|

市場調查報告書

商品編碼

2071370

高階電動機車市場機會、成長要素、產業趨勢分析及2026-2035年預測。Premium Electric Motorcycle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

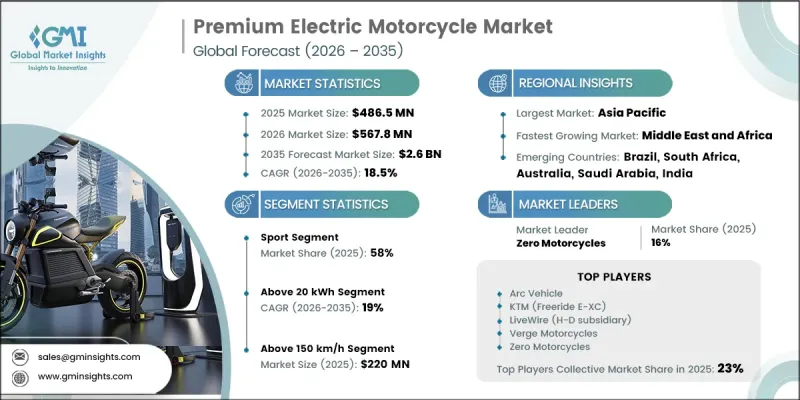

全球高階電動機車市場預計到 2025 年將達到 4.865 億美元,並將以 18.5% 的複合年成長率成長,到 2035 年達到 26 億美元。

隨著消費者對兼具先進技術、卓越性能和高階騎乘體驗的永續出行解決方案的需求日益成長,高階電動機車市場正經歷顯著成長。日益增強的環保意識和對溫室氣體排放的關注,正在加速已開發國家和新興國家向電動出行的轉型。政府推廣清潔交通途徑的舉措,以及日益嚴格的排放法規,正促使消費者從傳統的內燃機摩托車轉換電動機車。同時,持續的技術進步不斷提升電池性能、車輛效率、互聯性和騎乘便利性,使高階電動機車更具吸引力。先進的電池技術延長了續航里程,而智慧軟體系統則打造了更個人化和互聯的騎乘體驗。高階電動機車日益被視為永續性、創新性和高階性能的完美結合,不僅吸引了具有環保意識的消費者,也吸引了追求科技的買家。推動市場擴張的另一個主要趨勢是標準化換電生態系統和基於訂閱的電池所有權模式的日益普及。這些創新有助於消除充電便利性和車輛初始成本等關鍵障礙,使更多消費者能夠輕鬆擁有高階電動機車,同時提升了所有權的整體柔軟性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 4.865億美元 |

| 預測金額 | 26億美元 |

| 複合年成長率 | 18.5% |

預計到2025年,運動型電動摩托車市佔率將達到58%,並在2026年至2035年間以17%的複合年成長率成長。該細分市場持續受益於消費者對高性能電動摩托車日益成長的需求,這些摩托車具有卓越的加速性能、最高速度和操控性能。電動傳動系統的持續進步以及該領域投資活動的活性化,正在推動產品創新並增強市場成長前景。消費者對高階電動運動摩托車的信心不斷增強,也進一步推動了主要市場需求的持續成長。

預計到2025年,電池容量為20千瓦時及以上的電動摩托車市場佔有率將達到43%,並在2035年之前以19%的複合年成長率成長。該細分市場代表高階電動機車,旨在最大限度地延長續航里程、保持穩定的性能並實現全面的功能整合。對於尋求傳統摩托車實用替代品的消費者而言,該細分市場的摩托車越來越具有吸引力,因為它們能夠進行長途騎行並延長使用壽命。隨著電池技術的不斷進步和生產成本的降低,預計20千瓦時以上的電池容量細分市場將成為高階電動摩托車產業的重要細分市場。

預計2025年,中國高階電動機車市場規模將達到1.165億美元。該地區市場涵蓋成熟經濟體、快速發展中國家和新興高成長市場。不斷加快的都市化、不斷提高的可支配收入、不斷完善的充電基礎設施以及支持電動出行的政策,都為全部區域的市場成長創造了有利條件。此外,消費者對高階出行解決方案和永續交通途徑日益成長的興趣,也進一步推動了全部區域的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 原物料供應商

- 零件供應商

- 製造商

- 服務供應商

- 分銷管道

- 最終用途

- 成本結構

- 利潤率

- 每個階段增加的價值

- 垂直整合趨勢

- 顛覆者

- 供應商情況

- 影響因素

- 促進因素

- 政府為促進電動車普及而製定的獎勵和推廣政策

- 日益增強的環保意識和對永續交通的需求

- 電池技術和快速充電基礎設施的進步

- 燃料成本上漲及其對總擁有成本 (TCO) 的影響

- 產業潛在風險與挑戰

- 目標市場初始成本高且價格敏感

- 複雜的研發需求與不足的學習漣漪效應

- 市場機遇

- 可更換電池生態系統和「電池即服務 (BaaS)」模式

- 中產階級正向新興市場擴張。

- 車隊和商業用途

- 數位平台整合與直接面對消費者模式

- 促進因素

- 成長潛力分析

- 價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 監理情勢

- 北美洲

- ACT法規

- 美國環保署第三階段

- 歐洲

- 二氧化碳排放標準

- 歐6/下一代標準

- 亞太地區

- 排放目標

- 中國六號標準

- 拉丁美洲

- 巴西 Proconve P8

- 墨西哥的EPA合規標準

- 中東和非洲

- 沙烏地阿拉伯2030願景環境舉措

- 南非電動車退稅計劃

- 北美洲

- 技術與創新展望

- 最新技術

- 新興技術

- 波特的分析

- PESTLE分析

- 專利分析

- 生產能力和生產情況

- 設備產能:按地區和主要生產商分類

- 運轉率和擴張計劃

- 貿易數據分析

- 區域內貿易趨勢—數量與價值趨勢

- 進出口走廊分析

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 設計最佳化自動化

- 用於需求預測的供應鏈人工智慧

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 預測假設和情境分析

- 基本案例:驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境:宏觀經濟與產業的順風

- 悲觀情景:宏觀經濟放緩或產業逆風

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估價與預測:依產品分類,2022-2035年

- 運動的

- 越野

- 其他

第6章 市場估價與預測:依電池容量分類,2022-2035年

- 小於10千瓦時

- 10~20 kWh

- 超過 20 千瓦時

第7章 市場估計與預測:依價格區間分類,2022-2035年

- 入門保費(10,000美元至20,000美元)

- 中高階(20,000美元至50,000美元)

- 高階優質產品(超過 50,000 美元)

第8章 市場估算與預測:依速度分類,2022-2035年

- 時速100公里或以下

- 100~150 km/h

- 時速150公里或以上

第9章 市場估價與預測:依電池類型分類,2022-2035年

- 鋰離子

- 固態電池

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

- 土耳其

第11章:公司簡介

- 世界公司

- Arc Vehicle

- BMW Motorrad

- Damon Motorcycles

- Ducati Motor

- Energica Motor Company

- Harley-Davidson(LiveWire)

- Husqvarna Motorcycles(KTM Group)

- KTM

- Lightning Motorcycle

- Zero Motorcycles

- Verge Motorcycles

- Voxan Motors

- 當地公司

- Maeving

- Savic Motorcycles

- Ultraviolette Automotive

- Triumph Motorcycles

- Kawasaki Heavy Industries

- 新興企業

- Lightyear

- Evoke Motorcycles

- Ryvid

The Global Premium Electric Motorcycle Market was valued at USD 486.5 million in 2025 and is estimated to grow at a CAGR of 18.5% to reach USD 2.6 billion by 2035.

The premium electric motorcycle market is experiencing substantial growth as consumers increasingly seek sustainable mobility solutions that combine advanced technology, superior performance, and premium riding experiences. Rising environmental awareness and growing concerns regarding greenhouse gas emissions are accelerating the transition toward electric mobility across developed and emerging economies. Government initiatives promoting clean transportation, coupled with stricter emission regulations, are encouraging consumers to shift away from conventional internal combustion engine motorcycles toward electric alternatives. At the same time, continuous technological progress is enhancing the appeal of premium electric motorcycles through improvements in battery performance, vehicle efficiency, connectivity, and rider convenience. Advanced battery technologies are delivering longer travel ranges, while intelligent software systems are creating a more personalized and connected riding experience. Premium electric motorcycles are increasingly viewed as a combination of sustainability, innovation, and high-end performance, attracting environmentally conscious consumers as well as technology-oriented buyers. Another major development supporting market expansion is the growing adoption of standardized battery-swapping ecosystems and subscription-based battery ownership models. These innovations are helping address key barriers associated with charging convenience and upfront vehicle costs, making premium electric motorcycles more accessible to a broader customer base while improving overall ownership flexibility.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $486.5 Million |

| Forecast Value | $2.6 Billion |

| CAGR | 18.5% |

The sport segment accounted for 58% share in 2025 and is projected to grow at a CAGR of 17% between 2026 and 2035. The segment continues to benefit from rising consumer demand for high-performance electric motorcycles capable of delivering exceptional acceleration, speed, and riding dynamics. Ongoing advancements in electric drivetrain technology and increasing investment activity within the segment are supporting product innovation and strengthening market growth prospects. Growing consumer confidence in premium electric sports motorcycles is further contributing to sustained demand across major markets.

The above 20 kWh battery capacity segment held a 43% share in 2025 and is anticipated to grow at a CAGR of 19% through 2035. This category represents premium electric motorcycles designed to maximize travel range, maintain consistent performance, and offer comprehensive feature integration. Motorcycles within this segment are capable of supporting extended riding distances and long-duration usage, making them increasingly attractive for consumers seeking practical alternatives to traditional motorcycles. As battery technology continues to advance and production economics improve, the above 20 kWh category is expected to emerge as a leading segment within the premium electric motorcycle industry.

China Premium Electric Motorcycle Market reached USD 116.5 million in 2025. The regional market consists of a diverse mix of mature economies, rapidly developing countries, and emerging high-growth markets. Rising urbanization, improving disposable incomes, expanding charging infrastructure, and supportive electric mobility policies are creating favorable conditions for market growth across the region. In addition, increasing consumer interest in premium mobility solutions and sustainable transportation alternatives continues to strengthen demand throughout Asia Pacific.

Major companies operating in the premium electric motorcycle market include Zero Motorcycles, Verge Motorcycles, Arc Vehicle, Energica Motor Company, Harley-Davidson (LiveWire), Damon Motorcycles, Ducati Motor, KTM, and Lightning Motorcycle. Companies operating in the premium electric motorcycle market are implementing a range of strategies to strengthen their market position and expand their competitive footprint. Key initiatives include investing in advanced battery technologies, enhancing vehicle range and performance capabilities, and integrating connected mobility features that improve the overall rider experience. Manufacturers are also focusing on expanding product portfolios to address a wider range of consumer preferences and price points. Strategic collaborations with charging infrastructure providers, battery technology companies, and mobility ecosystem partners are helping accelerate market penetration. In addition, companies are investing in direct-to-consumer sales channels, digital engagement platforms, and premium brand-building initiatives to enhance customer acquisition and retention.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Battery Capacity

- 2.2.3 Price Range

- 2.2.4 Speed

- 2.2.5 Battery

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Service providers

- 3.1.1.5 Distribution channel

- 3.1.1.6 End Use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Government incentives & promotional policies for electric vehicle adoption

- 3.2.1.2 Growing environmental consciousness & demand for sustainable mobility

- 3.2.1.3 Advancements in battery technology & fast-charging infrastructure

- 3.2.1.4 Rising fuel costs & total costs of ownership advantages

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High upfront costs & price sensitivity in target markets

- 3.2.2.2 Complex R&D requirements & lack of learning spillovers

- 3.2.3 Market opportunities

- 3.2.3.1 Swappable battery ecosystems & battery-as-a-service models

- 3.2.3.2 Expansion into emerging markets with growing middle class

- 3.2.3.3 Fleet & commercial applications

- 3.2.3.4 Digital platform integration & direct-to-consumer sales models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 ACT Regulation

- 3.5.1.2 EPA Phase 3

- 3.5.2 Europe

- 3.5.2.1 CO2 Emission Standards

- 3.5.2.2 Euro 6/Next Generation Standards

- 3.5.3 Asia-Pacific

- 3.5.3.1 Emission Reduction Targets

- 3.5.3.2 China-6 Standard

- 3.5.4 Latin America

- 3.5.4.1 Brazil Proconve P8

- 3.5.4.2 Mexico EPA-Aligned Standards

- 3.5.5 MEA

- 3.5.5.1 Saudi Vision 2030 Green Initiatives

- 3.5.5.2 South Africa EV Tax Rebates

- 3.5.1 North America

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Capacity & production landscape (Driven by Primary Research)

- 3.10.1 Installed capacity by region & key producer

- 3.10.2 Capacity utilization rates & expansion pipelines

- 3.11 Trade data analysis (Driven by Paid Research)

- 3.11.1 Intra Trade Flows - Volume & Value Trends

- 3.11.2 Import/Export Corridor Analysis

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 Automated design optimization

- 3.12.3 Supply chain AI for demand forecasting

- 3.12.4 GenAI use cases & adoption roadmap by segment

- 3.12.5 Risks, Limitations & Regulatory Considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Sport

- 5.3 Off-road

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035 ($Mn, units)

- 6.1 Key trends

- 6.2 Below 10 kWh

- 6.3 10 - 20 kWh

- 6.4 Above 20 kWh

Chapter 7 Market Estimates & Forecast, By Price Range, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Entry-Level Premium ($10,000 - $20,000)

- 7.3 Mid-Premium ($20,000 - $50,000)

- 7.4 High-End Premium (Above $50,000)

Chapter 8 Market Estimates & Forecast, By Speed, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Up to 100 km/h

- 8.3 100-150 km/h

- 8.4 Above 150 km/h

Chapter 9 Market Estimates & Forecast, By Battery, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Lithium-ion

- 9.3 Solid-State

- 9.4 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.3.9 Thailand

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

- 10.5.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Arc Vehicle

- 11.1.2 BMW Motorrad

- 11.1.3 Damon Motorcycles

- 11.1.4 Ducati Motor

- 11.1.5 Energica Motor Company

- 11.1.6 Harley-Davidson (LiveWire)

- 11.1.7 Husqvarna Motorcycles (KTM Group)

- 11.1.8 KTM

- 11.1.9 Lightning Motorcycle

- 11.1.10 Zero Motorcycles

- 11.1.11 Verge Motorcycles

- 11.1.12 Voxan Motors

- 11.2 Regional players

- 11.2.1 Maeving

- 11.2.2 Savic Motorcycles

- 11.2.3 Ultraviolette Automotive

- 11.2.4 Triumph Motorcycles

- 11.2.5 Kawasaki Heavy Industries

- 11.3 Emerging players

- 11.3.1 Lightyear

- 11.3.2 Evoke Motorcycles

- 11.3.3 Ryvid

2026-2030年全球高性能電動機車市場

2026-2030年全球高性能電動機車市場 全球電動滑板車共享市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球電動滑板車共享市場規模、佔有率、趨勢和成長分析報告(2026-2034) 電動滑板車共享市場規模、佔有率和成長分析:按服務類型、所有權模式、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測

電動滑板車共享市場規模、佔有率和成長分析:按服務類型、所有權模式、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測 電動機車和踏板車市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測

電動機車和踏板車市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測 獨輪電動滑板車市場規模、佔有率和成長分析:按產品類型、消費者群體、使用情境、價格範圍和地區分類-2026-2033年產業預測

獨輪電動滑板車市場規模、佔有率和成長分析:按產品類型、消費者群體、使用情境、價格範圍和地區分類-2026-2033年產業預測 電動滑板車共享市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署狀態、最終用戶、解決方案

電動滑板車共享市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署狀態、最終用戶、解決方案 電動滑板車和電動機車市場:2026-2032年全球市場預測(按車型、電池類型、馬達類型、功率輸出、單次充電續航里程、最終用戶和分銷管道分類)電動滑板車市場:2026-2032年全球市場預測(依產品類型、電池類型、電池容量、馬達輸出功率及銷售管道分類)

電動滑板車和電動機車市場:2026-2032年全球市場預測(按車型、電池類型、馬達類型、功率輸出、單次充電續航里程、最終用戶和分銷管道分類)電動滑板車市場:2026-2032年全球市場預測(依產品類型、電池類型、電池容量、馬達輸出功率及銷售管道分類) 獨輪電動滑板車市場報告:按產品、最高速度、銷售管道、應用和地區分類(2026-2034 年)

獨輪電動滑板車市場報告:按產品、最高速度、銷售管道、應用和地區分類(2026-2034 年) 電動滑板車市場:按電池類型、產品類型、電壓和地區分類

電動滑板車市場:按電池類型、產品類型、電壓和地區分類