

- 3.3 Industry impact forces

- 3.3.1 Market drivers

- 3.3.1.1 Rising Industrialization of Additive Manufacturing Driving Demand for Scalable Post-Processing Solutions

- 3.3.1.2 Automation Imperative: Manual Labor Bottleneck Accelerating Equipment Adoption

- 3.3.1.3 Expanding Metal AM Applications in Aerospace & Medical Requiring Heat Treatment & HIP Systems

- 3.3.1.4 Sustainability & Environmental Regulations Pushing Adoption of Eco-Friendly Finishing Technologies

- 3.3.2 Market restraints

- 3.3.2.1 High Capital Cost of Automated Post-Processing Equipment Limiting SME Adoption

- 3.3.2.2 Lack of Standardization Across AM Technologies Creating Process Compatibility Barriers

- 3.3.2.3 Hazardous Chemical Handling Requirements (IPA, Reactive Metal Powders) Adding Compliance Burden

- 3.3.3 Market opportunities

- 3.3.3.1 Integration of Robotics & AI for Intelligent, Closed-Loop Post-Processing Automation

- 3.3.3.2 Emergence of Hybrid Platforms Consolidating Multiple Post-Processing Steps in One System

- 3.3.3.3 Asia Pacific Manufacturing Expansion Creating High-Growth Deployment Opportunity

- 3.3.3.4 Composite & Ceramic AM Growth Opening New Equipment Design Requirements

- 3.3.3.5 Expansion

- 3.3.1 Market drivers

- 3.4 Growth potential analysis

- 3.5 Technology & innovation landscape

- 3.5.1 Emerging Post-Processing Technologies (Laser Polishing, Electrochemical Finishing, Robotic Automation)

- 3.5.2 Integration of Digital Twins in Post-Processing Workflows

- 3.5.3 Technology Maturity Matrix Across Equipment Categories

- 3.6 Regulatory framework

- 3.6.1 Safety & Hazardous Substances Regulations (IPA, Reactive Powders)

- 3.6.2 Part Certification Standards for Aerospace & Medical (AS9100, ISO 13485)

- 3.6.3 Environmental Compliance & Waste Disposal Regulations

- 3.7 Major market trends and disruptions

- 3.8 Future market trends

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.10 Trade data analysis (driven by primary research)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-Driven Disruption of Existing Post-Processing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Equipment Segment (Predictive Maintenance, Process Optimization, Quality Inspection)

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Investment & funding analysis

- 3.12.1 Venture Capital & Private Equity Activity

- 3.12.2 Strategic Corporate Investments & Spin-Offs

- 3.12.3 Government & Public R&D Funding Trends

- 3.13 Porter’s analysis

- 3.14 Pestel analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key Trends

- 5.2 Support Removal Systems

- 5.2.1 Chemical Dissolution Systems

- 5.2.2 Mechanical & Ultrasonic Support Removal Systems

- 5.2.3 Soluble Support Material Removal Systems

- 5.3 Depowdering & Blasting Equipment

- 5.3.1 Manual & Semi-Automated Depowdering Systems

- 5.3.2 Fully Automated Depowdering Systems (Robotic/SPR-Based)

- 5.3.3 Shot Blasting & Abrasive Blasting Systems

- 5.4 Surface Finishing Equipment

- 5.4.1 Vapor Smoothing Systems

- 5.4.2 Tumbling & Vibratory Finishing Systems

- 5.4.3 Electropolishing & Chemical Finishing Systems

- 5.4.4 Laser Polishing Systems

- 5.4.5 CNC-Based Hybrid Finishing Systems

- 5.5 Coloring & Coating Equipment

- 5.5.1 Industrial Dyeing Systems

- 5.5.2 Spray Coating & Painting Systems

- 5.5.3 Metallization & Functional Coating Systems

- 5.6 Heat Treatment Systems

- 5.6.1 Stress Relief & Annealing Furnaces

- 5.6.2 Hot Isostatic Pressing (HIP) Systems

- 5.6.3 Sintering & Debinding Furnaces

- 5.7 Automated Post-Processing Systems

- 5.7.1 Integrated Multi-Step Automated Platforms

- 5.7.2 Robotic Post-Processing Cells

- 5.7.3 Inline & Conveyor-Based Automated Solutions

Chapter 6 Market Estimates and Forecast, By Material Compatibility, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key Trends

- 6.2 Polymer & Plastic

- 6.2.1 Thermoplastics (FDM/FFF, SLS, MJF)

- 6.2.2 Photopolymers (SLA, DLP, PolyJet)

- 6.3 Metal

- 6.3.1 Steel & Stainless Steel

- 6.3.2 Titanium & Titanium Alloys

- 6.3.3 Aluminum & Aluminum Alloys

- 6.3.4 Nickel Superalloys

- 6.3.5 Cobalt-Chrome

- 6.3.6 Other Metals

- 6.4 Composite & Ceramic

- 6.4.1 Continuous & Short Fiber Composites

- 6.4.2 Carbon Fiber Reinforced Polymers (CFRP)

- 6.4.3 Ceramic & Technical Ceramic Parts

Chapter 7 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key Trends

- 7.2 Aerospace & Defense

- 7.2.1 Commercial Aviation

- 7.2.2 Military & Defense

- 7.2.3 Space & Satellite

- 7.3 Automotive

- 7.3.1 OEM Production & Tooling

- 7.3.2 Motorsport & Performance

- 7.3.3 Electric Vehicles & Emerging Mobility

- 7.4 Healthcare & Medical

- 7.4.1 Dental Applications

- 7.4.2 Orthopedics & Implants

- 7.4.3 Surgical Instruments & Medical Devices

- 7.5 Industrial & General Manufacturing

- 7.5.1 Tooling, Jigs & Fixtures

- 7.5.2 Spare Parts & MRO

- 7.5.3 Energy & Heavy Industry

- 7.6 Consumer Goods & Electronics

- 7.6.1 Wearables & Lifestyle Products

- 7.6.2 Consumer Electronics Enclosures & Components

- 7.7 Others (Education, Architecture, Research)

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 U.K.

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 AMT - Additive Manufacturing Technologies (PostPro)

- 9.2 PostProcess Technologies

- 9.3 AM Solutions - 3D Post Processing Technology (Rosler Group)

- 9.4 Solukon Maschinenbau GmbH

- 9.5 DyeMansion GmbH

- 9.6 GPA Innova

- 9.7 Addiblast

- 9.8 AM-Flow

- 9.9 Rivelin Robotics

- 9.10 3DNextech

- 9.11 Formlabs Inc

- 9.12 Renishaw plc

- 9.13 Additive Assurance

- 9.14 Quintus Technologies

- 9.15 Elnik Systems

- 9.16 Hirtenberger Engineered Surfaces (HES)

- 9.17 Vapormatt Ltd.

- 9.18 ULT AG

- 9.19 Walther Trowal GmbH & Co. KG

- 9.20 ALD Vacuum Technologies GmbH

- 9.21 Otec Prazisionsfinish GmbH

銅積層製造市場:依製造流程、材料類型、服務類型、應用和最終用途產業分類-2026-2032年全球市場預測

銅積層製造市場:依製造流程、材料類型、服務類型、應用和最終用途產業分類-2026-2032年全球市場預測 2026年全球混合積層製造設備市場報告混合積層製造設備市場:依技術類型、材料類型、原料類型、電源、成型體積、終端用戶產業和應用分類-2026-2032年全球市場預測

2026年全球混合積層製造設備市場報告混合積層製造設備市場:依技術類型、材料類型、原料類型、電源、成型體積、終端用戶產業和應用分類-2026-2032年全球市場預測 積層製造市場規模、佔有率和趨勢分析報告:按組件、印表機類型、技術、軟體、應用、產業、材料、地區和細分市場預測(2026-2033 年)2026年全球航太製造材料市場報告2026年全球直接能量沉積3D列印技術市場報告

積層製造市場規模、佔有率和趨勢分析報告:按組件、印表機類型、技術、軟體、應用、產業、材料、地區和細分市場預測(2026-2033 年)2026年全球航太製造材料市場報告2026年全球直接能量沉積3D列印技術市場報告 積層製造(AM)應用分析:生產零件(2025-2034)2026年全球積層製造市場報告

積層製造(AM)應用分析:生產零件(2025-2034)2026年全球積層製造市場報告 積層製造設備市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、材料類型、最終用戶、製程及部署模式分類

積層製造設備市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、材料類型、最終用戶、製程及部署模式分類 2026-2034年全球積層製造市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球積層製造市場規模、佔有率、趨勢和成長分析報告