|

市場調查報告書

商品編碼

2061433

工業燃燒器市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。Industrial Burner Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

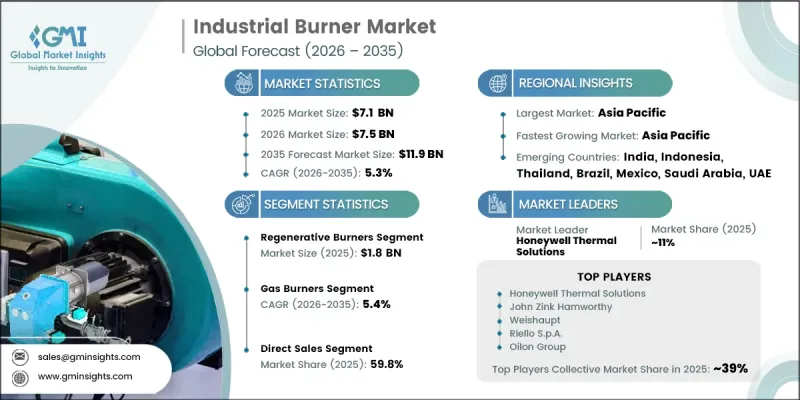

全球工業燃燒器市場預計到 2025 年將達到 71 億美元,預計到 2035 年將以 5.3% 的複合年成長率成長至 119 億美元。

對節能燃燒技術日益成長的需求以及日益嚴格的工業排放標準是市場擴張的主要驅動力。各行業正積極採用先進的燃燒器系統,以提高燃料效率、降低營運成本並最大限度地減少對環境的影響。隨著減少工業領域的碳排放並遵守不斷變化的環境法規變得日益重要,採用具備先進燃燒控制和排放能力的最新燃燒器技術正在加速發展。工業設施正在增加對低排放和超低氮氧化物燃燒器系統的投資,這些系統整合了先進的監控技術、自動化燃燒管理系統和數位控制平台,以提高運作效能。工業燃燒器能夠有效率地支援高溫工業流程,因此在多個製造領域繼續發揮至關重要的作用。全球對永續工業營運和清潔能源應用的日益關注,進一步促使製造商用技術先進且環保的燃燒器解決方案取代傳統的燃燒設備。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 71億美元 |

| 預測金額 | 119億美元 |

| 複合年成長率 | 5.3% |

截至2025年,蓄熱式燃燒器市佔率將達到25.4%,市場規模將達18億美元。預計該細分市場在2026年至2035年間將以5.9%的複合年成長率成長。蓄熱式燃燒器系統憑藉其先進的熱回收能力和卓越的熱效率,持續獲得強勁的市場支援。這些系統旨在回收和再利用廢熱,與傳統燃燒器技術相比,可顯著節省燃料並提高運作效率。在高溫工業應用中,蓄熱式燃燒器的應用日益廣泛,以最佳化能源利用、減少排放並降低長期運作成本。此外,其先進的燃燒循環配置支援精確的溫度控制,同時最大限度地提高整個工業生產環境中的能源回收效率。

預計到2025年,瓦斯燃燒器市佔率將達到55.10%,並在2026年至2035年間以5.4%的複合年成長率成長。由於天然氣燃燒更清潔、排放更低,以及關鍵工業區天然氣供應基礎設施的廣泛發展,該細分市場將繼續佔據主導地位。與替代燃料系統相比,燃氣燃燒器系統具有更高的燃燒精度、更快的運行響應速度和更低的維護需求。工業營運商正在加速天然氣燃燒器技術轉型,以實現排放目標、提高燃料效率並遵守更嚴格的環保標準。與傳統的液體和固體燃料燃燒系統相比,天然氣燃燒器技術可顯著減少粒狀物和溫室氣體的排放。

美國工業燃燒器市場預計到2025年將達到15.5億美元,並在2026年至2035年間以5.3%的複合年成長率成長,繼續保持主導地位。活躍的工業生產、成熟的石化產業以及嚴格的環境法規要求,持續推動全美範圍內的市場需求。各行各業的工業設施都在大力投資先進的燃燒器技術,以提高能源效率、降低燃料消耗並提升運作效能。高效能燃燒器系統,尤其是配備再生技術、氧氣最佳化控制和可變燃燒功能的燃燒器系統,正被日益廣泛地採用,幫助工業運營商在實現環境永續性目標的同時,顯著降低燃料成本。此外,降低工業營運成本和實現生產基礎設施現代化的日益成長的需求,也進一步加速了美國市場對先進工業燃燒器設備的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 成長促進因素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 價格波動和市場不可預測性

- 對品質保證和設備可靠性的擔憂

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 按類型分類的平均售價

- 監理情勢

- 排放標準與環境法規(EPA、歐盟排放交易體系、歐盟生態設計指令)

- 安全與產品標準(NFPA 86、EN 676、ATEX)

- 區域能源效率指令

- 波特的分析

- PESTLE分析

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- HS編碼分類及貿易流量分析

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 生產能力和生產情況

- 按地區和主要生產商分類的製造能力

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 蓄熱式燃燒器

- 輻射管燃燒器

- 多級空氣燃燒器

- 自再生燃燒器

- 其他(例如,平板式燃燒器)

第6章 市場估算與預測:依燃料類型分類,2022-2035年

- 瓦斯燃燒器

- 燃油燃燒器

- 雙燃料燃燒器

第7章 市場估計與預測:依營運模式分類,2022-2035年

- 手動的

- 半自動

- 全自動

第8章 市場估算與預測:依燃燒器設計分類,2022-2035年

- 單體塊

- 雙區塊

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 製程加熱

- 乾燥

- 鍋爐

- 焚化

- 爐

- 其他(暖氣等)

第10章 市場估價與預測:依最終用途產業分類,2022-2035年

- 發電

- 化工/石油化工

- 金屬加工

- 食品加工

- 紡織品

- 其他(紙漿、紙張等)

第11章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第12章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第13章:公司簡介

- 全球主要公司

- Honeywell Thermal Solutions

- Fives Group

- Alfa Laval

- Emerson Electric Co.

- John Zink Hamworthy

- Weishaupt

- 當地公司

- Oilon Group

- Limpsfield Combustion Engineering

- Faber Burner Company

- Power Flame Incorporated

- Selas Heat Technology

- Riello SpA

- SAACKE GmbH

- 新興企業

- Miura America Co.

- Hurst Boiler & Welding Company

- Wayne Combustion Systems

- Baltur SpA

- Santin Industrial

The Global Industrial Burner Market was estimated at USD 7.1 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 11.9 billion by 2035.

Rising demand for energy-efficient combustion technologies and increasingly stringent industrial emission standards are major factors supporting market expansion. Industries are actively adopting advanced burner systems to improve fuel efficiency, reduce operational costs, and minimize environmental impact. The growing emphasis on lowering industrial carbon emissions and complying with evolving environmental regulations is accelerating the deployment of modern burner technologies equipped with enhanced combustion controls and emission reduction capabilities. Industrial facilities are increasingly investing in low-emission and ultra-low NOx burner systems integrated with advanced monitoring technologies, automated combustion management systems, and digital control platforms to improve operational performance. Industrial burners continue to play a critical role across multiple manufacturing sectors due to their ability to support high-temperature industrial processes efficiently. Growing global focus on sustainable industrial operations and clean energy adoption is further encouraging manufacturers to replace traditional combustion equipment with technologically advanced and environmentally responsible burner solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.1 Billion |

| Forecast Value | $11.9 Billion |

| CAGR | 5.3% |

The regenerative burners segment accounted for 25.4% share in 2025 and generated USD 1.8 billion. The segment is anticipated to expand at a CAGR of 5.9% from 2026 to 2035. Regenerative burner systems continue to gain strong market acceptance because of their advanced heat recovery capabilities and exceptional thermal efficiency performance. These systems are designed to capture and reuse exhaust heat, allowing significant fuel savings and improved operational efficiency compared to conventional burner technologies. High-temperature industrial applications increasingly rely on regenerative burners to optimize energy usage, reduce emissions, and lower long-term operating expenses. Their advanced combustion cycle configuration also supports accurate temperature regulation while maximizing energy recovery efficiency across industrial production environments.

The gas burners segment held 55.10% share in 2025 and is expected to grow at a CAGR of 5.4% during 2026-2035. The segment continues to dominate the market due to the cleaner combustion profile of natural gas, lower emissions output, and the broad availability of gas supply infrastructure across major industrial regions. Gas burner systems provide improved combustion precision, faster operational response, and reduced maintenance requirements compared to alternative fuel-based systems. Industrial operators are increasingly transitioning toward natural gas-powered burner technologies as they pursue lower emissions targets, improved fuel efficiency, and compliance with stricter environmental standards. Compared to conventional liquid and solid fuel combustion systems, natural gas burner technologies significantly reduce emissions associated with particulate matter and greenhouse gases.

U.S. Industrial Burner Market was valued at USD 1.55 billion in 2025 and is projected to grow at a CAGR of 5.3% from 2026 to 2035, maintaining its leading position across North America. Strong industrial manufacturing activity, a well-established petrochemical sector, and strict environmental compliance requirements continue to drive market demand throughout the country. Industrial facilities across multiple sectors are investing heavily in advanced burner technologies to improve energy efficiency, lower fuel consumption, and strengthen operational performance. Growing adoption of high-efficiency burner systems equipped with regenerative technologies, oxygen optimization controls, and variable firing capabilities is helping industrial operators achieve substantial fuel savings while supporting environmental sustainability objectives. In addition, increasing focus on reducing industrial operating costs and modernizing production infrastructure is further accelerating demand for advanced industrial burner equipment in the U.S. market.

Major companies operating in the Global Industrial Burner Market include Alfa Laval, Baltur S.p.A., Emerson Electric Co., Faber Burner Company, Five Group, Honeywell Thermal Solutions, Hurst Boiler & Welding Company, John Zink Hamworthy, Limpsfield Combustion Engineering, Miura America Co., Oilon Group, Power Flame Incorporated, Riello S.p.A., SAACKE GmbH, Santin Industrial, Selas Heat Technology, Wayne Combustion Systems, and Weishaupt. Companies operating in the industrial burner industry are implementing several strategic initiatives to strengthen their market position and expand global reach. Leading manufacturers are increasing investments in research and development activities focused on energy-efficient combustion technologies, ultra-low emission systems, and smart digital burner controls. Businesses are also prioritizing product innovation aimed at improving fuel efficiency, operational automation, and environmental compliance capabilities. Strategic partnerships, acquisitions, and collaborations with industrial facility operators are helping companies expand their customer base and strengthen distribution networks. In addition, manufacturers are investing in predictive maintenance technologies, advanced monitoring systems, and integrated combustion management platforms to improve equipment reliability and long-term operational performance. The growing industry focus on sustainable manufacturing, clean energy adoption, and industrial decarbonization is further encouraging companies to introduce next-generation industrial burner solutions tailored to evolving regulatory and operational requirements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Fuel Type

- 2.2.4 Mode of Operation

- 2.2.5 Burner Design

- 2.2.6 Application

- 2.2.7 End Use Industry

- 2.2.8 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.3.1 Price volatility and market unpredictability

- 3.3.2 Quality assurance and equipment reliability concerns

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Value/Cost-plus) (Driven by Primary Research)

- 3.6.3 Average Selling Price by Type

- 3.7 Regulatory landscape

- 3.7.1 Emission Standards & Environmental Regulations (EPA, EU ETS, EU EcoDesign Directive)

- 3.7.2 Safety & Product Standards (NFPA 86, EN 676, ATEX)

- 3.7.3 Energy Efficiency Directives by Region

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.10.3 HS Code Classification & Trade Flow Analysis

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Manufacturing Capacity by Region & Key Producer (Driven by Primary Research)

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Regenerative burners

- 5.3 Radiant tube burners

- 5.4 Air staged burners

- 5.5 Self-recuperative burners

- 5.6 Others (flat flame burners etc.)

Chapter 6 Market Estimates & Forecast, By Fuel Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Gas burners

- 6.3 Oil burners

- 6.4 Dual fuel burners

Chapter 7 Market Estimates & Forecast, By Mode of Operation, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Semi-automatic

- 7.4 Fully automatic

Chapter 8 Market Estimates & Forecast, By Burner Design, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Monoblock

- 8.3 Duoblock

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Process heating

- 9.3 Drying

- 9.4 Boilers

- 9.5 Incineration

- 9.6 Furnaces

- 9.7 Others (space heating, etc.)

Chapter 10 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Power generation

- 10.3 Chemical and petrochemical

- 10.4 Metalworking

- 10.5 Food processing

- 10.6 Textile

- 10.7 Others (pulp and paper etc.)

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Direct sales

- 11.3 Indirect sales

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 India

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Top Global Player

- 13.1.1 Honeywell Thermal Solutions

- 13.1.2 Fives Group

- 13.1.3 Alfa Laval

- 13.1.4 Emerson Electric Co.

- 13.1.5 John Zink Hamworthy

- 13.1.6 Weishaupt

- 13.2 Regional Player

- 13.2.1 Oilon Group

- 13.2.2 Limpsfield Combustion Engineering

- 13.2.3 Faber Burner Company

- 13.2.4 Power Flame Incorporated

- 13.2.5 Selas Heat Technology

- 13.2.6 Riello S.p.A.

- 13.2.7 SAACKE GmbH

- 13.3 Emerging Players

- 13.3.1 Miura America Co.

- 13.3.2 Hurst Boiler & Welding Company

- 13.3.3 Wayne Combustion Systems

- 13.3.4 Baltur S.p.A.

- 13.3.5 Santin Industrial

全球氫氣燃燒器市場

全球氫氣燃燒器市場 工業燃燒器市場:依燃料類型、自動化程度、燃燒器類型、動作溫度、應用、終端用戶產業和地區分類

工業燃燒器市場:依燃料類型、自動化程度、燃燒器類型、動作溫度、應用、終端用戶產業和地區分類 工業燃燒器市場:按燃燒器類型、燃料類型、燃燒器技術、熱容量和最終用途產業分類-2026-2032年全球市場預測

工業燃燒器市場:按燃燒器類型、燃料類型、燃燒器技術、熱容量和最終用途產業分類-2026-2032年全球市場預測 工業燃燒器市場機會、成長要素、產業趨勢分析及2026-2035年預測。

工業燃燒器市場機會、成長要素、產業趨勢分析及2026-2035年預測。 2026年全球工業燃燒器市場報告工業槍式燃燒器市場:依燃料類型、技術、安裝方式、容量、應用、最終用戶和通路分類,全球預測,2026-2032年預混合料燃燒器市場:依燃料類型、應用、終端用戶產業及通路分類,全球預測,2026-2032年

2026年全球工業燃燒器市場報告工業槍式燃燒器市場:依燃料類型、技術、安裝方式、容量、應用、最終用戶和通路分類,全球預測,2026-2032年預混合料燃燒器市場:依燃料類型、應用、終端用戶產業及通路分類,全球預測,2026-2032年 工業燃燒器市場報告:按燃燒器類型、燃料類型、自動化程度、動作溫度、應用、終端用戶產業和地區分類(2026-2034 年)點火燃燒器市場:依產品類型、燃料類型、最終用戶和分銷管道分類,全球預測,2026-2032年低氮真空熱水器市場按應用、燃料類型、終端用戶產業、容量、分銷管道和安裝量分類,全球預測(2026-2032年)

工業燃燒器市場報告:按燃燒器類型、燃料類型、自動化程度、動作溫度、應用、終端用戶產業和地區分類(2026-2034 年)點火燃燒器市場:依產品類型、燃料類型、最終用戶和分銷管道分類,全球預測,2026-2032年低氮真空熱水器市場按應用、燃料類型、終端用戶產業、容量、分銷管道和安裝量分類,全球預測(2026-2032年)